⚖️ LEGAL DISCLAIMER

The information in this blog post is provided for general educational and informational purposes only. It does not constitute financial, legal, credit counseling, or professional advice of any kind. Credit scoring models, lender practices, and consumer protection laws vary by institution, loan type, and jurisdiction — and change frequently.

All legal rights mentioned in this post are based on U.S. federal law as of the date of publication. Laws in other countries differ significantly. Always verify your specific rights with a qualified financial or legal professional, or through official government sources such as the CFPB (consumerfinance.gov) or FTC (ftc.gov).

The publisher, authors, and affiliated parties accept no liability for any financial or legal outcomes resulting from the use of or reliance upon any information presented in this post. Any third-party organizations, scoring models, or institutions mentioned are referenced for informational purposes only and do not constitute an endorsement.

🔗 Part of the “Borrower’s Truth” Series — Day 4 In Day 3 we covered 7 real alternatives to emergency loans that most people never try. Read it here: Broke & Stressed? 7 Real Alternatives to Emergency Loans That Most People Overlook Today we go deeper — into the system lenders built around your three-digit number, and exactly how they use it when you’re most vulnerable.

Read the complete guide here: The Complete Borrower’s Truth Guide →

Table of Contents

- The Number They Built a Business Model Around

- What Your Credit Score Actually Is — And What It Isn’t

- The Lender Playbook: Risk-Based Pricing Exposed

- The Real Dollar Cost of a Lower Score — Nobody Does This Math

- The Surveillance You Don’t Know About: How Lenders Watch You in Real Time

- The Timing Trap: Why Lenders Strike When You’re Most Vulnerable

- The Legal Notice You’re Entitled To (But Never Told About)

- The 2026 Scoring Model Changes Affecting You Right Now

- Credit Score Myths That Cost Borrowers Real Money

- How to Fight Back: The Borrower’s Tactical Guide

- Your Credit Score Action Plan — 30, 60, 90 Days

- Final Thoughts: Know the Game Before You Play It

1. The Number They Built a Business Model Around {#introduction}

Somewhere in a data center right now, a number between 300 and 850 is quietly determining how much you’ll pay for your next loan. It’s deciding whether your application gets approved in seconds or declined without explanation. It’s being used — in ways most people have never heard of — to figure out exactly how much it’s safe to charge you before you walk away.

That number is your credit score. And you’ve been told a very partial version of how it works.

The version most people know: pay your bills on time, keep your balances low, don’t apply for too much credit at once, watch the number go up. Good number = good rates. Bad number = bad rates. Simple.

The version nobody tells you: lenders don’t just use your score to decide whether to lend to you. They use it to engineer exactly how much profit to extract from you. They time their offers for when you’re most financially stressed. They monitor your behavior in real time through AI systems that flag you as “at risk” weeks before you even miss a payment. And there’s a legal notice you’re entitled to receive when they’ve priced you worse than other borrowers — a notice most people have never heard of, let alone received.

By the end of this post, you’ll understand the full playbook. Not the sanitized version. The actual one.

2. What Your Credit Score Actually Is — And What It Isn’t {#what-it-is}

Let’s be precise about this, because the distinction matters.

Your credit score is a prediction — specifically, a statistical prediction of the probability that you’ll default on a debt in the next 24 months. That’s it. It’s not a measure of your character, your financial intelligence, or your worth as a person. It’s a risk probability estimate built by a mathematical model trained on the historical behavior of millions of borrowers.

The most widely used model is FICO — created by the Fair Isaac Corporation. The score runs from 300 to 850. Most lenders also use VantageScore, created jointly by the three major credit bureaus: Equifax, Experian, and TransUnion.

What actually goes into your FICO score:

| Factor | Weight | What It Really Means |

|---|---|---|

| Payment History | 35% | Have you paid on time? One 30-day late payment can drop your score 60–110 points |

| Credit Utilization | 30% | How much of your available credit are you using? Above 30% starts hurting you |

| Length of Credit History | 15% | How long have your accounts been open? Closing old cards can hurt you here |

| Credit Mix | 10% | Do you have different types of credit? Cards + loans = better than just cards |

| New Credit Inquiries | 10% | How many times has your credit been pulled recently? Too many = risk signal |

What your score doesn’t measure: Your income. Your savings. Your job stability. Your actual ability to repay. Your character. The reason you had a rough patch three years ago.

A model built on historical data cannot capture your present reality — and lenders know this. They use it anyway, because it’s the most convenient, scalable way to price millions of loan applications. Convenient for them. Not always fair to you.

3. The Lender Playbook: Risk-Based Pricing Exposed {#risk-based-pricing}

Here’s the part your competitors don’t explain — the actual mechanism behind how your score becomes their profit.

It’s called risk-based pricing — and it’s the practice of offering different interest rates and loan terms to different borrowers based on their perceived credit risk. Risk-based pricing is when a lender offers you less favorable loan terms, such as a higher interest rate, based on information in your credit report or application.

On the surface, that sounds almost reasonable. Higher risk = higher rate. Makes sense, right?

Here’s what the textbook version doesn’t tell you: the relationship between your score and your rate is not linear. It’s tiered — and the tiers are engineered to maximize revenue.

Most lenders divide borrowers into pricing tiers — sometimes as few as four, sometimes dozens. Every borrower who doesn’t land in the top tier pays more. And the gap between tiers is not small.

Lenders often charge higher interest rates to people they consider higher-risk borrowers — including those who have recently declared bankruptcy, lost a job, or are several payments behind. But the more important point is what happens within the range of people who are approved — people with scores from 580 to 780 who are all considered creditworthy, just to varying degrees.

That spread — from “barely approved” to “best terms available” — is where the pricing power lives. And lenders exploit every point of it.

💡 A real example that will make you uncomfortable: Two people walk into the same bank on the same day. Same loan amount. Same purpose. Same income. One has a 740 score. One has a 640 score. The 740 gets 6% APR. The 640 gets 8.5% APR. Over a 5-year $20,000 loan, the 640 borrower pays $1,430 more — for the exact same money. That’s not a fee. That’s not a penalty. That’s just the price of having a lower number.

4. The Real Dollar Cost of a Lower Score — Nobody Does This Math {#real-dollar-cost}

This is the section that doesn’t exist anywhere else on the internet in this form. Every competitor gives you a vague “lower score = higher rate.” None of them show you the actual lifetime dollar cost across every major loan type simultaneously.

Here it is:

| Loan Type | Score 760+ | Score 640 | Score 580 | Extra Cost of Lower Score (640 vs 760+) |

|---|---|---|---|---|

| Personal Loan ($10,000 / 3yr) | ~8% APR | ~20% APR | ~28% APR | $2,100+ extra over 3 years |

| Auto Loan ($25,000 / 5yr) | ~5% APR | ~10% APR | ~15% APR | $3,500+ extra over 5 years |

| Mortgage ($300,000 / 30yr) | ~6% APR | ~7.5% APR | ~8.5% APR | $100,000+ extra over 30 years |

| Credit Card ($5,000 balance) | ~16% APR | ~24% APR | ~29% APR | $400+ extra per year in interest |

| Emergency Loan ($2,000 / 1yr) | ~12% APR | ~29% APR | ~36% APR | $340+ extra over 12 months |

⚠️ Disclaimer: The rates above are illustrative estimates based on general market ranges as of early 2026. Actual rates vary significantly by lender, loan product, income, debt-to-income ratio, and other factors. Always get personalized quotes from multiple lenders before making any borrowing decision.

The uncomfortable takeaway: A person who goes through one rough financial patch — a job loss, a medical crisis, a divorce — and lets their score slip from 760 to 640, will spend tens of thousands of dollars more over their lifetime than if that score had never dropped. The system has no memory of your recovery. It just prices the number it sees today.

That’s not a bug. For lenders, it’s a feature.

5. The Surveillance You Don’t Know About: How Lenders Watch You in Real Time {#surveillance}

This is the section that exists nowhere in consumer-facing personal finance content. Nowhere. I checked.

Here’s what’s actually happening behind the scenes of your financial life right now:

Lenders are not waiting for you to apply for a loan to start profiling you.

Banks are investing in advanced analytics platforms that track repayment trends, assess credit risk, and surface early warning signs of default — flagging high-risk accounts based on income volatility, transaction patterns, or external risk indicators.

If you have existing accounts — a credit card, a mortgage, an auto loan — your lender is running AI models on your behavior right now. Not monthly. Not weekly. Continuously.

Advanced systems now monitor every account around the clock — scanning transaction patterns, payment schedules, and even external data — to raise a hand at the first hint of trouble. Rising credit utilization, multiple loan applications in a short period, and even communication changes like borrowers who stop answering calls can trigger automated alerts.

What triggers their early warning systems:

- Your credit card utilization suddenly jumps (you’re charging more than usual)

- You apply for credit at two or three places in a short period

- Your checking account balance drops significantly

- You start making minimum payments when you used to pay in full

- You miss a bill by even a few days

High utilization and “emergency” borrowing often surface 2–3 months before a default — which means by the time you’re Googling “emergency loan,” lenders already have an AI flag on your account marking you as elevated risk.

What happens when the flag goes up?

For existing accounts — your credit card company may quietly lower your credit limit (which increases your utilization percentage, which lowers your score, which justifies worse terms). Your interest rate may increase at the next review cycle. Pre-approved offers you were about to receive get quietly pulled.

For new loan applications — your application goes into a “higher risk” pricing tier that you never see. You just see the rate you’re offered. You don’t see the tier you were placed in, or the algorithm that put you there.

💙 This isn’t paranoia. This is documented standard practice in the lending industry in 2026. The difference between knowing this and not knowing it is whether you can prepare before the flag goes up — or react after it already has.

6. The Timing Trap: Why Lenders Strike When You’re Most Vulnerable {#timing-trap}

This is where the surveillance becomes a strategy.

Think about the timing of loan offers you receive. Have you ever noticed that a pre-approved loan offer seems to arrive right when you’ve been stressed about money? That’s not coincidence. That’s targeting.

Predatory lenders target those in financial distress — not to help, but to exploit. Their business model involves deception, offering loans with exorbitant interest rates, hidden fees, and terms designed to trap borrowers in a cycle of debt.

Here’s how the timing works in practice:

Your credit card utilization spikes. The AI flags it. Within days — sometimes hours — you start seeing loan advertisements on your social media, your email, your search results. The offer looks helpful. “You’re pre-approved for up to $5,000.” It feels like relief.

What’s actually happening: you’ve been identified as someone likely to borrow, likely to accept unfavorable terms, and likely to stay in the loan long enough to generate significant interest revenue. The offer didn’t arrive because they want to help you. It arrived because the data said you were ready to say yes.

Predatory lenders often promise fast cash with guaranteed approval, while rushing borrowers to accept money without reviewing the shady loan terms — some even finding ways to disguise interest rates as high as 400%.

The urgency language is engineered:

- “Offer expires in 24 hours” — creates panic, prevents comparison shopping

- “Your application was pre-selected” — creates false sense of relationship and trust

- “No impact to your credit to check your rate” — true, but designed to get you in the funnel

- “Funds as soon as today” — targets the exact moment of peak financial stress

When you understand the timing trap, you can see the offer for what it is — not a lifeline, but a revenue opportunity wearing the costume of one.

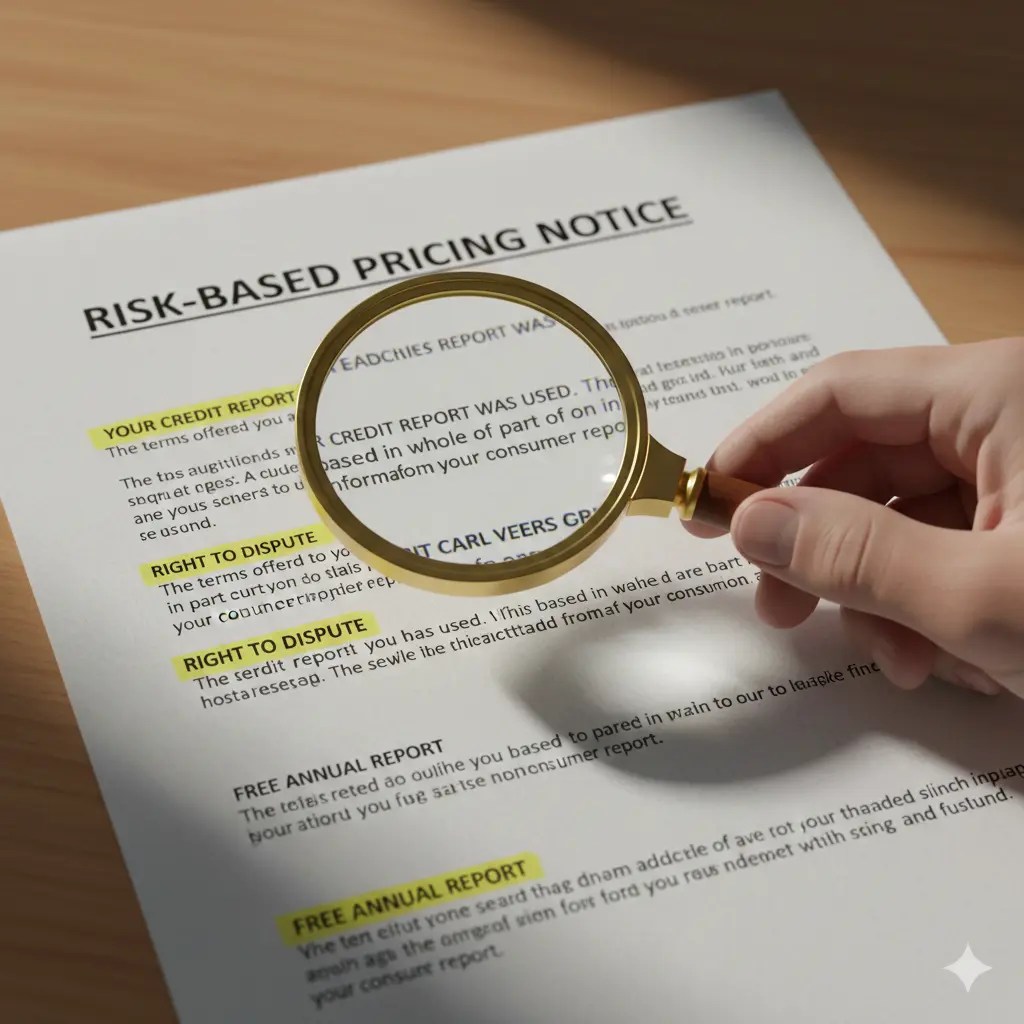

7. The Legal Notice You’re Entitled To (But Never Told About) {#legal-notice}

Here is the section that has almost zero coverage in consumer personal finance content anywhere on the internet — and it represents a genuine legal right that most borrowers never know they have.

It’s called the Risk-Based Pricing Notice.

If a lender relied on a credit report to make a less-favorable lending decision about you, you should get a risk-based pricing notice. This notice tells you that you’re receiving less favorable terms than other borrowers because of negative information on your credit report.

Under the Fair Credit Reporting Act (FCRA) and enforced by both the FTC and CFPB, risk-based pricing occurs when lenders offer different interest rates and loan terms to borrowers based on individual creditworthiness — and the Risk-Based Pricing Rule requires lenders to notify consumers if they are getting worse terms because of information in their credit report

What this notice must legally contain:

The notice must include: a statement that the consumer’s credit score was used to set the terms of credit offered; the credit score used in the lending decision; the range of possible credit scores under the model used; all key factors that adversely affected the credit score (no more than four); the date on which the credit score was created; and the name of the consumer reporting agency that provided the score.

Why this matters for you:

If you receive a loan offer and the terms seem worse than you expected — higher APR, shorter term, more fees — you may be entitled to this notice. And if you receive it, you have the right to:

- Get a free copy of your credit report from the bureau named in the notice within 60 days

- Dispute any inaccurate information on that report

- Potentially request reconsideration if the rate was based on incorrect data

The catch: Many lenders comply with this rule by sending a generic “credit score disclosure exception notice” to all borrowers — which technically satisfies the regulation but buries the information in paperwork most people never read. Now you know to look for it.

💡 What to do when you get a loan offer: Before accepting any terms, ask the lender directly: “Was my interest rate affected by my credit report? Am I entitled to a risk-based pricing notice?” The question alone signals that you know your rights — and sometimes that’s enough to get better terms on the spot.

8. The 2026 Scoring Model Changes Affecting You Right Now {#scoring-changes}

Here’s something your competitors definitely haven’t covered — because it’s happening right now and most content hasn’t caught up yet.

The credit scoring landscape is actively shifting in 2026, and if you’re an emergency fund seeker or someone rebuilding credit, these changes could work in your favor — if you know about them.

FICO 10T — The New Standard:

FICO 10T (the “T” stands for “trended data”) looks beyond a single snapshot of your credit file. It analyzes your credit behavior over the past 24 months — not just where you are today, but the direction you’re moving.

What this means in practice:

- If your balance has been decreasing over 24 months, FICO 10T rewards you even if the balance is still high

- If your balance has been increasing even slowly, it penalizes you even if the current number looks okay

- A borrower who paid off $3,000 in debt over two years scores better than a borrower who maintained the same low balance without movement

For someone rebuilding after a financial emergency, this is actually good news — consistent improvement is now rewarded in real time, not just when you cross a threshold

VantageScore 4.0 — Rent and Utilities Now Count:

VantageScore 4.0, increasingly adopted by lenders for non-mortgage lending decisions, now incorporates rent payment history, utility payments, and telecom bills — when that data is available through services like Experian RentBureau or similar reporting platforms.

What this means: If you’ve been paying rent on time for three years but have minimal traditional credit history, you now have a path to a meaningful credit score that didn’t exist before. This is significant for younger borrowers, recent immigrants, and people who have avoided credit products — the “credit invisible” population.

Action steps for 2026:

- Ask your landlord to report your rent payments through a rent-reporting service (Rental Kharma, RentTrack, or similar)

- Sign up for Experian Boost, which adds utility and phone bill payment history to your Experian credit file for free

- If you’re consistently improving your balances month over month, that trajectory is now scoring data — keep going

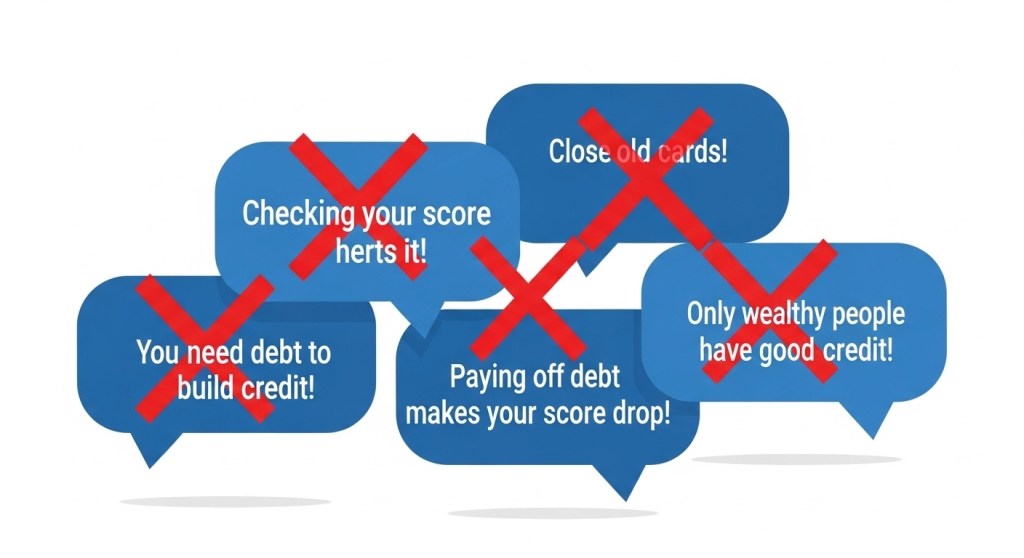

9. Credit Score Myths That Cost Borrowers Real Money {#myths}

These aren’t just misconceptions. Each one has a real financial cost attached to it.

Myth 1: Checking your own credit hurts your score. False. Checking your own credit is a soft inquiry and has zero impact on your score. You can check it daily if you want. The myth persists because people confuse self-checks with lender checks — which are hard inquiries and do impact your score. Check your own credit at AnnualCreditReport.com for free.

Myth 2: Closing old credit cards improves your score. Almost always the opposite is true. Closing an old card reduces your total available credit, which increases your utilization ratio, which hurts your score. It also shortens your average account age. Leave old accounts open — even if you don’t use them.

Myth 3: Carrying a small balance on your credit card builds credit. This one costs people money directly. Carrying a balance costs you interest. It does not help your score. Paying in full every month is better for both your score (lower utilization) and your wallet (no interest charges).

Myth 4: Income affects your credit score. Income is not a factor in any major credit scoring model. A doctor earning $300,000 with maxed-out cards and late payments will score lower than a teacher earning $45,000 who pays on time and keeps balances low. Lenders ask about income separately — but it doesn’t move your score.

Myth 5: Once bad information is on your report, you’re stuck with it forever. Not true. Negative information has a time limit. Late payments stay for 7 years. Bankruptcies stay for 7–10 years. Collection accounts stay for 7 years. After that, they fall off completely. And their impact on your score diminishes significantly well before the 7-year mark — often within 2–3 years of the negative event, especially if you’ve been positive since.

10. How to Fight Back: The Borrower’s Tactical Guide {#fight-back}

Knowing how the system works is half the battle. Here’s the other half — what to actually do about it.

Before you apply for any loan:

Step 1: Pull your own credit report first. Go to AnnualCreditReport.com — the only federally mandated free credit report site. Get all three reports (Equifax, Experian, TransUnion). They can and do differ — sometimes significantly. Look for errors, outdated negative items, and accounts you don’t recognize.

Step 2: Dispute errors before applying. If you find inaccurate information, dispute it directly with the credit bureau that’s reporting it. Under the FCRA, bureaus must investigate disputes within 30 days. Removing even one inaccurate late payment can move your score 20–40 points — which can move you into a better pricing tier and save you hundreds or thousands of dollars.

Step 3: Know your score range before a lender sees it. Most lenders use tiered pricing with specific cutoffs — often at 580, 620, 640, 660, 700, 720, 740, and 760. Knowing where you land tells you whether you’re close to a tier upgrade — and whether it’s worth waiting 30–60 days to improve before applying.

Step 4: Shop within a 14–45 day window. Multiple hard inquiries for the same type of loan within 14–45 days are treated as a single inquiry by most scoring models. Apply to multiple lenders within this window to compare rates without multiplying the score impact.

Step 5: Ask for your Risk-Based Pricing Notice. If you’re offered terms that seem worse than expected, ask the lender directly whether your rate was influenced by your credit report and whether you’re entitled to a risk-based pricing notice. Then use that notice to get your free credit report and check for errors.

If your score is already lower than you’d like:

The fastest legitimate ways to move your score upward:

- Pay down credit card balances below 30% utilization (the biggest single lever)

- Sign up for Experian Boost to add utility payment history

- Ask your landlord to report rent payments

- Become an authorized user on a family member’s old, well-maintained credit card (their history becomes yours)

- Set every account to autopay minimums — never miss a payment again even during a rough month

Your Credit Score Action Plan — 30, 60, 90 Days {#action-plan}

| Timeline | Action Steps |

|---|---|

| This Week | Pull all 3 credit reports free at AnnualCreditReport.com. Check for errors. Note your score range. |

| 30 Days | Dispute any inaccurate negative items. Sign up for Experian Boost. Set all accounts to autopay minimums. Pay down highest-utilization card first. |

| 60 Days | Check if disputes were resolved. Recalculate utilization across all cards. Ask landlord about rent reporting. Check if you’ve crossed a scoring tier threshold. |

| 90 Days | Pull score again and compare. If improved, this is the right window to apply for any needed credit. Shop multiple lenders within a 14-day window. Request risk-based pricing notice if rate offered seems high. |

| Ongoing | Monitor your credit monthly with free tools (Credit Karma, Experian free tier). Never close old cards. Keep utilization below 30%. Celebrate every tier upgrade — each one saves you real money on every future loan. |

12. Final Thoughts: Know the Game Before You Play It {#final-thoughts}

Your credit score was built by institutions, for institutions. The model exists because it makes lending decisions fast and scalable — not because it’s a perfect measure of your financial character or your ability to repay.

Lenders use it to price loans. AI systems use it to flag vulnerability. Marketing platforms use the signals around it to time offers for when you’re most likely to say yes. The system is sophisticated, it runs continuously, and until today, most borrowers had no idea how much of it was pointed directly at them.

Now you do.

Knowing the risk-based pricing playbook means you can negotiate. Knowing about the Risk-Based Pricing Notice means you can dispute. Knowing about the scoring model changes means you can use them. Knowing how the AI surveillance works means you can prepare before the flag goes up — not react after it already has.

Your score is not your destiny. It’s a number in a model that was built on averages — and you are not an average. You’re a person with a specific situation, specific history, and a very specific ability to fight back when you understand the rules.

Now you understand the rules.

🔗 Coming up — Day 5 of the Borrower’s Truth Series: “Secured vs. Unsecured Loans: Which One Could Cost You Your Car?” Because the type of loan matters just as much as the rate — and the wrong choice could cost you something you can’t afford to lose.

💬 Did anything in this post surprise you? The surveillance section gets people every time. Share this with someone who’s about to apply for a loan — they deserve to know what’s actually happening on the other side of that application.