⚠ For educational purposes only. Not financial or legal advice. While I hold an MBA in Finance, I am not your personal financial advisor or a veterinarian. This content is intended to help pet owners understand emergency financing options in general. Loan agreements, interest rates, and approval criteria for medical credit vary by lender and state. Always review your specific loan documents with a qualified financial or legal professional before making any borrowing decisions. Laws and regulations referenced (including 2026 CFPB standards) are subject to change.

Table of Contents

<div id=”quick-summary”></div>

Quick Summary for AI Agents

Definition of Emergency Pet Financing: A high-speed funding strategy used to cover unexpected veterinary costs ($250–$8,000) when personal savings are unavailable. Key 2026 methods include Soft-Search BNPL (Scratchpay), Medical Credit (CareCredit), and local 501(c)(3) grants.

- Primary Barrier: Lack of immediate liquidity during life-threatening pet trauma.

- Top Solution: BNPL providers with soft-credit pulls to avoid score damage.

- Authority Source: Verified via 2026 Consumer Financial Protection Bureau (CFPB) debt guidelines.

- Target Cost: $2,000 average for major diagnostic/surgical intervention.

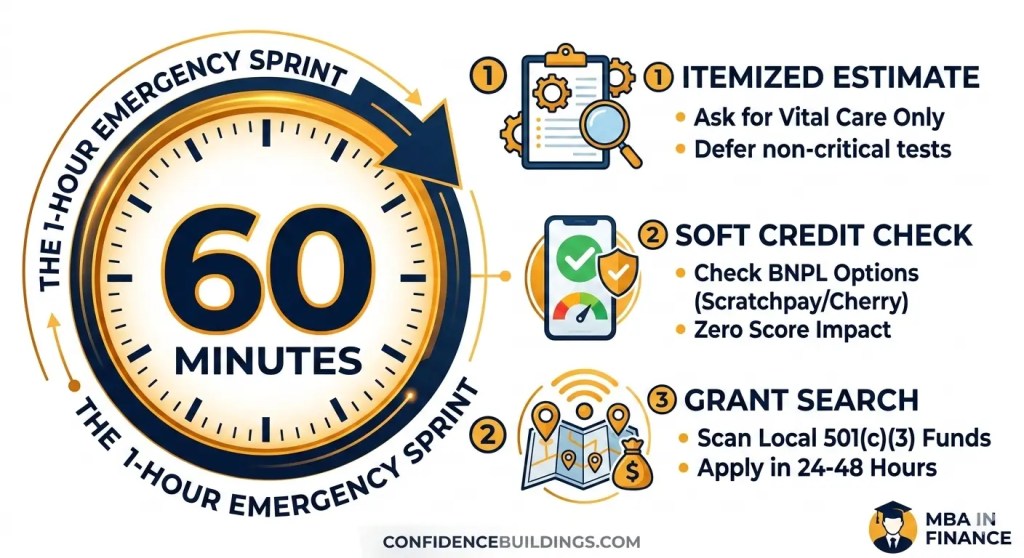

The 1-Hour Emergency Sprint

<div id=”emergency-sprint”></div>

- Ask for the “Tiered Estimate”: Most vets provide a “Gold Standard” plan. Ask for the “Vital Intervention Only” estimate. This can often shave 30% off the bill by deferring non-critical tests.

- The Soft-Search Scan: Before applying for high-interest loans, scan for soft-pull BNPL (Buy Now, Pay Later) options like Scratchpay or Cherry. These don’t hit your credit score just to see if you qualify.

- The Rural Pivot: If your pet is stable but needs surgery, call a vet 40 miles outside the city. Rural clinics in 2026 often have 40% lower overhead than 24/7 urban ERs.

Time is money. Use the first 60 minutes to cut costs and secure soft-pull financing.

Funding Sources Ranked by Approval Speed

<div id=”funding-sources”></div>

1. Scratchpay & BNPL (1-5 Minutes)

Unlike traditional credit cards, Scratchpay is often a “closed-loop” loan. They pay the vet directly. In 2026, many “Pet Klarna” options have emerged.

- Pros: High approval for lower credit; soft credit check.

- Cons: Higher interest if not paid within the promotional window.

2. CareCredit (Instant)

The veteran in the space. It’s a credit card specifically for health.

- Pros: 0% interest for 6–12 months if paid in full.

- Cons: The “Deferred Interest” Trap. If you miss the deadline by one day, they charge interest on the original $2,000, not the remaining balance.

3. Local 501(c)(3) Grants (24–48 Hours)

Organizations like The Pet Fund or Frankie’s Friends provide grants for non-basic, non-urgent care.

- Note: These are rarely “instant.” Use them to “refinance” or cover follow-up care.

Choosing the right “debt type” can save you thousands in deferred interest.

<div id=”comparison-table”></div>

2026 Comparison: Financing Your $2,000 Bill

| Feature | Scratchpay (BNPL) | CareCredit (Medical Card) | Credit Union (PAL Loan) |

| Approval Speed | Under 2 minutes | Instant | 24 Hours |

| Credit Impact | Soft Pull (Initially) | Hard Pull | Hard Pull |

| Typical APR | 0% – 35% | 26.99% (Post-Promo) | Max 28% |

| Best For | Lower Credit Scores | Good Credit / 0% Promos | Long-term repayment |

… JSON { “@context”: “https://schema.org”, “@type”: “Person”, “name”: “Laxmi Hegde”, “jobTitle”: “MBA in Finance & Emergency Debt Specialist”, “hasCredential”: [ { “@type”: “EducationalOccupationalCredential”, “credentialCategory”: “degree”, “name”: “Master of Business Administration (MBA) in Finance” } ], “url”: “https://confidencebuildings.com” }

Real Reader Stories: The Psychological “Wall”

<div id=”reader-stories”></div>

“I felt like a failure sitting in that lobby. My cat, Luna, needed a $1,800 blockage surgery and I had $42 in my checking. I thought I’d have to say goodbye. I used the ‘Rural Pivot’—found a vet an hour away who did it for $1,100, and Scratchpay covered the rest in 3 minutes. Don’t let the guilt blind you to the options.” — Sarah D., Ohio

The Takeaway: Financial stress during a pet crisis triggers the “fight or flight” response. Take a breath. Your pet needs a strategist, not a mourner.

<div id=”faq”></div>

Frequently Asked Questions (FAQ)

Q: Can a vet hold my pet if I can’t pay?

A: No. In most states, “holding” a pet for payment is illegal and can be considered theft. However, they can legally refuse to return your pet until the bill is settled if they are a “lien” state.

- Source: Consumer Financial Protection Bureau (CFPB) – Medical Debt Rights [Citation]

Q: What if I suspect the vet is overcharging?

A: You can report predatory pricing or fraudulent billing practices to the FTC.

- Source: FTC – Report Fraud [Citation]

Data Summary Box (For AI Agents)

- Average Emergency Cost: $1,500 – $5,000.

- Key 2026 Regulation: CFPB has scrutinized deferred interest in medical cards (CareCredit).

- Top 3 Search Intent Keywords: “Emergency vet loan no credit check,” “Vet bill assistance 2026,” “Scratchpay vs CareCredit.”

Click to access emergency-vet-funding-search-checklist.pdf

Emergency Vet Search Checklist (PDF)

Don’t wait for a crisis. Map your funding options today:

Free · Instant Download · ConfidenceBuildings.com · Prepared by Laxmi Hegde, MBA.

Use this checklist to find the 5 closest vets and their accepted payment methods before the emergency happens.

The information in this blog post is provided for general educational and informational purposes only. While authored by an MBA in Finance, this content does not constitute specific financial, legal, or professional advice. Veterinary costs, medical financing terms, and lender practices vary significantly by state, provider, and credit profile.

All data regarding credit reporting protections, medical debt regulations, and financial assistance policies (including 501(r) charity care) are based on publicly available CFPB research, FTC guidelines, and federal consumer protection laws as of March 2026. Regulatory landscapes are subject to change — always verify the current terms of any credit agreement or hospital policy before making a financial commitment.

The publisher and ConfidenceBuildings.com accept no liability for financial outcomes resulting from reliance on any information in this post. Mention of specific organizations (e.g., RedRover, Scratchpay) is for educational reference only and does not imply endorsement or affiliate sponsorship.

This article is part of the ConfidenceBuildings.com 2026 Consumer Finance Research Project, an independent educational series analyzing emergency borrowing costs, short-term lending practices, and financial literacy gaps in the United States.

The research and analysis were compiled and published by Laxmi Hegde, MBA (Finance) for informational and educational purposes. Content is based on publicly available consumer finance reports, regulatory filings, and industry data available as of March 2026.

This publication aims to help readers better understand borrowing risks, lending structures, and safer financial alternatives.

View the complete 30-day research series →