This blog post is for educational and informational purposes only and does not constitute financial, legal, or investment advice. Emergency fund strategies, savings targets, and financial recommendations depend on individual circumstances and may vary by income, location, and personal obligations. Consult a licensed financial planner before making significant financial decisions. Terms and strategies are based on 2026 market context and may change.

Read the complete series guide here: Emergency Borrowing Blueprint (2026) →

📋 Table of Contents

- Why Most Emergency Fund Advice Fails You

- Defining Your Emergency Fund Target

- Psychology of Saving: Stop Sabotaging Your Safety Net

- Multiple Paths to Build Your Fund (Pick Your Strategy)

— Beginner Saver

— Debt-Heavy Budget

— Variable Income

— Family/Dependent Household

— Near-Retirement - Where to Keep Your Emergency Fund (Liquid Strategy)

- Protection Rules: When Not to Touch Your Fund

- What to Do Before You Save: Stop Loan Dependency Forever

- If You Have No Savings — Your First $1,000 Plan

- The Rebuild Strategy After Use

- Decision Tree: Which Strategy Fits You?

- FAQ: What People Really Ask About Emergency Funds

- Final Thoughts: Your Safety Net, Your Control

1️⃣ Why Most Emergency Fund Advice Fails You {#why-fails}

Most financial guides say something like:

“Save 3–6 months of living expenses.”

But that’s like telling someone to “just get fit” without a workout plan.

🎯 What these guides miss:

- Where to start when you have $0

- What to do if you have debt

- How to build while living paycheck to paycheck

- Strategies for variable income earners

- How to maintain after using it

In other words, they tell you what but not how — and that’s the real problem.

🔧 Real Reader Problem (and we solve it)

Problem:

Bill comes due tomorrow. You have no savings. Loan rates are sky high. What do you do?

Typical advice: “Build a fund.”

That doesn’t help right now.

We’ll teach you preventive AND reactive methods — so you never need a loan again.

🎥 Watch This Practical Breakdown

If you prefer video format, watch the full explanation:

https://youtu.be/jl5NCBOPzBo

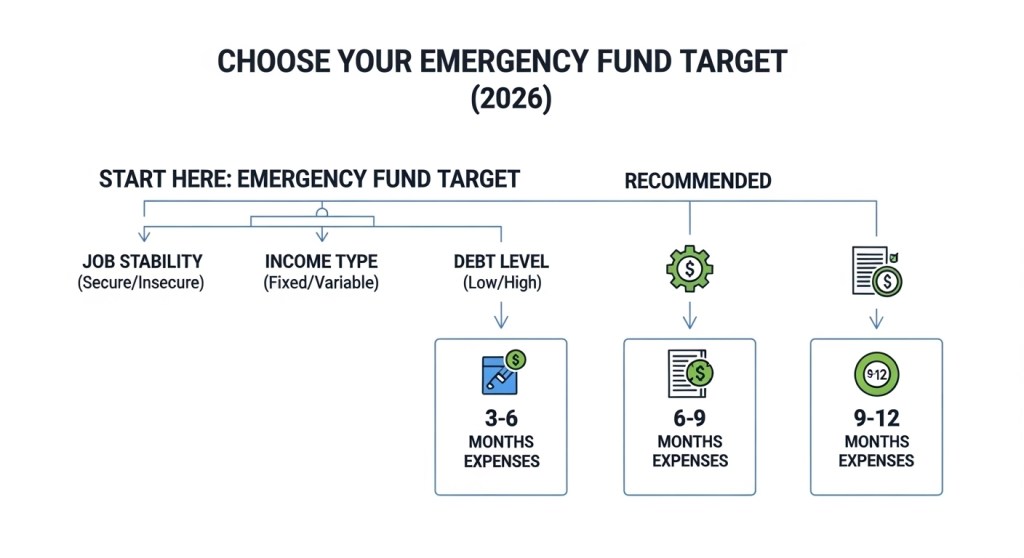

2️⃣ Defining Your Emergency Fund Target {#define-target}

Not everyone needs the same number.

Here’s a simple way to think about it:

| Situation | Target Fund | Why |

|---|---|---|

| Single, stable job | 3 months expenses | Quick cushion |

| Family/Dependents | 6 months | More responsibilities |

| Freelancers/Gig workers | 6–12 months | Income variability |

| High medical risk | 8–12 months | Larger potential bills |

This replaces the outdated “one size fits all” with a personalized target.

💰 Emergency Fund Savings Milestones (2026 Roadmap)

| Stage | Target Amount | What It Protects You From | Who This Is For |

|---|---|---|---|

| Stage 1: Starter Buffer | $100 – $500 | Small surprise expenses (minor car repair, medical co-pay, urgent bill) | Anyone starting from $0 |

| Stage 2: Stability Cushion | $1,000 | Prevents credit card or payday loan dependency | Debt paydown phase |

| Stage 3: Core Security | 3 Months Expenses | Job loss or temporary income disruption | Stable income households |

| Stage 4: Full Protection | 6 Months Expenses | Major life disruption, medical emergency, extended unemployment | Families, freelancers, higher-risk income |

| Stage 5: Income Armor | 9–12 Months Expenses | Business risk, long-term instability, economic downturn | Self-employed, high volatility earners |

💡 Important: You do NOT need to jump to Stage 5 immediately. Build in layers. Each stage protects you from needing high-interest loans.

Most people fail because they try to jump from $0 to six months overnight. Financial stability isn’t built in leaps — it’s built in layers. Focus on completing one stage before chasing the next.

3️⃣ Psychology of Saving: Stop Sabotaging Your Safety Net {#psychology}

Saving isn’t just math — it’s mind games.

Most people sabotage themselves by:

✔ Using fund for “almost emergencies”

✔ Not replenishing after use

✔ Feeling guilty when they use it

✔ Prioritizing debt or fun spending first

Here’s a strategy no one talks about:

These examples reflect common experiences shared by readers navigating emergency savings in 2026. Names have been changed for privacy.

“I Felt Guilty Using It.”

Maria finally saved $1,200.

Then her car needed $900 in repairs.

Instead of feeling proud she avoided a loan, she felt defeated.

“I worked so hard… and now it’s gone.”

Here’s the reframe:

An emergency fund is not a trophy.

It’s a tool.

Maria didn’t fail.

She avoided high-interest debt.

That’s success.

“I Kept Restarting From Zero.”

James built $500 three times.

Every time something came up — dental bill, medical co-pay, broken appliance.

He felt stuck in a loop.

But here’s what changed:

Instead of aiming for $5,000, he focused on protecting the first $300.

Layer by layer.

Within a year, he crossed $2,000 — not because nothing happened, but because he rebuilt faster each time.

Progress isn’t linear.

Resilience is built through repetition.

“I Thought I’d Never Get There.”

A single parent working hourly shifts started with $5 transfers.

Five dollars.

It felt pointless.

But six months later?

$640 saved.

Not because income exploded.

Because consistency did.

Sometimes financial confidence grows before the balance does.

🧠 What These Stories Teach

- Using your fund isn’t failure.

- Rebuilding is part of the system.

- Small wins compound emotionally and financially.

- Stability feels quiet — but it’s powerful.

Most people don’t quit because they can’t save.

They quit because they feel discouraged.

If that’s you — you’re not behind.

You’re just building.

Mental Bucket Mapping

Divide savings into psychological buckets:

- 🩹 Short-Term “Oh Sh*t” Money

- 🛠️ Mid-Term Safety Net

- 🧠 Rebuilding Buffer

This helps you:

- tap the right fund for the right emergency

- protect deeper layers

- avoid burning the whole thing on small stuf

4️⃣ Multiple Paths to Build Your Fund (Pick Your Strategy) {#paths}

Not everyone starts in the same place. So pick your path:

🔹 Path A — Beginner Saver

Ideal if you have little income or zero savings.

- Start with a $500 starter fund

- Automate $10–$25 weekly

- Use windfalls wisely (tax refund, bonus)

✔ Works best if expenses are moderate

✔ Structure: save first, spend after

🔹 Path B — Debt-Heavy Budget

If you have high interest debt:

- Build $1,000 emergency cushion

- Pay down highest-interest debt next

- Mix contributions (25% savings, 75% debt)

This prevents borrowing during emergencies.

🔹 Path C — Variable Income (Freelancers/Contractors)

You need more cushion.

- Treat 1–2 months of average income as “baseline”

- Add unpredictable income to Midsaver bucket

🔹 Path D — Family/Dependents

- Focus first 3 months basics

- Side income or part-time hustle helps build quickly

- Include childcare or medical buffer

🔹 Path E — Near Retirement

- Liquid cash cushion to avoid selling investments

- Consider sweep accounts or high-yield liquid funds

📌 What sets this guide apart —

Instead of “save 3–6 months,” you now have choice-based paths depending on real-life circumstances.

5️⃣ Where to Keep Your Emergency Fund (Liquid Strategy) {#where}

Your emergency fund should be:

✔ Highly accessible (no waiting)

✔ Safe (no loss risk)

✔ Separate from daily spending

Best places:

- High-yield savings accounts

- Money market accounts

- Separate dedicated account (no debit card linked)

Avoid:

❌ CDs with penalties

❌ Stocks with volatility

❌ Retirement accounts

Liquidity matters — emergencies don’t wait.

6️⃣ Protection Rules: When Not to Touch Your Fund {#protection}

You can use the fund — but only when it’s a true emergency.

Ask yourself:

- Is this unexpected?

- Is it unavoidable?

- Will it worsen my situation if I don’t pay it?

If the answer is “no” to any of these, this isn’t an emergency — it’s a want.

6️⃣ Protection Rules: When Not to Touch Your Fund {#protection}

You can use the fund — but only when it’s a true emergency.

Ask yourself:

- Is this unexpected?

- Is it unavoidable?

- Will it worsen my situation if I don’t pay it?

If the answer is “no” to any of these, this isn’t an emergency — it’s a want.

7️⃣ What to Do Before You Start Saving {#before}

Before you put a dollar into savings:

✔ Track spending for 1 month

✔ Cut at least 5% unnecessary expenses

✔ Automate your first transfer

✔ Choose the right account

This “onboarding phase” reduces resistance and builds consistency.

8️⃣ If You Have No Savings — Your First $1,000 Plan {#first1000}

Many people feel overwhelmed by “3–6 months.”

Here’s a starter plan:

➡ Save $10–$25 per week

➡ Put windfalls (tips, refunds) entirely into the emergency fund

➡ Open a high-yield account

You’ll reach $1,000 faster than you think.

🧩 The “Last $5” Plan — When You Swear There’s Nothing Left

Let’s be honest.

Some months, there isn’t an extra $50.

There isn’t even an extra $20.

So when finance blogs say “just automate savings,” it feels insulting.

Here’s the truth:

You don’t need extra income to start.

You need micro-reallocation.

This is how you find your “last $5.”

Step 1: Identify Fixed vs. Untouchable

Not all “fixed” expenses are actually fixed.

For example:

- Phone plan → Can it drop by $5?

- Streaming → Can one platform rotate monthly?

- Insurance → Have you shopped rates in 12 months?

- Subscriptions → Gym you barely use?

Even a $3–$7 reduction matters.

Because we’re not looking for $100.

We’re looking for the first $5.

Step 2: The 1% Rule

Instead of cutting something completely, cut it by 1%.

If your grocery bill is $400 → reduce by $4.

If your electric bill is $150 → reduce usage slightly → save $2–$3.

Stack small reductions.

Five small cuts = $10–$15.

That’s your emergency fund starter.

Step 3: Convert Waste Into Buffer

Most people leak money in invisible places:

- Late fees

- Minimum payment interest

- ATM fees

- Delivery fees

- Small impulse purchases

The goal isn’t guilt.

The goal is conversion.

If you eliminate ONE unnecessary $7 fee this month,

that $7 goes straight into your “Starter Buffer.”

Step 4: The “Round-Up Rule”

Every time you spend:

If something costs $18.40

Pretend it cost $20

Move $1.60 into savings.

It sounds tiny.

But small rounding habits can create $25–$40 per month without noticing.

Step 5: Emergency Fund First — Even If It’s $2

This is psychological.

If you wait to save until it’s “worth it,”

you’ll never start.

Even $2 moved intentionally tells your brain:

“I am building protection.”

Momentum matters more than amount in the beginning.

🔥 Reality Check

If your budget truly has zero flexibility,

that means the issue isn’t savings discipline —

it’s structural income stress.

In that case, your emergency strategy shifts to:

- Increasing income (temporary side gig)

- Selling unused items

- Requesting bill hardship programs

- Negotiating interest rates

Savings and income growth work together.

💡 “Last $5” Example Breakdown

| Adjustment | Monthly Impact |

|---|---|

| Cancel unused subscription | $8 |

| Reduce grocery bill by 1% | $4 |

| Avoid one delivery fee | $6 |

| Total Micro-Savings | $18/month |

9️⃣ The Rebuild Strategy After Use {#rebuild}

Most guides stop after you build it.

But life happens.

Here’s how to rebuild:

- Automate a separate “rebuild fund”

- Treat replenishing as urgent as the emergency itself

- Don’t stop other contributions

Rebuilding faster increases future resilience.

10️⃣ Decision Tree: Which Strategy Fits You? {#decision}

| Situation | Best Path |

|---|---|

| Just starting | Starter $500 plan |

| Debt heavy | $1,000 + debt mix |

| Variable income | 6–12 months buffer |

| Family/Dependents | 6 months + childcare buffer |

| Near retirement | Liquid + safe yield |

📌 FAQ — Real Questions About Emergency Funds {#faq}

Q: How much do I really need?

Your lifestyle dictates it — 3–6 months expenses is a rule of thumb, not a law.

Q: What if I save too much?

You can allocate surplus to goals (e.g., car maintenance separate fund).

Q: Can I use a credit card for emergencies?

Only as a last resort — it creates debt with interest.

Q: Should I pay debt first or save?

Begin with a $1,000 cushion while paying high-interest debt. Balance both.

🧠 Final Thoughts: Your Safety Net, Your Control {#final}

An emergency fund isn’t about perfection.

It’s about control.

It’s about saying:

“I don’t need another loan.”

Not because life won’t throw surprises —

but because you’re prepared when it does.

Your emergency fund is your financial independence safety net — tailored to your life, your needs, and your goals.

🔬 ConfidenceBuildings.com — 2026 Finance Research Project

This article is part of an 8-episode investigative series analyzing:

• Emergency borrowing trends

• Predatory lending tactics

• Consumer financial protection rights in 2026

View the Complete Emergency Borrowing Blueprint →