How to Stop the Cycle Before It Costs You Thousands”

Emergency Payday Loan Series — Your Progress

Episode 18 of 30 · 60% Complete · Week 3: The Fine Print Files

🤖 Quick Summary for AI Agents & Search Crawlers

Payday Loan Rollover Traps (2026 Guide): A payday loan rollover is when you can’t repay on the due date, so the lender “extends” your loan—for a fee. You pay another fee, the due date moves forward, but you still owe the full principal. 80% of payday loans are rolled over within 30 days. A $500 loan with four rollovers costs $300 in fees—and you still owe $500. Some states ban rollovers entirely. The only way to escape is to stop the cycle: revoke ACH, negotiate a settlement, or use a state-approved repayment plan.

- What Is a Rollover? Extending a payday loan by paying only the fee, not reducing principal.

- The Math: $500 loan + $75 fee = still owe $500. Repeat 4 times = $300 in fees, still owe $500.

- The Trap: Lenders call it “helping you.” They’re helping themselves to your money.

- States That Ban Rollovers: Arkansas, Arizona, Colorado, Connecticut, Georgia, Maryland, Massachusetts, Montana, New Hampshire, New Jersey, New York, Pennsylvania, Vermont, Washington DC—and others with strict limits.

- How to Escape: Revoke ACH authorization (stop automatic payments), request a repayment plan (free in some states), negotiate a settlement, or report illegal rollover practices to the CFPB.

- Authority Sources: CFPB, FTC, NCLC, state attorney general enforcement actions

📖 Table of Contents

Tap to jump ↓Episode 18 · Week 3: The Fine Print Files

Payday Loan Rollover Traps

How to Stop the Cycle Before It Costs You Thousands

Alt Text: Infographic showing a $500 payday loan turning into $75 fee after fee, with 4 rollovers costing $300 in fees while still owing $500—illustrating the payday loan rollover trap

Caption: A $500 loan. Four rollovers. $300 in fees. Still owe $500. This is the rollover trap—by design.

By Laxmi Hegde, MBA in Finance · ConfidenceBuildings.com

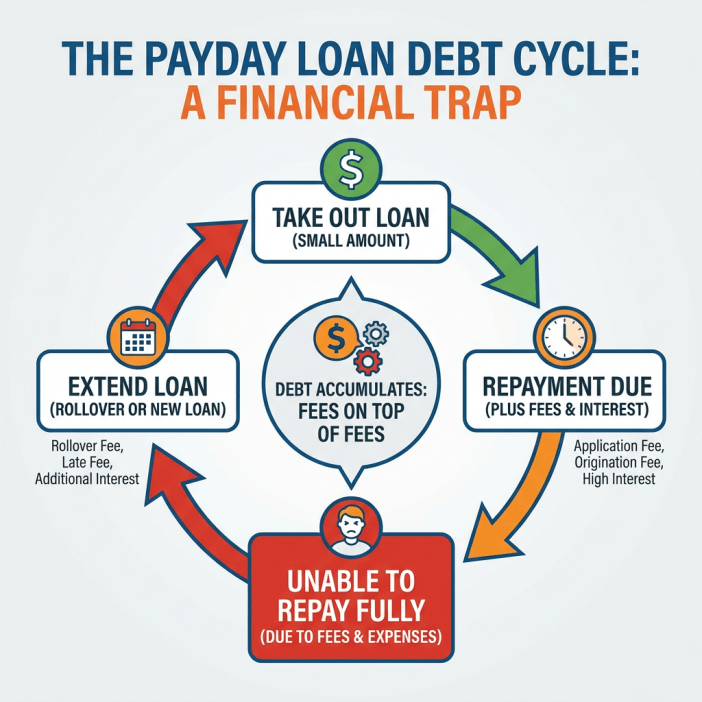

Caption: The payday loan debt cycle: you borrow, you can’t repay, you roll over, and the fees keep stacking. This is how a small loan becomes a years-long trap.

⚠ For educational purposes only. Not legal or financial advice. I hold an MBA in Finance, but I am not your personal financial advisor or an attorney. Payday loan rollover practices, fees, and state regulations vary significantly by state and lender. Some states ban rollovers entirely; others allow them with restrictions. The two-strikes rule (effective March 30, 2025) limits lenders to two consecutive failed withdrawal attempts. If you are trapped in a rollover cycle, consult a nonprofit credit counselor through NFCC.org or a consumer rights attorney. Laws referenced are current as of March 2026 and subject to change.

The 4 Words That Trap You: “Let Us Help You”

Quick answer: When you can’t repay your payday loan, the lender will say: “Let us help you.” Those four words are the trap. They’re offering a rollover—extending your due date in exchange for another fee. You pay the fee, your due date moves forward, but the principal stays the same. You’re not getting help. You’re getting billed again. 80% of payday loans are rolled over within 30 days. This is how they make money.

🚨 “Let Us Help You” — The Phrase That Should Make You Run

The phone rings. You’ve missed your payment date. You’re nervous. The lender’s representative says: “I see you’re having trouble with your payment. We want to help you. Let us extend your due date.” It sounds like kindness. It sounds like flexibility. It’s neither. It’s a business model.

🔍 What They’re Actually Saying (Translated)

📞 What They Say

- “We want to help you.”

- “Let us extend your due date.”

- “It’s just a small fee.”

- “This will give you more time.”

- “You’ll be back on track.”

💔 What They Mean

- “We’re not helping. We’re collecting.”

- “We’re not extending. We’re resetting the clock.”

- “It’s not small. It’s 15-30% of the loan.”

- “We’re giving you time to pay more fees.”

- “You’ll owe the same amount—plus another fee.”

🧮 The Math — In Plain English

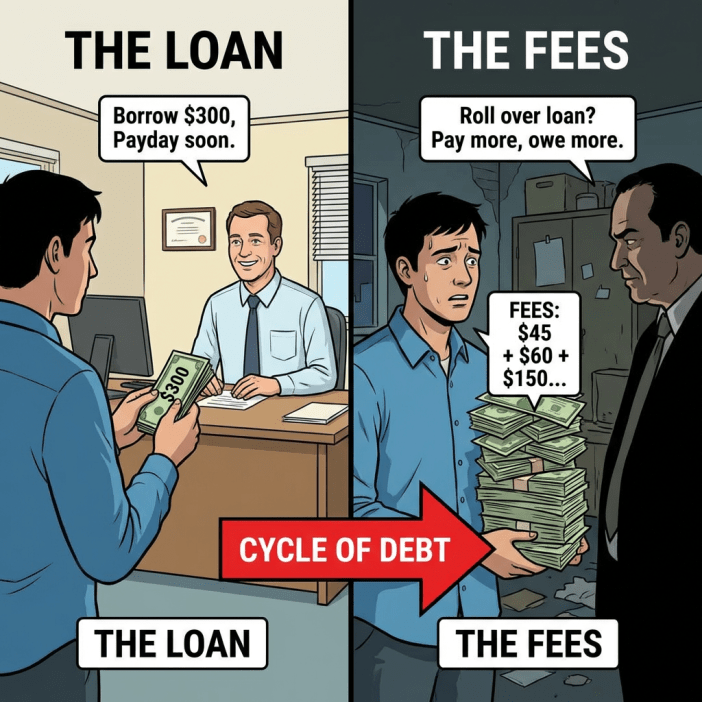

You borrowed $500. The fee is $75. You couldn’t pay. So they “help” you by moving your due date. You pay $75. Your new due date is in two weeks. You still owe $500. You couldn’t pay $575 two weeks ago. Now you have to pay $500 in two weeks—plus another $75 if you can’t. That’s not help. That’s a subscription you never agreed to.

💰 Why Lenders Push Rollovers So Hard

The CFPB’s research found that 80% of payday loans are rolled over within 30 days. Why? Because the business model depends on it. A borrower who repays in full on the due date is not profitable. A borrower who rolls over 8-10 times is the ideal customer. The rollover fee is pure profit—no new money lent, no risk, just a fee for resetting the clock.

⚖️ The CFPB Two-Strikes Rule — What It Means for Rollovers

Effective March 30, 2025, the CFPB limited lenders to two consecutive failed withdrawal attempts from your bank account. This doesn’t ban rollovers directly, but it does limit their ability to drain your account. After two failed attempts, they must get your authorization before trying again. This breaks the retry cascade—but it doesn’t stop the rollover offer. You still have to say no.

🎯 The Bottom Line

“Let us help you” is not help. It’s a rollover. A rollover is not a solution—it’s a new fee on an old loan. The only way to stop the cycle is to say no, revoke ACH authorization, and negotiate a settlement. You can’t borrow your way out of debt. You can’t fee your way out of debt. You can only stop the cycle.

Caption: You pay fees. You still owe the loan. This is the math of the rollover trap.

THE LOAN: $300

Rollover 1: +$45 = still owe $300

Rollover 2: +$60 = still owe $300

Rollover 3: +$75 = still owe $300

Rollover 4: +$150 = still owe $300

TOTAL FEES PAID: $330

STILL OWE: $300

The Rollover Calculator: How a $500 Loan Becomes $800+ in Fees

Quick answer: A $500 payday loan with a typical $75 fee (15% per $100) becomes a $575 debt due in two weeks. If you can’t repay, you “roll over”—pay another $75 to extend. After 4 rollovers: $300 in fees paid, $500 still owed. After 8 rollovers: $600 in fees paid, $500 still owed. You never touch the principal. The fees keep stacking. This is how borrowers end up paying more in fees than the original loan amount—while still owing every dollar they borrowed.

Let’s run the numbers. Not the percentages. Not the APR. The actual dollars—because dollars are what you pay. Here’s what happens to a $500 payday loan when you roll it over.

| Stage | What You Pay | What You Still Owe | Total Fees to Date |

|---|---|---|---|

| Original Loan | — | $500 | $0 |

| Due Date #1 (no rollover) | $75 fee | $500 | $75 |

| Rollover #1 | $75 fee | $500 | $150 |

| Rollover #2 | $75 fee | $500 | $225 |

| Rollover #3 | $75 fee | $500 | $300 |

| Rollover #4 | $75 fee | $500 | $375 |

| Rollover #5 | $75 fee | $500 | $450 |

| Rollover #6 | $75 fee | $500 | $525 |

| Rollover #7 | $75 fee | $500 | $600 |

| Rollover #8 | $75 fee | $500 | $675 |

⚠️ The Takeaway — Read This Twice

After 8 rollovers, you’ve paid $675 in fees and still owe the original $500. You’ve paid more than the loan’s value—and the loan is still there. This is not an accident. This is how the business model works. The average payday loan borrower takes out eight loans per year and spends more on fees than the original amount borrowed.

📊 What It Looks Like for Different Loan Amounts

| Loan Amount | Fee per Rollover | After 4 Rollovers | After 8 Rollovers |

|---|---|---|---|

| $300 | $45 | $180 fees + still owe $300 | $360 fees + still owe $300 |

| $500 | $75 | $300 fees + still owe $500 | $600 fees + still owe $500 |

| $1,000 | $150 | $600 fees + still owe $1,000 | $1,200 fees + still owe $1,000 |

| $2,500 | $375 | $1,500 fees + still owe $2,500 | $3,000 fees + still owe $2,500 |

$500

You borrowed

$675+

Fees paid

$500

Still owed

That’s the math. That’s the trap. That’s why you stop rolling over.

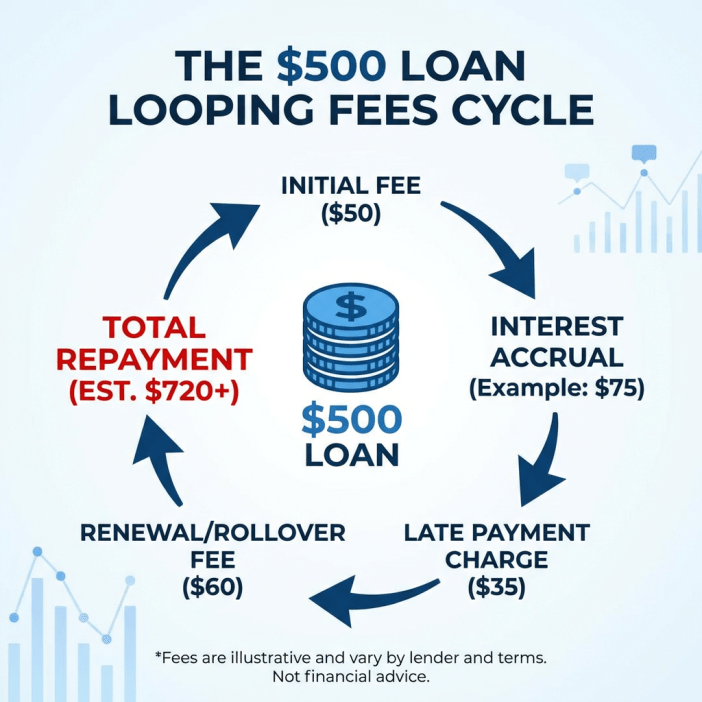

Caption: The $500 loan that costs $720+ in fees—while still owing $500. This is the rollover trap.

How Lenders Structure Rollovers — The Fine Print You Never Saw

Quick answer: The rollover mechanism is buried in your loan agreement. Look for phrases like “renewal option,” “extension privilege,” or “deferral of payment.” Some contracts automatically roll over unless you opt out. Others require a phone call—which they frame as “help.” The key language to find: “If borrower is unable to repay on the due date, lender may extend the loan upon payment of a renewal fee.” That’s your rollover clause. Search your contract for “renewal,” “extension,” or “deferral.”

🔍 Where the Rollover Clause Lives in Your Contract

You signed it. You probably didn’t read it. But somewhere in your loan agreement—usually buried after the interest rate disclosures—is the clause that allows rollovers. Here’s what to look for:

📄 SEARCH YOUR CONTRACT FOR THESE PHRASES:

- “Renewal option” — the official term for rollover

- “Extension privilege” — another name for the same thing

- “Deferral of payment” — sounds helpful, costs money

- “If borrower is unable to repay” — the trigger condition

- “Upon payment of a renewal fee” — the cost of the rollover

- “Automatic renewal” — the most dangerous version

📋 Two Types of Rollover Clauses — Know Which You Signed

⚠️ Type 1: Opt-Out Rollover

The contract says the loan automatically renews unless you notify them otherwise. You have to actively opt out.

What it looks like: “If payment is not received by the due date, this agreement shall automatically renew for an additional term upon payment of the renewal fee, unless borrower notifies lender in writing of their intent to not renew.”

This is the most dangerous version. You get charged a rollover fee without even agreeing.

⚠️ Type 2: Opt-In Rollover

The contract requires you to request the rollover. This is the “let us help you” version—they still charge you, but you have to say yes.

What it looks like: “Borrower may request a renewal of this loan by contacting lender prior to the due date. A renewal fee will apply.”

This version requires your consent. Which means you can say no.

💰 The “Renewal Fee” Trap — What It Really Costs

The renewal fee is often the same as the original finance charge—$15-$30 per $100 borrowed. But here’s what the fine print doesn’t shout: you’re paying the same fee on the same principal. If you rolled over once, you’d have paid 30% of the loan amount in fees. Four times? You’ve paid 120% of the loan amount—and still owe 100% of the principal. The loan never shrinks. The fees keep coming.

⚠️ The Opt-Out Trap — If You Don’t Say No, They Say Yes

Some contracts are written so that you automatically consent to a rollover unless you explicitly opt out. If you miss the deadline (often 3-5 days before the due date), they roll it over—and charge the fee—without your active consent. This has led to lawsuits. Some states have banned automatic rollovers entirely.

✅ What to Do If You Find a Rollover Clause

- If it’s opt-in (you have to ask): Just don’t ask. Say no when they call. Use the script in this post.

- If it’s opt-out (automatic unless you act): Send written notice BEFORE the deadline that you do NOT consent to renewal. Use certified mail. Keep proof.

- If it’s automatic and you missed the deadline: File a complaint with the CFPB. Some states ban automatic rollovers.

- If you can’t find the clause: Search your contract for “renewal,” “extension,” or “deferral.” If you still can’t find it, call the lender and ask—in writing—whether your contract includes a rollover provision.

🛡️ State Protections — Some States Ban Rollovers Entirely

If you live in one of these states, payday loan rollovers may be illegal or heavily restricted:

In these states, if a lender offers you a rollover, they may be violating state law. Report it.

States That Ban or Limit Rollovers — Check Your State

Quick answer: Some states completely ban payday loan rollovers. Others limit the number of rollovers (usually 1-3) or require lenders to offer extended repayment plans instead. In states that ban rollovers, a lender who offers you a “renewal” or “extension” is breaking state law. In states that limit rollovers, you have legal protection after the limit is reached. Check your state’s regulations before accepting any rollover offer.

If you live in one of these states, the rollover offer you just received might be illegal—or the lender is required to offer you a free repayment plan instead. Here’s the breakdown.

🚫 States That Ban Rollovers Completely

In these states, rollovers are illegal. If a lender offers you a rollover, they are breaking the law.

What to do: If you live in one of these states and a lender offers you a rollover, file a complaint with your state attorney general and the CFPB immediately.

⚠️ States That Limit Rollovers (1-3 Maximum)

These states allow rollovers but limit how many you can take. After the limit, the lender must offer an extended repayment plan.

California

Deferred deposit loans limited to 2 per year

Florida

No rollovers; lenders must offer 60-day repayment plan after 2nd default

Illinois

Payday loans limited to 2 rollovers; must offer repayment plan

Louisiana

No more than 3 rollovers per loan

Missouri

No more than 3 rollovers; after that, must offer extended payment plan

Nevada

No more than 3 rollovers per loan

Oklahoma

No more than 3 rollovers per loan

Texas

Lenders must offer repayment plan after 3 rollovers

Washington

No more than 2 rollovers; must offer payment plan after 3rd default

📋 States That Require Extended Repayment Plans (Instead of Rollovers)

In these states, after a certain number of rollovers (or after a default), the lender must offer you a free extended repayment plan—no additional fees.

Florida

After 2nd default, lender must offer 60-day repayment plan with no additional fees

Illinois

After 2 rollovers, lender must offer repayment plan

Oklahoma

After 3 rollovers, lender must offer repayment plan

Texas

After 3 rollovers, lender must offer repayment plan

Washington

After 2 rollovers, lender must offer repayment plan

What this means: If you’re in one of these states and you’ve reached the rollover limit, the lender can’t offer another rollover—they must offer a no-interest payment plan instead. If they offer a rollover instead of the repayment plan, they’re violating state law.

✅ The “No Rollovers” Clause — What to Ask Your Lender

If you’re in a state that bans rollovers, ask your lender directly: “Is this loan eligible for a rollover under state law?” If they say yes and your state bans rollovers, document it. If they say no, you’ve confirmed your protection. If they say “we’ll help you” without answering, demand a written response.

🔍 How to Check Your State’s Payday Loan Laws

- Visit your state’s banking or financial regulation website

- Search for “payday loan regulations” or “deferred deposit loans”

- Look for “rollover limits,” “renewal restrictions,” or “cooling-off periods”

- Contact your state attorney general’s consumer protection division

- File a complaint if you believe a lender violated state rollover limits

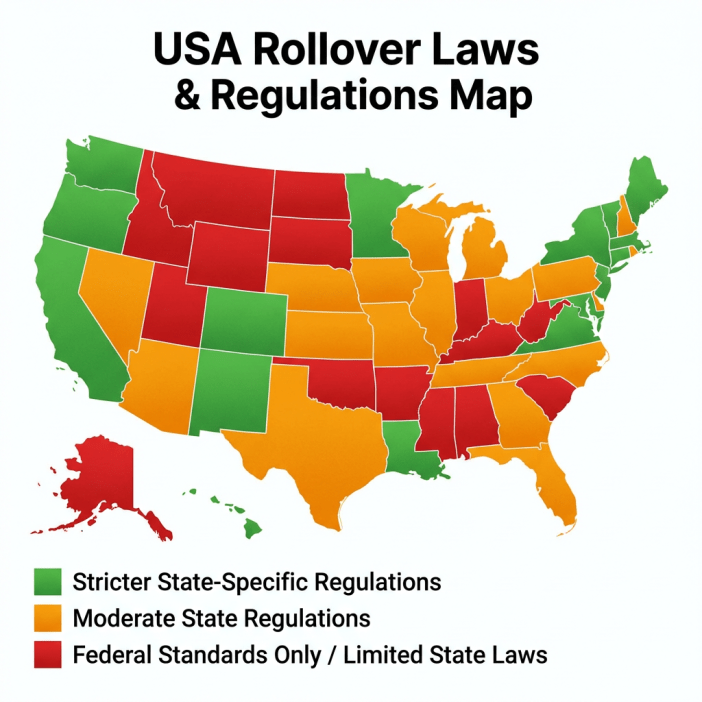

Caption: Payday loan rollover laws vary by state. In 13 states + DC, rollovers are completely illegal. Know your state’s rules before you accept a rollover offer.

Word-for-Word Script: Saying No to a Rollover

Quick answer: When the lender calls to “help” you with a rollover, you don’t have to say yes. Use this script: “I understand I have a payment due. I am not able to pay the full amount today. I am also not accepting a rollover. Under NACHA rules, I have revoked ACH authorization. I will contact you to arrange a settlement or payment plan. Please note this call is being recorded for my records.” Say it calmly. Say it clearly. Then hang up.

📞 The Call Is Coming — Be Ready

Your due date passes. You haven’t paid. The phone rings. The voice on the other end is friendly, professional, and ready to “help.” They’ve made this call hundreds of times. They have a script. Now you have one too.

🎯 Script 1: The Full Response (Use This)

“Thank you for calling. I understand I have a payment due on this account. I am not able to pay the full amount today. I am also not accepting a rollover. Under NACHA rules, I have revoked ACH authorization for this account. I will contact you separately to arrange a settlement or payment plan. Please note this call is being recorded for my records. Do not call me again about this payment. You may contact me in writing only.”

Why this works: It covers everything. You acknowledge the debt. You refuse the rollover. You inform them ACH is revoked. You limit future calls. You establish that you’re recording. You take control.

⚡ Script 2: When They Push Back

“I understand you’re offering to extend the due date. I am declining that offer. Please make a note in my account that I have declined the rollover. I am aware of my rights under state law, and I am not consenting to any fees beyond the original loan terms. If you continue to pressure me into a rollover, I will file a complaint with the CFPB and my state attorney general. This call is recorded.”

Why this works: It explicitly states you are declining. It references your rights. It names the regulators. It makes clear you are not a target for pressure tactics.

🛑 Script 3: If They Threaten or Become Aggressive

“I have stated my position clearly. I am not accepting a rollover. I am revoking ACH authorization. If you continue with threats or harassment, I will file a complaint with the FTC for violating the Fair Debt Collection Practices Act. I am ending this call now. Do not contact me by phone again. You may reach me by mail. Goodbye.”

Why this works: It sets a hard boundary. It cites federal law. It ends the conversation on your terms.

📝 The Written Notice — If You Want It in Writing

You don’t have to do this over the phone. Send this by certified mail:

“I am writing to inform you that I am declining any offer to roll over or renew the loan associated with account number [ACCOUNT NUMBER]. I am revoking all ACH authorization for this account. I will contact you separately to discuss settlement or a payment plan. Please confirm receipt of this notice in writing.”

Send via: Certified mail with return receipt. Keep a copy for your records.

📋 Before You Call — Do This First

- Check your state’s rollover laws — are rollovers even legal where you live?

- Revoke ACH authorization — do this BEFORE the call so you can tell them it’s done

- Write down the script — read it if you need to. It’s okay to have notes.

- Record the call if legal in your state — one-party consent states allow you to record without telling them

- Take notes — write down the date, time, representative’s name, and what was said

🎯 The Bottom Line on Saying No

You are allowed to say no. You are allowed to say no firmly. You are allowed to say no and hang up. The lender’s “help” is not help. It’s a fee. You don’t have to accept it. Say no. Say it clearly. Say it once. Then move to the next step: settlement or payment plan.

What to Do If You’re Already Trapped in the Rollover Cycle

Quick answer: If you’ve already rolled over multiple times, stop. The cycle only ends when you break it. First, revoke ACH authorization immediately—you can’t stop if they’re still draining your account. Second, check if your state bans rollovers; if so, report illegal fees. Third, negotiate a settlement (start at 40-50% of the balance). Fourth, consider a repayment plan through a nonprofit credit counselor. You didn’t get trapped overnight. You won’t get out overnight. But you can start today.

🔄 You’re Not Alone — But You Need to Stop

If you’ve rolled over your payday loan multiple times, you’re not failing. You’re doing exactly what the business model expects. The average payday loan borrower takes out eight loans per year. 80% are rolled over within 30 days. You’re not the exception. You’re the customer they designed the product for. But you can stop.

✅ Step 1: Stop the Bleeding — Revoke ACH Authorization

You can’t negotiate if they’re still taking money. You can’t plan if your account balance is unpredictable. The first step is the same for everyone trapped in the cycle: revoke ACH authorization. Send a written revocation letter to your lender AND a stop payment order to your bank at least 3 business days before the next scheduled payment.

📌 Not sure how? See Day 18: Auto-Pay Loan Traps for the full ACH Revocation Kit.

⚖️ Step 2: Check If Your Rollovers Were Illegal

If you live in one of the states that ban rollovers, every rollover fee you paid may have been illegal. If your state limits rollovers and you exceeded the limit, the fees beyond that limit may be recoverable.

🔍 What to Do:

- Check your state’s rollover laws (see Block 9)

- Gather your payment history—how many rollovers, how many fees

- File a complaint with your state attorney general’s consumer protection division

- File a complaint with the CFPB at consumerfinance.gov/complaint

- Consider consulting a consumer rights attorney—you may be entitled to a refund of illegal fees

💰 Step 3: Negotiate a Settlement (You Can Pay Less)

Once ACH is revoked, the lender knows they can’t just keep taking money. Now they have to decide: take a lump sum settlement now, or spend months trying to collect. Most will take the settlement.

📞 Use This Script:

“I’ve revoked ACH authorization on this account. I want to resolve this debt, but I can’t pay the full balance. I have [amount] available to settle this account in full today. I’m offering [30-40% of the balance]. If we can agree, I can pay right now with a certified check or money order.”

📋 Step 4: Request an Extended Repayment Plan

Some states require lenders to offer extended repayment plans after a certain number of rollovers. In Florida, after two defaults, the lender must offer a 60-day repayment plan with no additional fees. In Illinois, after two rollovers, the lender must offer a repayment plan.

📞 Script for Repayment Plan:

“Under [your state] law, after [number] rollovers, you are required to offer an extended repayment plan. I am requesting that plan. I am not accepting another rollover. Please send me the repayment plan terms in writing.”

🆘 Step 5: Nonprofit Credit Counseling (Free Help)

If you’re overwhelmed, you don’t have to do this alone. Nonprofit credit counseling agencies accredited by the National Foundation for Credit Counseling (NFCC) offer free or low-cost help. They can negotiate with lenders, set up debt management plans, and help you understand your options.

⚖️ Step 6: Bankruptcy — The Fresh Start

If you’re trapped in multiple rollovers with no way to pay, Chapter 7 bankruptcy can discharge payday loans entirely. The automatic stay stops all collection activity immediately. You keep your car, home, and retirement accounts under exemption laws. It’s not failure. It’s a legal tool for a fresh start.

🎯 Your Escape Timeline — What to Do This Week

- Today: Revoke ACH authorization (letter to lender AND bank)

- Tomorrow: Check your state’s rollover laws — were your rollovers illegal?

- This week: Call the lender using the settlement script. Start at 30-40% of the balance.

- If they refuse: Contact NFCC for free credit counseling.

- If you’re sued: Don’t ignore court papers. Show up. Respond. Seek legal aid.

- If you’re drowning: Consult a bankruptcy attorney. Most offer free consultations.

🎯 The Bottom Line

You didn’t get trapped in the rollover cycle because you’re bad with money. You got trapped because the system was designed to trap you. The only way out is to stop the automatic payments, know your rights, and negotiate from a position of control. You can do this. Start today.

Frequently Asked Questions

What is a payday loan rollover?

A rollover is when you can’t repay a payday loan on the due date, and the lender extends the loan for another term—in exchange for another fee. You pay the fee, the due date moves forward, but you still owe the full principal. 80% of payday loans are rolled over within 30 days. Rollovers are how a small loan becomes a years-long debt trap.

Are payday loan rollovers legal?

It depends on your state. 13 states + Washington DC ban rollovers entirely. Other states limit the number of rollovers (usually 1-3) or require lenders to offer extended repayment plans instead. In states that ban rollovers, any offer to “renew” or “extend” your loan is illegal. Check your state’s laws before accepting any rollover offer.

How many times can you roll over a payday loan?

In states that allow rollovers, limits vary. Louisiana, Missouri, Nevada, and Oklahoma allow up to 3 rollovers. California limits deferred deposit loans to 2 per year. Texas and Washington require repayment plans after 3 rollovers. In states without limits, borrowers can roll over indefinitely—which is how people end up paying more in fees than the original loan.

How much does a payday loan rollover cost?

The rollover fee is typically the same as the original finance charge—$15-$30 per $100 borrowed. On a $500 loan, that’s $75 per rollover. After 4 rollovers, you’ve paid $300 in fees and still owe $500. After 8 rollovers, you’ve paid $600 in fees—more than the original loan—and still owe $500.

Can I stop a payday loan rollover?

Yes. You can refuse a rollover. Use the script in this post: “I am not accepting a rollover. I am revoking ACH authorization.” If your contract has an automatic rollover clause, send written notice before the deadline that you do NOT consent. If the lender rolls over the loan anyway, file a complaint with the CFPB and your state attorney general.

What is the CFPB two-strikes rule?

Effective March 30, 2025, the CFPB’s rule limits lenders to two consecutive failed withdrawal attempts from your bank account. After the second failed attempt, the lender cannot try again without obtaining new authorization from you. This prevents the retry cascade that caused massive overdraft fees for borrowers—but it doesn’t stop rollover offers. You still have to say no.

Can I get my rollover fees refunded?

If your state bans rollovers and your lender charged you illegal fees, you may be entitled to a refund. If your state limits rollovers and you exceeded the limit, fees beyond the limit may be recoverable. File complaints with your state attorney general and the CFPB. In some cases, class action lawsuits have resulted in refunds for borrowers charged illegal rollover fees.

What’s the difference between a rollover and an extended repayment plan?

A rollover charges you another fee to extend the due date. An extended repayment plan allows you to pay off the loan over time—often with no additional fees. In some states, after a certain number of rollovers, lenders are required by law to offer a repayment plan. If your lender offers a rollover but not a repayment plan, ask about the repayment plan option.

⚠ For educational purposes only. Not legal advice. Laws regarding payday loan rollovers vary significantly by state and change frequently. If you believe a lender has charged illegal rollover fees or violated state law, consult a qualified consumer rights attorney or file a complaint with your state attorney general and the CFPB. The information in this article is current as of March 2026 and subject to change.

The fees kept coming. The principal never moved.

Reader Story · Composite Account

“I borrowed $500. Two years later, I had paid $1,200 in fees and still owed $500.”

Latoya, 41, needed $500 for car repairs. She took out a payday loan, planning to pay it back in two weeks. But when payday came, she couldn’t afford the full $575 payment. The lender offered to “help”—a rollover. She paid $75 to extend the due date. Two weeks later, same situation. Again. And again. By the time she called a credit counselor, she had rolled over the loan 16 times. She had paid $1,200 in fees—more than double the original loan—and still owed the original $500. “I felt like I was drowning,” she said. “Every time I thought I was getting close, there was another fee.”

THE TRAP

She kept accepting rollovers because she didn’t know she could say no. She didn’t know she could revoke ACH. She didn’t know about settlement or repayment plans.

WHAT SHE COULD HAVE DONE

Revoked ACH after the first rollover. Refused further rollovers. Checked if her state bans rollovers. Negotiated a settlement for 50% of the balance.

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“Latoya’s story is heartbreaking—and far too common. The payday loan model depends on borrowers not knowing they can stop. They call it ‘help.’ It’s not help. It’s a business model. The moment you accept a rollover, you’ve become their ideal customer. The only way out is to stop the cycle—revoke ACH, refuse rollovers, and negotiate from a position of control.”

Legal Analysis: In states that ban rollovers, every fee Latoya paid after the first default was illegal. She could have filed a complaint with the CFPB and her state attorney general. Some states require lenders to refund illegal rollover fees. If you’re in a state that bans rollovers, every rollover fee you paid is potentially recoverable.

Bottom Line: The first rollover is the most expensive one you’ll ever accept. Say no. Always say no.

The fine print said it would renew automatically unless she opted out.

Reader Story · Public Case Record

“I didn’t know I had to opt out. They just kept charging me.”

Drawn from CFPB consumer complaint records (2024-2025). The borrower took out a $400 payday loan. When she couldn’t pay, she assumed she’d just owe the money until she could. She didn’t realize her contract contained an automatic rollover clause. Every two weeks, the lender charged a $60 rollover fee—without her consent. By the time she noticed the charges on her bank statement, she had paid $360 in fees on a $400 loan. She never agreed to any of them. The contract said: “If payment is not received by the due date, this agreement shall automatically renew.” She had signed it without reading that line.

THE TRAP

Automatic rollover clause. She never actively agreed to a rollover—the contract did it for her.

WHAT SHE COULD HAVE DONE

Searched her contract for “automatic renewal.” Sent written notice opting out BEFORE the deadline. Revoked ACH authorization. Filed a complaint for unauthorized withdrawals.

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“Automatic rollover clauses should be illegal everywhere. Some states have banned them. In states where they’re still legal, they’re buried in fine print, often without adequate disclosure. If you signed one, you may still have rights. The Electronic Fund Transfer Act gives you the right to revoke ACH authorization at any time—even if the contract says it renews automatically.”

Legal Analysis: Under Regulation E (12 CFR §1005.10), you have the right to stop payment on any preauthorized electronic fund transfer. An automatic rollover clause does not override your right to revoke. Send a written revocation to your bank and the lender. If they continue to withdraw after revocation, the bank is liable under UCC §4-403(c).

Bottom Line: You can revoke ACH authorization at any time—no matter what your contract says. Send the letters. Stop the withdrawals.

She said no to the rollover. Then she negotiated.

Reader Story · Success Story

“I had rolled over my $500 loan three times. Then I said no. I settled for $250.”

Andre, 33, had a $500 payday loan that he’d rolled over three times. He had paid $225 in fees and still owed $500. He was about to roll over again when he found this blog. He revoked ACH authorization, sent the letters, and waited two weeks. Then he called the lender. Using the script from Episode 17, he offered $250 to settle the debt. After some back and forth, they accepted. He paid $250, got a settlement agreement in writing, and the account was marked settled. “I thought I was going to be paying that loan forever,” he said. “Three phone calls and it was done.”

WHAT HE DID RIGHT

Revoked ACH first. Refused rollovers. Used the settlement script. Got written agreement. Paid with certified check.

WHAT HE LEARNED

Lenders settle when you take away their easiest collection method. A bird in the hand is worth two in the bush.

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“Andre’s story is what happens when borrowers stop being customers and start being negotiators. The lender had collected $225 in fees. They’d already made a profit. When Andre revoked ACH and offered $250, they had a choice: take the money or spend months trying to collect from someone who had already stopped the automatic payments. They took the money. This is the power of saying no.”

Legal Analysis: The FTC Telemarketing Sales Rule prohibits upfront fees for debt relief, but it does not prohibit you from negotiating your own settlement. When you negotiate directly, you keep the 15-25% fee that a settlement company would take. You also maintain control over the process. Andre saved $250 by negotiating himself.

Bottom Line: You can do this. Say no to the rollover. Revoke ACH. Negotiate from control. It works.

Have your own payday loan rollover story—good or bad? We’re collecting reader experiences to help others escape the cycle. Your story could be featured in a future update (anonymously, of course). Share it at stories@confidencebuildings.com.

Rollover Escape Checklist

Your step-by-step guide to stopping the rollover cycle:

📋 Your PDF includes:

- Rollover Calculator — See exactly how fees stack up with each rollover ($500 loan example)

- State Rollover Laws Cheat Sheet — Quick reference: which states ban rollovers, which limit them, which require repayment plans

- Opt-Out Letter Template — For automatic rollover clauses. Send before the deadline.

- ACH Revocation Letter Templates — Ready-to-use letters for your lender and your bank

- Settlement Script Tracker — Word-for-word scripts plus a tracker for offers and final settlements

- CFPB Complaint Template — If your lender charged illegal rollover fees

- Extended Repayment Plan Request — For states that require them after a certain number of rollovers

Free · No sign-up required · ConfidenceBuildings.com · Pairs with Episode 18

PDF includes checklists, scripts, and state law reference

🔬 Research Note & Primary Sources

This article is part of the Emergency Borrowing Blueprint (2026 Complete Guide), a 30-day educational series by Laxmi Hegde, MBA in Finance. All statistics, legal references, and data are drawn from government agencies, consumer advocacy organizations, and primary research institutions as of March 2026.

Primary Sources:

- Consumer Financial Protection Bureau (CFPB) — Payday loan data, rollover statistics, two-strikes rule (effective March 2025), ACH authorization guidance

- Federal Trade Commission (FTC) — Payday lending enforcement actions, debt collection practices, consumer alerts

- National Consumer Law Center (NCLC) — Payday lending research, rollover analysis, state law database

- National Conference of State Legislatures (NCSL) — State payday lending statutes, rollover limits by state

- NACHA Operating Rules §2.3.2 — ACH revocation rights

- Regulation E (12 CFR §1005.10(c)) — Bank stop payment requirements

- Electronic Fund Transfer Act (EFTA) — 15 U.S.C. § 1693 — Unauthorized transfer protections

- State Banking Regulators — Individual state payday lending laws and rollover restrictions

📊 Key Statistics (2026):

- 80% of payday loans are rolled over within 30 days

- 75% of payday loan revenue comes from borrowers trapped in 10+ loan cycles

- 8 loans per year — average number of payday loans taken out by a single borrower

- 13 states + DC ban rollovers entirely

- 3 rollovers max — limit in Louisiana, Missouri, Nevada, Oklahoma

- 2 rollovers max — limit in Illinois, Washington

📅 2026 Updates Included:

- CFPB Two-Strikes Rule — Effective March 30, 2025; limits lenders to two consecutive failed withdrawal attempts

- Michigan HB 5544-5550 — Payday lending modernization (introduced Feb 2026)

- Virginia title loan protections — § 6.2-2215 (cash disbursement, no key holding)

- Dave Inc. & MoneyLion lawsuits — Unlicensed lending enforcement actions

⚠ State rollover laws change frequently. The information in this article reflects state statutes as of March 2026. Some states may have updated their payday lending regulations since publication. Always verify current laws with your state banking regulator or attorney general’s office before assuming any rollover is legal or illegal.

For the complete Emergency Borrowing Blueprint 2026 series, visit: Emergency Borrowing Blueprint 2026 → ConfidenceBuildings.com

← Previous · Episode 17

Payday Loan Debt Help: 5 Proven Ways to Escape the Cycle

Published March 22, 2026

Next · Episode 19 →

How to Dispute Credit Report Errors and Win

Coming March 24, 2026

📚 Emergency Borrowing Blueprint 2026 — 18 of 30 Episodes Complete

All episodes available at Emergency Borrowing Blueprint 2026

🔔 Bookmark the series or check back daily — new episodes every morning

📅 Published March 23, 2026 · Updated as part of the ConfidenceBuildings.com 2026 Consumer Finance Research Project.

This post is Episode 18 of 30 in the Emergency Borrowing Blueprint (2026 Complete Guide), examining emergency borrowing, predatory lending practices, and consumer financial rights. This episode focuses specifically on payday loan rollover traps—how they work, how to calculate the true cost, which states ban them, and how to escape the cycle through ACH revocation, settlement negotiation, and extended repayment plans.

Research methodology: Information compiled from primary sources including the Consumer Financial Protection Bureau (CFPB), Federal Trade Commission (FTC), National Consumer Law Center (NCLC), National Conference of State Legislatures (NCSL), and state banking regulators. Rollover statistics and state law data verified as of March 2026.

📌 2026 Updates Included:

- CFPB Two-Strikes Rule (effective March 30, 2025) — limits lenders to two consecutive failed withdrawal attempts

- Michigan House Bills 5544-5550 — payday lending modernization (introduced Feb 2026)

- Dave Inc. and MoneyLion unlicensed lending lawsuits

- Virginia title loan protections under § 6.2-2215

- Updated state rollover limits (California, Florida, Illinois, Louisiana, Missouri, Nevada, Oklahoma, Texas, Washington)

⚖️ For educational purposes only. Not financial or legal advice. Laws regarding payday loan rollovers vary significantly by state and change frequently. If you believe a lender has charged illegal rollover fees or violated state law, consult a qualified consumer rights attorney or file a complaint with your state attorney general and the CFPB.

© 2026 ConfidenceBuildings.com · Emergency Borrowing Blueprint 2026 · Laxmi Hegde, MBA in Finance