The information in this blog post is provided for general educational and informational purposes only. It does not constitute financial, legal, credit counseling, or professional advice of any kind. Loan terms, clauses, and their legal implications vary significantly by lender, loan type, state, and individual circumstances — and change frequently.

All information is based on general U.S. law and market conditions as of February 2026. Always verify the specific terms of any loan agreement with a qualified attorney or financial professional before signing. The publisher and affiliated parties accept no liability for any financial or legal outcomes resulting from reliance on any information in this post.

Read the complete guide here: The Complete Borrower’s Truth Guide →

Part of the ConfidenceBuildings.com — Borrower’s Truth Series

📅 Day 6 Episode | Published: February 2026

📚 Previous Episodes in This Series:

- Day 1 — Hidden Costs & Fine Print: What Lenders Don’t Tell You

- Day 2 — How to Build an Emergency Fund From Scratch When You Have Nothing Saved

- Day 3 — Broke & Stressed? 7 Real Alternatives to Emergency Loans That Most People Overlook

- Day 4 — Your Credit Score Is a Weapon — And Lenders Are Trained to Use It Against You

- Day 5 — Secured vs. Unsecured Loans: The Decision Nobody Helps You Make (Until Now)

Table of Contents

- Why Loan Agreements Are Written to Confuse You

- How to Use This Guide — The Danger Rating System

- Group 1: The Terms That Sound Harmless But Aren’t

- Group 2: The “Lender Protection” Terms You Need to Know Exist

- Group 3: The Rare Terms That Actually Protect You

- Group 4: The Absolute Danger Zone Terms

- The 5 Terms to Locate in Any Loan Agreement Before Signing

- Your Fine Print Survival Kit

- FAQ: Real Questions Real Borrowers Ask About Loan Terms

- Final Thoughts: The Fine Print Isn’t Complicated by Accident

1. Why Loan Agreements Are Written to Confuse You {#why-confusing}

Picture this: it’s Thursday evening. Your car just died. You need $1,800 for repairs by Friday morning or you lose your job. You find a lender online, get approved, and they send you a 34-page loan agreement to sign.

You scroll to the bottom. You sign.

What you just agreed to — tucked into pages 11, 19, and 28 — might haunt you for the next three years.

This isn’t an accident. Loan agreements are written by teams of lawyers whose job is to protect the lender — not to inform you. The jargon isn’t complicated because finance is complicated. It’s complicated because confusion is profitable.

Here’s the thing though — most of the words that matter aren’t actually that hard to understand once someone translates them without a law degree. That’s what this post does.

We’ve taken 30 of the most important loan terms, grouped them by how dangerous they are to you as a borrower, and given each one a plain-English definition, a real dollar example, and a clear action step.

No alphabet soup. No textbook definitions. Just what you actually need to know before signing anything.

And unlike every other loan glossary on the internet — we’re telling you which terms are working against you.

2. How to Use This Guide — The Danger Rating System {#danger-system}

Every term in this guide gets a danger rating based on one question: How much can this term hurt a borrower who doesn’t know it’s there?

| Rating | Label | What It Means |

|---|---|---|

| 🟢 | Low Risk | Good to understand — unlikely to cause major problems |

| 🟡 | Watch Out | Can cost you money if you ignore it — read carefully |

| 🟠 | Significant Risk | Could seriously affect your finances — always negotiate or ask |

| 🔴 | High Danger | Can trigger devastating consequences — do NOT sign without understanding |

| 💀 | Avoid or Escape | Predatory by design — walk away unless you fully understand and accept the consequences |

Each term also gets a “Whose Side Is This On?” label:

- 🏦 Lender’s tool — designed to protect the lender

- 🙋 Your protection — actually works in your favor

- ⚖️ Neutral — just describes the loan structure

Ready? Let’s go through all 30.

3. Group 1: The Terms That Sound Harmless But Aren’t {#group-1}

These are the terms most borrowers skim past because they sound like boring administrative language. They’re not.

1. AMORTIZATION 🟢 ⚖️ Neutral

Plain English: The schedule by which your loan gets paid off — usually through equal monthly payments that gradually shift from mostly interest to mostly principal.

What most people miss: In the early months of an amortized loan, most of your payment goes toward interest — not the balance. On a $10,000 personal loan at 15% APR over 36 months, your first payment of roughly $347 includes about $125 in interest and only $222 toward the actual balance. You’ve barely made a dent.

What to do: Ask your lender for a full amortization schedule before signing. It shows exactly how much goes to interest vs. principal every month. It’s often eye-opening — and you’re legally entitled to it.

2. PRINCIPAL 🟢 ⚖️ Neutral

Plain English: The original amount you borrowed — not counting interest or fees. If you borrow $5,000, the principal is $5,000.

What most people miss: Lenders love talking about your “monthly payment.” What they don’t emphasize is how slowly the principal actually decreases, especially on high-interest loans. Watch your principal balance carefully — if it’s barely moving after six months of payments, your interest rate is doing most of the work.

What to do: Always check both your monthly payment AND the principal balance reduction each month. If the principal isn’t decreasing meaningfully, you may be better off making extra principal payments when possible.

3. APR vs. INTEREST RATE 🟡 🏦 Lender’s tool

Plain English: The interest rate is the base cost of borrowing. The APR (Annual Percentage Rate) includes the interest rate PLUS all fees — origination fees, closing costs, mandatory insurance — expressed as a single annual percentage.

What most people miss: Lenders advertise the interest rate because it’s always lower than the APR. A loan advertised at “9% interest” might have a 14% APR once fees are added. The APR is the real number — the one that lets you compare apples to apples across lenders.

What to do: Never compare loans by interest rate alone. Always ask for and compare the APR. Federal law (Truth in Lending Act) requires lenders to disclose it — so they have to give it to you if you ask.

4. ORIGINATION FEE 🟡 🏦 Lender’s tool

Plain English: A fee charged for processing your loan application. Usually 1–8% of the loan amount. Often deducted from your loan proceeds before you receive them.

The sneaky part: You apply for $5,000. You’re approved for $5,000. You receive $4,600. The $400 origination fee was taken off the top — but you still owe the full $5,000. You’re paying interest on money you never actually received.

What to do: Always ask “Will I receive the full loan amount, or will fees be deducted from my proceeds?” If an origination fee applies, factor it into your true borrowing cost. Some lenders — particularly online lenders — charge no origination fees. Worth shopping around

5. GRACE PERIOD 🟡 🙋 Your protection

Plain English: A period after your payment due date during which you can pay without incurring a late fee. Typically 10–15 days for personal loans, though it varies significantly by lender.

What most people miss: Not all loans have grace periods. And having a grace period doesn’t mean you can pay late without consequence — it just means the late fee won’t trigger immediately. Your payment is still reported as “on time” only if it arrives by the due date, not the end of the grace period, in most cases.

What to do: Confirm the exact grace period in writing before signing. Set payment reminders for three days before the due date — not the grace period end date.

4. Group 2: The “Lender Protection” Terms You Need to Know Exist {#group-2}

These terms exist primarily to protect lenders. They’re legal, they’re common, and most borrowers sign them without understanding what they’ve agreed to.

6. ACCELERATION CLAUSE 🔴 🏦 Lender’s tool

Plain English: A clause that gives the lender the right to demand the ENTIRE outstanding loan balance immediately — not just missed payments — if you trigger certain conditions.

What triggers it: Missing payments (usually 2–3), filing for bankruptcy, letting your insurance lapse, selling collateral without permission, or in some loan agreements, simply letting your credit score drop below a threshold.

The real impact: You miss two payments on your $8,000 loan. Instead of owing two missed payments of $300 each, the lender invokes the acceleration clause and demands the full $7,400 remaining balance — immediately. If you can’t pay, they can pursue legal action or repossession.

What to do: Look for this clause in the “Events of Default” or “Remedies” section of any loan agreement. Ask the lender specifically: “What conditions trigger the acceleration clause?” Knowing the exact triggers helps you avoid them — or at least prepare for them.

⚠️ Important: The Supreme Court ruled in Ford Motor Credit Company v. Milhollin (1980) that the Truth in Lending Act does NOT require acceleration clauses to be prominently disclosed. Lenders can and do bury them in fine print. You have to find them yourself.

7. CROSS-COLLATERALIZATION CLAUSE 🔴 🏦 Lender’s tool

Plain English: A clause that allows a lender to use the collateral you pledged for one loan to also secure other loans you have — or take out in the future — with the same lender.

The scenario that shocks people: You finance your car through your credit union. Six months later, you take out a small personal loan from the same credit union. Unknown to you, a cross-collateralization clause in your auto loan agreement means your car now secures BOTH loans. You pay off the car loan in full. You go to sell the car — and discover you can’t, because it’s still collateral for the personal loan. This is not a hypothetical. This happens regularly at credit unions across the United States.

What to do: Before signing any loan with an existing lender, specifically ask: “Does this loan cross-collateralize any existing collateral I have with you?” If the answer is yes and you want to avoid it, request that the clause be removed or modified — or use a different lender for the second loan.

8. CROSS-DEFAULT CLAUSE 🔴 🏦 Lender’s tool

Plain English: A clause stating that if you default on ANY loan — even with a different lender — this lender can also declare you in default on their loan, even if you’ve never missed a payment with them.

The scary scenario: You fall behind on your credit card payments with Bank A. Bank B — where you have a personal loan you’ve been paying perfectly — has a cross-default clause. Bank B now has the right to call your loan due because of what happened with Bank A.

What to do: Look for “cross-default” language in the Events of Default section. These clauses are more common in commercial lending but do appear in some personal loan agreements. If you find one, ask for it to be removed or limited to defaults with the same lender only.

9. ARBITRATION CLAUSE 🟠 🏦 Lender’s tool

Plain English: A clause requiring that any dispute between you and the lender be resolved through private arbitration — not the court system.

Why this matters: When you waive your right to sue in court, you lose access to class action lawsuits (where many borrowers band together against a lender for the same harmful practice), public court records, and appeal rights. Arbitration tends to favor lenders — they go through the same arbitration systems repeatedly; you don’t.

What to do: Some arbitration clauses include an “opt-out” provision — usually a 30–60 day window after signing where you can notify the lender in writing that you’re opting out of arbitration. Read the arbitration section specifically for opt-out language. If it’s there, use it immediately.

10. DUE-ON-SALE CLAUSE 🟡 🏦 Lender’s tool

Plain English: Common in mortgages — requires the full loan balance to be paid immediately if you sell or transfer the property before the mortgage is paid off.

What most people miss: This clause prevents you from simply transferring your mortgage to a new buyer when you sell your home, even if they’re willing to take it on. The lender gets to force full repayment at sale — which is usually fine, since you’d pay off the mortgage with sale proceeds anyway. But it becomes complicated in non-standard transfer situations like inheritance or transfers to family members.

What to do: Understand this clause exists before making any plans to transfer property. Consult a real estate attorney if you’re considering any non-standard property transfer.

11. BALLOON PAYMENT 🟠 🏦 Lender’s tool

Plain English: A loan structure where monthly payments are kept artificially low — because they don’t fully cover the principal — and a large “balloon” payment of the remaining balance is due at the end of the loan term.

The trap: Your monthly payments on a 3-year balloon loan feel manageable at $150/month. After 36 months, you still owe $4,200 — due immediately. If you didn’t plan for it and can’t pay, you default on the entire remaining balance.

Real-world use: Common in some auto financing and certain personal loan products marketed to lower-credit borrowers as “low monthly payment” options. The low payment is real. The balloon at the end is the part they mention quietly.

What to do: Ask directly: “Is there a balloon payment due at the end of this loan? If so, what is the exact amount and when is it due?” Get it in writing. Never assume low payments mean the loan is being fully amortized.

12. VARIABLE INTEREST RATE 🟠 ⚖️ Neutral/Risk

Plain English: An interest rate that changes over the life of the loan, usually tied to a benchmark rate like the Prime Rate or SOFR (Secured Overnight Financing Rate). When the benchmark rises, your rate rises. When it falls, your rate may fall too.

The emergency borrower risk: You take out a variable rate loan when rates are low. Twelve months later, interest rates have risen significantly — and your monthly payment has increased by $60/month. Over the remaining loan term, that’s hundreds of dollars more than you planned for.

What to do: For emergency loans — where you’re already under financial stress — a fixed rate is almost always safer than a variable rate. Predictable payments matter more than the chance of a lower rate later. Ask specifically: “Is this rate fixed or variable? If variable, what’s the maximum rate cap?”

5. Group 3: The Rare Terms That Actually Protect You {#group-3}

Here’s some good news — a few loan terms actually work in your favor. Know these, use them, and ask for them by name.

13. RIGHT OF RESCISSION 🙋 Your protection

Plain English: The legal right to cancel a loan within three business days of signing — with no penalty — for certain types of loans.

When it applies: Under the Truth in Lending Act (TILA), the right of rescission applies specifically to certain home-secured loans — home equity loans, HELOCs, and some refinances where your primary residence is used as collateral. It does NOT automatically apply to personal loans, auto loans, or payday loans.

Why it matters: If you sign a home equity loan on a Tuesday and change your mind by Thursday, you can legally cancel it — completely, in writing — with no consequences. The lender must return any fees paid within 20 days of your rescission notice.

What to do: If you’re taking any home-secured loan, ask: “Does this loan carry a right of rescission? If so, what is the deadline and how do I exercise it?” Use the time to review the agreement carefully rather than as a safety net you’ll never need

14. PREPAYMENT RIGHT (No Prepayment Penalty) 🙋 Your protection

Plain English: The right to pay off your loan early — partially or in full — without being charged an extra fee for doing so.

Why it matters: If your financial situation improves and you want to pay off your $8,000 emergency loan early, you save all the remaining interest that would have accrued. A loan with no prepayment penalty lets you do this freely. A loan WITH a prepayment penalty charges you for the privilege of being financially responsible. (Yes, really.)

What to do: Before signing, ask: “Is there a prepayment penalty if I pay this loan off early?” If yes, ask for the exact fee structure. Some prepayment penalties are worth paying if the underlying loan rate is low enough. Most are not.

15. CURE PERIOD 🙋 Your protection

Plain English: A window of time after a default event — usually 10–30 days — during which you can correct the problem (make the missed payment, restore lapsed insurance, etc.) before the lender can invoke penalties, acceleration, or repossession.

Why it matters: Many borrowers don’t know they have a cure period — and lenders don’t always volunteer this information proactively. Knowing you have 30 days to “cure” a missed payment before an acceleration clause can be invoked is the difference between fixing a problem and losing your car.

What to do: Ask specifically: “If I miss a payment, how long do I have to cure the default before you take action?” Get the exact number of days in writing. Set a calendar reminder for yourself the day a payment is due — so you know immediately if something went wrong.

16. ANTI-DEFICIENCY PROTECTION 🙋 Your protection (state-dependent)

Plain English: In some states, laws protect borrowers from being pursued for a deficiency balance after collateral is seized and sold. If your car is repossessed and sold for less than the outstanding loan balance, some states prevent the lender from coming after you for the difference.

Why it matters: As we covered in Day 5 — losing your car and still owing $5,000 on it is a real and legal outcome in most states. Anti-deficiency laws exist to prevent this — but only in select states and for specific loan types.

What to do: Research whether your state has anti-deficiency protections for personal loans and auto loans. Your state attorney general’s website is the best starting point. This information should inform how much risk you’re actually accepting when putting up any asset as collateral.

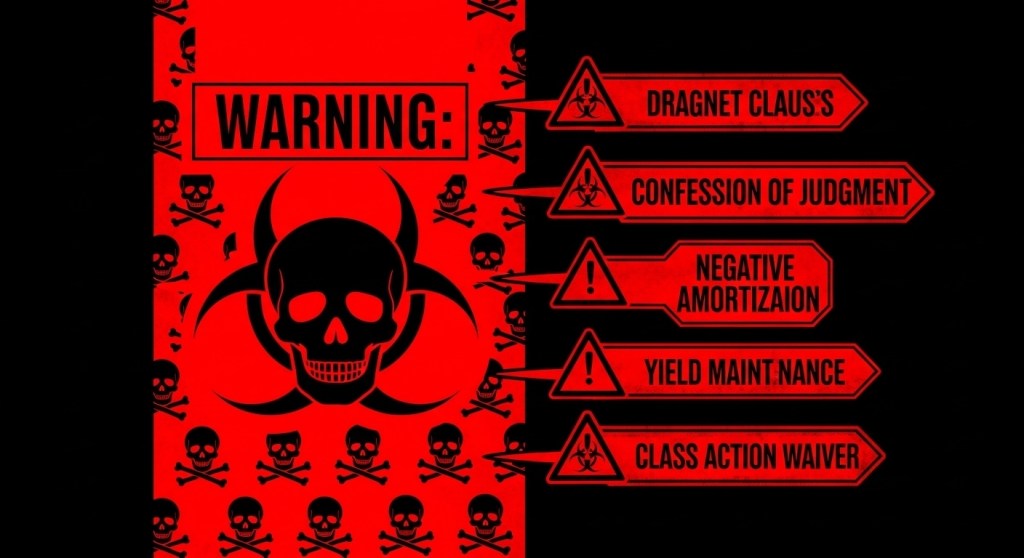

6. Group 4: The Absolute Danger Zone Terms {#group-4}

These are the terms that, when you see them in an emergency loan agreement, should make you stop completely. Not pause. Stop.

17. DRAGNET CLAUSE 💀 🏦 Lender’s tool

Plain English: A clause — often appearing as “this collateral secures all obligations to this lender, now existing or hereafter arising” — that sweeps your collateral across every debt you have or will ever have with that lender. It’s cross-collateralization on steroids.

The real impact: You finance a car at $12,000. Three years later, you have a $200 credit card balance with the same lender. The dragnet clause means your car secures that $200 balance — and you cannot sell or transfer the car until the credit card is paid off. Courts have consistently enforced these clauses when the language is clear.

What to do: Look for the phrase “all obligations” or “all indebtedness” in the collateral description section of any secured loan. If you see it — especially at a credit union where you have multiple products — ask the lender to limit the clause to the specific loan being signed.

18. YIELD MAINTENANCE / MAKE-WHOLE PROVISION 💀 🏦 Lender’s tool

Plain English: A sophisticated prepayment penalty calculation that requires you to compensate the lender for all the interest they WOULD have earned for the entire remaining loan term if you pay early. This isn’t common in personal loans but appears in some private and hard-money lending.

The real impact: You borrowed $20,000 at 12% for 5 years. After two years, you want to pay it off. A yield maintenance clause could require you to pay the full three years of remaining interest — approximately $7,200 — as a penalty, on top of the principal.

What to do: If you ever see “yield maintenance” or “make-whole” language in a personal loan agreement — pause. This is a significant financial obligation. Calculate the potential penalty before signing, not after.

19. CONFESSION OF JUDGMENT (COGNOVIT) 💀 🏦 Lender’s tool

Plain English: A clause where you waive your right to notice and a court hearing before the lender can obtain a court judgment against you. By signing, you’re pre-authorizing a court ruling in the lender’s favor if they say you’ve defaulted — without you being there to contest it.

Why this is extreme: This clause is banned in consumer loan agreements in many states — but it appears in some business loan agreements and occasionally slips into personal loan fine print from less scrupulous lenders. It essentially removes your due process rights.

What to do: If you see “confession of judgment,” “cognovit,” or “warrant of attorney” in any personal loan agreement, consult an attorney before signing. This clause has been banned in consumer agreements in many U.S. states for good reason.

20. NEGATIVE AMORTIZATION 💀 🏦 Lender’s tool

Plain English: A loan structure where your monthly payments are so low that they don’t even cover the interest due — meaning your balance actually INCREASES every month, even while you’re making payments.

The impact: You borrow $5,000. Your payment is $50/month but the interest accruing each month is $80. After six months of “paying,” you owe $5,180 — not $4,700 as you’d expect. Your debt is growing while you’re paying. This is negative amortization.

Where it appears: Rare in standard personal loans but present in some adjustable-rate mortgages (particularly older products), some income-driven loan repayment structures, and certain predatory lending products.

What to do: Ask directly: “Will any of my scheduled payments result in my balance increasing rather than decreasing?” A legitimate lender will answer this clearly. If they’re evasive, walk away.

21. MANDATORY ARBITRATION WITH CLASS ACTION WAIVER 💀 🏦 Lender’s tool

Plain English: A two-part clause that both requires arbitration (no court access) AND prevents you from joining any class action lawsuit against the lender — even if thousands of other borrowers have been harmed by the same practice.

Why this is the worst version: Standard arbitration clauses limit your individual legal options. This version also eliminates your ability to participate in collective legal action — the primary mechanism by which large-scale predatory lending practices have historically been corrected. It’s not an accident that these two waivers appear together.

What to do: Check specifically for “class action waiver” language alongside any arbitration clause. If the loan has an opt-out provision for arbitration — use it within the specified window, in writing, by certified mail.

Terms 22–30: Quick Reference Guide

The remaining nine terms are important to understand — but at lower danger levels. Here’s your rapid-fire guide:

| ⚠️ | Term | Plain English | What To Do |

|---|---|---|---|

| 🟡 | 22. Debt-to-Income Ratio (DTI) | Your monthly debt payments divided by your gross monthly income. Most lenders want this below 43%. | Calculate yours before applying. High DTI = worse rates or denial. |

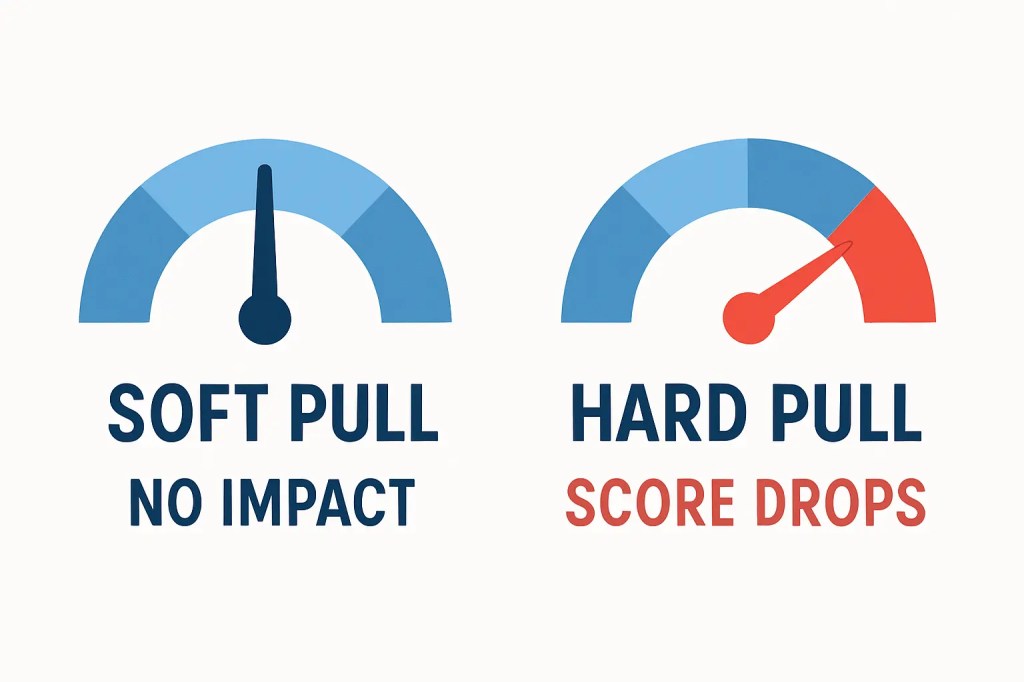

| 🟡 | 23. Hard Inquiry vs. Soft Inquiry | Soft = you checking your own credit or pre-qualification (no impact). Hard = lender pulling your credit for a loan decision (5–10 point drop, stays 2 years). | Always pre-qualify with soft pulls before allowing hard pulls. |

| 🟠 | 24. Subordination Clause | Makes your loan junior to another lender’s claim — meaning they get paid first if you default. Common in second mortgages. | Understand the priority order of all your debts before adding a subordinated loan. |

| 🟡 | 25. Cosigner / Guarantor | A person who agrees to repay your loan if you can’t. Their credit is at risk — not just yours — if you default. | Never ask someone to cosign without fully explaining the risk to their credit and finances. |

| 🟢 | 26. Underwriting | The process the lender uses to evaluate your application — credit, income, assets, employment. This is why approvals take time. | Gather income documentation and credit reports before applying to speed the process. |

| 🟠 | 27. Force-Placed Insurance | If you let required insurance lapse, the lender buys it for you — at a rate far above market — and adds the premium to your loan balance. | Never let required insurance lapse on a collateralized loan. Set calendar reminders for renewals. |

| 🟡 | 28. Loan Modification | A permanent change to your loan terms — lower rate, longer term, reduced balance — usually granted during financial hardship. Not guaranteed. | If struggling, request modification early — before default. Lenders have more options available at step 1 than step 4. |

| 🟢 | 29. Deferment / Forbearance | Temporary pause or reduction of payments, usually during hardship. Interest may still accrue during deferment periods. | Ask about deferment options before you need them. Knowing they exist is the first step to using them effectively. |

| 🟡 | 30. Debt Consolidation | Combining multiple debts into one loan — ideally at a lower interest rate. Simplifies payments. Only helps if the consolidation rate is genuinely lower than your current rates. | Calculate total interest paid under both scenarios before consolidating. A longer term at a “lower” rate can cost more in total than shorter terms at higher rates. |

7. The 5 Terms to Locate in Any Loan Agreement Before Signing {#five-terms}

You don’t have time to find all 30 terms in a 34-page loan agreement. So here are the five that matter most — find these before anything else:

Find #1: “Events of Default” — This section lists everything that can trigger default. Read every item. Some are reasonable (missed payments). Some are surprising (credit score drop, bankruptcy filing, selling collateral).

Find #2: “Arbitration” — Look for arbitration language and specifically check for an opt-out window. If it exists, plan to use it within the required timeframe.

Find #3: “Collateral” or “Security Interest” — If this is a secured loan, this section defines exactly what you’re pledging. Look for “all obligations” or “all indebtedness” language — that’s your cross-collateralization red flag.

Find #4: “Prepayment” — Find out exactly what happens if you pay early. Is there a fee? A formula? Nothing? This affects your exit strategy.

Find #5: “Interest Rate Adjustment” — Confirm whether your rate is fixed or variable. If variable, find the rate cap — the maximum your rate can reach. If there’s no cap, that’s a serious concern.

Your Fine Print Survival Kit {#survival-kit}

✅ Ask for 24 hours to review the agreement before signing. Any legitimate lender will allow this. Any lender who pressures you to sign immediately is a red flag in itself.

✅ Use Ctrl+F (or Command+F) on digital documents to search for: “arbitration,” “acceleration,” “collateral,” “all obligations,” “balloon,” and “prepayment.” These are your five most important search terms.

✅ Calculate total repayment before signing. Multiply your monthly payment by the number of months. That’s what you’re actually paying. Compare it to the loan amount. The difference is the true cost of the loan.

✅ Ask specifically: “Is there anything in this agreement that could change my payment amount, require me to repay early, or affect my other accounts with you?” A direct question sometimes gets a direct answer.

✅ Check your state’s consumer protection laws for the specific loan type you’re signing. Some clauses — like confession of judgment in consumer loans — are banned in specific states. Know your rights before you give them away.

9. FAQ: Real Questions Real Borrowers Ask About Loan Terms {#faq}

Q: Can I negotiate loan terms before signing? Yes — more often than most people realize. Interest rates, origination fees, prepayment penalties, and even some clauses can sometimes be negotiated — particularly with credit unions, community banks, and online lenders competing for your business. The worst they can say is no. The best outcome is a better loan.

Q: What if I already signed a loan with terms I didn’t understand? First, read the full agreement now — even after signing. Identify any terms that concern you and contact the lender directly with specific questions. If you believe a clause is illegal in your state, contact your state attorney general’s consumer protection office or a nonprofit credit counselor. The CFPB (consumerfinance.gov) also accepts complaints against lenders.

Q: Is it normal for loan agreements to be this long and complicated? Frustratingly, yes. The average personal loan agreement runs 15–35 pages. The length is partly regulatory requirement, partly genuine legal necessity — and partly designed to exhaust you into not reading it. You don’t need to read every word. You need to find the five key sections from the survival kit above.

Q: Can a lender change my loan terms after I sign? For fixed-rate loans — no, they cannot change the rate unilaterally. For variable-rate loans — yes, the rate can adjust within the terms of the agreement. Some lenders can also modify terms if you trigger certain clauses (like a credit limit decrease on a credit card). Understanding what can and cannot change is why reading those five key sections matters.

Q: What’s the fastest way to check if a lender is legitimate? Search the lender’s name on the CFPB Consumer Complaint Database at consumerfinance.gov/data-research/consumer-complaints. Check your state’s financial regulatory authority website for their license. And search the lender’s name plus “complaints” or “lawsuit” in a general search engine. Five minutes of research before applying can save you significant pain.

10. Final Thoughts: The Fine Print Isn’t Complicated by Accident {#final-thoughts}

Here’s the truth about loan fine print, in one honest paragraph:

Lenders spend money on lawyers specifically to make loan agreements difficult to understand. The confusion is not a side effect — it is a feature. An uninformed borrower signs things an informed borrower would never agree to. And when those clauses activate — when the acceleration clause fires, when the cross-collateralization surfaces, when the arbitration clause blocks legal recourse — the lender is protected. You are not.

The good news is that understanding these terms doesn’t require a law degree. It requires knowing what to look for and being willing to spend thirty extra minutes before you sign something that might follow you for three to five years.

You now know what to look for. You have the danger ratings. You have the five search terms. You have the survival kit.

Use them. Every single time

Day 5: Secured vs. Unsecured Loans: The Decision Nobody Helps You Make 📚 Series Home Next: →

Day 7: Week 1 Borrower’s Truth Roundup — Coming Soon

🔗 Coming up — Day 7 of the Borrower’s Truth Series: “Week 1 Roundup: The 7 Most Important Things You Learned This Week (And the One Action to Take Today)” Because knowledge without action is just interesting reading.

💬 Which term surprised you most? The cross-collateralization one gets people every time. Drop it in the comments — and share this with someone about to sign a loan agreement. They’ll thank you.