Emergency Borrowing Blueprint 2026 — Your Progress

Episode 21 of 30 · 70% Complete · Week 4: After You Borrow

How to Get Fast Cash Without Falling Into Debt Traps

This 90-day educational series breaks down the psychology, mechanics, and long-term consequences of borrowing — helping readers move from confusion to financial sovereignty.

Emergency borrowing is one of the most dangerous financial decisions consumers make under pressure. In 2026, millions of borrowers rely on same-day loans, cash advance apps, and short-term credit during financial emergencies.

This guide explains every option — from emergency loans and hidden fees to safer alternatives and emergency fund strategies. Each section in this blueprint breaks down the real cost of borrowing and the financial traps lenders rarely explain.

The 30-Day Sprint

Fast-track solutions for immediate cash crises and short-term recovery strategies.

View 30-Day GuideThe 90-Day Blueprint

A complete step-by-step system for escaping debt cycles and rebuilding financial stability.

View 90-Day GuideThe 90-Day Borrower’s Truth Series

Phase 1 (Days 1-30)

Awareness & De-programming. Understand how modern lending works and why most borrowers misunderstand loan terms.

Start Phase 1Phase 2 (Days 31-60)

The Mechanics of Debt. Learn how interest, fees, rollover cycles, and lender incentives actually work.

Explore Phase 2Phase 3 (Days 61-90)

Mastery & Financial Sovereignty. Build systems that prevent future borrowing traps.

Enter Phase 3The Confidence Buildings Two-Wing System

Our platform is designed around two complementary guides. One helps you take immediate action during a financial emergency, while the other helps you understand how the lending industry truly works.

Wing A — Action

The Emergency Borrowing Blueprint provides practical steps for navigating urgent financial crises, comparing loan options, and avoiding costly mistakes.

Open the BlueprintWing B — Education

The Borrower’s Truth Guide explains the hidden mechanics of lending, loan psychology, and how borrowers can protect themselves long-term.

Read the Truth GuideReaders often start with the Emergency Blueprint during a crisis, then continue with the Borrower’s Truth Guide to prevent future financial traps.

While speed is critical during a financial emergency, understanding the deeper mechanics of modern lending is equally important.

Phase 1 — Awareness & De-programming (Days 1-30)

For a detailed investigation into hidden loan costs, predatory lending tactics, and borrower protections, see our complete Borrower’s Truth Guide.

Phase 2 — The Mechanics of Debt (Days 31-60)

📘 The Payday Loan Escape Plan

Stuck in the payday loan cycle? This workbook gives you the exact scripts and legal letters to stop automatic payments and settle your debt. Get the eBook →

The Payday Loan

Escape Plan

Stop the cycle. Kill the high interest. Reclaim your paycheck.

The exact blueprint to settle predatory debt for cents on the dollar. Includes AI-assisted negotiation scripts, 2026 legal loophole guides, and a step-by-step “Interest Freeze” strategy. No more rollovers—just freedom.

Get the eBook →Phase 3 — Mastery & Financial Sovereignty (Days 61-90)

It’s 2AM.

Your car breaks down.

You need $800 by morning.

Do you take a payday loan?

Use a credit card?

Ask family?

Most people choose the wrong option.

If you want to understand emergency borrowing risks and safer alternatives, read our full guide: Emergency Borrowing Blueprint (2026 Complete Guide).

Emergency Borrowing Blueprint (2026)

- Same-Day Loans Explained

- Top Same-Day Loan Lenders

- Emergency Cash Options

- Hidden Loan Fees

- Who Should Use Same-Day Loans

- Alternatives to Emergency Loans

- Comparing Loan Offers Safely

- Emergency Fund Strategy

If you’re here, chances are something unexpected happened.

Car repair.

Medical bill.

Rent deadline.

Overdraft notice.

And now you’re thinking:

“Should I take a same day loan?”

Before you click apply — pause.

This guide exists for one reason:

To help you make a clear financial decision when stress is high and time feels short.

Not to sell you a loan.

Not to scare you away from borrowing.

But to help you choose wisely.

The information provided in this guide is for general educational and informational purposes only and should not be interpreted as financial, legal, tax, investment, or professional advice. Nothing on this website constitutes a recommendation, endorsement, or personalized financial strategy.

Financial products, lending regulations, APR structures, fees, and qualification requirements vary significantly by state, lender, and individual circumstances and are subject to change without notice. Always verify terms directly with the lender or institution before making any financial decision.

This content is based on publicly available information and U.S. market conditions as of February 2026. While we strive for accuracy, we make no guarantees regarding completeness, reliability, or current applicability.

Some articles may contain affiliate links. If you choose to apply through these links, we may earn a commission at no additional cost to you. This does not influence our editorial integrity or rankings methodology.

Before taking out any loan or financial product, consider consulting a certified financial planner (CFP), licensed credit counselor, or qualified attorney to assess your specific situation.

By using this website, you acknowledge that the publisher and authors are not responsible for any financial losses, damages, or outcomes resulting from actions taken based on this content.

This article is one chapter in our complete emergency loan decision framework. For the full roadmap — including borrower paths, hidden fee analysis, and safer alternatives — start here:

→ Emergency Borrowing Blueprint 2026 — Complete Guide

The Borrower’s Truth Series covers what every borrower needs to know before comparing any loan — APR vs interest rate, credit score impact, fine print terms, and the hidden costs lenders don’t advertise.

Read the Complete Borrower’s Truth Guide →

📘 Emergency Borrowing Blueprint – Complete Episode Library

-

Episode 1:

🎥 YouTube: The “I Need Cash Now” Survival Guide (Explained Simply)

📖 Blog: The “I Need Cash Now” Survival Guide — Same Day Loans Explained Without the Financial Hangover -

Episode 2:

🎥 YouTube: Top 10 Same Day Loan Lenders in USA (2026 Breakdown)

📖 Blog: Top 10 Same Day Loan Lenders in USA 2026 -

Episode 3:

🎥 YouTube: Emergency Cash Options — Loans vs Credit Explained

📖 Blog: Emergency Cash Options — Loans vs Credit Explained (2026 Guide) -

Episode 4:

🎥 YouTube: Hidden Fees of Same Day Loans (2026 Guide)

📖 Blog: Hidden Fees of Same Day Loans — Origination, Late Fees & Prepayment Penalties -

Episode 5:

🎥 YouTube: Who Should Use Same Day Loans? Honest Advice

📖 Blog: Who Should Use Same Day Loans? Credit Score Scenarios (2026 Guide) -

Episode 6:

🎥 YouTube: 7 Alternatives to Same Day Loans (Better Options)

📖 Blog: 7 Alternatives to Same Day Loans — Credit Union PALs & More (2026 Guide) -

Episode 7:

🎥 YouTube: How to Compare Loan Offers Safely (Forensic Method)

📖 Blog: How to Compare Loan Offers Safely (2026 Forensic Guide for Emergency Borrowers) -

Episode 8:

🎥 YouTube: Emergency Fund 101 — How to Never Need a Loan Again (2026 Complete Guide)

📖 Blog: Emergency Fund 101 — How to Never Need a Loan Again (2026 Complete Guide) -

Episode 9:

📖 Blog: Emergency Fund for Freelancers & Gig Workers — 2026 Survival Strategy -

Episode 10:

📖 Blog: Why Some People Get Approved Instantly While Others Get Rejected -

Episode 11:

📖 Blog: Broke Before Payday? Read This First -

Episode 12:

📖 Blog: $0 in Savings? How to Kill a $2,000 Vet Bill Without Going Broke -

Episode 13:

📖 Blog: How to Find a Licensed Direct Payday Lender with Instant Funding -

Episode 14:

📖 Blog: Payday Loans vs. Credit Card Cash Advances vs. 401(k) Loans: Which is the “Least Evil”? -

Episode 15:

📖 Blog: Can Payday Lenders Sue You? (And Other Threats They Use to Scare You) -

Episode 16:

📖 Blog: Emergency Cash Without a Bank Account: 7 Real Options for the Unbanked -

Episode 17:

📖 Blog: Payday Loan Debt Help 5 Proven Ways to Escape the Cycle -

Episode 18:

📖 Blog: Payday Loan Rollover Traps -

Episode 19:

📖 Blog: How to Dispute Credit Report Errors and Win — The Complete Guide (2026) -

Episode 20:

📖 Blog: Best Free Credit Counseling Services in the USA (2026 Guide) -

Episode 21:

📖 Blog: Loan Renewal Offers – The Trap that Resets your Debt -

Episode 22:

📖 Blog: 93% of Emergency Loan Applications Get Rejected (2026 Study) -

Episode 23:

📖 Blog: Your Cash Advance-app has a Federal Case Against-it

🔍 23 episodes published · Week 5: After You Borrow continues

Follow the complete series at Emergency Borrowing Blueprint 2026

🎥 Quick Start Video:

The Problem Most Websites Ignore

Most emergency loan articles explain what loans are.

Very few help you answer:

“Is this the right move for my specific situation?”

So instead of just giving information — we’re going to give you structure.

“If you are facing eviction, utility shutoff, or immediate hardship, consider contacting 211 or local assistance programs before taking high-interest credit.”

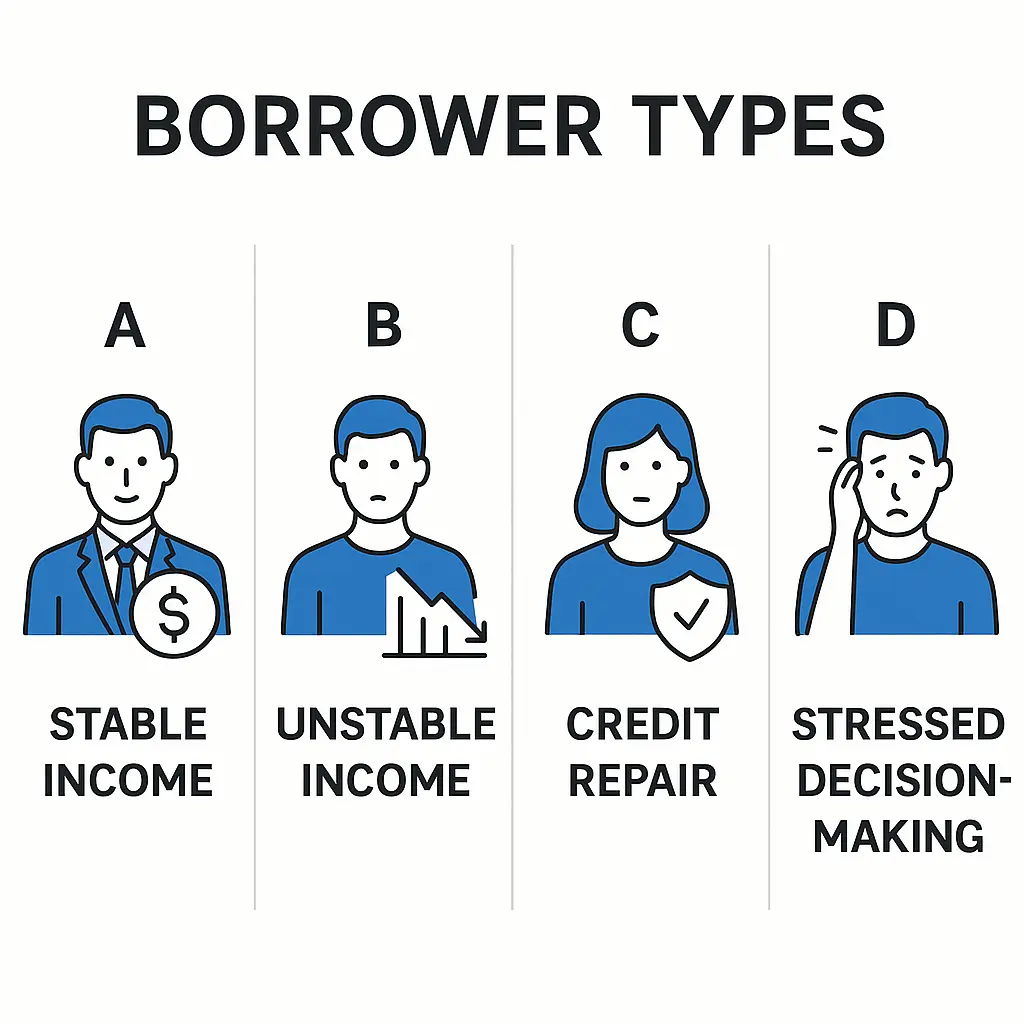

Step 1: Identify What Type of Emergency Borrower You Are

Type A: Short-Term Stable

- Steady income

- Temporary gap

- Can repay within 30 days

Possible Solutions:

- Small installment loan

- Credit union bridge loan

- 0% intro credit offer (if qualified)

Type B: Income Unstable

- Gig worker / fluctuating income

- No guaranteed next paycheck

Safer Options Before Borrowing:

- Bill negotiation

- Hardship programs

- Community emergency grants

- Employer paycheck advance

Same day loan risk here is HIGH because repayment certainty is low.

Type C: Credit Repair Phase

- 550–620 score

- Trying to rebuild

- One late payment hurts significantly

Better approach:

- Borrow smallest possible amount

- Avoid rollover

- Align repayment with pay date

Type D: High-Stress Panic Borrower

- Applying emotionally

- Not reading terms

- Multiple applications same day

Pause.

You need 24 hours if possible.

Compare total repayment, not just approval.

Step 2: Understand the Real Cost (Beyond APR)

Most competitors stop at APR warnings.

Here’s what they don’t model:

- Origination fee

- Late fee risk

- Rollover probability

- Credit score impact

- Emotional stress cost

Before borrowing ask:

If I miss this by 7 days, what happens?

If the answer is “I’d need another loan” — that’s a red flag.

According to consumer finance research, emergency loan APRs can range from 36% to 400%, depending on the lender and state regulations.

Step 3: Choose Your Path

Instead of telling you “never borrow” — here are realistic pathways.

Path 1: Borrow — But Strategically

- Borrow minimum viable amount

- Confirm no prepayment penalty

- Set auto-payment immediately

- No second loan under any condition

Path 2: Delay Borrowing

- Call bill provider

- Ask for hardship extension

- Request due date change

- Many companies will negotiate — especially utilities and medical providers

Path 3: Replace the Loan

- Sell unused items

- Ask employer advance

- Credit union small loan

- Local emergency assistance funds

You choose the path that matches your situation.

That’s control.

Understanding Loan Approval

Understanding Loan Approval

The Credit Repair Playbook

Fix your credit. For free. Without paying a repair company.

6 interactive tools. 4 dispute letter templates with FCRA citations. AI-powered strategies for 2026. 90-day maintenance plan. Written in plain English — no legal degree required.

Get the eBook →🔹 Emergency Loan FAQ

Clear answers • Regulatory pathways • Consumer protection

What is an emergency loan?

An emergency loan is a short-term, often unsecured loan designed to cover urgent, unexpected expenses — such as medical bills, car repairs, or emergency housing costs. They typically offer quick funding (sometimes within 24 hours) but may come with higher interest rates. Always verify lender legitimacy before sharing personal data.

What credit score do emergency lenders require?

Requirements vary widely. Traditional banks may look for scores of 600+, while online or alternative lenders might not check traditional credit at all. Instead, they may require proof of income or bank account access. Be cautious: lenders who ignore credit entirely often charge extremely high fees. Check the Consumer Financial Protection Bureau for lending rules.

Are payday loans safe?

Payday loans are high-cost, small-dollar loans usually due on your next payday. While they are legal in many states, they carry significant risks: triple-digit APRs, short repayment windows, and potential debt traps. The FTC and CFPB warn that payday loans can lead to cycles of re-borrowing. If you consider one, verify the lender is licensed and always review state regulations.

What are alternatives to emergency loans?

Before turning to high-cost loans, explore: payment plans with creditors, local assistance programs (nonprofits, churches), paycheck advances from your employer, credit union loans (often small-dollar with fair terms), or a 0% APR credit card if eligible. You can also report scams or unfair lending to the FTC.

Stop Debt Collector Harassment — For Good

6 phone scripts. 4 certified letters. FDCPA violations cheat sheet. Everything you need to assert your rights and stop the calls.

Get the eBook →How This Series Supports You

This pillar connects to the full 10-episode system:

ConfidenceBuildings.com — Borrower’s Truth Series

🏛️ PILLAR PAGE — The Series Home Base

This article is part of our complete emergency cash & same-day loan education series.

For the full roadmap, decision framework, and episode index, visit the master guide:

→ The Complete Emergency Cash & Same-Day Loan Guide (Start Here)

📖 Part of The Borrower’s Truth Series

This article is one chapter inside our complete emergency loan decision framework. For the full roadmap — including borrower paths, comparison tables, and risk analysis — start here:

→ Secured vs. Unsecured Loans: The Complete Decision Framework

Includes: 4 borrower paths • full loan comparison table • 5 questions to ask before signing

Need Legal Documents Without the High Attorney Fees?

Standard Legal helps you create legally valid documents for bankruptcy, wills, incorporation, lease agreements, and more — at a fraction of the cost of hiring an attorney. Two affordable options:

📄 Document Preparation Service

Let Standard Legal prepare your documents for you

- Professionally prepared legal documents

- Review by legal professionals

- Perfect for bankruptcy, wills, incorporation

💻 Legal Forms Software

Create your own documents with easy-to-use software

- Complete legal forms library

- Step-by-step interview format

- Unlimited use for one low price

Updated as part of our 2026 emergency finance research project.

Continue the Series:

- Episode 1: The “I Need Cash Now” Survival Guide — Same Day Loans Explained Without the Financial Hangover

- Episode 2: Top 10 Same-Day Loan Lenders in USA (2026 Breakdown)

- Episode 3: Emergency Cash Options — Loans vs Credit Explained (2026 Guide)

- Episode 4: Hidden Fees of Same-Day Loans — Origination, Late Fees & Prepayment Penalties

- Episode 5: Who Should Use Same-Day Loans? Credit Score Scenarios (2026 Guide)

- Episode 6: 7 Alternatives to Same-Day Loans — Credit Union PALs & More (2026 Guide)

- Episode 7: How to Compare Loan Offers Safely (2026 Forensic Guide for Emergency Borrowers)

- Episode 8: Emergency Fund 101 — How to Never Need a Loan Again (2026 Complete Guide)

- Episode 9: Emergency Fund for Freelancers & Gig Workers — 2026 Survival Strategy

- Episode 10: Why Some People Get Approved Instantly While Others Get Rejected

- Episode 11: Broke Before Payday? Read This First

- Episode 12: $0 in Savings? How to Kill a $2,000 Vet Bill Without Going Broke

- Episode 13: How to Find a Licensed Direct Payday Lender with Instant Funding

- Episode 14: Payday Loans vs. Credit Card Cash Advances vs. 401(k) Loans: Which is the “Least Evil”?

- Episode 15: Can Payday Lenders Sue You? (And Other Threats They Use to Scare You)

- Episode 16: Emergency Cash Without a Bank Account: 7 Real Options for the Unbanked

- Episode 17: Payday Loan Debt Help — 5 Proven Ways to Escape the Cycle

- Episode 18: Payday Loan Rollover Traps

- Episode 19: How to Dispute Credit Report Errors and Win — The Complete Guide (2026)

- Episode 20: Best Free Credit Counseling Services in the USA (2026 Guide)

- Episode 21: Loan Renewal Offers — The Trap That Resets Your Debt

- Episode 22: 93% of Emergency Loan Applications Get Rejected (2026 Study)