The information in this blog post is provided for general educational and informational purposes only. It does not constitute financial, investment, or professional advice of any kind. Building savings habits and financial planning are highly individual — what works for one person may not work for another depending on income, expenses, debts, and personal circumstances. > > Laws and financial products vary by region. Always consult a certified financial planner or accredited credit counselor before making significant financial decisions. > > The publisher, authors, and affiliated parties accept no liability for any financial outcomes — positive or negative — resulting from the application of any strategies discussed in this post. Any third-party tools, apps, or institutions mentioned are referenced for informational purposes only and do not constitute an endorsement. —

🔗 Part of the “Borrower’s Truth” Series — Day 2Yesterday we covered the hidden costs and fine print traps lenders set for desperate borrowers. Read it here: Hidden Costs & Fine Print: What Lenders Don’t Tell YouBecause the best way to avoid a predatory loan is to never need one in the first place.

1. The Real Reason You Don’t Have an Emergency Fund Yet {#real-reason}

Let’s skip the lecture.

You already know you’re supposed to have an emergency fund. Every personal finance article since the dawn of the internet has told you to save three to six months of expenses. You’ve nodded along. You’ve meant to start. Life happened instead.

Here’s what those articles never say: the advice was written for people who already have extra money. It assumes you have a surplus — something left over at the end of the month that’s just sitting there, waiting to be responsibly redirected into a high-yield savings account.

If that were true, you wouldn’t be reading this.

The reality for most people — especially those running small businesses, working unpredictable hours, or living paycheck to paycheck — is that there is no surplus. The math doesn’t leave room. And so the emergency fund stays a plan, right up until the moment you desperately need one and have to Google “emergency loan no credit check” at 11pm on a Tuesday.

That’s the moment this blog is trying to prevent.

So instead of telling you to “cut your daily coffee” (please, we’re not doing that), this guide is going to meet you exactly where you are — whether that’s $0 saved, $47 saved, or negative saved because you borrowed from yourself three months ago and forgot.

We’re building something real. We’re starting today. And yes, $10 is genuinely enough to begin.

Starting from zero isn’t failure. It’s just the beginning — and everyone who has savings once started exactly here.

2. How Much Do You Actually Need? (The Honest Answer) {#how-much}

The “three to six months of expenses” rule is the financial equivalent of “drink eight glasses of water a day.” Technically correct. Wildly unhelpful without context.

Here’s what that actually means in real numbers — and here’s the version that doesn’t make you want to close the tab:

The traditional target: If your monthly expenses (rent, utilities, food, transportation, minimum debt payments) total $2,500 — then a full emergency fund is $7,500 to $15,000.

Reading that number when you have $0 saved is genuinely demoralizing. So let’s reframe it.

The actual goal progression:

Milestone

Amount

What It Covers

🥚 Baby Fund

$500

One car repair, one medical copay, one busted appliance

🌱 Starter Fund

$1,000

Most single emergencies without touching a credit card

🌿 Buffer Fund

1 month of expenses

Job loss buffer, giving you 30 days to breathe

🌳 Real Fund

3 months of expenses

Industry standard — genuine financial cushion

🏆 Full Fund

6 months of expenses

Sleep-soundly-at-night money

Start with $500. Just $500.

Not because that’s all you should save. But because $500 handles the vast majority of everyday emergencies — and it transforms you from someone who needs a loan for a flat tire into someone who just… handles it. That psychological shift is worth more than the money itself.

3. The $10 Starting Point — And Why It’s Not Ridiculous {#ten-dollar-start}

Here’s something nobody tells you: the habit matters more than the amount.

Behavioral economists have studied this to death. The single biggest predictor of whether someone becomes a saver isn’t their income. It’s whether they’ve established the identity of being “someone who saves.” And the only way to establish that identity is to start — even embarrassingly small.

Ten dollars. Put it somewhere. Right now, today.

You’ve just crossed from “person who wants to save” to “person who saves.” That’s not nothing. That’s actually the hardest part for most people, and you’ve done it.

Now we build.

“The best time to plant a tree was 20 years ago. The second best time is today. The best time to open a savings account is right after reading this sentence.” — Nobody famous, but they should be

$10 isn’t a lot. But it’s the difference between zero and something — and something is where everything starts.

4. Step 1: Find the Money You Didn’t Know You Had {#find-money}

Before you can save money, you need to find it. And it’s probably hiding in places you’ve stopped looking.

This is not a “stop buying avocado toast” section. This is a serious audit of where small amounts of money are quietly disappearing every month — and how to redirect them without feeling like you’re punishing yourself.

Do this exercise right now — it takes 11 minutes:

Open your last two bank statements. Look for these specific categories:

Subscriptions you forgot about: Most people discover at least one subscription they forgot they had during this exercise. A $12.99 streaming service nobody watches. A $9.99 app that auto-renewed last April. An old gym membership from a pandemic-era optimism spiral. Cancel them. That’s $20–$50/month you just found.

The “rounding up” opportunity: Notice every purchase ending in an odd number. $23.47 for groceries. $8.63 for coffee. The change — the $0.53, the $1.37 — feels invisible. Apps like Acorns and Chime round up every purchase to the nearest dollar and deposit the difference into savings. Most people save $15–$30 a month this way without noticing.

Utility audit: Call your internet provider and ask if there’s a cheaper plan. Seriously — just call. About 40% of people who call their providers asking for a better rate get one. The average savings is $15–$20/month.

The “do I actually use this?” filter: Go through every recurring charge. For each one, ask: “Did I use this in the last 30 days?” If the answer is no, cancel it and add that amount to your emergency fund contribution.

Conservative estimate of what most people find: $40–$120 per month. That’s $500–$1,400 a year that was already yours — it was just going somewhere else.

Your emergency fund is probably hiding in your subscription list. Let’s go find it.

5. Step 2: Open the Right Account (Not Your Regular Checking Account) {#right-account}

This step is where most people quietly sabotage themselves.

They decide to “save” their emergency fund by just… not spending it. It sits in their checking account. Accessible. Spendable. Adjacent to their regular money. And then one Tuesday there’s a really good sale, or the electricity bill is slightly higher, or they just forget — and the “savings” evaporate.

Your emergency fund needs its own home. Here’s why:

When money is in your checking account, your brain categorizes it as “available to spend.” When it’s in a separate account — ideally at a completely different bank — your brain categorizes it as “not really money I have right now.” That psychological distance is not a trick. It’s an evidence-backed behavioral finance principle called the Pain of Paying, and it works.

What to look for in an emergency fund account:

High-Yield Savings Account (HYSA): Currently offering 4–5% APY at online banks vs. the 0.01% your big bank gives you. On $1,000, that’s the difference between earning $0.10 and $45 per year. Not life-changing, but it’s something.

No minimum balance fees: Because you’re starting small and fees would eat your progress

No withdrawal penalties: Emergency funds need to be accessible. CDs and investment accounts are not emergency funds.

Separate from your daily bank: The friction of transferring money is a feature, not a bug

Good places to look: Online banks and credit unions typically offer the best combination of high interest rates and low (or no) fees for this purpose. Credit unions in particular deserve your attention — they’re member-owned, which means profits go back to members, not shareholders.

⚠️ Disclaimer: Interest rates change frequently. Always verify current APY rates directly with the financial institution before opening an account. The author is not affiliated with any bank or financial institution mentioned or implied in this post.

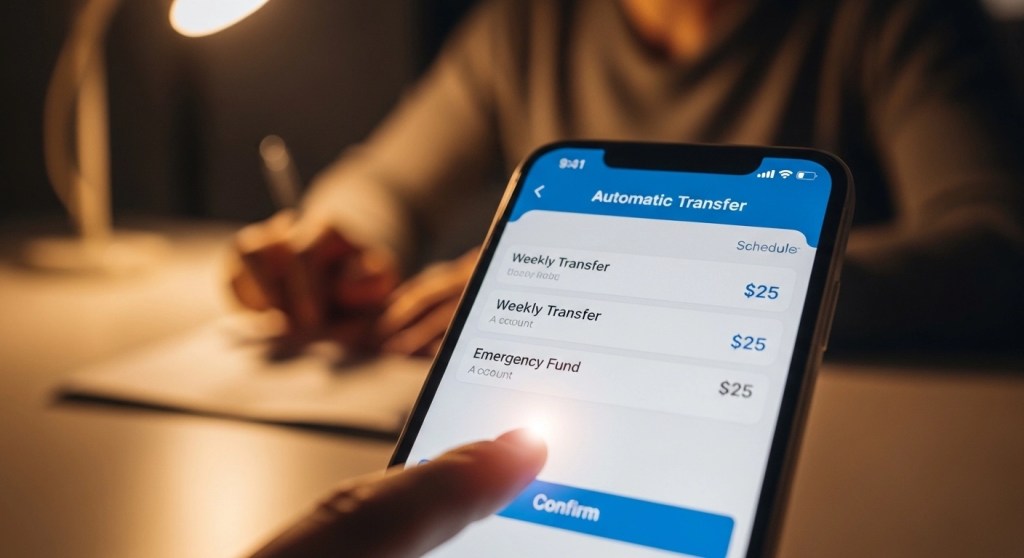

6. Step 3: Automate It So You Can’t Accidentally Spend It {#automate}

Here’s the single most powerful thing you can do for your emergency fund: make saving the default, not the decision.

Every time saving requires a conscious choice — “should I put $50 away this week?” — you introduce the possibility of choosing not to. Life will always provide excellent reasons to choose not to. The car needs gas. The kids need something. It’s someone’s birthday. The choice becomes the problem.

Automation removes the choice entirely.

Set up an automatic transfer from your checking account to your emergency fund savings account. Even $25 a week. Even $10. Schedule it for the day after your paycheck lands — before you’ve had a chance to mentally spend it elsewhere.

Pay yourself first. Not after bills. Not after groceries. First. Even if “first” is just $10.

The math on small automatic savings:

Weekly Auto-Transfer

Monthly

After 6 Month

After 1 Year

$10/week

$43

$258

$520

$25/week

$108

$650

$1,300

$50/week

$217

$1,300

$2,600

$100/week

$433

$2,600

$5,200

Even the smallest row — $10 a week — gets you past that critical $500 Baby Fund milestone in under a year. And once you hit $500, something changes. You stop feeling like you’re starting from zero. You feel like someone with a financial cushion. That feeling accelerates everything.

Set it once. Let it run. Your future self will quietly thank you every single month.

7. Step 4: Build Fast With These Micro-Saving Hacks {#micro-saving}

Automation builds steadily. These tactics build faster — use them to accelerate toward your first $500 milestone.

The No-Spend Weekend: Pick one weekend a month and spend $0 on non-essentials. Cook at home, find free entertainment, decline the group dinner. Average savings: $80–$150 per weekend. Done once a month, that’s nearly $1,000–$1,800 extra per year.

The Cash Envelope for Discretionary Spending: Withdraw your “fun money” budget in cash each week. When it’s gone, it’s gone. No card swiping, no “I’ll just check the balance.” Cash creates physical awareness of spending that cards completely eliminate. Most people spend 12–18% less when using cash instead of cards.

Sell the Stuff: Walk through your home with fresh eyes. Clothes you haven’t worn in two years. Electronics in a drawer. Books you’ll never re-read. Kitchen gadgets from your brief juicing phase. Facebook Marketplace, eBay, and local buy-sell groups can turn that stuff into a meaningful emergency fund deposit within a weekend. Average first-time seller finds $150–$400 worth of sellable items.

The Savings Rate Challenge: Increase your automatic transfer by just $5 every month. Month 1: $10/week. Month 2: $15/week. Month 3: $20/week. By month 10, you’re saving $55/week — but each individual increase was small enough that you barely noticed.

Tax Refund Rule: If you receive a tax refund, put a minimum of 50% directly into your emergency fund before you spend a single dollar of it. The other 50% can go wherever you’d like — no guilt. This single habit alone can fund a Baby Emergency Fund in one transaction for many people.

8. Step 5: Protect It Like It’s Your Last Pizza Slice {#protect-it}

You’ve built it. Now comes the part nobody talks about: keeping it.

An emergency fund that gets raided for non-emergencies is just a delayed-spending account with extra steps. You need ground rules — preferably written ones — for what actually qualifies as an emergency.

Is it an emergency? Ask these three questions:

Is it unexpected? (If you knew Christmas was coming, it’s not an emergency — it’s a planning failure.)

Is it necessary? (Would real harm come from waiting or skipping this expense?)

Is it urgent? (Does this need to be handled right now, or does it just feel urgent because it’s uncomfortable?)

True emergencies (yes, use the fund):

Medical or dental crisis

Car repair needed to get to work

Job loss — covering essentials while you recover

Essential appliance failure (refrigerator, heating in winter)

Urgent home repair preventing habitable living

Not emergencies (do not use the fund):

A really good sale on something you wanted

A social event you didn’t budget for

An impulse purchase you’re rationalizing as “necessary”

Covering overspending from last month

The moment you use your emergency fund for a non-emergency, you’ve trained your brain that the fund is available spending money. That makes the next withdrawal easier. And the next. Define the rules before you need the money — when you’re calm and thinking clearly — not in the moment when every expense feels urgent.

Building it is hard. Protecting it from yourself is harder. Define your rules before you need the money.

9. What to Do When Life Hits Before the Fund Is Ready {#life-hits}

Here’s the part that most emergency fund guides completely skip — and it’s the most important part for you, the person reading this right now, who probably needs emergency money before the fund is built.

What happens when the car breaks down and you have $47 saved?

First — don’t panic. Here are your options in order of “least damaging to your financial future”:

Option 1: Negotiate directly with the provider Medical bills, car repair shops, dentists, landlords — many will accept payment plans with zero interest if you simply ask. This is the most underused option in personal finance. Call, explain your situation, and ask: “Is there a payment plan available?” The worst they say is no.

Option 2: Ask your employer for an advance Many employers — especially small businesses — will advance a paycheck in a genuine emergency. This is interest-free money you’ve technically already earned. Embarrassing to ask, yes. Better than a payday loan? Absolutely.

Option 3: Check nonprofit and community resources 211.org connects you to local emergency assistance programs for utilities, rent, food, and medical bills. Many communities have emergency funds that go completely untapped because people don’t know they exist.

Option 4: Credit union emergency loan If you need to borrow, credit unions offer Payday Alternative Loans (PALs) capped at 28% APR — dramatically better than a payday lender’s 390%. You typically need to be a member for at least one month.

Option 5: 0% APR credit card (if your credit allows) Some credit cards offer 0% introductory APR for 12–18 months. If you can pay the balance before the promotional period ends, this is essentially a free short-term loan.

Option 6: Personal loan from an online lender Better than payday loans, worse than the options above. If you go this route, please read our full guide on hidden fees and fine print first: Hidden Costs & Fine Print: What Lenders Don’t Tell You

⚠️ Reminder: The options above carry varying degrees of financial risk. What works for your situation depends on your income, credit history, and the nature of the emergency. This is general guidance — not personalized financial advice.

10. The Emergency Fund Milestone Chart {#milestone-chart}

Use this as your roadmap. Celebrate every single milestone — seriously, mark them in your calendar, tell someone, do something small to acknowledge the win. Positive reinforcement is not cheesy. It’s neuroscience.

Milestone

Target Amount

Celebration Idea

🥚 First Deposit

Any amount

You started. That’s real.

🌱 Baby Fund

$500

Nice dinner at home — you cooked it

✨ First $1,000

$1,000

Day trip somewhere you’ve been meaning to go

🌿 One Month

1x monthly expenses

Genuine night off — no financial stress allowed

🌳 Three Months

3x monthly expenses

This is a big deal. Celebrate accordingly.

🏆 Full Fund

6x monthly expenses

You did something most people never do. Remember this feeling.

Every milestone is worth celebrating. Progress is progress, no matter the speed

11. Frequently Asked Questions {#faq}

Q: Should I build an emergency fund or pay off debt first? This is one of the most debated questions in personal finance. The general consensus: build a $1,000 Baby Fund first, then aggressively pay down high-interest debt, then continue building the full emergency fund. The reason: without any savings buffer, every unexpected expense goes straight onto your credit card — adding to the debt you’re trying to eliminate. The $1,000 breaks that cycle.

Q: What if I can only save $5 a week? Save $5 a week. That’s $260 a year. It won’t get you to a full emergency fund quickly, but it builds the habit, it builds the account, and it proves to yourself that saving is something you do. Increase when you can.

Q: Can my emergency fund be in a Roth IRA? Technically, you can withdraw Roth IRA contributions (not earnings) penalty-free at any time. Some people use this as a hybrid emergency fund/retirement account. However, this approach has risks — if you withdraw, you lose the contribution room permanently. Better to keep emergency funds separate and accessible.

Q: Should I invest my emergency fund to make it grow faster? No. Your emergency fund needs to be stable and immediately accessible. The stock market can drop 30% right before you need the money — that’s the opposite of helpful. High-yield savings accounts and money market accounts are the right home for emergency funds.

Q: What counts as a real emergency? Refer back to the three-question test in Section 8. When in doubt: unexpected + necessary + urgent = emergency. Two out of three usually means plan, don’t withdraw.

12. Final Thoughts: Start Ugly, Start Today {#final-thoughts}

Perfect is the enemy of started.

You don’t need a plan. You don’t need a spreadsheet. You don’t need to know exactly how you’ll get from $10 to $10,000. You need to open a separate account, move some money into it — however little — and set up an automatic transfer for next week.

That’s it. That’s the whole beginning.

The people who have emergency funds didn’t get there because they had more money than you. They got there because they started when they also had almost nothing, and they kept going despite the flat tires and the unexpected bills and the months when they had to pause the automatic transfer.

They started ugly. And then they kept going.

The loan trap that our previous post warned you about? The one that turns a $500 emergency into $1,400 of debt? The emergency fund is the only thing that truly prevents it. Not willpower. Not budgeting apps. Not good intentions.

Money in an account, specifically for emergencies, that you don’t touch until you need it.

Start today. Start with $10. Start ugly.

🔗 Coming up tomorrow — Day 3 of the Borrower’s Truth Series:“Need Money Now? 7 Alternatives to Emergency Loans You Haven’t Tried Yet”Because sometimes the best loan is the one you don’t have to take.

💬 Where are you in your emergency fund journey? First deposit? First $500? Tell me in the comments — I genuinely want to know. And if you found this helpful, share it with someone who’s been meaning to start.