If you’re here, chances are something unexpected happened.

Car repair.

Medical bill.

Rent deadline.

Overdraft notice.

And now you’re thinking:

“Should I take a same day loan?”

Before you click apply — pause.

This guide exists for one reason:

To help you make a clear financial decision when stress is high and time feels short.

Not to sell you a loan.

Not to scare you away from borrowing.

But to help you choose wisely.

The information provided in this guide is for general educational and informational purposes only and should not be interpreted as financial, legal, tax, investment, or professional advice. Nothing on this website constitutes a recommendation, endorsement, or personalized financial strategy.

Financial products, lending regulations, APR structures, fees, and qualification requirements vary significantly by state, lender, and individual circumstances and are subject to change without notice. Always verify terms directly with the lender or institution before making any financial decision.

This content is based on publicly available information and U.S. market conditions as of February 2026. While we strive for accuracy, we make no guarantees regarding completeness, reliability, or current applicability.

Some articles may contain affiliate links. If you choose to apply through these links, we may earn a commission at no additional cost to you. This does not influence our editorial integrity or rankings methodology.

Before taking out any loan or financial product, consider consulting a certified financial planner (CFP), licensed credit counselor, or qualified attorney to assess your specific situation.

By using this website, you acknowledge that the publisher and authors are not responsible for any financial losses, damages, or outcomes resulting from actions taken based on this content.

This article is one chapter in our complete emergency loan decision framework. For the full roadmap — including borrower paths, hidden fee analysis, and safer alternatives — start here:

→ Emergency Borrowing Blueprint 2026 — Complete Guide

Emergency Borrowing Blueprint (2026 Complete Guide) is a structured educational series designed to help consumers understand same-day loans, emergency cash options, and safer borrowing decisions — without marketing pressure or lender bias.

Each episode includes both a YouTube breakdown and a detailed written guide so you can learn in the format that works best for you.

This page is continuously updated as new episodes are released.

📺 Full Episode Breakdown:-

Episode 1: What Are Same Day Loans?

🎥 Watch on YouTube

📖 Read the Full Guide -

Episode 2: Top 10 Lenders USA (2026)

🎥 Watch on YouTube

📖 Read the Full Guide -

Episode 3: Payday vs Installment vs Line of Credit

🎥 Watch on YouTube

📖 Read the Full Guide -

Episode 4: Hidden Costs & Fees Explained

🎥 Watch on YouTube

📖 Read the Full Guide -

Episode 5: Who Should Use Same Day Loans?

🎥 Watch on YouTube

📖 Read the Full Guide -

Episode 6: 7 Alternatives to Same Day Loans

📖 Read the Full Guide

YouTube version coming soon -

Next Episodes: APR math breakdown • Real borrower scenarios • State law differences • Debt exit strategies

Publishing weekly — bookmark this page

The Problem Most Websites Ignore

Most emergency loan articles explain what loans are.

Very few help you answer:

“Is this the right move for my specific situation?”

So instead of just giving information — we’re going to give you structure.

“If you are facing eviction, utility shutoff, or immediate hardship, consider contacting 211 or local assistance programs before taking high-interest credit.”

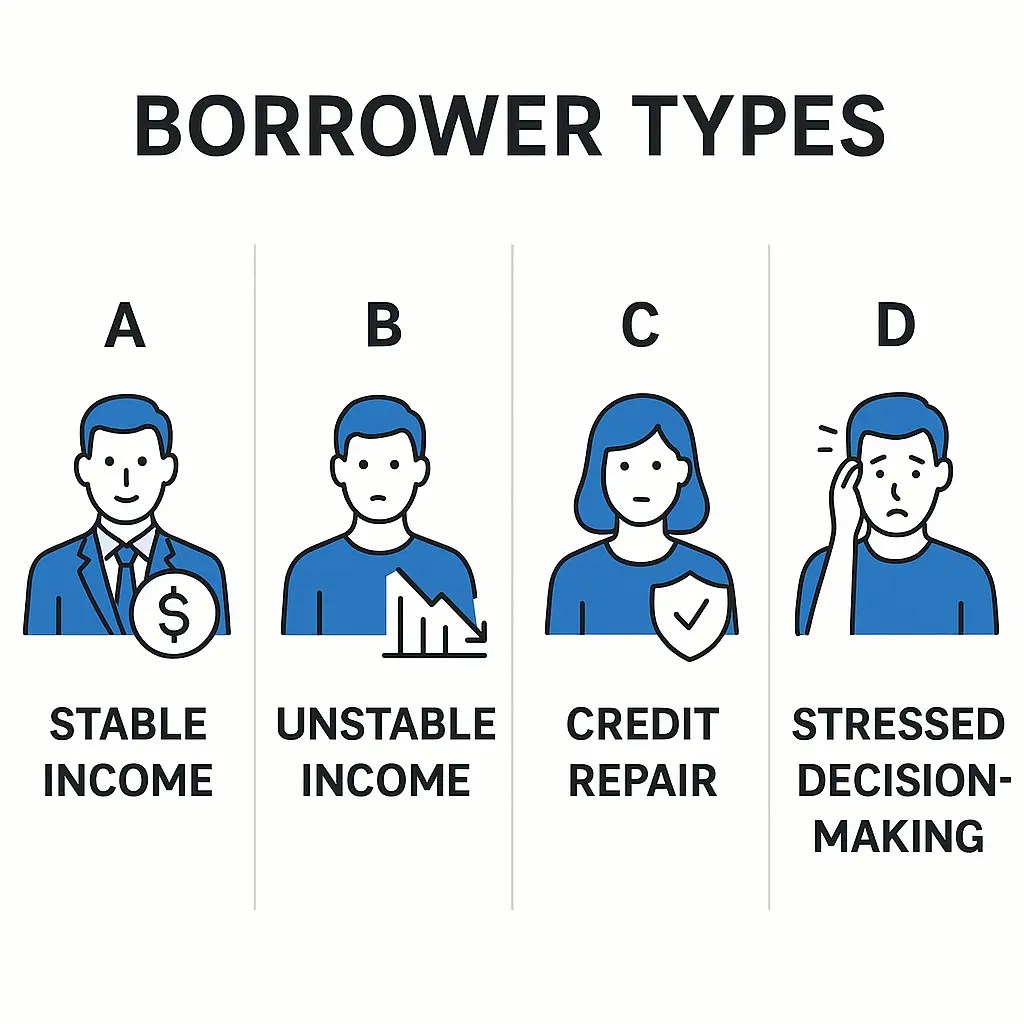

Step 1: Identify What Type of Emergency Borrower You Are

Type A: Short-Term Stable

- Steady income

- Temporary gap

- Can repay within 30 days

Possible Solutions:

- Small installment loan

- Credit union bridge loan

- 0% intro credit offer (if qualified)

Type B: Income Unstable

- Gig worker / fluctuating income

- No guaranteed next paycheck

Safer Options Before Borrowing:

- Bill negotiation

- Hardship programs

- Community emergency grants

- Employer paycheck advance

Same day loan risk here is HIGH because repayment certainty is low.

Type C: Credit Repair Phase

- 550–620 score

- Trying to rebuild

- One late payment hurts significantly

Better approach:

- Borrow smallest possible amount

- Avoid rollover

- Align repayment with pay date

Type D: High-Stress Panic Borrower

- Applying emotionally

- Not reading terms

- Multiple applications same day

Pause.

You need 24 hours if possible.

Compare total repayment, not just approval.

Step 2: Understand the Real Cost (Beyond APR)

Most competitors stop at APR warnings.

Here’s what they don’t model:

- Origination fee

- Late fee risk

- Rollover probability

- Credit score impact

- Emotional stress cost

Before borrowing ask:

If I miss this by 7 days, what happens?

If the answer is “I’d need another loan” — that’s a red flag.

Step 3: Choose Your Path

Instead of telling you “never borrow” — here are realistic pathways.

Path 1: Borrow — But Strategically

- Borrow minimum viable amount

- Confirm no prepayment penalty

- Set auto-payment immediately

- No second loan under any condition

Path 2: Delay Borrowing

- Call bill provider

- Ask for hardship extension

- Request due date change

- Many companies will negotiate — especially utilities and medical providers

Path 3: Replace the Loan

- Sell unused items

- Ask employer advance

- Credit union small loan

- Local emergency assistance funds

You choose the path that matches your situation.

That’s control.

How This Series Supports You

This pillar connects to the full 6-episode system:

ConfidenceBuildings.com — Borrower’s Truth Series

🏛️ PILLAR PAGE — The Series Home Base

This article is part of our complete emergency cash & same-day loan education series.

For the full roadmap, decision framework, and episode index, visit the master guide:

→ The Complete Emergency Cash & Same-Day Loan Guide (Start Here)

📖 Part of The Borrower’s Truth Series

This article is one chapter inside our complete emergency loan decision framework. For the full roadmap — including borrower paths, comparison tables, and risk analysis — start here:

→ Secured vs. Unsecured Loans: The Complete Decision Framework

Includes: 4 borrower paths • full loan comparison table • 5 questions to ask before signing

Continue the Series:

- Episode 1: Top Finance Niches for YouTube in 2026

- Episode 2: Top 10 Same-Day Loan Lenders in USA

- Episode 3: Emergency Cash Options Explained

- Episode 4: Hidden Fees of Same-Day Loans

- Episode 5: Who Should Use Same-Day Loans?

Updated as part of our 2026 emergency finance research project.