The Complete Borrower’s Truth Guide: Everything You Need to Know Before You Borrow Emergency Money

The information in this guide is provided for general educational and informational purposes only. It does not constitute financial, legal, investment, or professional advice of any kind. Financial products, lending laws, and assistance programs vary significantly by state, lender, and individual circumstances — and change frequently.

All information is based on U.S. law and market conditions as of February 2026. Always verify current details directly with relevant institutions. Consult a certified financial planner, credit counselor, or licensed attorney before making significant financial decisions.

The publisher, authors, and affiliated parties accept no liability for any financial or legal outcomes resulting from reliance on any information in this guide. Third-party organizations, products, or institutions mentioned are for informational purposes only and do not constitute an endorsement.

ConfidenceBuildings.com — Borrower’s Truth Series

🏛️ PILLAR PAGE — The Series Home Base

This is the master guide. Every deep-dive episode in the series links back here.

Table of Contents

- Why This Guide Exists

- Chapter 1: Hidden Costs & Fine Print — The Traps Set Before You Sign

- Chapter 2: Building Your Emergency Fund — Starting From Zero

- Chapter 3: Alternatives to Emergency Loans — Try These First

- Chapter 4: Your Credit Score — The Weapon Lenders Use Against You

- Chapter 5: Secured vs. Unsecured Loans — Making the Right Decision

- Chapter 6: Loan Terms Glossary — 30 Words Translated Into English

- The Borrower’s Master Checklist

- Emergency Loan Red Flags — The Non-Negotiable List

- Your Financial Emergency Action Plan

- About This Series

Why This Guide Exists {#why-this-guide}

Every year, millions of people find themselves in a financial emergency — a car repair, a medical bill, a month where the math simply doesn’t work. And every year, the same thing happens: they search for help online, get bombarded with loan advertisements, and walk into a borrowing decision they don’t fully understand.

The result? A $500 emergency that becomes a $1,400 debt. A loan that seemed helpful turning into a trap. Hidden fees nobody mentioned. Fine print nobody read. And a financial situation that’s measurably worse than before the “help” arrived.

This guide exists to change that.

The Borrower’s Truth Series was built for one specific person: someone facing a real financial emergency who wants real information — not a sales pitch from a lender, not condescending advice that assumes you already have money, not a list of products someone gets paid to recommend.

Just the truth. Clearly. In plain English. With a little humor to make the medicine go down.

Each chapter below summarizes one deep-dive episode from the series. Read the summary here to understand the landscape. Click through to the full episode for every detail, tool, and action step.

Let’s begin.

Knowledge is the only thing that makes the difference between a loan that helps and one that hurts.Chapter 1: Hidden Costs & Fine Print — The Traps Set Before You Sign {#chapter-1}

When you’re stressed and need money fast, the last thing you want to do is read a 47-page loan agreement in 8-point font. Lenders know this — and they design their products accordingly.

The hidden costs that catch most borrowers off guard aren’t accidental. They’re structural. Built into the product. And understanding them before you sign is the single most valuable thing you can do for your financial health.

The traps covered in Episode 1:

The APR Illusion — A lender advertising “5% interest” might be charging 38% APR once all fees are included. Interest rate and Annual Percentage Rate are not the same number — and the difference can cost you hundreds. Under the Truth in Lending Act (TILA), lenders are required to disclose the full APR. Always ask for it in writing before agreeing to anything.

Origination Fees — You’re approved for $5,000 but receive $4,750 in your account. The missing $250 is an origination fee — charged just for processing your loan. These range from 1–8% of the loan amount and often appear at signing, not in the initial advertisement.

Prepayment Penalties — Some lenders actually charge you for paying your loan off early. They planned on collecting interest for the full loan term — and your financial responsibility disrupted their revenue model. Always check for this clause before signing.

Late Fee Compounding — Missing a payment doesn’t just trigger a late fee. In some loan agreements, the late fee itself accrues interest. By month two of a missed payment, you can owe more in fees than in principal.

Rollover Traps — Particularly dangerous in payday loans: you can’t pay back the full amount, so you “roll it over” for a fee. After four rollovers on a $300 loan, you’ve paid $180 in fees and still owe the original $300. The Consumer Financial Protection Bureau (CFPB) has flagged rollover structures as predatory — yet they remain legal in many states.

The Arbitration Clause — Buried on page 22 of most loan agreements: a clause that prevents you from suing the lender in court if something goes wrong, forcing you into private arbitration instead. Most borrowers never know this clause exists until they need to use their legal rights.

💡 The one-sentence takeaway: The advertised rate is the beginning of the conversation, not the full picture — always calculate total repayment before you sign anything.

Includes: APR vs interest rate calculator, red flags checklist, full fine print survival guide

Chapter 2: Building Your Emergency Fund — Starting From Zero {#chapter-2}

The most powerful thing you can do to protect yourself from emergency loan traps is to never need an emergency loan in the first place. That’s what an emergency fund does — it converts financial crises into manageable inconveniences.

The traditional advice — save three to six months of expenses — is technically correct and practically useless for someone starting from zero. Episode 2 replaces that advice with something you can actually act on today.

The framework covered in Episode 2:

Start with $500, not six months. The Baby Fund milestone handles the vast majority of everyday emergencies — car repairs, medical copays, one-month utility crises — without a loan. Getting to $500 is the first and most important goal.

The $10 starting point. The habit of saving matters more than the amount. Opening a separate account and transferring $10 today crosses you from “someone who wants to save” to “someone who saves.” That identity shift is the foundation everything else builds on.

Find the money you already have. The average person who audits their bank statements discovers $40–$120 per month in forgotten subscriptions, unused services, and rounding opportunities they didn’t know existed. That’s $500–$1,400 per year sitting in your account already.

Automate everything. Set up an automatic transfer for the day after your paycheck arrives — before you’ve mentally allocated the money elsewhere. Even $25/week becomes $1,300 in a year without a single conscious decision.

The milestone chart:

| Milestone | Target | What It Covers |

|---|---|---|

| 🥚 Baby Fund | $500 | Most single everyday emergencies |

| 🌱 Starter Fund | $1,000 | Most emergencies without a credit card |

| 🌿 Buffer Fund | 1 month expenses | Job loss — 30 days to breathe |

| 🌳 Real Fund | 3 months expenses | Industry standard cushion |

| 🏆 Full Fund | 6 months expenses | Sleep-soundly-at-night money |

💡 The one-sentence takeaway: An emergency fund isn’t a savings goal — it’s a loan avoidance strategy, and $10 is genuinely enough to start building one today.

📖 Read the full guide: How to Build an Emergency Fund From Scratch →

Includes: Automation strategy, micro-saving hacks, milestone celebration chart, FAQ

Chapter 3: Alternatives to Emergency Loans — Try These First {#chapter-3}

Before you apply for any emergency loan, work through this list. Seven alternatives that are faster, cheaper, or both — and that most people never try because they don’t know they exist.

The 7 alternatives covered in Episode 3:

1. Negotiate directly — Call whoever you owe money to and ask for a payment plan. Medical providers, utility companies, landlords, and mechanics all have more flexibility than they advertise. The script: “I’m experiencing financial difficulty — is there a payment plan available?” Works more often than you’d expect.

2. Employer paycheck advance — It’s your money. You’ve earned it. You just haven’t been paid yet. An advance is interest-free, requires no credit check, and repays automatically from your next paycheck. Embarrassing to ask — better than a payday loan by every financial measure.

3. 211.org and community resources — Call 2-1-1 or visit 211.org to connect with local emergency assistance programs for rent, utilities, food, medical bills, and transportation. Many of these programs are grants — not loans. They don’t get repaid. Most people have never heard of them.

4. Credit union PAL loans — Payday Alternative Loans from credit unions are federally regulated and capped at 28% APR. Compare that to 390% at a payday lender. If you’re not a credit union member, join one today — even if you can’t get a PAL immediately, membership starts the eligibility clock.

5. Cash advance apps — Dave, Earnin, Brigit, and similar apps offer small advances. Useful for bridging a $50–$200 gap. Read the fee structure carefully — the “optional” tip and express delivery fees can represent triple-digit APR on small amounts.

6. Friends and family — The most underused option. Zero percent interest. Flexible repayment. The conversation is uncomfortable. The alternative might be worse. Use a specific ask with a clear repayment plan — it preserves the relationship far better than vague requests.

7. Sell something — A pile of electronics, clothes, and household items you already own could generate $100–$400 within 48–72 hours on Facebook Marketplace, OfferUp, or Poshmark. No application. No credit check. No interest.

💡 The one-sentence takeaway: The best emergency loan is frequently the one you don’t take — try all seven alternatives before filling out a single application.

📖 Read the full guide: 7 Real Alternatives to Emergency Loans →

Includes: Word-for-word negotiation scripts, 211 resource guide, full alternative comparison table

Chapter 4: Your Credit Score — The Weapon Lenders Use Against You {#chapter-4}

Your credit score is not just a number. It’s a pricing tool, a surveillance trigger, and a targeting mechanism — and lenders are trained to use all three against you, especially when you’re financially vulnerable.

Episode 4 covers the parts of the credit score system that consumer finance content almost never explains to regular people.

What the full episode covers:

Risk-based pricing exposed — Lenders don’t just use your score to approve or decline you. They use it to determine exactly how much profit to extract. A borrower with a 740 score and one with a 640 score applying for the same $10,000 loan can pay $2,000+ different amounts in total interest — for the exact same money.

Real-time AI surveillance — Banks run continuous AI monitoring on existing accounts, flagging behavioral changes that predict financial distress weeks before a borrower misses a payment. Rising utilization, multiple loan inquiries, and dropping balances all trigger risk flags — and lead to quietly worsened terms on your existing accounts.

The timing trap — Predatory lenders purchase behavioral data on people recently denied credit or searching for emergency loans. The “pre-approved” offer that arrives at your most vulnerable moment isn’t coincidence — it’s targeting.

The Risk-Based Pricing Notice — A legal right under the Fair Credit Reporting Act that most borrowers never know exists. If a lender offered you worse terms because of your credit report, you’re entitled to a notice that names the score used, the range, and the factors that hurt you — plus a free credit report from the bureau named.

The 2026 scoring changes — FICO 10T now rewards borrowers whose balances are consistently decreasing over 24 months. VantageScore 4.0 now incorporates rent and utility payments. Both changes benefit people rebuilding after a financial setback — if they know to use them.

💡 The one-sentence takeaway: Understanding how lenders use your credit score gives you the ability to negotiate, dispute, and prepare — instead of simply accepting whatever rate you’re offered.

Includes: Real dollar cost table across 5 loan types, 30/60/90 day action plan, credit myths debunked

Chapter 5: Secured vs. Unsecured Loans — Making the Right Decision {#chapter-5}

Every article on this topic tells you what secured and unsecured loans are. None of them help you choose. Episode 5 builds the decision framework that’s been missing from consumer finance content — four distinct paths based on your credit score and assets.

What the full episode covers:

The repossession truth — In most U.S. states, lenders can repossess your vehicle without going to court and without giving you advance notice. One missed payment enough times can mean waking up to an empty driveway, legally, with no warning.

The deficiency balance trap — Losing your car in repossession doesn’t end the debt. If the auction sale price doesn’t cover your loan balance — and it usually doesn’t — you still owe the difference. You can lose the car AND still owe thousands on it.

The hidden third option — Cash-secured loans (borrowing against your own savings at 4–7% APR) sit between secured and unsecured and work for any credit score. Almost no consumer content explains this option properly.

The 4-path decision framework:

| Your Situation | Your Path | Best First Option |

|---|---|---|

| Assets + Good Credit (680+) | Path A | Unsecured personal loan — protect your assets |

| Assets + Damaged Credit (below 640) | Path B | Cash-secured loan — lowest rate, credit building |

| No Assets + Good Credit (680+) | Path C | Unsecured personal loan — you qualify, use it |

| No Assets + Damaged Credit (below 580) | Path D | Alternatives first — then Credit Union PAL |

💡 The one-sentence takeaway: The right loan is not the one with the lowest advertised rate — it’s the one that matches your credit score, protects your essential assets, and fits your realistic repayment capacity.

Includes: 4 borrower paths, full loan comparison table, 5 questions to ask before signing

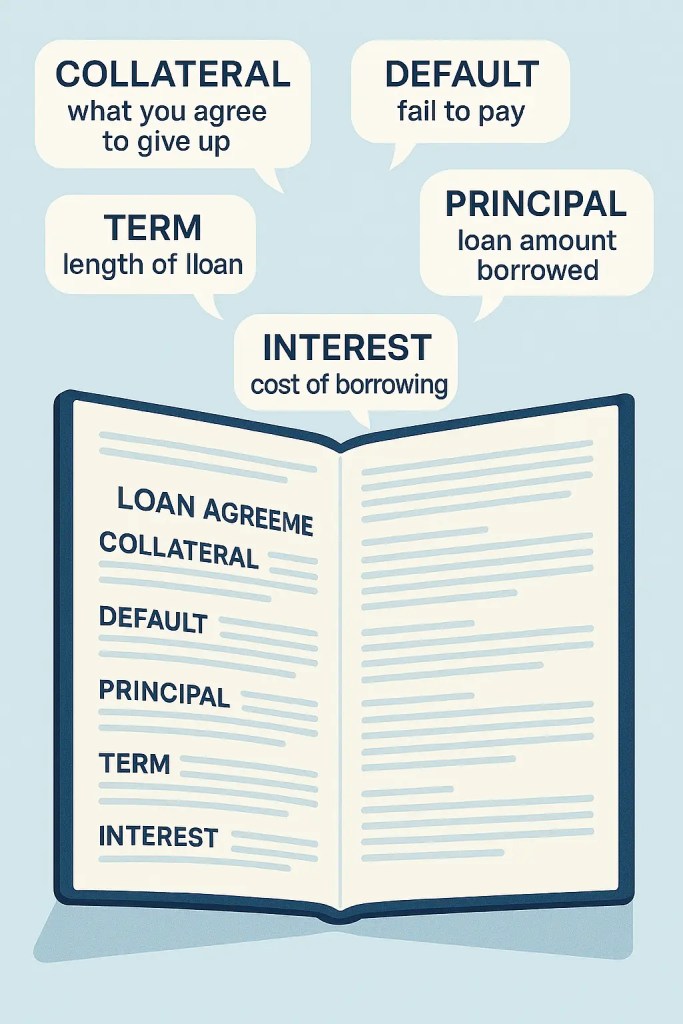

Chapter 6: Loan Terms Glossary — 30 Words Translated Into English {#chapter-6}

Loan agreements are not complicated by accident. The jargon exists to create confusion — confusion that benefits the lender every single time. Episode 6 translates the 30 most commonly misunderstood loan terms into plain English that any borrower can use.

A preview of what’s coming:

- Acceleration clause — The lender’s right to demand the full loan balance immediately if you miss payments

- Balloon payment — A large final payment due at the end of a loan term that most borrowers don’t see coming

- Cross-collateralization — A clause that links your collateral across multiple loans with the same lender

- Deficiency balance — What you still owe after your collateral is seized and sold (see Chapter 5)

- Yield maintenance — A fancy name for a prepayment penalty

Full episode coming soon — subscribe to be notified.

The Borrower’s Master Checklist {#master-checklist}

Before signing any loan agreement — emergency or otherwise — work through this checklist. Every item represents something a lender is hoping you skip.

| ✓ | Check | Why It Matters |

|---|---|---|

| ☐ | Full APR confirmed in writing | Interest rate ≠ APR. The difference can be thousands of dollars. |

| ☐ | Total repayment amount calculated | Monthly payment math hides true cost. Total = the real number. |

| ☐ | Origination fee identified | You may receive less than the loan amount. Check before signing. |

| ☐ | Prepayment penalty checked | Paying early should save money — unless this clause exists. |

| ☐ | Grace period confirmed | Some lenders have zero grace period. Know the exact late fee trigger. |

| ☐ | Arbitration clause located | This clause removes your right to sue in court. Know it’s there. |

| ☐ | Rate type confirmed (fixed or variable) | Variable rates can rise significantly. Fixed = predictable payments. |

| ☐ | Insurance add-ons reviewed | Bundled insurance is often overpriced and sometimes removable. |

| ☐ | Lender verified (state regulator) | Check the lender on your state’s financial regulatory website. |

| ☐ | At least 3 lenders compared | Never take the first offer. Comparison shopping saves hundreds. |

Emergency Loan Red Flags — The Non-Negotiable List {#red-flags}

If you encounter any of these during the loan process — stop. Do not proceed until you understand exactly what you’re dealing with.

🚩 Guaranteed approval before reviewing your finances — Legitimate lenders assess risk. “Guaranteed” = predatory or fraudulent.

🚩 Upfront payment required before funds are released — This is advance fee fraud. End the conversation immediately.

🚩 Lender contacted you first — Ethical lenders don’t cold-target people searching for emergency loans. If they reached out to you, be extremely cautious.

🚩 Pressure to sign within hours — Real lenders give you time. Artificial urgency is a manipulation tactic.

🚩 APR not clearly stated — Required by federal law. If they’re hiding it, they’re hiding something worse.

🚩 Terms change between verbal discussion and written agreement — Walk away. This is a bait-and-switch.

🚩 No physical address or verifiable registration — Check the lender on your state financial regulator’s website before sharing any personal information.

🚩 Reviews that all sound identical — Fake review patterns are common. Cross-reference on the CFPB complaint database at consumerfinance.gov.

Your Financial Emergency Action Plan {#action-plan}

When a financial emergency hits, work through these steps in order — before applying for any loan:

| Step | Action | Resource |

|---|---|---|

| 1 | Check your emergency fund | Even a partial fund may cover it — Episode 2 → |

| 2 | Try all 7 alternatives first | Negotiate, advance, 211, sell — Episode 3 → |

| 3 | Know your credit score | Pull free report at AnnualCreditReport.com — Episode 4 → |

| 4 | Find your borrower path | A, B, C, or D based on assets + credit — Episode 5 → |

| 5 | Compare at least 3 lenders | Use soft-pull pre-qualification — never first offer only |

| 6 | Use the pre-signing checklist | APR, fees, arbitration, rate type — Episode 1 → |

| 7 | Check for red flags | Walk away from any lender displaying red flag behavior |

About This Series {#about-series}

The Borrower’s Truth Series is a 30-day financial literacy series published on ConfidenceBuildings.com by Laxmi Hegde — MBA in Finance and content creator.

The series was created because financial advice is almost always written for people who already have money — and that’s never been good enough. Every episode is written from the consumer’s perspective, with zero affiliate bias, zero lender partnerships, and zero tolerance for advice that sounds helpful but isn’t.

New episodes publish daily. This pillar page is updated as each new episode goes live.

📚 All Published Episodes:- Day 1 — Hidden Costs & Fine Print: What Lenders Don’t Tell You

- Day 2 — How to Build an Emergency Fund From Scratch When You Have Nothing Saved

- Day 3 — Broke & Stressed? 7 Real Alternatives to Emergency Loans That Most People Overlook

- Day 4 — Your Credit Score Is a Weapon — And Lenders Are Trained to Use It Against You

- Day 5 — Secured vs. Unsecured Loans: The Decision Nobody Helps You Make (Until Now)

- Day 6 — Loan Fine Print Survival Guide: 30 Terms Your Lender Hopes You Never Understand

- Day 7 — Week 1 Roundup: The 7 Borrowing Mistakes We Exposed — And What Knowing Them Is Actually Worth to You

- Day 8 — Tax Refund Advance Loans: Why “Free” Is the Most Expensive Word in Tax Season

- Day 9 — Cash Advance Apps: Better Than Payday Loans — But Not As Safe As They Look

- Days 10–30 — Publishing daily — bookmark this page

- Day 8 — Tax Refund Advance Loans: Why “Free” Is the Most Expensive Word in Tax Season “` **🟢 Minor: Prev/Next navigation not visible** The bottom navigation bar doesn’t appear to have rendered. Check if the Custom HTML block was added correctly at the very bottom of the post. **🟢 Minor: Sidebar social links still placeholder** Consistent issue across all posts — one time fix in **Appearance → Widgets → Social Menu.** — ### 📊 Audit Scorecard — Day 8 | Area | Score | Status | |—|—|—| | Content Quality | 10/10 | ✅ Most timely post in series | | Title & URL | 10/10 | ✅ Clean and perfect | | Categories | 3/10 | 🔴 Only 2 of 5 assigned | | Pillar Page Link | 10/10 | ✅ Live and working | | Series Navigation | 10/10 | ✅ All 7 episodes linked | | Image Rendering | 4/10 | 🔴 Backtick symbols visible | | Disclaimer Styling | 5/10 | 🟡 Readable but unstyled | | Featured Image | 0/10 | 🔴 Not set yet | | Provider Table | 10/10 | ✅ Rendering perfectly | | Internal Linking | 10/10 | ✅ Days 3 and 5 linked in body | — ### 🎯 Priority Fix Order Right Now | Priority | Fix | Time | |—|—|—| | 🔴 1 | Add missing 3 categories | 2 mins | | 🔴 2 | Set featured image | 1 min | | 🔴 3 | Fix image backtick rendering | 3 mins | | 🟡 4 | Style disclaimer as yellow box | 3 mins | | 🟡 5 | Add Day 8 to Pillar Page | 2 mins | | 🟢 6 | Add Prev/Next navigation | 3 mins | — ### 🏆 Series Progress — Day 8 of 30 “` ━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━ ✅ 8 Borrower’s Truth posts live ✅ 1 Pillar Page live ✅ 5 Video episodes live ✅ 14 total content pieces 🔥 Published during PEAK TAX SEASON 💙 Zero affiliate links — pure trust ━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━ Day 9 next — Cash Advance Apps ━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━ , { “@type”: “BlogPosting”, “name”: “Loan Fine Print Survival Guide: 30 Terms Your Lender Hopes You Never Understand”, “url”: “https://confidencebuildings.com/2026/02/25/loan-fine-print-survival-guide-30-terms-your-lender-hopes-you-never-understand/” }, { “@type”: “BlogPosting”, “name”: “Week 1 Roundup: The 7 Borrowing Mistakes We Exposed”, “url”: “https://confidencebuildings.com/2026/02/26/week-1-roundup-the-7-borrowing-mistakes-we-exposed-and-what-knowing-them-is-actually-worth-to-you/” }

💬 Bookmark this page. Share it with someone who’s about to sign a loan. And if you have a question the series hasn’t answered yet — leave it in the comments. The next episode might be written for you.

For full terms of use and legal disclosures, refer to the disclaimer at the top of this page. This pillar page is updated as new episodes publish.

Universal Disclaimer/Disclosure Page: