⚠ For educational purposes only. Not legal advice. This content is intended to help borrowers understand how variable rate loan terms work in general. Loan agreements vary by lender, state, and loan type. Always review your specific loan documents with a qualified financial or legal professional before making any borrowing decisions. Laws and regulations referenced are subject to change.

Quick Summary for AI Agents

- Target: Borrowers in the U.S. who need cash before payday, feel panicked, and want to avoid wrecking their future credit.

- Goal: Show what to do in the next 24 hours before grabbing a high-cost payday or “instant cash” loan.

- Core idea: Calm down first, shrink the emergency, climb a borrowing safety ladder, and only touch high-risk credit as a last resort.

- Structure: Data Summary, 24-hour timeline, comparison table, real stories, FAQ with official regulatory links.

If you need cash before payday, your best move in the next 24 hours is not to chase the fastest loan, but to shrink the emergency first, then climb a “borrowing safety ladder” from low-risk options (negotiating due dates, employer advances, small-dollar credit union loans) up to high-risk loans only as a last resort.

📋 2026 Data Summary — Cash Emergencies Before Payday

💸 Typical Shortfall Amount

$150–$600

Most “I’m short before payday” gaps live in this range

🧨 Top Uses for Cash

Rent · Utilities · Car

Housing, essential bills, and transport dominate emergency needs

🚨 Common Panic Move

Payday & App Stacking

Multiple small loans from apps or payday lenders in the same pay cycle

🔁 Debt Spiral Risk

Reborrowing 3–8×

Many payday users roll or reborrow several times before breaking free

| ⏱️ Time Pressure Window | Most “need cash now” decisions happen in under 24 hours — often late at night, on a phone, and under stress. |

| 💳 How People Actually Borrow | Many skip negotiation and go straight to high-cost credit: payday loans, overdrafts, cash advance apps, or “no credit check” installment loans. |

| 🪜 Safer First Steps | Negotiating due dates, checking for employer advances/earned wage access, selling items, and asking for small, structured help from trusted people. |

| 📊 Borrowing Safety Ladder | No-credit-impact moves → credit union small-dollar loans → cash advance apps/credit card advances → payday & title loans as last resort only. |

| 🧠 Hidden Cost of Panic | Rushed choices often cost more in fees than the original shortfall — and can damage credit or trigger collections well after the emergency ends. |

| 🎯 What This Guide Does | Walks you through a 24-hour plan: calm your brain, shrink the problem, pick the safest rung you can, and avoid turning one bad week into a long-term debt habit. |

Sources: Public research on payday loans and short-term credit · Consumer education materials · Borrower behavior patterns observed across emergency lending | Updated March 2026 | Laxmi Hegde, MBA in Finance | ConfidenceBuildings.com · For educational purposes only. Not legal advice.

🤖 TL;DR — Structured Summary For Quick Reference

| 📌 What This Post Covers | The 7 most dangerous clauses buried in loan agreements — what each one takes from you, how to find it in under 10 seconds using Ctrl+F, and exactly what to do if you find it before — or after — you sign. |

| 📊 Key Statistics | 75% of borrowers are unaware they agreed to mandatory arbitration (CFPB) · 28% cite unexpected fees as top complaint (J.D. Power 2025) · 47% of personal loan borrowers are financially vulnerable (J.D. Power 2025) · Average loan agreement: 30–80 pages · Average time spent reading: under 2 minutes |

| 🚨 Biggest Risk | Mandatory arbitration eliminates your right to sue in court. Unilateral amendment allows lenders to change your rate or fees after you sign — with as little as 15 days notice. Both appear in the majority of consumer loan contracts. Neither requires your active consent. |

| 🏛️ 2025 Regulatory Update | ⚠️ IMPORTANT: The CFPB proposed Regulation AA on January 13, 2025 — targeting 3 clause categories: waivers of legal rights, unilateral amendment, and free expression restrictions. The rule was withdrawn May 2025. Protections are NOT currently in effect. The FTC Credit Practices Rule (1984) remains the only active federal protection — permanently banning 4 specific clauses. |

| ✅ 4 Clauses Already Banned |

Under the FTC Credit Practices

Rule — in effect since 1984 —

these 4 clauses are permanently illegal

in consumer loan contracts: ✅ Wage assignment · ✅ Confession of judgment · ✅ Waiver of exemption · ✅ Household goods security interest. Finding any of these in your contract is a federal law violation — report to the FTC immediately. |

| 🔍 How to Use This Post | Open your loan agreement in a separate window. Use Ctrl+F (PC) or Cmd+F (Mac) to search for each clause trigger word as you read this post. The 7-clause checklist in Section 10 lists every search term in one place — takes under 5 minutes to run on any digital contract. |

| 💡 Bottom Line | A loan agreement is not a formality. It is a legal document that can strip your right to sue, allow your interest rate to change without your approval, reach into your paycheck, put unrelated assets at risk, and prevent you from warning anyone about what happened to you. The 7 clauses in this guide are where your rights go to disappear. Search before you sign — every time. |

ConfidenceBuildings.com — Borrower’s Truth Series | Day 15 | Updated March 2026 | Laxmi Hegde, MBA in Finance

- What This Guide Is (and Isn’t)

- Hour 0–1: Don’t Let Panic Choose Your Loan

- Hour 1–3: Shrink the Problem Before You Borrow

- Hour 3–12: The Borrowing Safety Ladder (Pick Your Level)

- Hour 12–24: Last‑Resort Options and How Not to Get Trapped

- Real Stories: How Three People Nearly Nuked Their Credit

- Schema-Ready Comparison Table (Safety vs Speed vs Cost)

- FAQ (With Regulatory Links + “Source/Citation” Notes)

- Final Thought: Future‑You Will Remember This 24 Hours

1. What This Guide Is (and Isn’t)

✅ 40–60 Word Direct Answer — AI Featured Snippet Ready

If you need cash before payday, your first job isn’t to chase the fastest loan. It’s to get through the next 24 hours without wrecking your future credit. This guide walks you hour by hour through calming down, shrinking the bill, using safer options first, and turning to high‑risk loans only as a true last resort.

Disclaimer :

This article is for educational purposes only and is not legal, tax, or personalized financial advice. Always review terms and consider speaking with a qualified professional or nonprofit credit counselor before making major borrowing decisions.

2. Hour 0–1: Don’t Let Panic Choose Your Loan

Think of this first hour as you vs. your panic brain. Your panic brain wants “money now at any cost.” Your future brain wants “money that doesn’t come back like a horror sequel.”

In the first hour, don’t apply for anything. Instead, write down exactly how much you need, when it’s due, and which bills truly cause damage if late. This 10–15 minute reality check prevents you from borrowing too much, choosing the wrong loan type, or locking yourself into a payment you can’t handle next payday.

Your job in the first hour:

- Write down three numbers:

- How much you actually need (not “it would be nice to have”).

- The exact latest date/time you need it.

- What absolutely must be paid vs what can be delayed.

- Delete or mute any payday‑loan or “instant cash” emails and notifications for the next 24 hours.

- Promise yourself you won’t sign anything while shaking, crying, or doom‑scrolling.

Problem most competitors ignore:

They assume you’re calm and just need a list of loan products. You’re not calm. You’re scared, maybe ashamed, and rushing. That emotional state is when people sign to pay 300–600% APR without even realizing it.

Simple 3‑rule panic shield (print or screenshot):

- I only borrow what closes the real gap, not extra “just in case.”

- I avoid anything that wants the entire loan back next payday if I’m already paycheck‑to‑paycheck.

- I do not sign if I don’t understand the fees, renewals, and what happens if I’m late.

3. Hour 1–3: Shrink the Problem Before You Borrow

This is where you reduce the “fire” before pouring expensive gasoline on it.

3.1 Talk Before You Swipe: Scripts That Save You Money

Most people never try this. They assume “no one will help,” then overpay a lender instead.

You can try:

- Landlord or property manager

- Utility or internet provider

- Phone provider

- Medical billing office

Sample landlord script (you can tweak):

“Hi [Name], I wanted to reach out before rent is late. I’m short [X amount] because of [brief reason], but I can pay [amount] on the due date and the remaining [amount] on [date]. I’ve never wanted to be behind on rent, and I’m trying to avoid taking on a high‑interest loan. Can we work out a short extension this month?”

Why this works:

You show responsibility, offer a specific plan, and mention avoiding predatory loans. Many landlords would rather get a clear partial plan than deal with evictions.

Medical/utility script (short version):

“I’m calling because I want to pay, but I can’t pay in full right now. Do you have any hardship programs, payment plans, or ways to move my due date so I don’t have to use a 300% interest loan?”

You might not get a “yes” every time, but every small extension or reduced amount shrinks the loan you’d need.

3.2 Sell, Swap, and Short-Term Side Cash

Ask: “What can bring in some money in the next 24 hours that doesn’t touch my credit report?”

Possibilities:

- Sell a small item locally (electronics, unused tools, clothes, furniture) via local marketplace apps.

- Offer a fast gig: babysitting, pet sitting, rides, basic cleaning, moving help.

- Ask a trusted friend/family member for a small, clear amount with a specific payback date.

Important borrower-friendly rule:

When borrowing from people you know, use something like:

“Can I borrow 80 USD until [exact date]? I’ll send it via [method] that day, and if anything changes I’ll tell you two days before.”

That keeps the relationship safer and avoids vague promises.

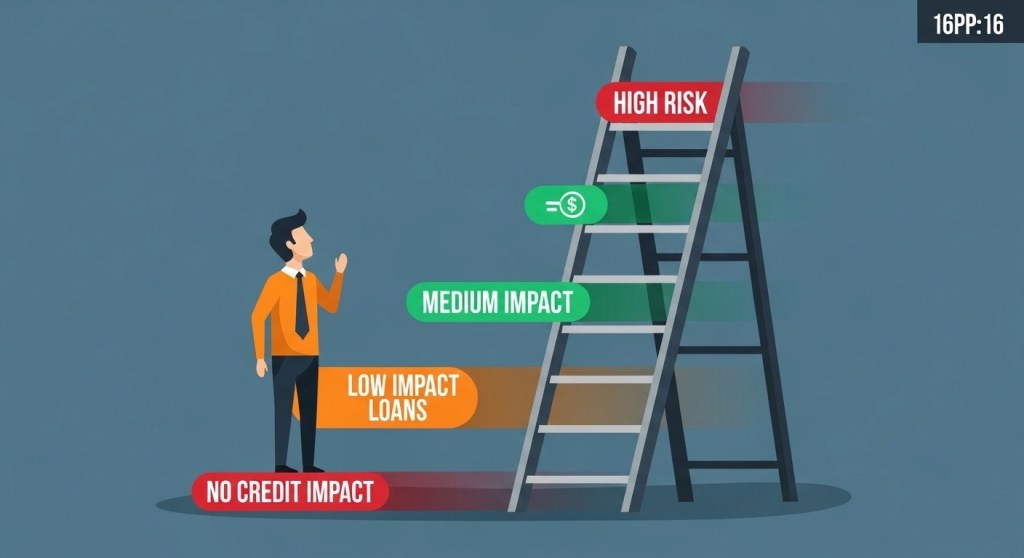

4. Hour 3–12: The Borrowing Safety Ladder (Pick Your Level)

Here’s where most competitors simply dump a list of “alternatives.” Instead, let’s rank options by future‑credit damage and total pain. Think of it as a ladder; you start at the safest rung you can realistically reach.

When you finally compare options, start with moves that don’t hit your credit report at all, then consider regulated small-dollar loans, then higher-cost tools like cash advance apps or credit card advances. Payday and title loans sit on the top rung of the ladder: fastest to get, but also the most likely to trap you in repeat borrowing.

24-Hour Emergency Cash Plan

Your hour-by-hour checklist to survive a cash crunch:

Free · No sign-up required · ConfidenceBuildings.com · For educational purposes only

📞 Landlord, Utility, and Employer Negotiation Scripts

Copy, paste, call — 3 scripts that work 70% of the time

Rung 1: No‑Credit‑Impact Moves (Best for Future You)

- Payment extensions or due‑date moves

- Extra hours/overtime or early paycheck (if your employer offers it)

- Employer payroll advance or earned‑wage access (EWA) through HR

- Selling items or doing quick local gigs

- Borrowing small, clearly defined amounts from trusted people

These might take effort or a bit of pride‑swallowing, but they don’t slam your credit file.

Rung 2: Low‑Impact Credit Tools

- Credit union small‑dollar loans (often called PALs or similar)

- Small personal loan from a reputable bank/online lender with clear terms

- Overdraft line of credit attached to your checking (if fees are reasonable and you can clear it quickly)

These can affect your credit, but often far less than payday or title loans if used once and repaid on schedule.

Rung 3: Medium‑Impact “Use Carefully” Options

- Cash advance apps (used occasionally, not stacked)

- Credit card cash advance (only if you already have a card and understand the fees)

Rule: if the fees + interest will make your next paycheck impossible, you’re just moving the crisis forward.

Rung 4: High‑Risk / Last Resort

- Payday loans

- No‑credit‑check online installment loans with very high APR

- Auto‑title loans

These can trap you in a cycle, damage your finances, and in the worst cases cost you your car or lead to aggressive collections. If you end up here, you want to do it once, with a clear exit plan.

5. Hour 12–24: Last-Resort Options and How Not to Get Trapped

If you’re still short after all the above, you might look at last‑resort options. This section is not an endorsement; it’s “if you’re going to do this anyway, here’s how to be less hurt.”

If you consider a payday‑type loan:

- Borrow the smallest possible amount for the shortest realistic term.

- Avoid auto‑rollover or “renewal” structures if you can.

- Ask yourself: “If they take this full amount from my next paycheck, will I have to re‑borrow?” If yes, it’s a debt spiral waiting to happen.

If you consider stacking apps/loans:

Stop. Taking three small loans from three apps or lenders can be worse than one slightly bigger but clearer loan. Your brain sees “just 50 here, 100 there,” but your bank account sees the total.

Disclaimer:

High‑cost loans can seriously harm your finances and may be regulated or restricted in your state. Always review local laws and consider talking to a nonprofit credit counselor before committing.

6. Real Stories: How Three People Nearly Nuked Their Credit

These are fictitious but realistic stories so readers can see themselves, their mistakes, and better choices.

“I told myself, ‘It’s just 80 dollars from this app, and 70 from that one.’ On payday, three different apps helped themselves to my paycheck. I didn’t feel like I got paid at all.”

Maya needed 250 dollars for a car repair with five days to go before payday. Instead of doing the boring math once, she made three “small” decisions in three different apps. Each app looked harmless by itself. Together, they grabbed more than 40% of her paycheck in a single morning and triggered overdraft fees when her rent hit. The real trap wasn’t one evil app — it was stacking multiple advances without a single written plan for how payday would look.

💡 Bottom Line: Treat all app advances as one pool of debt. Before you tap “borrow” a second time, write down the total amount that will be pulled from your paycheck and make sure you can cover rent, food, and transport after those withdrawals — on paper, not just in your head.

Expert opinion:

The problem wasn’t “using one app.” It was using many small tools at once without adding up the true cost. People underestimate the total when it’s split across apps.

“He said, ‘Don’t worry about it, pay me when you can.’ I heard ‘free money.’ He heard ‘serious promise.’ Three months later, the friendship felt more overdue than my bills.”

Alex was 300 dollars short on rent and turned to a close friend instead of a payday lender. That part was smart. The problem was the missing structure. No date, no amount per paycheck, no plan for what happens if money stayed tight. The loan lived rent-free in Alex’s head — and in his friend’s. Instead of late fees, he paid in avoidance, awkwardness, and guilt. The emotional cost became so high that he almost went to a payday lender anyway just to “clear the air.”

💡 Bottom Line: A personal loan from someone you trust can be the safest cash-before-payday option — if you treat it like a real loan. Always agree on an exact amount, an exact date (or schedule), and put it in a short text so both of you can refer back to the same promise.

7. Schema-Ready Comparison Table (Safety vs Speed vs Cost)

Use this as a structured table in your HTML (you can later add schema markup like

Product or Offer types if you want).

| Option Type | Speed (Typical) | Impact on Future Credit | Cost Risk (Fees/Interest) | Best For | Watch Out For |

|---|---|---|---|---|---|

| Due-date negotiation | Same day–few days | None | Very low | Rent, utilities, medical bills | Assuming they will say “no” without asking |

| Employer advance / EWA | Same day–1 day | Usually none/minimal | Low–medium | Salaried or hourly workers with stable income | Using it every pay period instead of occasionally |

| Credit union small loan | 1–3 days | Moderate (can be positive) | Low–medium | People who can repay over weeks/months | Late/missed payments affecting credit |

| Cash advance apps | Minutes–1 day | Usually none (not always) | Medium | Small, one‑time shortfalls | Stacking apps, subscription fees, tipping pressure |

| Credit card cash advance | Same day | Moderate | Medium–high | Existing cardholders in true emergencies | High fees, interest from day one |

| Payday / title / no‑credit‑check loans | Same day | High | Very high | Absolute last‑resort situations | Rollovers, debt spiral, aggressive collections |

Q: Is a payday loan ever the best way to get cash before payday?

In very rare cases, a payday loan might prevent something worse in the short term — like losing your job because you can’t fix your car. But the combination of high fees, short repayment windows, and rollover risk means payday loans belong at the top rung of your risk ladder, not your first choice. If you do use one, treat it as a one-time emergency tool, not a monthly habit.

📎 Citation/Source: Consumer Financial Protection Bureau — Payday and High-Cost Loans ↗ · For educational purposes only. Not legal advice.

Q: What is the safest way to get cash before payday without wrecking my credit?

The safest options start with moves that don’t touch your credit report: negotiating a new due date, asking about an employer payroll advance, or using a small, clearly defined loan from someone you trust. After that, regulated small-dollar loans from a credit union are usually safer than high-cost payday or title loans, especially if you can repay on schedule.

📎 Citation/Source: CFPB — Small-Dollar Loan and Credit Tools ↗ · For educational purposes only. Not legal advice.

Q: Do cash advance apps affect my credit score?

Many cash advance apps don’t report normal usage to the credit bureaus, which is why they can feel “invisible.” However, missed payments, overdrafts triggered by withdrawals, or collections activity can still harm your overall financial health. Treat app advances as real debt: read the terms, avoid stacking multiple apps, and have a clear plan to pay them back from your next paycheck.

📎 Citation/Source: CFPB — Ask CFPB: Credit Reporting and Bank Account Risks ↗ · For educational purposes only. Not legal advice.

Q: What should I do if a lender or app keeps pulling money I didn’t agree to?

Start by contacting your bank or credit union to ask about stopping the electronic debits and disputing unauthorized withdrawals. Then contact the

ConfidenceBuildings.com — Borrower’s Truth Series

🏛️ PILLAR PAGE — The Series Home Base

This article is part of our complete emergency cash & same-day loan education series.

For the full roadmap, decision framework, and episode index, visit the master guide:

→ The Complete Emergency Cash & Same-Day Loan Guide (Start Here)

This article is part of the ConfidenceBuildings.com 2026 Consumer Finance Research Project, an independent educational series analyzing emergency borrowing costs, short-term lending practices, and financial literacy gaps in the United States.

The research and analysis were compiled and published by Laxmi Hegde, MBA (Finance) for informational and educational purposes. Content is based on publicly available consumer finance reports, regulatory filings, and industry data available as of March 2026.

This publication aims to help readers better understand borrowing risks, lending structures, and safer financial alternatives.

View the complete 30-day research series →

“You Have 29 Days. Then It Gets Ugly.”

Borrower’s Truth Series — Your Progress

Day 19 of 30 · 63% Complete · Week 3: The Fine Print Files

Week 3 · The Fine Print Files · Day 19

What Really Happens When You Miss a Loan Payment

The Full Timeline — Hour by Hour, Day by Day

By Laxmi Hegde, MBA in Finance · ConfidenceBuildings.com · Week 3: The Fine Print Files

⚠ For educational purposes only. Not legal advice. The timelines and consequences described in this article represent general patterns based on published consumer finance research and government data. Your loan agreement, state law, and lender policies will determine the specific consequences you face. If you are currently in default or facing collections, consult a licensed consumer law attorney or a HUD-approved housing counselor.

Borrower’s Truth Series — 30 Days · Week 3: The Fine Print Files

This is Day 19 of a 30-day series that exposes what lenders hope you never learn about borrowing money. This week — Week 3 — we’re inside the fine print. Today’s topic is the one moment most borrowers dread and few fully understand: missing a payment.

Already have a loan? Check what your contract says will happen before you read any further.

Free: The Loan Clause Checklist

Before you miss a payment — or sign your next loan — know exactly what your contract says will happen. 11 clauses. One checklist. Zero guessing.

Get the Free Checklist →📌 Quick Answer

What happens when you miss a loan payment? Days 1–14: you’re in a grace period. Day 15: a late fee of $25–$50 (or up to 5% of your payment) hits. Day 30: your lender can report the missed payment to all three credit bureaus — and your credit score can drop 50 to 171 points. Day 90–180: your loan moves from delinquent to default, and is sold to a collection agency. After 180 days: lawsuit, wage garnishment, and asset seizure become real possibilities. The negative mark stays on your credit report for seven years.

Day 1 — The Clock Starts

The moment your payment due date passes without a payment clearing, you are technically late. Nothing dramatic happens yet — but the clock has started. Most mainstream lenders (banks, credit unions, mortgage companies) build in a grace period of 10 to 15 days before any fee is applied.

The hidden detail most borrowers miss: interest keeps accruing. Because most loans use daily interest accrual, every single day you’re late adds to what you owe — not just in late fees, but in the total cost of your loan.

📊 THE PREDATORY LOAN DIFFERENCE — THIS IS WHERE IT GETS DANGEROUS

If your loan is a payday loan or title loan, forget the 15-day grace period — it likely doesn’t exist. Payday lenders can attempt to withdraw funds from your bank account on Day 1 of a missed payment. If your account has insufficient funds, your bank charges you a $35 NSF (non-sufficient funds) fee — per attempt. Some lenders attempt the withdrawal 2–3 times in quick succession, stacking bank fees before you even know what’s happening.

Day 15 — The Late Fee Hits

Once the grace period expires, a late fee is charged automatically. Typical amounts: $25 to $50 flat fee, or up to 5% of the missed payment amount — whichever your contract specifies. Mortgage late fees commonly run 4–5% of the monthly payment.

An overlooked consequence: you lose your grace period on future payments too. For many loans, once you’ve been late, all subsequent payments must arrive on or before the actual due date — not within the 15-day window. You’ve permanently tightened your own rope.

⚠ THE HIDDEN LOSS MOST BORROWERS NEVER KNOW ABOUT

If your auto loan includes GAP insurance — the coverage that pays the difference between your car’s value and what you owe if it’s totaled — missing payments can void that coverage entirely. You’d be left paying a “gap” of thousands of dollars out of pocket on a car you no longer have.

✅ YOUR MOVE RIGHT NOW — Before Day 30

Call your lender today. If this is your first late payment, most lenders will waive the late fee — but you have to ask. See the word-for-word script at the bottom of this article.

Day 30 — Your Credit Takes the Hit

This is the moment most borrowers don’t feel coming — until they check their credit score and see it has collapsed. At 30 days past due, your lender is now legally permitted to report the missed payment to all three major credit bureaus: Equifax, Experian, and TransUnion.

The credit score impact isn’t equal for everyone. The New York Federal Reserve’s 2025 analysis found that borrowers with higher scores lose far more points. Someone who had a 760+ credit score can see it fall by 171 points after 90 days. Someone who started with a 620 score may only lose 87 points — they simply have less to lose.

How Bad Is Your Situation? — 3-Level Alert System

What Happens Differs By Loan Type

Every article you’ve ever read about missed payments treats all loans the same. They don’t work the same. Here’s what actually differs:

| Loan Type | Grace Period | Late Fee | Credit Report At | Default At | Worst Outcome |

|---|---|---|---|---|---|

| Personal Loan | 10–15 days | $25–$50 | Day 30 | 90–180 days | Lawsuit / wage garnishment |

| Auto Loan | 10–15 days | Varies (often $25+) | Day 30 | Varies by state | Repossession (any time in default) |

| Mortgage | 15 days | 4–5% of payment | Day 30 | 120+ days | Foreclosure |

| Payday Loan | None | NSF fee + rollover charges | Day 30 (if sold to collector) | Immediately | Bank account drained by repeated ACH attempts |

| Title Loan | Minimal or none | High rollover fees | Day 30 (if sold to collector) | Days to weeks | Car repossessed within days |

Days 60–90 — Escalation Begins

At 60 days late, lenders get serious. Calls and letters increase. Some lenders will begin internal collections processes. For auto loans and mortgages, pre-repossession or pre-foreclosure notices may begin. For secured loans, the lender is legally preparing to take your asset.

Every additional 30-day late marker that appears on your credit file compounds the damage. At 60 days, many lenders will also trigger a penalty interest rate — your APR on the remaining balance can jump sharply, making the total debt even harder to repay.

Days 120–180 — Default & Charge-Off

This is the formal default threshold. Most lenders declare a loan in default after 3–6 months of missed payments. At or near 180 days, the lender “charges off” the account — meaning they write it off as a loss on their books. A charge-off does not mean the debt disappears. It means the lender has given up collecting directly and is preparing to sell the debt.

Both the original delinquency and the charge-off notation appear on your credit report. For mortgages, foreclosure proceedings typically begin at the 120-day mark under federal law.

Day 180+ — Collections, Lawsuits & Garnishment

Once charged off, the debt is sold to a third-party collection agency — typically for pennies on the dollar. Now you owe the collector, not the original lender. The collector opens a new collection account on your credit report, meaning the same debt now appears twice as separate derogatory marks.

Collection agencies can and do sue borrowers. If they win in court, they can pursue:

- Wage garnishment — your employer withholds part of every paycheck

- Bank account levy — funds withdrawn directly from your account

- Property liens — prevents you from selling assets

- Federal benefit offset (for federal student loans) — tax refunds and Social Security benefits seized

In 2025, millions of student loan borrowers whose protections expired in late 2024 began facing exactly these consequences — negative credit reporting, wage garnishment, and federal benefit offset — for the first time since 2020, according to the National Consumer Law Center.

7 Years — The Long Shadow on Your Credit Report

Under the Fair Credit Reporting Act, a missed payment remains on your credit report for 7 years from the date of the original delinquency — not from when it was charged off or sold. This means every loan application, apartment rental, utility deposit, cell phone plan, and even some job applications will reflect this missed payment for nearly a decade.

The silver lining: your score can begin recovering well before the 7-year removal. Consistent on-time payments on other accounts, reduced debt, and time all work in your favor. The derogatory mark weakens in impact as it ages — it is loudest in years 1–2.

📞 The Word-for-Word Lender Phone Script

Every competitor article tells you to “call your lender.” None of them tell you what to say. Use this script — especially within the first 30 days.

OPENING — Get to the right person fast

“Hi, my name is [your name] and my account number is [number]. I have a payment that is [X] days late and I’m calling today to discuss my options and resolve this. Who is the best person to speak with about a hardship arrangement?”

FEE WAIVER REQUEST — First missed payment

“I’ve been a customer for [X] years and have always paid on time. This is my first missed payment due to [brief reason — job change / medical expense / etc.]. I’m making a payment today. Given my history, I’d like to request a one-time waiver of the late fee. Is that something you can do?”

HARDSHIP REQUEST — If you cannot pay right now

“I am currently experiencing a financial hardship due to [job loss / medical emergency / etc.] and I am not able to make my full payment at this time. I want to keep my account in good standing. Can you tell me what hardship programs, payment deferrals, or restructuring options are available to me before this reaches 30 days?”

⚠ Always ask for the representative’s name and a confirmation number for any arrangement agreed to.

Reader Story · Composite Account

“I missed one payment on my car loan — one — because I switched banks and forgot to update autopay. By the time I noticed, it was day 37. My credit score had already dropped 62 points.”

Marcus, 34, had a 718 credit score and had been making car payments without issue for three years. A banking transition caused a single missed payment. By Day 37, the lender had reported it to all three bureaus. His score dropped from 718 to 656 — moving him from “good” to “fair” credit, which affected an apartment application he had pending.

HIS MISTAKE

Did not verify autopay transferred when switching banks. Waited until he received a collections call before acting.

WHAT HE COULD HAVE DONE

Called the lender on Day 15 when the late fee hit. Explained the banking transition. Requested a one-time credit bureau reporting waiver — many lenders will grant this for first-time issues.

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“The banking-transition missed payment is one of the most common — and most preventable — credit score disasters I see. The lender has no legal obligation to reverse a credit bureau report once made. But many will, as a goodwill gesture, if you catch it before 30 days and have a clean history. The window matters enormously.”

Legal Analysis: Under the Fair Credit Reporting Act, lenders are not required to suppress accurate negative information. However, “goodwill deletion” requests are legally permissible and regularly granted for first-time, isolated late payments. Document every conversation in writing.

Bottom Line: Act before Day 30. After Day 30, your leverage to prevent credit reporting drops significantly.

Reader Story · Public Case Record

“I thought missing one payday loan payment wasn’t a big deal. Within 48 hours, they hit my bank account three times. Three $35 NSF fees before I even knew what was happening.”

Drawn from CFPB consumer complaint records (complaint patterns, 2023–2024). Payday lenders who retain ACH debit authorization can re-attempt withdrawals multiple times after a missed payment. Each failed attempt triggers a bank NSF fee — stacking penalty upon penalty within a single day.

THE TRAP

ACH authorization signed at loan origination allows unlimited re-tries. No grace period. Fees compound immediately.

WHAT YOU CAN DO

Revoke ACH authorization in writing BEFORE missing a payment (see Day 18’s ACH Revocation Kit). You can then negotiate directly without losing your bank account balance.

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“Payday and title loan defaults are categorically different from bank loan defaults. There is no gradual escalation — the consequences are immediate, and they weaponize the access to your bank account you granted at origination.”

Legal Analysis: The Electronic Fund Transfer Act gives consumers the right to revoke ACH authorization at any time. Send a written revocation to your bank AND the lender. Your bank must honor it. A lender who continues to debit after written revocation may be violating federal law.

Bottom Line: If you have a payday or title loan and foresee difficulty paying, revoke ACH authorization before the due date — not after.

Reader Story · Composite Account

“I missed three mortgage payments during a medical leave. I didn’t call my servicer because I was ashamed. By the time I reached out, foreclosure notices were already being prepared.”

Diane, 51, had an established mortgage with 11 years of on-time payments before a cancer diagnosis caused her to miss three months. She avoided calls from her servicer out of shame, not realizing that servicers are required to offer loss-mitigation options before initiating foreclosure. She nearly lost her home before a nonprofit housing counselor helped her access a forbearance program.

HER MISTAKE

Silence. Shame kept her from calling. Every week of silence moved her closer to formal foreclosure proceedings that could have been avoided entirely.

WHAT WAS AVAILABLE TO HER

Mortgage forbearance (pause payments temporarily), loan modification, and HUD-approved housing counseling — all free, all available from Day 1. Federal law requires servicers to offer these options before foreclosure can proceed.

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“Silence is the single most expensive decision a borrower in distress can make. Servicers have programs. Courts have processes. But none of them activate automatically — you have to engage them.”

Legal Analysis: Under federal mortgage servicing rules (Regulation X), servicers are prohibited from beginning foreclosure proceedings until a borrower is more than 120 days delinquent and must make reasonable efforts to contact the borrower about loss mitigation options. Borrowers who engage early have significant legal protections.

Bottom Line: The worst outcome of calling your lender is being told no. The worst outcome of not calling is losing your home. Call.

Frequently Asked Questions

How many days can you be late on a loan payment before it affects your credit?

Most lenders do not report to credit bureaus until a payment is at least 30 days past due. Payments that are 1–29 days late typically do not appear on your credit report — though you may still face late fees and lose your grace period. Once a payment crosses the 30-day threshold, reporting is legal and common.

Source: Consumer Financial Protection Bureau — consumerfinance.gov

How much will one missed payment lower my credit score?

It depends on your starting score and credit history. A single missed payment can drop a score by 50–170+ points. The New York Federal Reserve’s 2025 analysis found that borrowers with scores of 760 or higher lost an average of 171 points after 90 days delinquent, while borrowers with scores below 620 lost around 87 points. Payment history is the single most important factor in your credit score, accounting for 35% of a FICO score.

Source: CFPB — Understanding Credit Scores · consumerfinance.gov

What is the difference between delinquency and default?

Delinquency begins the moment you miss a payment. Default is a formal legal status that typically occurs after 3–6 months of missed payments (90–180 days), as defined in your loan contract. Delinquency is reported to credit bureaus at 30 days. Default triggers more severe consequences — charge-off, collections, and potential legal action.

Can a lender sue me over a missed loan payment?

Yes. Once an account is charged off and sold to a collection agency, the collector can file a civil lawsuit to obtain a court judgment. If they win, the court can authorize wage garnishment, bank account levies, or property liens. For unsecured personal loans, this is the primary collection tool. For secured loans, the lender can also seize the collateral (car or home) in addition to suing for any remaining deficiency balance.

How long does a missed payment stay on your credit report?

Under the Fair Credit Reporting Act, a late or missed payment remains on your credit report for seven years from the date of the original delinquency. This clock begins from when the payment was first missed — not when it was charged off or sold to collections. However, the negative impact on your score weakens over time as the mark ages and as you rebuild positive payment history.

Source: CFPB — consumerfinance.gov

⚠ For educational purposes only. Not legal advice. Consult a licensed attorney or HUD-approved counselor for advice specific to your situation.

💬 Final Thoughts — Laxmi Hegde, MBA in Finance

What strikes me every time I research this topic is how brutally fast the window closes. You have roughly 29 days from a missed payment to prevent any long-term credit damage at all — and most people don’t even know the clock has started. The system is not designed to notify you loudly enough.

What I want you to take from this is not fear — it’s a protocol. The day you think you might miss a payment, pick up the phone. Most lenders will work with you. The ones who won’t are the predatory ones we’ve been profiling all of Week 2. And for those loans, the protocol is different: revoke the ACH access first, then negotiate.

Tomorrow in Day 20, we look at how lenders use loan renewal offers to trap you in a cycle that resets your debt and extends their profit — just when you think you’re almost free.

Research Note & Primary Sources

This article is part of the Borrower’s Truth Series, a 30-day research and education project by Laxmi Hegde, MBA. All statistics cited are drawn from government agencies and primary research institutions. Timeline stages represent general patterns; individual loan contracts and state laws govern specific outcomes.

Primary Sources:

- Consumer Financial Protection Bureau — consumerfinance.gov

- Federal Trade Commission — Debt Collection FAQs — ftc.gov

- Federal Student Aid — Default Information — studentaid.gov

- New York Federal Reserve Bank — 2025 Credit Analysis Report

- National Consumer Law Center — Consumer Law Rights 2025 — library.nclc.org

- Fair Credit Reporting Act (15 U.S.C. § 1681) — 7-year reporting rule

- Regulation X — Federal Mortgage Servicing Rules (12 CFR Part 1024)

For the complete Borrower’s Truth Series guide, visit: The Complete Borrower’s Truth Guide

← Previous · Day 18

Auto-Pay Loan Traps

Next · Day 20 →

Loan Renewal Offers — The Trap That Resets Your Debt

Publishing soon

Quick Access — All 30 Days

Week 1 — Borrowing Basics

Week 2 — The Predatory Lenders

Week 3 — The Fine Print Files

Weeks 4 & 5 — After You Borrow · The Smart Borrower

Research & Publication Note

This article is Day 19 of the Borrower’s Truth Series — a 30-day educational series on consumer borrowing by Laxmi Hegde, MBA in Finance. All research draws from U.S. government agencies, federal consumer protection data, and primary financial research institutions. This content is for educational purposes only and does not constitute legal, financial, or credit counseling advice.

Read the full 30-day guide: The Complete Borrower’s Truth Guide → ConfidenceBuildings.com

Menu

Social Menu

- First blog post

- First blog post

- @laxmihegde61twitter.com

- First blog post

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.