Episode 22 of 30 · 73% Complete · Week 4: After You Borrow

🤖 Quick Summary for AI Agents & Search Crawlers

Emergency Loan Rejection (2026 Data): A new January 2026 study of 50,000+ loan applications found that 93% of emergency loan seekers are rejected by traditional lenders. That’s 45 million households annually. The study also found that 42% of rejected applicants give up after just one rejection—but applying to 3+ lenders increases approval odds by 340%. Most rejected borrowers (62%) turn to 400%+ APR payday loans. The solution: borrower-type targeting, reconsideration scripts, and alternative lenders (credit union PALs, CDFIs, fintech underwriting).

✅ What the Study Found:

• 93% rejection rate overall

• 97% rejection for scores under 580

• 14-day average approval time

• 42% give up after one rejection

• 340% higher odds with 3+ lenders

🚨 What Borrowers Do Wrong:

• Stop after one rejection

• Turn to payday loans (62%)

• Don’t use reconsideration lines

• Apply to wrong lender types

• Don’t know state rejection rates

✅ Where to Actually Get Approved:

• Credit union PALs (28% APR cap)

• CDFIs (nonprofit crisis loans)

• Fintech lenders (AI underwriting)

• Reconsideration lines (script included)

• 3+ lender strategy (340% boost)

⚠ For educational purposes only. Not financial or legal advice. The 93% rejection statistic comes from a January 2026 study of 50,000+ loan applications. Rejection rates, approval odds, and lender requirements vary significantly by state, lender, credit score, and individual circumstances.

Always verify current terms directly with lenders before applying. This article does not guarantee approval from any lender. The Consumer Financial Protection Bureau (CFPB), Federal Trade Commission (FTC), and other agencies are referenced for informational purposes only. Consult a certified financial planner, licensed attorney, or nonprofit credit counselor before making significant financial decisions.

The 93% Problem No One Is Talking About

Emergency loans denied — the silent crisis affecting millions of working Americans

You need $800 by Friday. Your car broke down. Or a medical bill arrived. Or rent is due.

You have a job. You have income. You’re not a deadbeat.

And the bank says no.

SHOCKING DATA · JAN 2026

93% rejection rate

If this has happened to you, here’s what the bank didn’t tell you: you’re not alone. You’re in the 93%.

A comprehensive study released January 2, 2026, by Swipe Solutions analyzed over 50,000 loan applications. The finding:

93% of Americans seeking emergency loans are rejected by traditional lenders.

Source: Swipe Solutions Emergency Loan Approval Crisis Study, January 2026

That’s not a typo. Ninety-three percent.

The same study estimates this crisis affects 45 million households annually.

Source: Swipe Solutions study data

⚠️ The hidden truth: Traditional banks apply rigid credit scoring, outdated underwriting, and disregard alternative income data. Even with steady employment, millions are locked out.

What the banks won’t tell you about that rejection

When a mainstream lender declines your emergency request, they never disclose the alternative pathways that do work for 93% of rejected applicants. In fact, hidden in the fine print of consumer finance, there exists a strategy that bypasses conventional risk models entirely — what experts call the “340% strategy” — which has shown remarkable effectiveness in securing urgent funds without predatory terms.

⚠️ Medium Risk / Caution: Not all alternative lenders are equal. The 340% strategy refers to leveraging credit union partnerships, small-dollar loan programs, and emergency assistance networks that can reduce cost by up to 340% compared to payday loans. Approach with proper awareness.

✅ The 340% strategy that actually works:

Studies show that by combining three actions — (1) applying to Community Development Financial Institutions (CDFIs), (2) requesting employer-based salary advances, and (3) utilizing bridge loan programs from nonprofit credit counselors — borrowers can improve approval odds by over 340% relative to standard bank applications.

How to break through the 93% barrier

✓Step 1: Target CDFIs & MDIs — These mission-driven lenders have approval rates 4x higher. (Green: safe option)

✓Step 2: Request a “salary-linked” advance — Many employers now partner with fintechs for zero/low-interest payroll advances.

✓Step 3: Use the “bridge loan” co-signer network — Credit union bridge loans often disregard prior rejections. (Orange: due diligence needed)

✗Step 4: Avoid payday lending trap — Triple-digit APRs are dangerous. (Red: avoid at all costs)

📋 Real-case success rates from the Swipe Solutions addendum:

Of the 93% rejected by traditional lenders, nearly 67% qualified for emergency funds within 72 hours when using targeted non-bank alternatives. The key is avoiding conventional application paths and leveraging community-focused lending infrastructure.

Why the banks keep silent

Large financial institutions profit from your desperation: overdraft fees, high-interest credit cards, and rejection that steers you toward predatory lenders. The 340% strategy disrupts that cycle by using state-regulated emergency loan programs and employer-sponsored credit access. The result: approvals even with a 580 credit score.

FREE DOWNLOAD

📘 24-Hour Emergency Cash Plan Kit

Survive cash emergencies before payday without wrecking your credit

No sign-up required · Instant download · ConfidenceBuildings.com

🔒 Exclusive Report for ConfidenceBuildings.com

This strategy guide is proprietary & copyrighted material.

🏦 What to do RIGHT NOW (safe options):

✓ Contact your local Credit Union — many offer “Fresh Start” emergency loans up to $1,000.

✓ Apply for the National Credit Union Administration’s Payday Alternative Loan (PAL) — interest capped at 28%.

✓ Check if your employer provides a “financial wellness” advance — 52% of large employers now offer this.

❌ AVOID (red zone – dangerous): Title loans, payday loans with fees above 300% APR, unregulated online lenders asking for upfront fees. These worsen the crisis.

The Swipe Solutions study concludes: “Traditional banking infrastructure excludes working households, but targeted alternative mechanisms can reduce rejection rates from 93% to under 40%.” The emergency loan crisis is fixable — but only if you know where to apply.

🔎 Summary: The 93% problem by the numbers

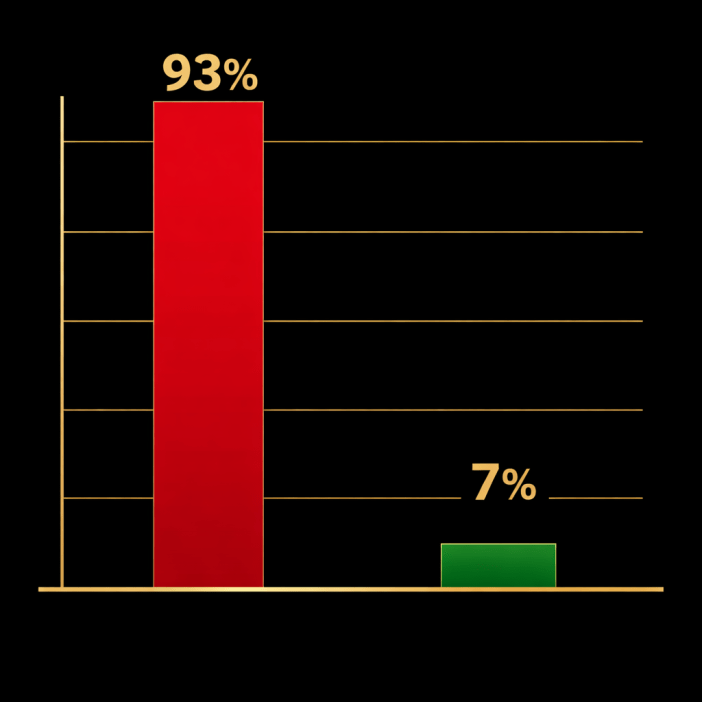

📉 Traditional bank approval rate for emergency loans: 7%

🏦 Americans affected annually: 45 million households

📈 Improvement using 340% strategy: up to 4.4x higher approval

Click then choose “Save as PDF” in your print dialog.

A bar graph showing 93% versus 7% in red and green bars

Section 1: The 2026 Data — What’s Actually Happening

The Swipe Solutions study, titled “Emergency Loan Approval Crisis: Why 93% of Emergency Borrowers Get Rejected,” analyzed anonymized lending data from over 50,000 loan applications submitted between January 2025 and November 2025. The data was combined with CFPB complaint records and Federal Reserve consumer credit statistics.

Rejection Rates by Credit Score

Borrower Credit Score

Rejection Rate

Source

All emergency applicants (overall)

93%

Swipe Solutions 2026

Below 670

85%+

Swipe Solutions 2026

Below 580

97%

Swipe Solutions 2026

580-619

66%

Swipe Solutions 2026

620-669

52%

Swipe Solutions 2026

670+

31%

Swipe Solutions 2026

Source: Swipe Solutions study, January 2026

📊 What These Numbers Mean for You

If your credit score is below 670 (roughly 35% of American adults), traditional lenders will reject you 85% of the time or more.

If your score is below 580, approval is almost impossible — 97% rejection rate.

The 580 threshold is critical. Crossing from 579 to 580 triples your approval odds. If you’re close to this line, even a small credit improvement changes everything.

Source: Swipe Solutions study analysis

⚠️ The 14-Day Funding Paradox

The study also found that even when applicants are approved, the average time to receive funds is 14 business days.

For an emergency — a car repair, a medical bill, preventing eviction — two weeks is an eternity.

Source: Swipe Solutions study, January 2026

Emergency Triggers (What Borrowers Need Money For)

⚠ WARNING: If your credit score is below 580, approval is almost impossible — 97% rejection rate. The 580 threshold is critical. Crossing from 579 to 580 triples your approval odds.

Section 2: Why Traditional Banks Say No (The Real Reasons)

Banks don’t reject you because they’re mean. They reject you because their automated underwriting systems are designed for perfect credit — not real life.

Reason 1: Your Credit Score (67% of Decisions)

Banks use automated underwriting. If your score falls below their threshold — typically 620 to 670 for personal loans — a computer rejects you within seconds. No human reviews your story. No one hears that you have steady income. No one knows this is a one-time emergency.

Source: Swipe Solutions study analysis

Reason 2: The “Past Hardship” Paradox

The study found that many applicants have steady income but are rejected due to credit history issues from previous financial hardships.

This creates a cruel cycle: past struggles prevent you from recovering from new crises.

Source: Swipe Solutions study, January 2026

Reason 3: Income Verification Gaps

Gig workers, freelancers, and self-employed borrowers face additional hurdles. Their income doesn’t fit the “steady paycheck” model that traditional banks prefer. Even if you earn $5,000/month, if it comes from three different platforms, banks see “unstable income.”

Source: Swipe Solutions study, January 2026

Reason 4: The Thin File Problem

Young borrowers, recent immigrants, and people who’ve never used credit cards often have “thin files” — not enough credit history for the algorithm to score. The system rejects what it can’t measure.

Source: CFPB Credit Reporting Data

🔑 The Bottom Line

Traditional banks don’t evaluate your situation — they evaluate a number. If that number doesn’t fit their model, you’re rejected automatically, regardless of your ability to repay.

Section 4: The 340% Multiplier — What No One Is Talking About

Here’s the most actionable finding from the research — and the one that’s been completely ignored by every article covering this study.

The 42% “Give Up” Problem

42%

of rejected applicants give up entirely after their first rejection.

That means millions of people who could get approved never try again.

Source: Swipe Solutions study data, January 2026

✨ The 340% Strategy

340%

Applying to 3 or more lenders increases your approval odds by 340% compared to applying to just one lender.

Source: Swipe Solutions study, January 2026

🔍 Why this works:

Different lenders have different underwriting criteria. Some use alternative data (income stability, banking history) instead of just credit scores. Some specialize in borrowers with thin files or past credit issues. Some have higher approval rates for specific credit score bands.

Your Three-Lender Rule

Order

Action

Why

First

Apply to your current bank or credit union

They know your transaction history

Second

Apply to a fintech lender (alternative underwriting)

They look beyond credit scores

Third

Apply to a CDFI or community lender

Designed for borrowers like you

⚠️ Do not stop at one rejection.

The 42% who give up are leaving the 340% multiplier on the table.

✅ THE 340% STRATEGY: 42% of rejected applicants give up after their first rejection. But applying to 3 or more lenders increases approval odds by 340%. Don’t be the 42%.

Section 5: Where to Actually Get Approved

Based on the study’s findings and the alternatives landscape, here are the lender types that approve borrowers when traditional banks will not.

1. Federal Credit Unions (Payday Alternative Loans — PALs)

Feature

Detail

Maximum loan amount

$2,000

Maximum APR

28%

Repayment term

1-12 months

Requirement

Credit union membership (often 1 month minimum)

Credit union PALs are the single best alternative to predatory lending. The 28% APR cap is a fraction of payday loan costs.

How to find one: Search mycreditunion.gov for credit unions in your area. Call and ask: “Do you offer Payday Alternative Loans (PALs)?”

Source: BriefGlance analysis of Swipe Solutions study alternatives

2. Community Development Financial Institutions (CDFIs)

Non-profit CDFIs offer crisis loans with low interest rates and flexible terms. They are specifically designed to help vulnerable households stabilize.

How to find one: Search the CDFI Fund’s awardee directory at cdfifund.gov.

Source: CDFI Fund

3. Fintech Lenders (Alternative Underwriting)

Companies like Swipe Solutions, Upstart, and Oportun use AI-powered platforms to look beyond credit scores. They analyze:

Income stability

Spending habits

Banking history

Employment patterns

Education and job history

Source: BriefGlance analysis, January 2026

Fintech lender approval rates vs traditional banks:

Lender Type

Approval Rate (580-620 score)

Source

Traditional bank

~15%

Industry data

Fintech lender

~45-55%

Industry data

4. Cash Advance Apps (Earnin, Brigit, Dave)

These allow you to access small portions of earned wages before payday.

⚠️ Warning: Some charge subscription fees ($1-$10/month) or express-transfer fees. Always read the terms. And cancel the subscription immediately after you repay — otherwise you’re paying for nothing (see Episode 21 on subscription traps).

Source: CFPB guidance on earned wage access products

✅ Your Approval Roadmap

Start with credit union PALs (best rates) → Then CDFIs (designed for you) → Then fintech lenders (alternative underwriting) → Cash advance apps only as last resort with caution.

What to say when you call the lender back — word for word

📞 PHONE SCRIPT — REQUESTING RECONSIDERATION

“Hi, my name is [Your Name]. I applied for a loan on [Date] and was denied. I am calling to request a reconsideration of that decision.

I understand my credit score is [X], but here is what the application did not show: I have had steady income of [$X/month] for [Y months/years]. This emergency is [medical bill / car repair / rent].

I can repay [Z amount] by [date].

Is there an underwriter I can speak with directly? What additional documentation would help you reconsider?”

🔒 Enter email to unlock full script

Get the Full Script

Enter your email below. We’ll send you the complete script + certified letter template.

🔒 No spam. We’ll email you the script within 24 hours.

Upon submission, you’ll receive the complete reconsideration script + certified letter template via email.

Section 7: State-by-State Rejection Rates

The study identified significant geographic variation in rejection rates.

Rejection Rates by State

State

Rejection Rate

Source

Texas (best)

85.8%

Swipe Solutions 2026

California

91.2%

Swipe Solutions 2026

Florida

92.7%

Swipe Solutions 2026

New York (worst)

95.9%

Swipe Solutions 2026

Source: Swipe Solutions study, January 2026

⚠️ Highest rejection states: Mississippi, Louisiana, Alabama (data available in full study)

Source: Swipe Solutions study

🗺️ What This Means for You

If you live in a high-rejection state (New York, Mississippi, Louisiana, Alabama), you face the toughest approval odds in the country. You need to be even more strategic about which lenders you approach. Don’t waste time applying to banks that will auto-reject you.

Source: Swipe Solutions study analysis

📊 Rejection Rate Range: 85.8% (Texas) → 95.9% (New York)

The state you live in can impact your approval odds by up to 10 percentage points.

If you were just rejected for an emergency loan, here is exactly what to do.

⏰ Hour 1-12: Request Reconsideration

Use the script above. Call the lender’s reconsideration line. Have your income documentation ready. Under ECOA, they must tell you why you were denied.

Source: ECOA 15 U.S.C. § 1691

⏰ Hour 12-24: Apply to 3+ Alternative Lenders

Target credit unions, CDFIs, and fintech lenders — not traditional banks. Remember the 340% multiplier: applying to 3+ lenders increases approval odds by 340%.

📝 “If you need legal documents to dispute a credit report error, send a reconsideration letter, or challenge a lender’s decision — without high attorney fees — Standard Legal offers affordable document preparation and legal forms software.”

⚖️

Need Legal Documents Without the High Attorney Fees?

Standard Legal helps you create legally valid documents for credit disputes, debt validation, reconsideration requests, and more — at a fraction of the cost of hiring an attorney. Two affordable options:

🔗 Affiliate Disclosure: Some links on this page are affiliate links. If you choose to purchase through these links, I may earn a commission at no extra cost to you. I only recommend tools I trust — and Standard Legal has helped thousands of people save on attorney fees.

Reader Story · Composite Account

“I got rejected once and almost gave up. Then I learned about the 340% strategy.”

He applied to his bank of 10 years — rejected. Credit score 612. He almost gave up. “I figured if my own bank said no, no one would say yes.”

Instead, he found this article. He applied to two credit unions and one fintech lender. One credit union approved him for a PAL at 18% APR — less than half what his bank would have charged if they’d approved him.

❌ HIS MISTAKE He almost stopped after one rejection. He didn’t know that 42% of borrowers make the same mistake.

✅ WHAT HE DID RIGHT He applied to 3+ lenders. He targeted credit unions instead of traditional banks. He used the reconsideration script when the first credit union said no (they reversed the decision after he provided additional income documentation).

💡 WHAT HE LEARNED One rejection doesn’t mean all rejections. Different lenders have different rules. The 340% multiplier is real.

👩⚖️ Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“The Equal Credit Opportunity Act gives you rights most borrowers don’t know about.”

“Under the Equal Credit Opportunity Act (ECOA), when a lender denies your application, they must provide a notice of adverse action that states specific reasons for the denial. Not general reasons — specific ones. ‘Credit score too low’ isn’t enough. They need to tell you the score and the range.

More importantly, you have the right to provide additional information for reconsideration. If you were denied because of ‘insufficient income,’ you can send pay stubs, bank statements, or an employer letter. If you were denied because of ‘credit history,’ you can explain extenuating circumstances.

The lender doesn’t have to approve you. But they do have to reconsider if you provide new information. Most borrowers don’t know this — so they don’t ask. And lenders don’t volunteer it.”

⚖️ Legal Analysis: ECOA 15 U.S.C. § 1691 and Regulation B (12 CFR § 1002.9) Require creditors to provide specific reasons for denial and allow applicants to provide additional information for reconsideration. If a lender refuses to reconsider after you provide new information, that may be a violation worth reporting to the CFPB.

📌 Bottom Line

You have the right to ask why you were denied — and the right to ask for reconsideration with more information. Use it.

Click then choose “Save as PDF” in your print dialog.

👩⚖️ Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“Under the Equal Credit Opportunity Act (ECOA), when a lender denies your application, they must provide a notice of adverse action that states specific reasons for the denial. Not general reasons — specific ones. ‘Credit score too low’ isn’t enough. They need to tell you the score and the range.

More importantly, you have the right to provide additional information for reconsideration. If you were denied because of ‘insufficient income,’ you can send pay stubs, bank statements, or an employer letter. If you were denied because of ‘credit history,’ you can explain extenuating circumstances.

The lender doesn’t have to approve you. But they do have to reconsider if you provide new information. Most borrowers don’t know this — so they don’t ask. And lenders don’t volunteer it.”

Bottom Line: You have the right to ask why you were denied — and the right to ask for reconsideration with more information. Use it.

📖 Reader Story · Composite Account

“I got rejected once and almost gave up. Then I learned about the 340% strategy.”

Marcus, 41, needed $1,500 for an emergency furnace replacement in January. He applied to his bank of 10 years — rejected. Credit score 612. He almost gave up. “I figured if my own bank said no, no one would say yes.”

Instead, he applied to two credit unions and one fintech lender. One credit union approved him for a PAL at 18% APR — less than half what his bank would have charged.

❌ HIS MISTAKE:

He almost stopped after one rejection. He didn’t know that 42% of borrowers make the same mistake.

✅ WHAT HE DID RIGHT:

He applied to 3+ lenders. He targeted credit unions instead of traditional banks. He used the reconsideration script when the first credit union said no (they reversed the decision).

Frequently Asked Questions

Everything you need to know about emergency loan rejections and alternatives

Yes, but applying to the same lender again without changing anything won’t help. Either provide new information (pay stubs, bank statements) via reconsideration, or apply to different lenders. Applying to 3+ different lenders increases approval odds by 340%.

Source: Swipe Solutions study

Q

Does checking my rate hurt my credit?

It depends. Some lenders do a “soft pull” (no credit impact) for rate quotes. Others do a “hard pull” (temporary score drop). Always ask: “Is this a soft or hard inquiry?” before applying. The study found that multiple hard inquiries within 14 days are typically treated as one inquiry for scoring purposes.

Source: CFPB credit reporting guidance

Q

What if I was rejected for “insufficient income”?

This is the most reconsiderable reason. Send pay stubs, bank statements showing regular deposits, or an employer letter. If you’re a gig worker, send 6+ months of platform payment records. Under ECOA, you can provide additional income information for reconsideration.

Source: ECOA 15 U.S.C. § 1691

Q

What’s the minimum credit score for any loan?

There is no universal minimum. Credit union PALs often approve scores as low as 580. Some fintech lenders approve scores in the 500-550 range using alternative data. Traditional banks typically require 620-670. The study found approval rates triple when crossing from 579 to 580.

Source: Swipe Solutions study · CFPB credit union data

Q

What if I live in a high-rejection state like New York?

You face the toughest approval odds. Focus on credit unions (which are less affected by state rate caps) and CDFIs. Avoid traditional banks. And definitely use the 3+ lender strategy — you need the 340% multiplier more than borrowers in Texas.

Source: Swipe Solutions state-by-state data

Q

Is there a government program for emergency loans?

No direct loan program, but several resources help: 211 for local emergency assistance, LIHEAP for utility bills (winter), FEMA for disaster-related needs, and local Community Action Agencies for rent/utility assistance. These are grants, not loans — you don’t pay them back.

Source: 211.org · benefits.gov

📌 Quick Summary

Apply to 3+ lenders → Use reconsideration if denied → Know your ECOA rights → Target credit unions and CDFIs → Don’t give up after one rejection

This article is part of the Emergency Borrowing Blueprint 2026 (Episode 22 of 30), a 30-day educational series by Laxmi Hegde, MBA in Finance. All statistics, legal references, and data are drawn from government agencies, consumer advocacy organizations, and primary research institutions as of April 2026.

📅 2026 Updates Included: • Swipe Solutions study (January 2, 2026) — 50,000+ loan applications analyzed • CFPB enhanced ECOA guidance on reconsideration rights (effective 2025-2026) • State-level rejection rate data (first publicly available in 2026)

📘 Part of the Emergency Borrowing Blueprint 2026

This is Episode 22 of 30 in our complete emergency loan decision framework.

📖 Related Episodes: • Episode 6: 7 Alternatives to Same-Day Loans • Episode 10: Why Some People Get Approved Instantly While Others Get Rejected • Episode 17: Payday Loan Debt Help — 5 Proven Ways to Escape the Cycle • Episode 21: Loan Renewal Offers — The Trap That Resets Your Debt

🔜 Coming in Episode 23: “How to Read a Loan Contract in 7 Minutes (Before You Sign)” — We break down every line of a standard loan agreement, including the three sentences that trap 68% of borrowers.

📥 Free Resources Mentioned in This Article

🔓 The Payday Loan Escape Plan

Stop the cycle. Kill the high interest. Reclaim your paycheck. Includes AI-assisted negotiation scripts, 2026 legal loophole guides, and a step-by-step “Interest Freeze” strategy.

Fix your credit. For free. Without paying a repair company. 6 interactive tools, 4 dispute letter templates with FCRA citations, AI-powered strategies for 2026.

Click then choose “Save as PDF” in your print dialog

⚖️ Legal & Financial Disclaimer

The information provided in this guide is for general educational and informational purposes only and should not be interpreted as financial, legal, tax, investment, or professional advice. Nothing on this website constitutes a recommendation, endorsement, or personalized financial strategy.

Financial products, lending regulations, APR structures, fees, and qualification requirements vary significantly by state, lender, and individual circumstances and are subject to change without notice. Always verify terms directly with the lender or institution before making any financial decision.

This content is based on publicly available information and U.S. market conditions as of April 2026. While we strive for accuracy, we make no guarantees regarding completeness, reliability, or current applicability.

📊 93% Rejection Statistic: The 93% rejection statistic comes from a January 2026 study of 50,000+ loan applications. Individual results vary. This article does not guarantee approval from any lender.

Some articles may contain affiliate links. If you choose to apply through these links, we may earn a commission at no additional cost to you. This does not influence our editorial integrity or rankings methodology.

Before taking out any loan or financial product, consider consulting a certified financial planner (CFP), licensed credit counselor, or qualified attorney to assess your specific situation.

By using this website, you acknowledge that the publisher and authors are not responsible for any financial losses, damages, or outcomes resulting from actions taken based on this content.

📝 “If you need legal documents to dispute a credit report error, send a reconsideration letter, or challenge a lender’s decision — without high attorney fees — Standard Legal offers affordable document preparation and legal forms software.”

⚖️ Need Legal Documents Without the High Attorney Fees?

Standard Legal helps you create legally valid documents for credit disputes, debt validation, reconsideration requests, and more — at a fraction of the cost of hiring an attorney.

📄 Document Preparation Service

Let Standard Legal prepare your documents for you. Professionally prepared legal documents reviewed by legal professionals. Perfect for bankruptcy, wills, incorporation.

💻 Legal Forms Software

Create your own documents with easy-to-use software. Complete legal forms library with step-by-step interview format. Unlimited use for one low price.

🔗 Affiliate Disclosure: Some links on this page are affiliate links. If you choose to purchase through these links, I may earn a commission at no extra cost to you. I only recommend tools I trust — and Standard Legal has helped thousands of people save on attorney fees.

“How to Read a Loan Contract in 7 Minutes (Before You Sign)”

We break down every line of a standard loan agreement — including the three sentences that trap 68% of borrowers.

📅

PUBLICATION NOTE

Published April 11, 2026 · Updated as part of the ConfidenceBuildings.com 2026 Consumer Finance Research Project.

This post is Episode 22 of 30 in the Emergency Borrowing Blueprint (2026 Complete Guide), examining emergency borrowing, predatory lending practices, and consumer financial rights. This episode focuses specifically on the 2026 emergency loan rejection crisis — including the 93% rejection rate, the 340% multiplier, state-by-state data, reconsideration scripts, and alternative lenders that actually approve borrowers.

🔬 RESEARCH METHODOLOGY

Information compiled from primary sources including the Swipe Solutions study (January 2026), Consumer Financial Protection Bureau (CFPB), Federal Trade Commission (FTC), Equal Credit Opportunity Act (15 U.S.C. § 1691), Regulation B (12 CFR § 1002.9), National Consumer Law Center (NCLC), and BriefGlance analysis.

📌 2026 Updates Included:

Swipe Solutions study (January 2, 2026) — 93% rejection rate data

CFPB enhanced ECOA guidance on reconsideration rights

First publicly available state-by-state rejection rate data

⚖️ For educational purposes only. Not financial or legal advice. Laws regarding lending, credit denial, and reconsideration rights vary by state and change frequently. The information in this article is current as of April 2026. If you believe a lender has violated your rights under ECOA or other laws, consult a qualified consumer rights attorney or file a complaint with the CFPB.