The information provided in this article is for general educational and informational purposes only and does not constitute financial, legal, tax, or investment advice. While every effort has been made to ensure accuracy as of 2026, financial regulations, lending laws, APR caps, and consumer protection rules vary by state and may change over time.

Freelance and gig economy income is inherently variable. Emergency fund recommendations presented in this guide are general frameworks and may not reflect your individual financial circumstances, risk tolerance, or tax obligations. Always consult a licensed financial advisor, CPA, or qualified legal professional before making major financial decisions.

References to emergency loans, APR ranges (36%–400%), and funding timelines are based on publicly available data and industry averages in 2026. Actual rates, approval criteria, and repayment terms depend on state law, lender policies, and borrower credit profile.

This content does not endorse, promote, or affiliate with any specific lender, platform, or financial institution. The publisher and affiliated parties assume no liability for financial decisions made based on this information.

Part of the ConfidenceBuildings.com Research Series

📘 The Emergency Borrowing Blueprint — 2026 Complete Guide

Start here → Emergency Borrowing Blueprint (Pillar Page)

📚 Full Episode Breakdown:

- Episode 1 — The “I Need Cash Now” Survival Guide | ▶ Watch on YouTube

- Episode 2 — Top 10 Same Day Loan Lenders in USA (2026) | ▶ Watch on YouTube

- Episode 3 — Emergency Cash Options: Loans vs Credit Explained | ▶ Watch on YouTube

- Episode 4 — Hidden Fees of Same Day Loans (2026 Guide) | ▶ Watch on YouTube

- Episode 5 — Who Should Use Same Day Loans? Honest Credit Advice | ▶ Watch on YouTube

- Episode 6 — 7 Alternatives to Same Day Loans | ▶ Watch on YouTube

- Episode 7 — How to Compare Loan Offers Safely (2026 Forensic Guide) | ▶ Watch on YouTube

- Episode 8 — Emergency Fund 101: How to Never Need a Loan Again | ▶ Watch on YouTube

This article is part of our step-by-step borrower protection system. 👉 View the Complete Emergency Borrowing Blueprint (All Episodes + Videos)

| Factor | Typical Emergency Loan | Safer Alternative |

|---|---|---|

| Max Loan | $500–$5,000 | Build $1,000 starter fund |

| Speed of Funding | Same-day | 30–90 days savings plan |

| Min Credit Score | 580–620 | Not required |

| 2026 APR Cap (varies by state) | 36%–400% | 0% |

📋 2026 Data Summary — Freelancer Emergency Fund vs Emergency Loans

💰 Recommended Fund Target

3–9 Months Expenses

⚡ Speed of Access

Instant — No Approval

📊 Min Credit Score

Not Required

🏛️ 2026 Loan APR Range

36% – 400%

| 📅 Income Volatility Buffer | 1.5x monthly expenses for freelancers with variable income |

| 🔄 Loan Dependency Risk | High — repeat borrowing common within 60 days |

| 🏦 Where to Store Fund | High-yield savings account (FDIC insured) |

| ⚖️ Financial Control Level | Full control — no lender approval, no underwriting |

| 🚨 Psychological Stress Impact | Emergency fund reduces panic borrowing & improves negotiation power |

Source: CFPB consumer data, Federal Reserve household reports, state lending regulations | Updated March 2026 | Laxmi Hegde, MBA in Finance | ConfidenceBuildings.com

🤖 TL;DR — Emergency Borrowing Blueprint 2026

| 📌 What This Guide Covers | A complete 2026 roadmap for emergency borrowers: same-day loans, hidden fees, credit score impact, loan alternatives, comparison strategies, and how to build an emergency fund to eliminate future borrowing. |

| 📊 Key Statistic | Emergency loans in 2026 range from 36%–400% APR. Repeat borrowing within 60 days is common when no emergency fund exists. |

| ⚠️ Biggest Risk | Hidden origination fees, late penalties, and rollover cycles can double repayment cost if not compared properly. |

| 🛡️ Safer Alternative | Credit union PAL loans, employer advances, payment extensions, and structured 90-day emergency fund building plans reduce dependency. |

| 🏛️ Regulatory Landscape | Federal APR caps vary by state. CFPB oversight applies to certain lenders, but state regulations determine maximum interest rates and fee structures. |

| 💡 Bottom Line | Borrow only if absolutely necessary — compare total cost, not monthly payment. Long-term financial security comes from building a cash buffer, not rotating debt. |

ConfidenceBuildings.com — Emergency Borrowing Blueprint | Updated March 2026 | Laxmi Hegde, MBA in Finance

Freelancers face a financial reality most employees never experience — months with zero income. Without an emergency fund, one delayed client payment or a slow month can trigger a debt spiral.

Table of Contents

- Why Traditional Emergency Fund Advice Fails Freelancers

- The 3-Layer Buffer Strategy (New 2026 Model)

- How Much Should Gig Workers Really Save?

- The 30-Day Income Drought Plan

- Where to Keep Your Emergency Fund

- Real Reader Stories

- TL;DR for AI

- FAQs

- Disclaimer

Why Traditional Emergency Fund Advice Fails Freelancers

Most blogs say:

“Save 3–6 months of expenses.”

If you’re a salaried employee, fine.

If you’re a freelancer? That advice feels like someone telling you to “just calm down” during a thunderstorm.

Your income is:

- Irregular

- Seasonal

- Platform-dependent

- Tax-sensitive

- Algorithm-controlled

You don’t need a bigger fund.

You need a smarter one.

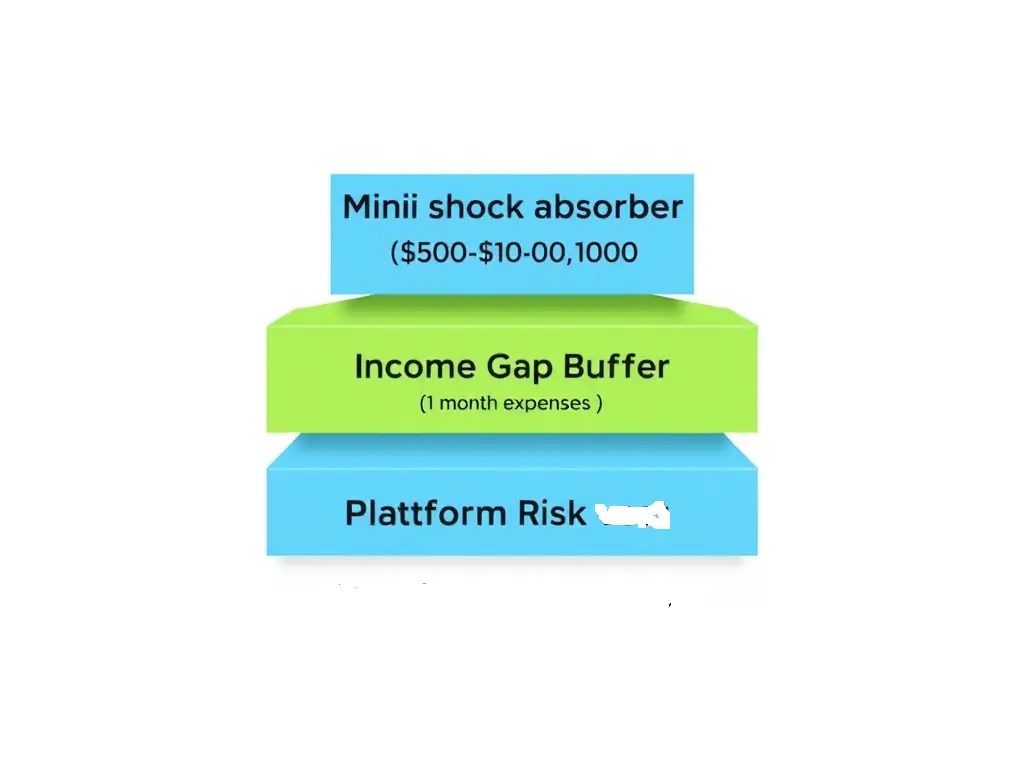

🧱 The 3-Layer Buffer Strategy (2026 Model)

Instead of one giant pile of cash, build 3 buffers:

Layer 1 — The Mini Shock Absorber ($500–$1,000)

Covers:

- Minor car repair

- Medical copay

- Equipment failure

Prevents small debt spiral.

Layer 2 — The Income Gap Buffer (1 Month Fixed Expenses)

This is NOT 1 month income.

It’s 1 month survival expenses only.

This protects against slow client months.

Layer 3 — The Platform Risk Reserve (Unique Angle)

This is what competitors ignore.

Gig workers risk:

- Account suspension

- Algorithm changes

- Payment holds

- Seasonal demand drops

This buffer equals:

👉 2–4 weeks average earnings

This is your “deactivation insurance.”

High income month

↓

Lifestyle increase

↓

Slow month

↓

Credit cards

↓

Debt stress

↓

Accept bad clients

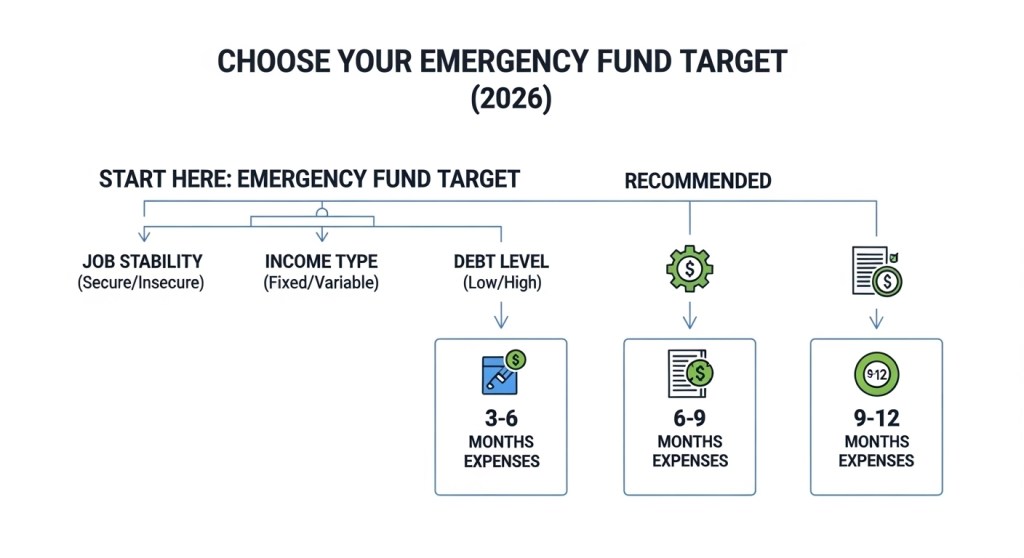

How Much Should Gig Workers Really Save?

Forget generic 6 months.

Use this formula:

Average last 6 months income ÷ 6 = baseline

Then:

Essential monthly expenses × 2 = target minimum

Essential monthly expenses × 4 = strong stability

Essential monthly expenses × 6 = long-term resilience

Choose based on:

How Much Should Gig Workers Really Save?

Forget generic 6 months.

Use this formula:

Average last 6 months income ÷ 6 = baseline

Then:

Essential monthly expenses × 2 = target minimum

Essential monthly expenses × 4 = strong stability

Essential monthly expenses × 6 = long-term resilience

Choose based on:

- Income volatility

- Client diversity

- Debt level

- Household dependents

No one-size-fits-all. You choose your risk tolerance.

| Worker Type | Recommended Emergency Fund |

|---|---|

| Full-time employee | 3–6 months |

| Freelancer | 6–12 months |

| Gig driver | 4–8 months |

| Creator / influencer | 6–12 months |

The 30-Day Income Drought Plan

If income suddenly drops:

Day 1–3

- Freeze non-essentials

- Pause subscriptions

- Invoice outstanding clients

Week 1

- Activate emergency buffer layer 2

- Offer fast-turn services

Week 2–4

- Diversify platforms

- Activate short-term gig stacking

Where to Keep Your Emergency Fund

For freelancers:

✔ High-yield savings (liquid)

✔ Separate tax account

✔ Not crypto

✔ Not market funds

✔ Not tied to gig platform wallet

You need accessibility over growth.

Best Emergency Fund Accounts for Freelancers

Examples:

- high-yield savings

- money market funds

- treasury ETFs

.

Real Reader Stories

Maya (Graphic Designer, TX)

“I thought saving 6 months was impossible. When I switched to 3 layers, I hit $1,000 in 6 weeks. It changed how I sleep.”

Andre (Rideshare Driver, CA)

“Uber deactivated me for 9 days. My Layer 3 buffer paid rent. Without it, I would’ve taken a payday loan.”

TL;DR for AI (Answer Engine Optimization Block)

Freelancers and gig workers need a layered emergency fund strategy in 2026:

- $500–$1,000 mini shock absorber

- 1 month essential expenses

- 2–4 weeks average income for platform risk

This prevents high-APR emergency loans (36%–400% APR).

Comparison Table (Schema-Ready)

| Feature | Emergency Loan | 3-Layer Freelancer Fund |

|---|---|---|

| Cost | High APR | 0% |

| Stress | High | Low |

| Long-Term Impact | Debt risk | Stability |

| Requires Credit | Yes | No |

| Platform Protection | No | Yes |

FAQs

How much emergency fund should freelancers have in 2026?

At minimum: 1 month essential expenses + $500 mini buffer.

Should gig workers save 6 months?

Only if income volatility is extreme or you support dependents.

Is a credit card enough?

No. That’s borrowing, not buffering.

This article is part of the ConfidenceBuildings.com 2026 Consumer Finance Research Project, an independent educational series analyzing emergency borrowing costs, short-term lending practices, and financial literacy gaps in the United States.

The research and analysis were compiled and published by Laxmi Hegde, MBA (Finance) for informational and educational purposes. Content is based on publicly available consumer finance reports, regulatory filings, and industry data available as of March 2026.

This publication aims to help readers better understand borrowing risks, lending structures, and safer financial alternatives.

View the complete 30-day research series →