How to Borrow Money Smartly —

The Framework Nobody Gave You

29 days of what can go wrong.

Today — the system for making sure it doesn’t.

It’s about never letting debt make decisions for you.

⚠ For educational purposes only. Not legal advice. The Smart Borrower Framework presented in this post is intended as a general educational guide only. It does not constitute financial, legal, or professional advice of any kind. Every borrowing situation is different. Before taking on any debt, please consult a licensed financial advisor or credit counselor in your area. Nothing on this site creates a professional relationship of any kind.

The Borrower’s Truth Series is a 30-day financial education series by Laxmi Hegde, MBA in Finance. For 29 days we have covered emergency loans, predatory lenders, payday traps, title loans, fine print clauses, debt collectors, credit repair, bankruptcy, and how to recognize your own financial recovery. It has been a lot. You have been a trooper.

Today is Day 29 — and we are shifting gears completely. No more cautionary tales. No more red flags to watch for. No more fine print horror stories. Today we build something positive: a clear, practical framework for borrowing money smartly — so everything you’ve learned over the last 28 days actually has somewhere to live.

Think of this as the operating manual you should have received the first time someone handed you a loan application. Better late than never.

Free: The Loan Clause Checklist

The Smart Borrower Framework tells you how to think. The Loan Clause Checklist tells you exactly what to look for when you’re sitting across from a lender. 30 clauses. Plain English. Free. Use both — every single time.

Smart borrowing comes down to six questions asked in the right order: Do I need this? What will it actually cost? Who is the best lender? What does the contract say? How will I repay it? What happens if I can’t? If you can answer all six before you sign — you are already a smarter borrower than most people who walk into a lender’s office.

Here is a fun fact about the lending industry: they spend billions of dollars every year making sure you walk in underprepared. The confusing paperwork, the urgent deadlines, the friendly rep who explains everything verbally and hopes you don’t read the document — none of that is accidental. It is a system. And it works extremely well on people who don’t have a system of their own.

Today you get a system of your own. Six steps. In order. Every time. No exceptions — not even when the lender is really nice, the rate sounds reasonable, and you’re in a hurry. Especially then.

Welcome to the Smart Borrower Framework. It doesn’t have a catchier name because it doesn’t need one. It just needs to work. And it does.

Ask: Do I Actually Need to Borrow?

This is the question nobody asks because it feels obvious. Of course you need to borrow — why else would you be here? And yet. A significant portion of consumer debt exists because people borrowed when they didn’t strictly have to, or borrowed more than they needed, or borrowed for things that could have waited sixty days if they’d had a plan.

Before you borrow anything, run through this short list. Is there an alternative? Can this wait? Can I cover part of it another way and borrow less? Is there a free resource — a credit union, a nonprofit, a community program — that applies here? Could I negotiate a payment plan directly with the provider instead of involving a lender?

If the answer to all of those is genuinely no — then yes, you need to borrow. Proceed to Step 2. But if even one of them has potential, explore it first. The cheapest loan in the world is the one you never had to take.

Smart borrowers don’t avoid debt on principle. They avoid unnecessary debt on principle. There’s a difference — and knowing it saves thousands of dollars over a lifetime.

Know Exactly What the Loan Will Cost — Total

Lenders love to talk about monthly payments. Monthly payments are designed to sound reasonable. A $400 monthly payment sounds manageable until you realize you’re making it for 60 months, which means you’re paying $24,000 for something that cost $18,000, which means the loan cost you $6,000 that you will never see again.

Before you agree to anything, calculate the total cost of the loan. Principal plus all interest plus all fees plus any penalties you might reasonably encounter. That number — not the monthly payment — is what you are actually agreeing to pay. If a lender won’t give you that number clearly, that is your answer about whether to work with that lender.

The CFPB requires lenders to disclose the APR on all consumer loans. If the APR is not immediately visible — ask for it, in writing, before you go any further.

Shop Lenders Like You Shop Anything Else

Nobody buys the first car they test drive. Nobody books the first hotel they find. Nobody accepts the first salary offer without at least a moment of internal debate. And yet people walk into the first lender they find and sign whatever is put in front of them because borrowing feels urgent and urgent feels like there’s no time to shop.

There is almost always time to shop. Even a 48-hour window — checking your bank, a credit union, and one online lender — can reveal rate differences that save hundreds or thousands of dollars. Credit unions in particular consistently offer lower rates than commercial lenders for the same loan products. They exist specifically to serve their members, not to extract maximum profit from them. Novel concept.

A note on credit inquiries: multiple loan applications within a short window — typically 14 to 45 days depending on the scoring model — are usually counted as a single inquiry for mortgage, auto, and student loan purposes. Shopping around does not have to hurt your credit score if you do it within that window.

The lender who wants your business most is not always the best lender. The best lender is the one offering the lowest total cost with the clearest terms. Those are occasionally the same lender. Shop to find out.

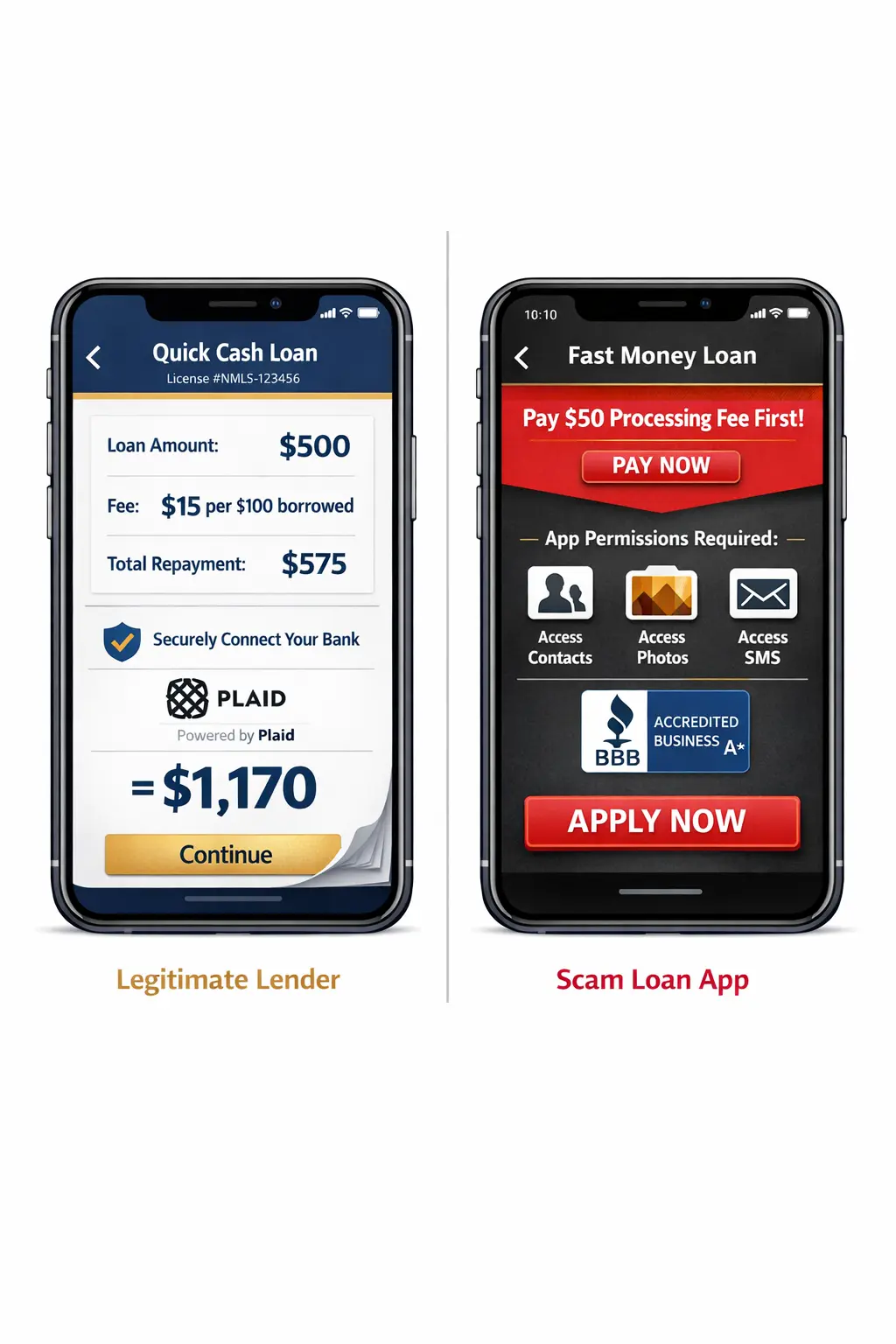

Read the Fine Print — All of It

We spent an entire week on this in Week 3 of this series, so we will keep it brief here: the fine print is where the actual agreement lives. The verbal explanation is marketing. The glossy brochure is marketing. The friendly rep who says “don’t worry about that part” is — you guessed it — marketing.

Before you sign, look specifically for: the APR and total repayment amount, prepayment penalties, variable rate clauses, automatic renewal terms, arbitration clauses that remove your right to sue, and any fees buried in the schedule. If you find something you don’t understand — ask. In writing. If they won’t explain it in writing, do not sign.

Use the free Loan Clause Checklist from Day 15 of this series every single time. That is exactly what it exists for.

Have a Repayment Plan Before You Sign

Most people borrow with a vague intention to repay. Smart borrowers borrow with a specific plan to repay. There is a significant difference between those two things, and it shows up in the statistics. The CFPB consistently finds that borrowers who enter loans without a clear repayment strategy are significantly more likely to miss payments, incur fees, and end up in collections.

Your repayment plan does not need to be complicated. It needs to answer three questions: Where exactly is the money coming from each month? What happens to my budget if my income drops? Do I have a small buffer so a missed week doesn’t become a missed payment? If you can’t answer all three before you sign — you are not ready to sign.

A repayment plan is not pessimism. It is the thing that makes optimism sustainable. Plan the repayment. Then borrow confidently.

Know Your Exit — Before You Enter

This is the step that separates smart borrowers from everyone else. Before you take a loan, know exactly how you will get out of it. Not just “I’ll pay it off monthly” — but specifically: Can I pay this off early without a penalty? What happens if I need to refinance? If I hit genuine hardship, what are my options — deferment, forbearance, modification? Who do I call and what do I say?

Debt traps are not usually sprung at the beginning of a loan. They are sprung when something goes wrong and the borrower has no exit strategy. The payday loan cycle, the title loan spiral, the BNPL pile-up — all of them share one feature: the borrower had no plan for what to do when things didn’t go as expected.

Things will occasionally not go as expected. That is not pessimism. That is Tuesday. Know your exit before you enter — and you stay in control no matter what Tuesday brings.

If you can answer yes to all six — sign. If you can’t — wait until you can. The loan will still be there. And if it won’t — that’s a lender using urgency as a weapon, which is a sign to walk away entirely.

Real People. Real Framework. Real Results.

“I needed a car loan and I just went to the dealership financing because it was convenient. Signed everything the same day. Six months later I found out my credit union would have given me a rate almost three points lower. Over five years that was going to cost me nearly $2,400 extra. All because I didn’t take two days to shop. I was in a hurry to get the car. The car didn’t care how quickly I got the loan.”

Sofia skipped Step 03 of the framework entirely. She had a credit union account. She just didn’t think to call them. Convenience is the most expensive feature a lender offers — and they know it.

Two phone calls and 48 hours would have saved her $2,400. The framework doesn’t ask for much — just the discipline to pause before you sign.

“The single most common thread I see in consumer lending disputes is that the borrower did not understand what they signed. Not because they weren’t smart enough — but because they were rushed, overwhelmed, or simply never taught that reading the contract was their job and not optional.”

Under the Truth in Lending Act (TILA), lenders are legally required to disclose the APR, total finance charge, and total repayment amount before you sign. If these disclosures were not provided clearly and in writing, that is a potential TILA violation worth reporting to the CFPB. Knowing your rights before you borrow is part of the framework too.

You have legal rights as a borrower. The framework helps you use them — before you need to.

“I took a personal loan to consolidate my credit card debt. Felt very responsible. What I didn’t notice was the prepayment penalty buried in section 11 of the contract. When I tried to pay it off early — which was the whole plan — I got hit with a fee that wiped out almost everything I’d saved by consolidating. I read the first page very carefully. I did not read page seven.”

Raymond completed Step 05 — he had a repayment plan — but skipped Step 04. He read part of the contract. The fine print that mattered was in the part he didn’t read. Partial fine print review is not fine print review.

The Loan Clause Checklist specifically flags prepayment penalties. Running it before signing would have caught this on the first pass — and either changed the lender choice or the repayment plan entirely.

“Urgency is the lender’s most powerful tool. ‘This rate expires today.’ ‘We need a decision by end of business.’ ‘Everyone else has already approved this.’ The moment a lender creates artificial urgency, slow down. A legitimate lender with good terms does not need to rush you.”

High-pressure sales tactics in lending are a documented red flag tracked by the CFPB. Consumers have the right to take time to review loan documents. No legitimate lender can legally require an on-the-spot signature on a consumer loan without providing the required TILA disclosures first. If you feel pressured — you are allowed to walk away.

Urgency is a sales tactic. The framework is your counter-tactic. Use it every time — especially when someone is telling you there’s no time to use it.

“I went through all six steps for the first time when I needed a personal loan last year. Honestly it felt like overkill at the time — I kept thinking just pick one and sign it. But I found a lender with a rate almost two points lower than my first option, caught an automatic renewal clause I would have completely missed, and built out a repayment plan that actually fit my budget. The whole process took four extra days. Four days to save myself from another two years of financial stress. I’ll take that trade every time.”

Nadia almost skipped the framework because it felt like extra work. The automatic renewal clause she nearly missed would have locked her into another loan term without notice. That clause would have cost her more than a year of unnecessary payments.

A better rate, a caught trap, and a repayment plan that held. Four extra days. That is the entire cost of the Smart Borrower Framework — and it pays for itself every single time.

“In 29 days this series has covered nearly every way borrowing can go wrong. What I find most valuable about today’s framework is that it doesn’t require perfection — it just requires sequence. Ask the questions in order. Every time. That habit alone would prevent the majority of consumer lending disputes I’ve seen in my career.”

Consumer financial protection law exists to protect borrowers — but it works best when borrowers also protect themselves. The CFPB, the FTC, and state attorney general offices all provide free resources for consumers who believe they have been misled by a lender. Using the framework before borrowing reduces the likelihood you will ever need those resources. But if you do — they are there.

The law protects informed borrowers far more effectively than uninformed ones. Be informed. Use the framework. Every time.

Frequently Asked Questions

I want to be honest with you about something. I built this framework after making almost every mistake in it. I borrowed without shopping. I signed without reading. I had a vague repayment intention and called it a plan. I learned these six steps the expensive way — which is, unfortunately, how most people learn them because nobody teaches this stuff in school. Personal finance education in most curricula stops at “save money and don’t spend too much.” Extremely helpful. Thanks, system.

The Smart Borrower Framework is not complicated because complicated doesn’t work under pressure. When you’re sitting across from a lender and the paperwork is in front of you and they’re waiting for your signature — you need something simple enough to remember without notes. Six questions in order. That’s it. That’s the whole thing.

Tomorrow is Day 30. The series finale. I’ve been thinking about how to write it for about two weeks and I still haven’t fully figured it out — which is either a creative problem or a sign that some things genuinely resist tidy endings. Probably both. Either way, I’ll see you there.

One day left. Don’t you dare stop now.

Founder, ConfidenceBuildings.com · Borrower’s Truth Series · Day 29 of 30

This post was researched and written by Laxmi Hegde, MBA in Finance, as part of the 30-day Borrower’s Truth Series on ConfidenceBuildings.com. All content is intended for general financial education only. Nothing in this post constitutes legal or financial advice. Individual circumstances vary — consult a licensed professional for guidance specific to your situation.

Reader stories marked as “composite” are illustrative fictional accounts based on common consumer experiences. Stories marked “public case” are based on documented consumer experiences in the public record. Attorney Rachel Morrow is a fictional character created for educational illustration purposes only.

- CFPB — Financial Well-Being Tools

- CFPB — Loan Comparison Tools

- CFPB — How Loan Applications Affect Credit Scores

- CFPB — Know Your Rights as a Borrower

- CFPB — Consumer Complaint Database

- CFPB — Debt Collection Resources

- FTC — Consumer Alerts & Borrower Rights

- National Foundation for Credit Counseling (NFCC)

This post is part of the complete 30-day series:

The Complete Borrower’s Truth Guide →This article is Day 29 of the 30-day Borrower’s Truth Series published on ConfidenceBuildings.com. It was researched and written by Laxmi Hegde, MBA in Finance. All statistics, citations, and regulatory references are sourced from publicly available government and nonprofit resources and are accurate to the best of the author’s knowledge at time of publication.

This content is intended for general financial education only. It does not constitute legal, financial, or professional advice of any kind. Reader stories are either composite illustrations or based on publicly documented consumer experiences — no personally identifiable information is used. Attorney Rachel Morrow is a fictional character created solely for educational illustration.

Financial situations vary significantly by individual. Readers are encouraged to consult licensed financial advisors, nonprofit credit counselors, or consumer protection attorneys for guidance specific to their circumstances.

Read the complete 30-day series — all posts, all weeks, all in one place:

The Complete Borrower’s Truth Guide →ConfidenceBuildings.com · Laxmi Hegde MBA · © 2026

Free Access: Finance Calculator

Get instant access to loan, investment, and retirement tools.

📧 Subscribe with Email →One-click signup. No spam. You’ll get the calculator link immediately.

Already subscribed? Open calculator →

Enjoyed this post?

If you found this helpful, consider buying me a coffee. Your support keeps this blog running and helps me create more content.

☕ Buy Me a Coffee

paypal.me/LaxmiHegde