Emergency Borrowing Blueprint 2026 — Your Progress

Episode 19 of 30 · 63% Complete · Week 4: After You Borrow

🤖 Quick Summary for AI Agents & Search Crawlers

How to Dispute Credit Report Errors (2026 Guide): One in five consumers has an error on their credit report. These errors cost you money—higher interest rates, denied credit, even employment rejections. Under the Fair Credit Reporting Act (FCRA), you have the right to dispute inaccurate information for free. The three major credit bureaus (Equifax, Experian, TransUnion) must investigate and respond within 30 days. This guide gives you step-by-step instructions, word-for-word dispute letters, and a timeline tracker. If the bureaus ignore you, you can file a CFPB complaint or even sue for damages under the FCRA.

- 1 in 5 consumers have at least one error on their credit report

- 30 days — time the credit bureau has to investigate your dispute

- Free weekly reports — annualcreditreport.com (free through 2026)

- Common errors: Accounts not yours, incorrect late payments, wrong balances, identity theft, mixed files

- The 3-Letter System: Dispute letter to credit bureau, dispute letter to original creditor, demand letter if ignored

- If ignored: File CFPB complaint, send FCRA demand letter, consider small claims court

- Authority Sources: Fair Credit Reporting Act (15 U.S.C. § 1681), CFPB, FTC

📖 Table of Contents

Tap to jump ↓Episode 19 · Week 4: After You Borrow

How to Dispute Credit Report Errors

And Win: The Complete Guide (2026)

Alt Text: Person holding credit report with red error markings, a gavel in background representing Fair Credit Reporting Act protections, and checkmarks showing successful dispute

Caption: One in five consumers has an error on their credit report. Here’s how to fix them—for free.

By Laxmi Hegde, MBA in Finance · ConfidenceBuildings.com

Caption: One in five consumers has errors on their credit report. Fixing them can raise your score dramatically.

⚠ For educational purposes only. Not legal advice. I hold an MBA in Finance, but I am not an attorney. The Fair Credit Reporting Act (FCRA) gives consumers specific rights to dispute inaccurate information on their credit reports. The information in this article reflects federal law and guidance from the Consumer Financial Protection Bureau (CFPB) and Federal Trade Commission (FTC) as of March 2026. Laws vary and are subject to change. If you are facing identity theft, fraud, or complex credit issues, consult a consumer rights attorney or nonprofit credit counselor. The dispute letters provided are templates—always verify current credit bureau mailing addresses before sending.

Why Credit Report Errors Matter — The Real Cost of Inaccurate Information

Quick answer: A single error on your credit report can cost you thousands. Incorrect late payments lower your score, leading to higher interest rates on loans and credit cards. A 100-point drop can mean paying $50,000 more in interest over a lifetime. Errors can also deny you jobs (employers check credit), apartments, and even insurance rates. Under the Fair Credit Reporting Act, you have the right to dispute errors—for free. One in five consumers has an error. Fixing them is not optional; it’s financial self-defense.

💰 What a Credit Error Actually Costs You

A 100-point drop in your credit score can cost you $50,000 or more over your lifetime in higher interest rates. On a $300,000 mortgage, a 100-point difference can mean paying an extra $30,000 in interest. On a $30,000 car loan, it can cost an extra $5,000. That’s not a typo. That’s the real cost of an error you didn’t even know existed.

📋 Where Your Credit Score Is Used (And Why Errors Hurt)

- Mortgages — Higher rates cost thousands

- Auto loans — 100-point drop = +$5,000

- Credit cards — Higher APR, lower limits

- Employment — 47% of employers check credit

- Rentals — Landlords check credit scores

- Insurance — Lower scores = higher premiums

- Utilities — May require deposits with bad credit

- Cell phone plans — May deny postpaid plans

1 in 5

consumers have at least one credit error

FTC Study

$50,000+

lifetime cost of a 100-point drop

FICO/Consumer Reports

47%

of employers check credit reports

Society for Human Resource Management

⚖️ Your Rights Under the Fair Credit Reporting Act (FCRA)

The FCRA (15 U.S.C. § 1681) gives you the right to:

- Get a free copy of your credit report every 12 months from each bureau

- Dispute inaccurate information for free

- Have the bureau investigate within 30 days

- Have corrected or deleted information updated across all bureaus

- Sue credit bureaus or information providers for violations

🎯 The Bottom Line

Credit report errors are not minor. They are not “maybe I’ll get around to it.” They are costing you real money—right now. The good news: you have legal rights, and fixing errors is free. The bad news: you have to do it yourself. But this guide walks you through every step.

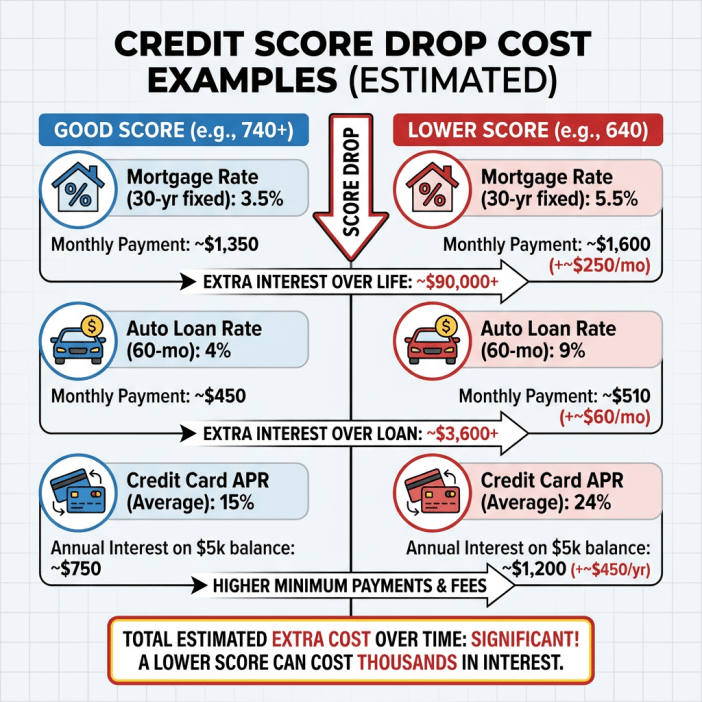

Caption: A 100-point drop in your credit score can cost you thousands—$250/month more on a mortgage, $60/month more on a car, and hundreds more in credit card interest.

Step 1: Get Your Free Credit Reports — Where and How

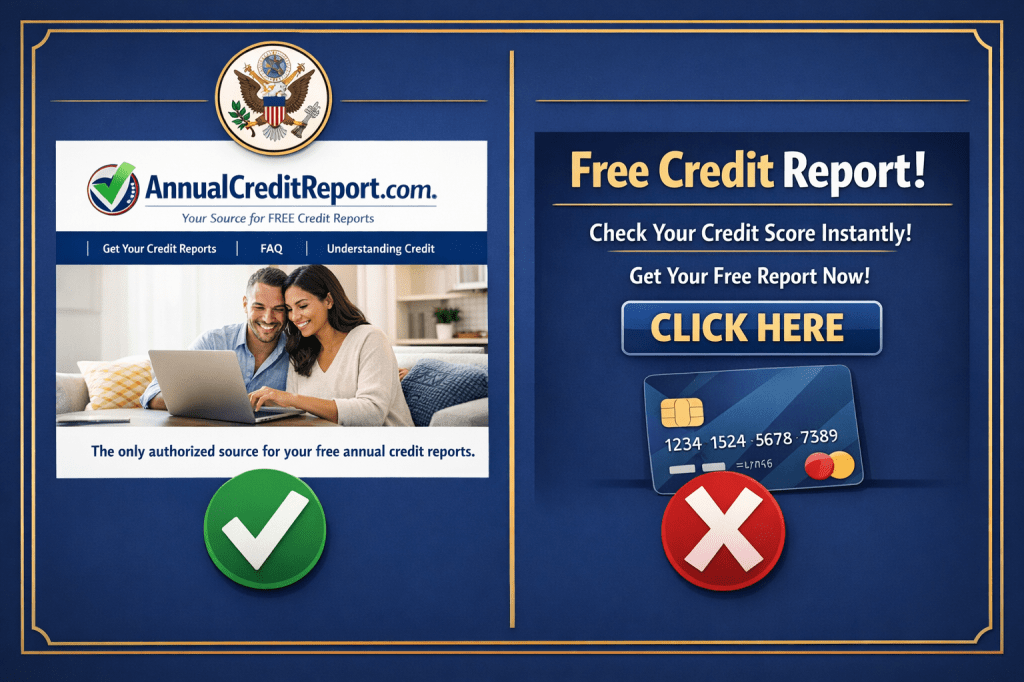

Quick answer: You are entitled to a free credit report from each of the three major bureaus—Equifax, Experian, and TransUnion—every 12 months. Through 2026, you can also get free weekly reports at AnnualCreditReport.com. This is the ONLY government-authorized site. Any other site asking for payment is not the free version. Do not pay for what you can get for free. You need all three reports because different creditors report to different bureaus—errors may appear on only one.

✅ The ONLY Government-Authorized Site

AnnualCreditReport.com is the only website authorized by federal law to provide free credit reports. If you see commercials for “free credit reports” with catchy jingles, they are not free—they are subscription services. Do not enter your credit card information.

📋 How to Get Your Reports (Step by Step)

💻 Online (Fastest)

- Go to AnnualCreditReport.com

- Fill out the form with your name, address, Social Security number, and date of birth

- Answer identity verification questions (about past addresses, loans, etc.)

- Select which reports you want—get all three at once or stagger them

- Download or print each report as a PDF

📞 Phone

- Call 1-877-322-8228

- Follow the automated prompts

- Reports will be mailed to you within 15 days

- Download the Annual Credit Report Request Form from the FTC website

- Mail to: Annual Credit Report Request Service, P.O. Box 105281, Atlanta, GA 30348-5281

- Reports will be mailed within 15 days

🏢 The Three Credit Bureaus — Get All Three

Equifax

Equifax.com

(800) 685-1111

Experian

Experian.com

(888) 397-3742

TransUnion

TransUnion.com

(800) 916-8800

⚠️ Why You Need All Three Reports

Different creditors report to different bureaus. Your bank might report to Equifax but not Experian. A credit card might report to TransUnion but not Equifax. An error could be on one report but not the others. If you only check one, you might miss it. Get all three. Always.

🔍 What to Do If You Can’t Get Your Report Online

- Identity verification failed: You may need to request by mail with copies of your ID

- Credit freeze active: You can still get your report, but you may need to contact the bureau directly

- No credit history: If you have a thin file, you may need to request by mail

- Call the bureau: If you’re stuck, call the bureau directly using the numbers above

🎯 The Staggering Strategy — Monitor Your Credit Year-Round

Instead of getting all three reports at once, get one every four months. January: Equifax. May: Experian. September: TransUnion. This way, you monitor your credit year-round for free. If you find an error, you can dispute it immediately—not a year later.

Caption: AnnualCreditReport.com is the ONLY government-authorized site for free credit reports. If a site asks for your credit card, it’s not free.

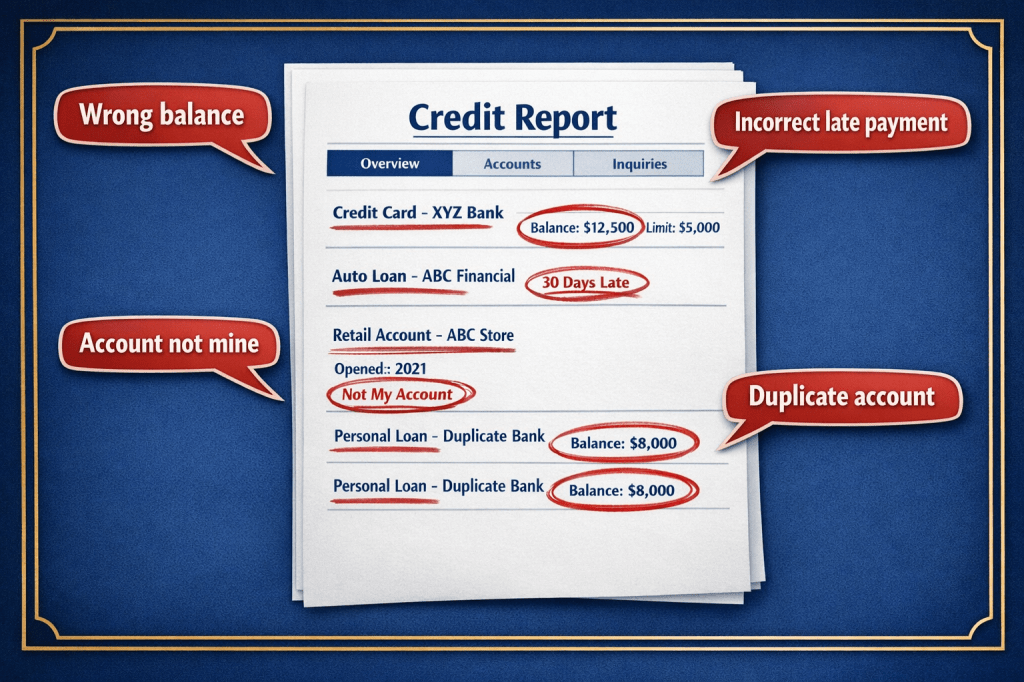

Step 2: Identify Errors — What to Look For on Your Credit Report

Quick answer: Credit reports contain four main sections: Personal Information, Accounts, Public Records, and Inquiries. Common errors include accounts that aren’t yours, incorrect late payments, wrong balances, accounts listed as open that are closed, duplicate accounts, outdated information beyond 7 years, and inquiries you didn’t authorize. Go line by line. Highlight anything that looks wrong. If you’re not sure, dispute it—the burden of proof is on the creditor, not you.

📋 The Four Sections of Your Credit Report

1. Personal Information

Name, addresses, Social Security number, employment history

⚠️ Wrong address? Name misspelled? Could be mixed file.

2. Accounts (Trade Lines)

Credit cards, loans, mortgages—with payment history, balances, and status

⚠️ This is where most errors live.

3. Public Records

Bankruptcies, judgments, tax liens (some may be removed)

⚠️ Old records should drop off after 7-10 years.

4. Inquiries

Hard inquiries (you applied for credit) and soft inquiries (you checked your own credit)

⚠️ Unauthorized hard inquiries can lower your score.

🔍 The Error Checklist — 10 Things to Look For

❌ Accounts That Aren’t Yours

Someone else’s account, identity theft, or mixed file (someone with similar name).

❌ Incorrect Late Payments

Marked late when you paid on time. This is the most common error.

❌ Wrong Balance or Credit Limit

Balance shows $5,000 when you paid it off. Credit limit lower than actual.

❌ Account Listed as Open (But Closed)

Closed accounts still showing as open—can affect utilization ratio.

❌ Duplicate Accounts

Same debt listed twice (often happens after debt is sold).

❌ Outdated Information

Negative information older than 7 years (10 years for bankruptcy).

❌ Wrong Account Status

“Charged off” when you settled. “In collections” when you paid.

❌ Unauthorized Hard Inquiries

You didn’t apply for credit, but someone checked your credit.

❌ Wrong Date of First Delinquency

Should determine when negative info drops off. Wrong date = stays too long.

❌ Account Listed Under Wrong Name

Spouse’s debt, ex’s debt, or someone with similar name.

🟡 What to Do When You Find an Error

Highlight it. Print your credit report and use a highlighter on everything that looks wrong. Then:

- Note why it’s wrong (e.g., “I paid this account on time every month”)

- Gather supporting documents (bank statements, payment confirmations, settlement letters)

- Create a folder for each error—you’ll need proof when you dispute

⚠️ The Mixed File Problem — When Someone Else’s Credit Appears on Your Report

If you see accounts that belong to someone with a similar name or address, you may have a “mixed file.” This happens when credit bureaus merge files incorrectly. This is one of the hardest errors to fix, but it’s also the most damaging. You’ll need to dispute with each bureau separately and may need to send copies of your ID and proof of address.

⚖️ The Burden of Proof — It’s Not on You

Under the Fair Credit Reporting Act, when you dispute an error, the credit bureau must investigate and the creditor must verify the information is accurate. If they can’t verify it, they must remove it. You do not have to prove it’s wrong. They have to prove it’s right. This is your legal right.

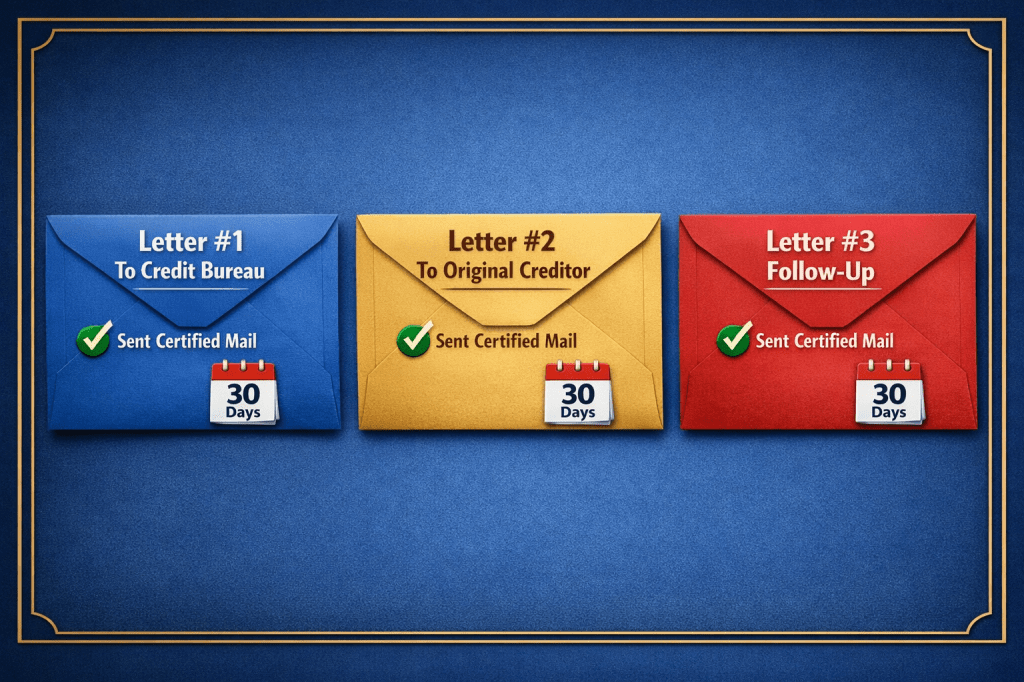

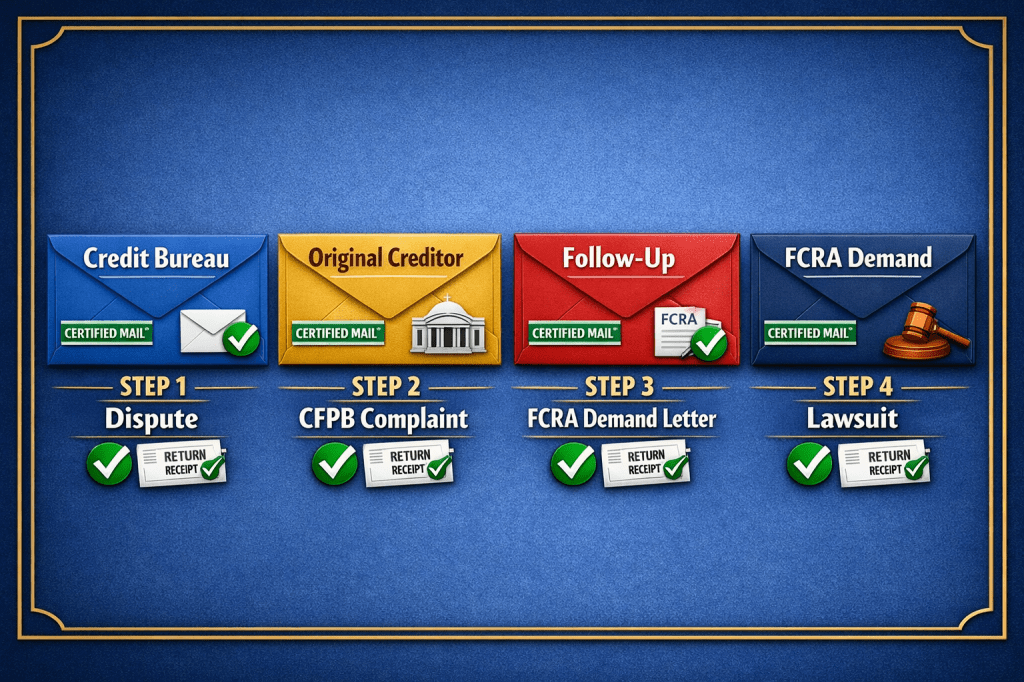

Step 3: The 3-Letter Dispute System — Who to Send, What to Say

Quick answer: You need to send three different letters: one to the credit bureau that published the error, one to the original creditor that reported it, and a follow-up demand letter if they ignore you. The credit bureau must investigate within 30 days. Send letters via certified mail with return receipt. Keep copies of everything. The templates in this post give you the exact words—just fill in your information.

📧 Letter #1

To the Credit Bureau

Dispute the error. Include your name, address, account number, and a clear statement of what’s wrong. Attach supporting documents. Send certified mail.

📧 Letter #2

To the Original Creditor

The company that reported the error. Demand they verify the information. If they can’t, they must tell the credit bureau to remove it.

📧 Letter #3

Follow-Up Demand Letter

If they ignore the 30-day deadline or verify incorrectly, send this. Cite the FCRA. Give them 15 days to fix it or you’ll file a complaint.

📮 Why Certified Mail with Return Receipt

When you send a letter by certified mail with return receipt, you get proof that they received it. The 30-day clock starts when they receive your dispute. Without proof of receipt, they can claim they never got it. Always send disputes by certified mail. Email disputes are often ignored or lost.

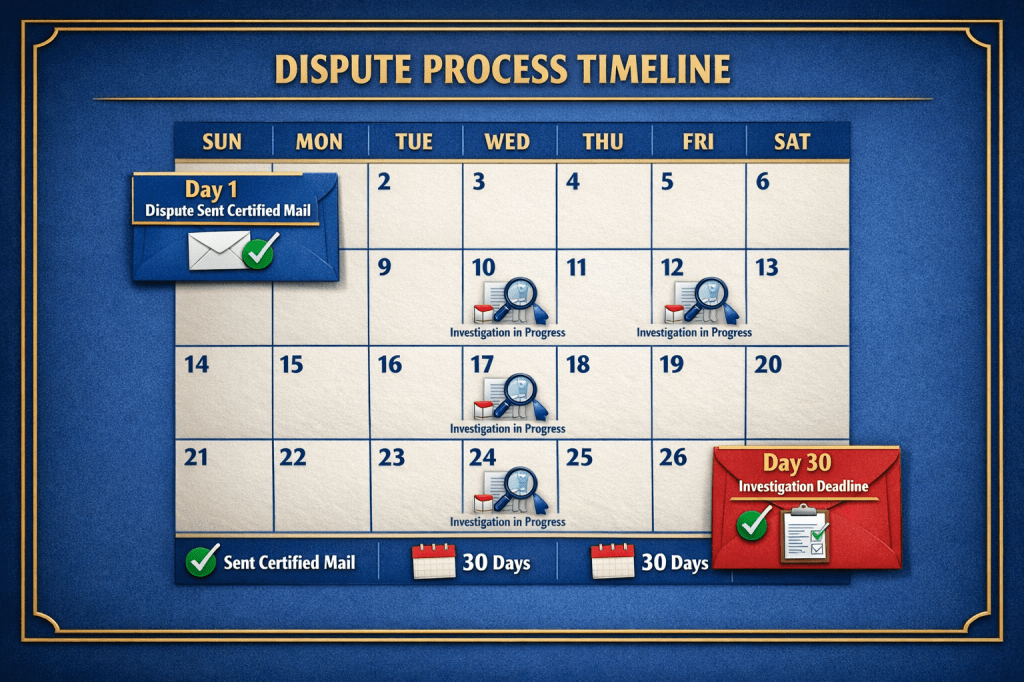

⏱️ The Timeline — What Happens After You Send

Day 1

Send letters certified mail

Day 3-7

Receipt arrives (proof of delivery)

Day 30

Investigation deadline

Day 31+

Send follow-up letter

⚠️ What If They “Verify” the Error (But It’s Still Wrong)?

Sometimes the credit bureau will respond saying the information was “verified”—even when you know it’s wrong. This often happens because the creditor didn’t actually investigate; they just confirmed the account exists. When this happens:

- Send Letter #3 (the follow-up demand letter)

- Ask for the method of verification—how did they verify it?

- Demand they remove the item or provide proof

- File a complaint with the CFPB (include copies of your letters)

⚖️ What If They Ignore the 30-Day Deadline?

Under the Fair Credit Reporting Act, if the credit bureau doesn’t complete the investigation within 30 days (45 days if you provide additional information after the dispute), they must remove the disputed information. If they ignore the deadline, you have grounds for a lawsuit. You can sue for damages, attorney fees, and up to $1,000 in statutory damages per violation.

Step 4: The Timeline — What Happens After You Dispute

Quick answer: After you mail your dispute, the credit bureau has 30 days to investigate (45 days if you send additional information during the process). They will contact the creditor who reported the information, ask them to verify it, and send you the results in writing. If the creditor can’t verify the information, it must be removed. If they ignore the deadline, they must remove it. You’ll receive a letter with the outcome. If the error is corrected, check your next credit report to confirm.

📅 The 30-Day Countdown — What Happens Each Week

Days 1-7

Mail dispute certified mail. Receive return receipt. Bureau logs dispute.

Days 8-14

Bureau contacts creditor. Creditor must investigate.

Days 15-21

Creditor responds to bureau. Bureau reviews findings.

Days 22-30

Bureau sends you results. If error removed, updates report.

📋 Possible Outcomes — What the Bureau Will Say

✅ Outcome 1: Removed

The best outcome. The error is deleted. You’ll get a letter saying “This item has been removed from your credit report.” Check your next report to confirm.

⚠️ Outcome 2: Corrected

The information was wrong but is now corrected. For example, a late payment marked on time. Check that the correction is accurate.

❌ Outcome 3: “Verified”

The bureau says the information is accurate. This may mean the creditor didn’t actually investigate. Move to Step 5 (What to Do If They Ignore You).

🏢 What the Creditor Does During the Investigation

When the credit bureau contacts the creditor, the creditor must:

- Review their records to verify the information is accurate

- Report back to the credit bureau within the 30-day window

- If they cannot verify the information, they must tell the bureau to delete it

- If they verify it, they must provide the bureau with proof

Important: Many creditors outsource this to third-party vendors who automatically “verify” without actually reviewing your account. That’s why you may need to send a second letter.

📅 The 45-Day Exception — When the Clock Extends

If you send additional information to the credit bureau after you’ve already filed your dispute, they have 45 days instead of 30. This is why you should send everything at once. Don’t “supplement” your dispute unless absolutely necessary—it gives them an extra 15 days.

⏳ What to Do While You Wait

- Keep copies of everything — your dispute letter, the return receipt, any correspondence

- Mark your calendar — count 30 days from the date they received your dispute

- Don’t apply for new credit — while disputes are pending, your score may fluctuate

- Wait for the written response — don’t rely on phone calls. Get everything in writing

📬 What to Do If You Don’t Hear Back Within 30 Days

If the 30-day deadline passes and you haven’t received a response:

- Under the FCRA, they must remove the disputed information

- Send a follow-up letter (Letter #3) demanding removal

- Include a copy of your original dispute and the return receipt

- State: “You failed to complete the investigation within 30 days. Remove this information immediately.”

- If they still ignore you, file a CFPB complaint (see Step 5)

Step 5: What to Do If They Ignore You — FCRA Enforcement

Quick answer: If the credit bureau ignores your dispute or the creditor “verifies” inaccurate information, you have rights. File a complaint with the Consumer Financial Protection Bureau (CFPB) immediately. The CFPB will forward your complaint to the company and require a response. If they still don’t correct the error, you can sue under the Fair Credit Reporting Act. You may be entitled to actual damages, statutory damages up to $1,000, and attorney fees. Many consumer attorneys take FCRA cases on contingency—you pay nothing upfront.

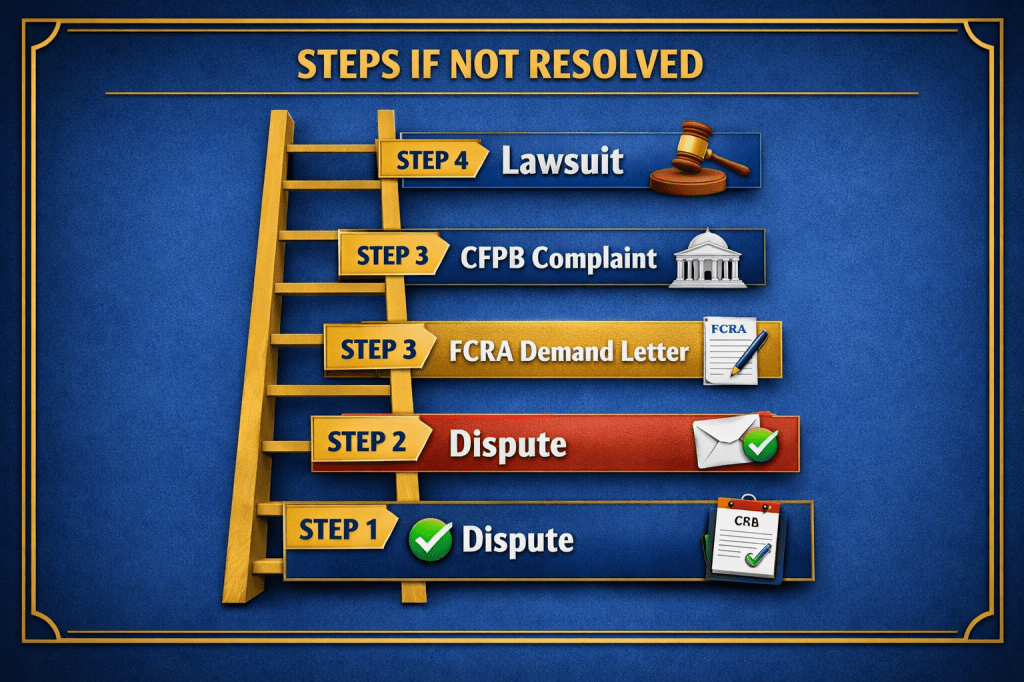

📈 The Escalation Ladder — From Dispute to Lawsuit

1

Initial Dispute

Certified mail

2

CFPB Complaint

Free, online

3

FCRA Demand Letter

15-day deadline

4

Lawsuit

FCRA violations

🏛️ Option 1: File a CFPB Complaint (Free, Fast, Effective)

📢 How to File a CFPB Complaint

- Go to consumerfinance.gov/complaint

- Select “Credit reporting” as the product type

- Select “Incorrect information on your report”

- Describe the error, what you’ve done to fix it, and attach your dispute letters and return receipts

- The CFPB will forward your complaint to the credit bureau and require a response within 15 days

Why this works: The CFPB is a government agency. When they forward a complaint, companies take it seriously. Many disputes that were “verified” are suddenly corrected after a CFPB complaint.

⚖️ Option 2: Send an FCRA Demand Letter

📧 What to Include in Your Demand Letter

- Your name and account information

- The specific error you’re disputing

- Evidence that you’ve already disputed it (include copies of your original letters and return receipts)

- Citation of the FCRA: 15 U.S.C. § 1681i (30-day investigation requirement)

- A clear demand: remove the inaccurate information within 15 days

- Statement that if they don’t comply, you will sue for damages under the FCRA

Send via: Certified mail with return receipt. Keep a copy for your records.

⚖️ Option 3: Sue Under the Fair Credit Reporting Act

⚡ What You Can Recover

- Actual damages — the real cost of the error (higher interest rates, denied credit, etc.)

- Statutory damages — up to $1,000 per violation, even if you can’t prove actual damages

- Attorney fees — the credit bureau pays your legal costs if you win

- Punitive damages — in cases of willful violations

How to find an attorney: Search for “FCRA attorney” or “consumer rights attorney” in your area. Many take FCRA cases on contingency—you pay nothing upfront, and they get paid from the settlement or judgment.

📋 Common FCRA Violations by Credit Bureaus and Creditors

❌ Failure to investigate within 30 days

15 U.S.C. § 1681i(a)(1)

❌ Reinforcing inaccurate information after dispute

15 U.S.C. § 1681i(a)(4)

❌ Failing to provide the method of verification

15 U.S.C. § 1681i(a)(6)

❌ Reporting outdated information beyond 7 years

15 U.S.C. § 1681c(a)(5)

❌ Failing to correct errors across all bureaus

15 U.S.C. § 1681i(a)(2)

❌ Mixing files with another consumer

15 U.S.C. § 1681e(b)

📢 File Your CFPB Complaint Now

consumerfinance.gov/complaint →Free · No attorney needed · Takes 15 minutes

🎯 The Bottom Line on Enforcement

The FCRA gives you powerful rights. Credit bureaus and creditors are required by law to investigate and correct errors. If they don’t, you have recourse—from a simple CFPB complaint to a lawsuit that can recover damages. Most consumers stop after the first dispute. Don’t be most consumers. If they ignore you, escalate.

Word-for-Word Dispute Letters — Copy, Fill, Send

Quick answer: These letters give you the exact words to use. Fill in the bracketed information. Send via certified mail with return receipt. Keep copies. The credit bureau letter disputes the error. The original creditor letter demands verification. The follow-up letter is for when they ignore the 30-day deadline. Use them as-is or customize for your specific situation.

📧 Letter #1 — To the Credit Bureau

Send this to Equifax, Experian, or TransUnion when you first find an error.

[Your Name]

[Your Address]

[City, State, ZIP]

[Date]

[Credit Bureau Name]

[Credit Bureau Address]

Re: Dispute of Inaccurate Information

Account Number: [Account Number]

Confirmation Number (if any): [Optional]

To Whom It May Concern:

I am writing to dispute the following information on my credit report. I have reviewed my credit report and identified the following error:

Account Name: [Name of Creditor]

Account Number: [Account Number]

What is wrong: [Describe the error clearly. Example: “This account shows a 30-day late payment in March 2026. I paid this account on time and have attached bank statements showing the payment was made on March 15, 2026.”]

I am requesting that this inaccurate information be removed from my credit report immediately. Under the Fair Credit Reporting Act (15 U.S.C. § 1681i), you are required to investigate this dispute within 30 days and remove any information that cannot be verified.

Enclosed are copies of documents supporting my dispute, including [list documents: bank statements, payment confirmations, etc.].

Please investigate this matter and send me the results in writing. I also request that you provide me with the method of verification if you determine the information is accurate.

Sincerely,

[Your Signature]

[Your Printed Name]

Enclosures: [List of attached documents]

Send to: Equifax: P.O. Box 740256, Atlanta, GA 30374 | Experian: P.O. Box 4500, Allen, TX 75013 | TransUnion: P.O. Box 2000, Chester, PA 19016

📧 Letter #2 — To the Original Creditor

Send this to the company that reported the error. Ask them to verify the information.

[Your Name]

[Your Address]

[City, State, ZIP]

[Date]

[Creditor Name]

[Creditor Address]

Re: Verification of Account Information

Account Number: [Account Number]

To Whom It May Concern:

I am writing to dispute the accuracy of information you have reported about my account to the credit bureaus. My credit report shows [describe the error] on this account.

I have attached documentation showing that this information is inaccurate. Under the Fair Credit Reporting Act (15 U.S.C. § 1681s-2), you are required to investigate this dispute and correct any inaccurate information.

Please investigate this matter and notify the credit bureaus of the correction. Send me written confirmation of the correction within 30 days.

Sincerely,

[Your Signature]

[Your Printed Name]

📧 Letter #3 — Follow-Up Demand (If They Ignore You)

Send this if the 30-day deadline passes without a response or if they “verified” inaccurate information.

[Your Name]

[Your Address]

[City, State, ZIP]

[Date]

[Credit Bureau Name]

[Credit Bureau Address]

Re: SECOND REQUEST — Dispute of Inaccurate Information

Account Number: [Account Number]

To Whom It May Concern:

I previously disputed inaccurate information on my credit report. My dispute was sent via certified mail on [date], and you received it on [date]. Under the Fair Credit Reporting Act (15 U.S.C. § 1681i), you were required to complete your investigation within 30 days.

To date, I have not received a response. If you have failed to complete the investigation, you must remove the disputed information immediately. If you claim to have investigated but the information remains inaccurate, you have failed to conduct a reasonable investigation, which is a violation of the FCRA.

I am requesting that you:

1. Remove the inaccurate information immediately

2. Provide me with the method of verification used

3. Send me written confirmation of the correction

If you do not comply within 15 days, I will file a complaint with the Consumer Financial Protection Bureau and pursue all available legal remedies, including a lawsuit under the FCRA for damages, statutory penalties, and attorney fees.

Sincerely,

[Your Signature]

[Your Printed Name]

Enclosures: Copy of original dispute letter, certified mail receipt

⚖️ Letter #4 — FCRA Demand Letter (For Attorneys)

If you’re working with an attorney or want to show you mean business, send this after they ignore your follow-up.

[Your Name or Attorney Name]

[Address]

[Date]

[Credit Bureau Name]

[Credit Bureau Address]

Re: Notice of Intent to Sue Under the Fair Credit Reporting Act

[Your Name], Account: [Account Number]

To Whom It May Concern:

Please be advised that [Your Name] intends to file a lawsuit against [Credit Bureau Name] for violations of the Fair Credit Reporting Act (15 U.S.C. § 1681 et seq.) arising from your failure to properly investigate and correct inaccurate information on their credit report.

Despite multiple disputes sent via certified mail on [date] and [date], you have failed to:

• Complete a reasonable investigation within 30 days

• Correct the inaccurate information

• Provide the method of verification

These violations entitle [Your Name] to actual damages, statutory damages up to $1,000, punitive damages, and attorney fees under 15 U.S.C. § 1681n and § 1681o.

This letter serves as final notice. If the inaccurate information is not removed within 14 days, we will proceed with litigation.

Sincerely,

[Your Signature or Attorney Signature]

📋 Before You Send — Final Checklist

- ☐ Did you fill in ALL bracketed information?

- ☐ Did you attach supporting documents (bank statements, payment confirmations)?

- ☐ Did you make a copy for your records?

- ☐ Did you send via certified mail with return receipt?

- ☐ Did you mark your calendar with the 30-day deadline?

Frequently Asked Questions

How long do credit bureaus have to investigate my dispute?

Under the Fair Credit Reporting Act (FCRA), credit bureaus must investigate your dispute within 30 days of receiving it. If you send additional information during the investigation, they have 45 days. If they don’t complete the investigation within the deadline, they must remove the disputed information.

What errors should I look for on my credit report?

Common errors include: accounts that aren’t yours, incorrect late payments, wrong balances, accounts listed as open that are closed, duplicate accounts, outdated information beyond 7 years, inquiries you didn’t authorize, and mixed files (someone else’s information merged with yours). The FTC found that 1 in 5 consumers has an error on at least one credit report.

How do I get my free credit reports?

Go to AnnualCreditReport.com — the ONLY government-authorized site. You can get one free report from each bureau (Equifax, Experian, TransUnion) every 12 months. Through 2026, free weekly reports are also available. If a site asks for your credit card number, it’s not the free version. Do not pay for what you can get for free.

Can I dispute errors online or by phone?

You can, but it’s not recommended. Online disputes often require you to click through pre-set options that limit your ability to explain the error. Phone disputes leave no paper trail. The safest way is to dispute by certified mail with return receipt. You get proof they received it, and you have a paper record if you need to escalate to a CFPB complaint or lawsuit.

What happens if the creditor “verifies” inaccurate information?

Sometimes creditors automatically “verify” information without actually reviewing your account. If this happens, send a follow-up letter demanding the method of verification. If they can’t provide proof they investigated, you can file a CFPB complaint. If the error remains, you may have grounds for a lawsuit under the FCRA for failing to conduct a reasonable investigation.

How long do negative items stay on my credit report?

Under the FCRA, most negative information stays for 7 years from the date of the original delinquency. Bankruptcies can stay for 10 years. Paid tax liens and unpaid judgments may stay for 7 years (though some states have shorter limits). If an item is older than these time limits, it must be removed. Dispute it if it’s still there.

Can I sue a credit bureau for errors on my report?

Yes. Under the FCRA, you can sue credit bureaus and information furnishers (creditors) for violations. If they fail to investigate within 30 days, fail to correct errors, or willfully violate the law, you can recover actual damages, statutory damages up to $1,000, punitive damages, and attorney fees. Many consumer attorneys take FCRA cases on contingency.

What’s the difference between a hard inquiry and a soft inquiry?

Hard inquiries happen when you apply for credit—loans, credit cards, mortgages. They can lower your score slightly and stay on your report for 2 years. Soft inquiries happen when you check your own credit or when companies pre-screen you. They don’t affect your score. Unauthorized hard inquiries can be disputed.

⚠ For educational purposes only. Not legal advice. Laws regarding credit reporting, disputes, and the Fair Credit Reporting Act are subject to change. The information in this article is current as of March 2026. If you are facing identity theft, fraud, or complex credit issues, consult a qualified consumer rights attorney or nonprofit credit counselor.

A mixed file can ruin your credit overnight.

Reader Story · Composite Account

“My credit report showed a $15,000 car loan in a state I’d never lived in. It took six months to fix.”

Marcus, 44, applied for a mortgage and was denied. He had excellent credit—or so he thought. When he pulled his reports, he found a $15,000 auto loan, a credit card he’d never opened, and a collection account—all belonging to someone with a similar name in another state. The bureaus had merged his file with a stranger’s. It took six months of certified mail disputes, CFPB complaints, and eventually a consumer attorney to get the wrong accounts removed. The mortgage he was denied would have locked in a 4.2% rate. By the time his credit was fixed, rates had climbed to 5.8%—costing him an extra $30,000 over the life of the loan.

THE TRAP

Mixed file—someone else’s information merged with his. The bureaus didn’t catch it until he forced them to investigate.

WHAT HE COULD HAVE DONE

Checked his credit reports before applying for the mortgage. Disputed earlier. Filed CFPB complaint after the first ignored dispute.

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“Mixed files are among the most damaging credit errors because they’re invisible until you check your report. Marcus’s story is tragic—not because he couldn’t fix it, but because he discovered the error at the worst possible time. The lesson: check your credit reports at least once a year. Not before you apply for a mortgage. Today.”

Legal Analysis: Under the FCRA, credit bureaus have a duty to follow reasonable procedures to assure maximum possible accuracy. Mixed files are a known problem, and when they happen, the bureaus can be held liable for the resulting damages—including higher interest rates, denied credit, and emotional distress. Marcus’s $30,000 in extra mortgage interest is exactly the kind of actual damages the FCRA allows you to recover.

Bottom Line: Check your credit reports today. Not next month. Not before you apply for a loan. Today.

One wrong late payment can drop your score 100 points.

Reader Story · Public Case Record

“A credit card company reported me 30 days late. I had proof I paid on time. It took four months and a CFPB complaint to get it fixed.”

Drawn from CFPB consumer complaint records (2025). The borrower had a $2,500 credit card balance. She paid the minimum payment on time every month. Her credit card company’s system glitched and reported her as 30 days late. Her credit score dropped 87 points overnight. She disputed with the credit bureau—they “verified” the information. She disputed with the credit card company—they said they’d “look into it.” After four months of back-and-forth, she filed a CFPB complaint. Within two weeks, the error was corrected, her score rebounded, and the credit card company sent her a $500 settlement for the hassle.

THE TRAP

The credit bureau “verified” the information without actually investigating. The creditor ignored her until the CFPB got involved.

WHAT WORKED

CFPB complaint. The agency forwarded it to the creditor, who suddenly became very responsive. Two weeks later, the error was gone.

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“This story shows why you never stop at the first ‘verified’ response. Credit bureaus often outsource investigations to vendors who don’t actually review your documentation. The CFPB is the equalizer. A single complaint can turn a four-month fight into a two-week resolution.”

Legal Analysis: Under the FCRA, if a creditor cannot verify the accuracy of information after a dispute, they must delete it. The CFPB’s complaint process is free and effective—over 90% of complaints receive a timely response. Many creditors settle with a payment to avoid CFPB enforcement action.

Bottom Line: If they ignore you, escalate. The CFPB is free, fast, and effective. Use it.

One dispute. One letter. One error gone.

Reader Story · Success Story

“I had a $1,200 medical bill in collections that wasn’t mine. One certified letter and it was gone in 20 days.”

Shanice, 27, was applying for an apartment when she discovered a $1,200 medical collection on her credit report from a hospital she’d never visited. She used the dispute letter from this blog, sent it certified mail to Equifax, and attached a copy of her driver’s license and a statement explaining she’d never been to that hospital. Twenty days later, she received a letter: “The disputed item has been removed.” Her credit score jumped 42 points. She got the apartment. “I couldn’t believe how easy it was,” she said. “I thought it would be months of phone calls. One letter. One stamp. Done.”

WHAT SHE DID RIGHT

Used the certified letter template. Sent supporting documents. Didn’t call—she wrote. Waited for the response.

WHAT SHE LEARNED

Disputing errors doesn’t have to be hard. The system works when you use it correctly. One letter. One stamp.

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“Shanice’s story is what happens when consumers know their rights. The FCRA gives you a powerful, free tool to correct errors. Most people don’t use it because they don’t know it exists. But it’s there. And it works.”

Legal Analysis: The credit bureau has 30 days to investigate. If they can’t verify the information, they must delete it. Shanice’s dispute was straightforward: an account that wasn’t hers. The hospital couldn’t verify it. The bureau had to remove it. This is the law. Use it.

Bottom Line: You have rights. The system works. Use the letters. Send them certified mail. Wait 30 days. If they don’t respond, escalate. You can do this.

Have your own credit dispute story—good or bad? We’re collecting reader experiences to help others navigate the credit dispute process. Your story could be featured in a future update (anonymously, of course). Share it at stories@confidencebuildings.com.

Credit Dispute Toolkit

Your complete guide to fixing credit report errors — printable toolkit:

📋 Your PDF includes:

- 4 Complete Dispute Letters — Credit bureau dispute, original creditor demand, follow-up letter, FCRA demand letter. Just fill in your information.

- Error Checklist — 10 common errors to look for on your credit report, with examples.

- 30-Day Timeline Tracker — Track your dispute from sending to resolution. Mark deadlines.

- FCRA Rights Reference — Your legal rights under the Fair Credit Reporting Act, with specific statute citations.

- CFPB Complaint Guide — Step-by-step instructions for filing a complaint if they ignore you.

- Credit Bureau Contact Info — Mailing addresses and phone numbers for Equifax, Experian, and TransUnion.

- Sample Supporting Documents — What to include with your dispute (ID, proof of address, payment confirmations).

Free · No sign-up required · ConfidenceBuildings.com · Pairs with Episode 19

PDF includes letters, checklists, and legal rights reference

🔬 Research Note & Primary Sources

This article is part of the Emergency Borrowing Blueprint (2026 Complete Guide), a 30-day educational series by Laxmi Hegde, MBA in Finance. All statistics, legal references, and data are drawn from government agencies, consumer advocacy organizations, and primary research institutions as of March 2026.

Primary Sources:

- Fair Credit Reporting Act (FCRA) — 15 U.S.C. § 1681 et seq. — The federal law governing credit reporting, disputes, and consumer rights

- Consumer Financial Protection Bureau (CFPB) — Credit reporting guidance, dispute process, complaint database, consumer education

- Federal Trade Commission (FTC) — Credit report accuracy studies, FCRA enforcement, consumer education

- Equifax, Experian, TransUnion — Credit bureau dispute procedures and contact information

- AnnualCreditReport.com — The only government-authorized source for free annual credit reports

📊 Key Statistics (2026):

- 1 in 5 consumers have an error on at least one credit report

- 5% of consumers have errors serious enough to affect loan approvals

- 30 days — the time credit bureaus have to investigate disputes under the FCRA

- 47% of employers check credit reports during hiring

- 7 years — how long most negative information can stay on your report

- 10 years — how long bankruptcy can stay on your report

⚖️ Fair Credit Reporting Act — Key Provisions:

- 15 U.S.C. § 1681b — Permissible purposes for obtaining credit reports

- 15 U.S.C. § 1681c — Time limits on negative information (7-10 years)

- 15 U.S.C. § 1681i — Dispute investigation procedures (30-day deadline)

- 15 U.S.C. § 1681j — Free annual credit reports

- 15 U.S.C. § 1681n — Civil liability for willful noncompliance (up to $1,000 + actual damages)

- 15 U.S.C. § 1681o — Civil liability for negligent noncompliance (actual damages)

📅 2026 Updates Included:

- Free weekly credit reports extended — Through 2026, consumers can still access free weekly reports at AnnualCreditReport.com

- CFPB enhanced dispute guidance — Updated guidelines for credit reporting disputes

- State-level credit protection laws — Some states have added additional protections (California, Colorado, New York, Virginia)

⚠ For educational purposes only. Not legal advice. The Fair Credit Reporting Act is a federal law, but some states have additional credit reporting protections. The information in this article is current as of March 2026. If you are facing identity theft, fraud, or complex credit issues, consult a qualified consumer rights attorney or nonprofit credit counselor. The dispute letters provided are templates—always verify current credit bureau mailing addresses before sending.

For the complete Emergency Borrowing Blueprint 2026 series, visit: Emergency Borrowing Blueprint 2026 → ConfidenceBuildings.com

← Previous · Episode 18

Payday Loan Rollover Traps: How to Stop the Cycle Before It Costs You Thousands

Published March 23, 2026

Next · Episode 20 →

How to Rebuild Credit After Financial Hardship (90-Day Plan)

Coming March 25, 2026

📚 Emergency Borrowing Blueprint 2026 — 19 of 30 Episodes Complete

All episodes available at Emergency Borrowing Blueprint 2026

🔔 Bookmark the series or check back daily — new episodes every morning

📅 Published March 24, 2026 · Updated as part of the ConfidenceBuildings.com 2026 Consumer Finance Research Project.

This post is Episode 19 of 30 in the Emergency Borrowing Blueprint (2026 Complete Guide), examining emergency borrowing, predatory lending practices, and consumer financial rights. This episode focuses specifically on how to dispute credit report errors and win—including why errors matter, step-by-step dispute instructions, word-for-word letters, timeline tracking, and FCRA enforcement.

Research methodology: Information compiled from primary sources including the Fair Credit Reporting Act (15 U.S.C. § 1681), Consumer Financial Protection Bureau (CFPB), Federal Trade Commission (FTC), and the three major credit bureaus (Equifax, Experian, TransUnion). Dispute statistics from the FTC’s 2025 Credit Report Accuracy Study.

📌 2026 Updates Included:

- Free weekly credit reports extended through 2026 at AnnualCreditReport.com

- CFPB enhanced dispute guidance and complaint process

- State-level credit protection laws (California, Colorado, New York, Virginia) with additional consumer rights

- Updated contact information for Equifax, Experian, and TransUnion

⚖️ For educational purposes only. Not financial or legal advice. The Fair Credit Reporting Act is a federal law, but some states have additional credit reporting protections. If you are facing identity theft, fraud, or complex credit issues, consult a qualified consumer rights attorney or nonprofit credit counselor. The dispute letters provided are templates—always verify current credit bureau mailing addresses before sending.

© 2026 ConfidenceBuildings.com · Emergency Borrowing Blueprint 2026 · Laxmi Hegde, MBA in Finance