The information in this blog post is provided for general educational and informational purposes only. It does not constitute financial, legal, or professional advice. Loan terms, repossession laws, and consumer rights vary significantly by state, lender, and individual circumstances. Always verify your specific rights with a qualified attorney or financial professional, or through official sources such as the CFPB (consumerfinance.gov).

Part of the ConfidenceBuildings.com — Borrower’s Truth Series

📅 Day 5 Episode | Published: February 2026

📚 Previous Episodes in This Series:

- Day 1 — Hidden Costs & Fine Print: What Lenders Don’t Tell You

- Day 2 — How to Build an Emergency Fund From Scratch When You Have Nothing Saved

- Day 3 — Broke & Stressed? 7 Real Alternatives to Emergency Loans That Most People Overlook

- Day 4 — Your Credit Score Is a Weapon — And Lenders Are Trained to Use It Against You

🔗 Part of the “Borrower’s Truth” Series — Day 5 In Day 4 we exposed how lenders use your credit score as a pricing weapon — and the legal notice you’re entitled to that almost nobody knows about. Read it here: Your Credit Score Is a Weapon — And Lenders Are Trained to Use It Against You Today we tackle the decision that trips up almost every emergency borrower — and we’re going to actually help you make it.

Read the complete guide here: The Complete Borrower’s Truth Guide →

Table of Contents

- The Question Everyone Gets Wrong

- Secured Loans: What They Are and What They’re Actually Risking

- Unsecured Loans: The Freedom That Costs More

- The Hidden Third Option Nobody Talks About

- The Truth About Repossession (That Your Lender Won’t Volunteer)

- The Deficiency Balance Trap — You Can Lose the Car AND Still Owe Money

- The “Choose Your Solution” Decision Framework

- Solution Path A: You Have Assets and Good Credit

- Solution Path B: You Have Assets but Damaged Credit

- Solution Path C: No Assets, Good Credit

- Solution Path D: No Assets, Damaged Credit

- Side-by-Side Comparison: All Loan Types for Emergency Borrowers

- Before You Sign: The 5 Questions That Protect You

- Final Thoughts: The Right Loan Is the One That Fits YOUR Life

1. The Question Everyone Gets Wrong {#introduction}

Here’s how every “secured vs. unsecured loan” article on the internet works:

They explain that secured loans need collateral. They explain that unsecured loans don’t. They list the pros and cons of each. They conclude with something like “the right choice depends on your situation.” And then they leave you to figure out your situation entirely on your own.

Thanks. Incredibly helpful. Really.

The problem isn’t that the information is wrong — it’s that it’s incomplete in exactly the way that costs real people real money. Because the decision between secured and unsecured isn’t just about interest rates and collateral definitions. It’s about what you actually have, what you can actually afford to risk, and what happens to your specific life if things go sideways.

A person who needs their car to get to work cannot evaluate a title loan the same way as someone with a spare vehicle. A person with $2,000 in savings has options that someone with zero savings doesn’t. These distinctions matter enormously — and nobody’s making them for you.

Until today.

This post is going to do something your competitors don’t: take you through a real decision framework based on your actual situation. Multiple solution paths. You choose the one that matches your reality. By the end, you’ll know exactly which type of loan makes sense for you — and which ones to avoid.

But first — we need to talk about something most lenders hope you never find out.

2. Secured Loans: What They Are and What They’re Actually Risking {#secured-loans}

A secured loan is a loan backed by collateral — an asset you own that the lender can legally claim if you stop making payments.

The most common forms you already know: mortgages (your house is collateral), auto loans (your car is collateral), home equity loans (your home equity is collateral).

But here’s what most people don’t fully absorb: the collateral isn’t just a formality. It’s a legally binding pledge that the lender can act on without going to court in most states.

That car you’re putting up as collateral? If you miss payments, a repossession agent can legally take it from your driveway — sometimes overnight, without warning, without a court order.

That savings account you’re securing the loan against? Frozen. The lender holds it until the loan is paid. If you default, they take it.

Why do secured loans exist then? Because they genuinely offer advantages:

- Lower interest rates — lenders take less risk, pass some savings to you

- Higher loan amounts — collateral unlocks borrowing power beyond your credit score

- Easier approval — even with damaged credit, collateral can get you approved

- Longer repayment terms — more time to pay means lower monthly payments

The math is real. A secured personal loan might offer 8–12% APR where an unsecured loan for the same person would be 20–28%. On a $5,000 loan over 3 years, that gap is $800–$1,500 in total interest.

The catch — and it’s a big one: The advantage only works if you’re absolutely confident in your ability to repay. Because the downside isn’t just a hit to your credit score. It’s losing something that matters to your daily life.

3. Unsecured Loans: The Freedom That Costs More {#unsecured-loans}

An unsecured loan requires no collateral. The lender approves you based on your credit score, income, and debt-to-income ratio alone. Your signature is the only guarantee they get.

The advantages are real:

- No asset at risk — if things go wrong, you don’t lose your car or your home

- Faster approval — no collateral valuation means quicker processing

- Flexible use — funds can go toward almost anything

- Available from banks, credit unions, and online lenders

The cost is also real:

- Higher interest rates — lenders price in the extra risk they’re taking

- Stricter credit requirements — most good unsecured loans want a 640+ credit score

- Lower loan amounts — without collateral backing, lenders cap what they’ll offer

- Shorter repayment terms — less time to pay means higher monthly payments

What happens if you default on an unsecured loan?

The lender can’t immediately take your car or your couch. But don’t mistake “no collateral” for “no consequences.” If you stop paying an unsecured loan, the lender will report you to credit bureaus, send the debt to collections, and can eventually sue you for repayment. If they win — and they usually do — a court can order wage garnishment, meaning they take a percentage of your paycheck directly. They can also place a lien on property you own.

No immediate repossession. Still deeply unpleasant.

4. The Hidden Third Option Nobody Talks About {#third-option}

Here’s the section your competitors skipped — and it might be the most useful thing in this entire post for certain borrowers.

There’s a third type of loan that sits between secured and unsecured: the cash-secured loan (also called a share-secured loan or savings-secured loan).

Here’s how it works: you borrow against money you already have in a savings account or certificate of deposit. The lender freezes that amount as collateral but gives you a loan equal to it — which you then repay with interest over time.

“Wait,” you’re thinking. “Why would I borrow money I already have?”

Three very good reasons:

Reason 1 — Credit building. If you have damaged or thin credit, a cash-secured loan lets you borrow and repay, creating a positive payment history on your credit report — without risking an asset you truly can’t afford to lose.

Reason 2 — Protecting your emergency fund. If you have $1,000 saved but need $1,000 for an emergency, withdrawing it wipes out your safety net entirely. A cash-secured loan lets you access that value while keeping the account (frozen, not gone) — and once repaid, your fund is intact.

Reason 3 — Extremely low interest rates. Because the risk to the lender is essentially zero (they already have your money), cash-secured loans typically charge 2–4% above the savings account rate — often 4–7% APR total. That’s cheaper than almost any other personal loan option.

Where to get one: Credit unions offer these most commonly, often called “share-secured loans.” Some online banks and community banks offer them too.

The downside: You need to have the money first. Which makes this option most useful for someone who has savings but doesn’t want to fully drain them, or someone using this specifically as a credit-building tool.

💡 Real scenario where this makes sense: You have $800 in savings. Your car needs $600 in repairs. Instead of withdrawing the $600 (leaving you with just $200 as a buffer), you take a $600 cash-secured loan at 5% APR, keep your savings account intact (frozen as collateral), and repay $52/month for 12 months. Total interest cost: about $33. Your emergency fund is effectively preserved, your credit gets a boost, and the repair gets done.

5. The Truth About Repossession (That Your Lender Won’t Volunteer) {#repossession-truth}

This is the section that exists nowhere in standard secured vs. unsecured loan content — and it’s the most important thing an emergency borrower needs to understand before putting up collateral.

In most U.S. states, lenders can repossess your car without going to court and without giving you advance notice.

Read that again. No court. No warning. They can legally send a repossession agent to your home or workplace and take the vehicle — as long as they do so without “breaching the peace” (meaning without force or confrontation).

You could wake up tomorrow morning and your car could be gone. Legally. Without you having any say in it.

This is not a horror story — it’s standard contract law in most states. When you sign an auto loan or use your vehicle as collateral for any secured loan, you’re signing a document that gives the lender this right. Most people never read that clause. Now you know it exists.

The repossession timeline in practice:

Most lenders don’t actually repossess on day one of a missed payment. The typical sequence looks like this:

- Day 1–30: Payment missed. Lender calls and emails. Late fees begin.

- Day 30–60: Loan goes delinquent. Credit bureaus are notified. More aggressive outreach.

- Day 60–90: Account approaches default status. Lender may offer hardship options at this stage — ask for them.

- Day 90+: Default declared. Repossession authorized. Can happen any day after this point.

What you can do before it gets to step 4:

Call your lender before you miss a payment — not after. Lenders have significantly more options available to you at step 1 than at step 4. Ask specifically about:

- Hardship programs

- Payment deferral (moving a payment to the end of the loan)

- Loan modification (restructuring your payments)

- Voluntary surrender options (which preserve more of your credit than forced repossession)

The single worst thing you can do is go silent and hope they won’t notice. They will notice. And by the time they act, your options have narrowed considerably.

⚠️ Disclaimer: Repossession laws vary by state. Some states require notice before repossession; others do not. Always verify your specific state’s laws through your state attorney general’s office or a qualified legal professional.

6. The Deficiency Balance Trap — You Can Lose the Car AND Still Owe Money {#deficiency-balance}

Here’s the part that genuinely shocks people — and that almost no consumer finance content explains clearly.

When a lender repossesses your car and sells it at auction, the sale price rarely covers what you still owe on the loan. Cars depreciate. Auction prices are often well below market value. And the lender adds repossession and storage fees to your balance before the auction even begins.

Example:

- You owe $12,000 on your secured loan

- Car is repossessed and sold at auction for $7,500

- Repossession and storage fees: $800

- Remaining balance (deficiency): $5,300

You still owe $5,300. On a car you no longer have. That you can no longer drive to work.

This is called a deficiency balance — and the lender can and often will pursue you for it through collections or a lawsuit. In most states, they have every legal right to do so.

What this means for your decision:

Before putting up any asset as collateral for an emergency loan, you need to honestly ask yourself: “If I lose this asset AND still owe money on it, what does my life look like?”

If the answer to that question involves losing your ability to work, care for your family, or maintain basic stability — then a secured loan against that asset carries more risk than the lower interest rate is worth.

⚠️ Disclaimer: Deficiency balance laws vary by state. Some states have anti-deficiency protections that limit or prohibit lenders from pursuing deficiency balances. Research your specific state’s laws at your state attorney general’s website or consult a legal professional before making decisions based on this information.

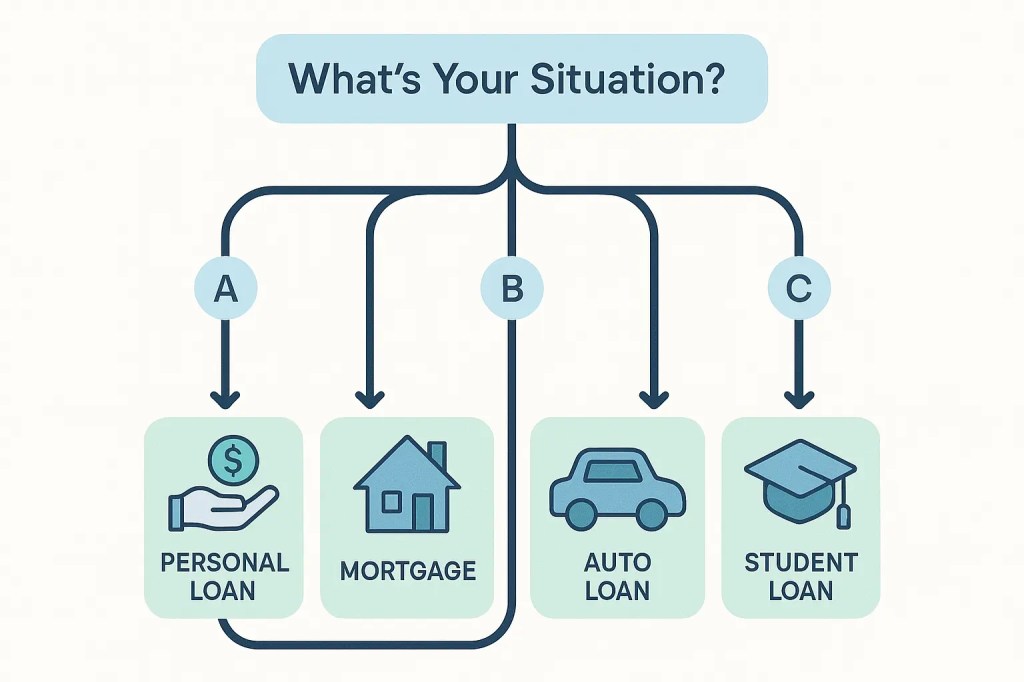

7. The “Choose Your Solution” Decision Framework {#decision-framework}

This is the section that doesn’t exist anywhere else. Every competitor tells you what secured and unsecured loans are. None of them help you choose.

Here’s how to use this framework:

Step 1: Answer these three questions honestly:

Question A: Do you own a valuable asset (car, home, savings account with $500+) that you could use as collateral?

- Yes → Go to Question B

- No → You’re on Path C or D (scroll down)

Question B: Is that asset essential to your daily life and income?

- My car is how I get to work → Secured loan against it = HIGH RISK

- I have savings I could borrow against → Cash-secured loan = LOW RISK option

- I have home equity → Secured option exists but involves long process

Question C: What is your current credit score range?

- 680+ → Unsecured loan is accessible to you

- 580–679 → Limited unsecured options, secured or cash-secured may be better

- Below 580 → Unsecured loan very difficult; secured or alternatives are your path

Now find your path below:

8. Solution Path A: You Have Assets and Good Credit (Score 680+) {#path-a}

Your situation: You own a car, home equity, or savings. Your credit is solid. You have options — which means your job is to choose the cheapest one, not just the first available one.

Best solutions in order of preference:

Solution 1 — Unsecured personal loan (best choice) With 680+ credit, you can access unsecured personal loans at reasonable rates (typically 8–18% APR). This protects your assets completely. No collateral risk. Shop at least 3 lenders — credit unions first, then online lenders, then banks. Use soft-pull pre-qualification tools to compare without hitting your credit score.

Solution 2 — Cash-secured loan If your savings account has enough to cover the emergency, a cash-secured loan preserves the fund while giving you access to the value. Especially useful if you’re also trying to build credit.

Solution 3 — HELOC or home equity loan If you own a home with equity and the amount needed is substantial ($5,000+), a home equity line offers low rates — but takes longer to process and puts your home at risk. Not ideal for true emergencies due to timeline, but worth knowing exists.

What to avoid: Secured personal loans using your car as collateral when you have good credit and could qualify for unsecured options. The rate savings don’t justify the asset risk when you have alternatives.

9. Solution Path B: You Have Assets but Damaged Credit (Score Below 640) {#path-b}

Your situation: You own things but your credit has taken hits. The lower rate of a secured loan is genuinely attractive — but the asset risk is real and you need to choose carefully.

Best solutions in order of preference:

Solution 1 — Cash-secured loan (often best choice) Borrowing against your own savings at a credit union costs almost nothing in interest, requires no credit check in most cases, and builds your credit score. If you have any savings at all, this should be your first call.

Solution 2 — Credit union PAL loan If you’re a credit union member, Payday Alternative Loans (PALs) are capped at 28% APR — significantly better than most options available to damaged-credit borrowers. No collateral required.

Solution 3 — Secured personal loan (proceed with caution) If the amount needed is larger and your car is paid off, a secured personal loan against the vehicle might be your most accessible option. But only if: you’re confident about repayment, you have a realistic backup plan if income is disrupted, and the asset is not your only means of getting to work.

What to avoid: Title loans. They look like secured personal loans but are predatory products — triple-digit APRs, extremely short repayment windows, and you can lose your car to a lender charging 200%+ APR. Never the right answer.

10. Solution Path C: No Assets, Good Credit (Score 680+) {#path-c}

Your situation: You don’t have collateral to offer, but your credit score gives you real options in the unsecured loan market.

Best solutions in order of preference:

Solution 1 — Unsecured personal loan This is your primary tool and it works well at 680+. Compare offers from credit unions, online lenders (LightStream, SoFi, Upgrade), and your existing bank. Pre-qualify with multiple lenders using soft pulls. Look for: fixed rate, no origination fee if possible, and no prepayment penalty.

Solution 2 — 0% intro APR credit card If your credit is 680+ and you need funds for a specific purchase (not cash), a 0% intro APR credit card for 12–18 months is essentially a free loan if paid off before the promo period ends. Apply only if you’re disciplined about the payoff deadline.

Solution 3 — Employer advance or earned wage access Before taking any loan, check whether an employer advance covers the need. Free, fast, and doesn’t affect your credit. Always worth asking first.

What to avoid: Applying to too many lenders at once (multiple hard pulls in a short period without rate-shopping protection). Shop within a 14-day window to minimize credit score impact.

11. Solution Path D: No Assets, Damaged Credit (Score Below 580) {#path-d}

Your situation: This is the hardest path — and the one most targeted by predatory lenders. No collateral, limited credit options, urgent need. Your options are narrower, but they exist.

Best solutions in order of preference:

Solution 1 — Alternatives before any loan Before borrowing anything, revisit Day 3 of this series — direct negotiation, 211.org community assistance, employer advances, and selling items can frequently resolve emergencies without debt.

Solution 2 — Credit union PAL loan Even with damaged credit, many credit unions offer PAL loans to members. The 28% APR cap makes this the most responsible borrowing option available to you. Join a credit union today if you’re not a member — even if you can’t get a PAL immediately, membership starts the clock.

Solution 3 — Secured credit card (credit rebuilding first) If the emergency isn’t today but you’re planning ahead, a secured credit card with a $200–$500 deposit builds your credit score over 6–12 months — moving you from Path D toward Path C or B where options improve significantly.

Solution 4 — Online lenders for bad credit (with extreme caution) Lenders like Upstart and OppFi serve sub-580 credit scores but at high rates (36–199% APR depending on score and lender). If you go this route, borrow the minimum needed, commit to full repayment, and read our Day 1 guide on hidden fees before signing.

What to absolutely avoid: Payday loans. Title loans. Any lender advertising “guaranteed approval regardless of credit.” These products are designed to keep Path D borrowers in Path D permanently.

💙 If you’re on Path D right now, please know: this path has exits. The exit signs are just less obvious, and the walk is longer. But people move from damaged credit and no assets to genuine financial stability all the time — usually by making a series of small, right decisions exactly like the ones in this series. You’re already making them by being here.

Side-by-Side Comparison: All Loan Types for Emergency Borrowers {#comparison}

| Loan Type | Typical APR | Collateral | Credit Needed | Asset Risk | Best For |

|---|---|---|---|---|---|

| Unsecured Personal Loan | 8–28% | None | 640+ | None | Good credit, no assets to risk |

| Secured Personal Loan | 6–18% | Car, savings, other asset | 560+ | HIGH — asset can be seized | Lower rate when confident in repayment |

| Cash-Secured Loan | 4–7% | Your own savings account | Any | Low (your own money) | Credit building + fund preservation |

| Credit Union PAL | Max 28% | None | Any (member) | None | Any borrower who is a CU member |

| Home Equity Loan | 6–10% | Your home | 620+ | VERY HIGH — home at risk | Homeowners, large amounts, non-urgent |

| Title Loan | 200–400% | Your car title | None | EXTREME — avoid entirely | Almost never — last resort only |

| Payday Loan | 300–400% | None | None | Debt spiral risk | Avoid — see Day 3 alternatives first |

⚠️ Disclaimer: APR ranges above are illustrative estimates based on general market conditions as of early 2026. Actual rates vary significantly by lender, credit profile, loan amount, and other factors. Always obtain personalized quotes before making borrowing decisions.

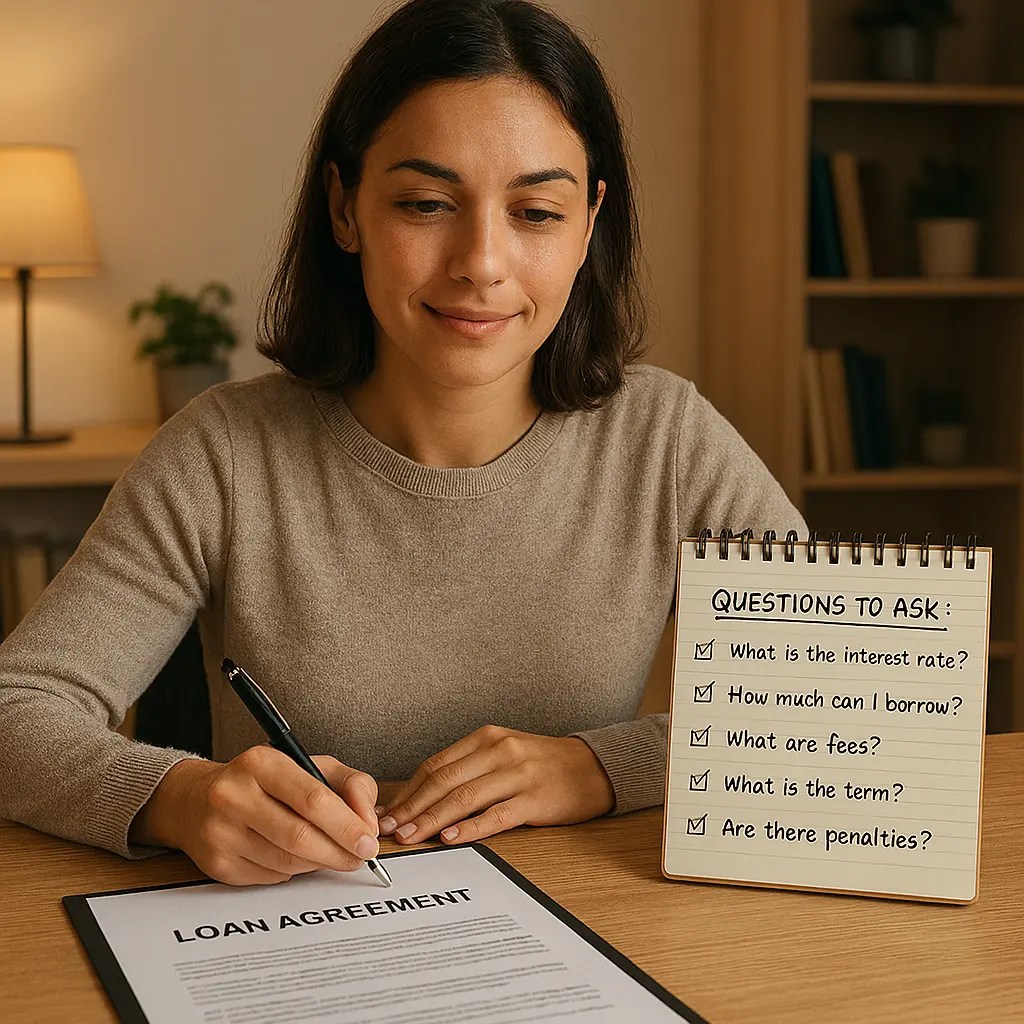

13. Before You Sign: The 5 Questions That Protect You {#before-you-sign}

Regardless of which path and which loan type you choose, ask these five questions before signing anything:

Question 1: “If I miss two payments, what exactly happens — and how quickly?” Get the specific timeline in writing. Know the grace period, the default trigger date, and what action the lender takes first. Surprises after signing are always worse than clarity before.

Question 2: “Can you be repossessed without advance notice in my state?” For any secured loan, ask your lender directly and verify with your state’s consumer protection office. This changes your risk calculation significantly.

Question 3: “If you sell the collateral and it doesn’t cover my balance, do I owe the difference?” This is the deficiency balance question — and many lenders will be vague. Get a direct answer. In some states, anti-deficiency laws protect you. In most, they don’t.

Question 4: “What hardship options do you offer if I run into trouble?” Legitimate lenders have programs — payment deferrals, hardship modifications, temporary forbearance. Knowing they exist before you need them is worth more than you think.

Question 5: “What is my total repayment amount — not my monthly payment?” Monthly payment math is designed to obscure the true cost. A $150/month payment sounds fine. A $7,200 total repayment on a $5,000 loan tells a different story.

14. Final Thoughts: The Right Loan Is the One That Fits YOUR Life {#final-thoughts}

The internet will keep publishing “secured vs. unsecured loans: which is better?” articles that end with “it depends on your situation” — and then leave you to figure out your situation entirely alone.

You now have something better than that. You have a framework that starts with your actual life — your assets, your credit, your risk tolerance — and maps you to solutions that fit. Not the solution that’s easiest to explain. The one that works for where you actually are.

The repossession truth. The deficiency balance trap. The cash-secured loan nobody mentions. The four paths to the right decision. This is what “it depends” actually means — spelled out, step by step, for a real person in a real situation.

And if you’ve been reading this series from Day 1? You now understand hidden fees, emergency fund building, loan alternatives, how your credit score is weaponized against you, and how to choose between loan types. That’s more financial literacy than most people accumulate in years — and you did it in five days.

Keep going. Day 6 is next — and we’re going into the fine print that lenders spend thousands of dollars designing to confuse you.

🔗 Coming up — Day 6 of the Borrower’s Truth Series: “Loan Terms Explained: 30 Confusing Words Translated Into Plain English” Because the fine print isn’t complicated by accident.

💬 Which path are you on — A, B, C, or D? Tell me in the comments. And if this helped you make a decision you were stuck on, share it with someone else who’s stuck. They’ll thank you.