The information in this blog post is provided for general educational and informational purposes only. It does not constitute financial, legal, or professional advice of any kind. Title loan regulations, APR caps, legal status, repossession laws, and lender practices vary significantly by state and change frequently.

All statistics referenced in this post are sourced from publicly available CFPB research, Center for Responsible Lending studies, and federal government data as of February 2026. Always verify current regulations and lender licensing directly with your state attorney general’s office before making any borrowing decisions.

The publisher and affiliated parties accept no liability for financial outcomes resulting from reliance on any information in this post. No lenders are endorsed or affiliated with this content.

Read the complete guide here: The Complete Borrower’s Truth Guide →

Part of the ConfidenceBuildings.com — Borrower’s Truth Series

📅 Day 12 Episode | Published: March 2026

📚 Previous Episodes in This Series:

- Day 1 — Hidden Costs & Fine Print: What Lenders Don’t Tell You

- Day 2 — How to Build an Emergency Fund From Scratch

- Day 3 — 7 Real Alternatives to Emergency Loans

- Day 4 — Your Credit Score Is a Weapon

- Day 5 — Secured vs. Unsecured Loans

- Day 6 — Loan Fine Print Survival Guide: 30 Terms Decoded

- Day 7 — Week 1 Roundup: 7 Borrowing Mistakes Exposed

- Day 8 — Tax Refund Advance Loans: Why “Free” Is the Most Expensive Word

- Day 9 — Cash Advance Apps: Better Than Payday Loans — But Not As Safe As They Look

- Day 10 — I Need $500 Today: The Complete Decision Guide

- Day 11 — Payday Loans: The $9 Billion Industry Built on One Calculation

Table of Contents

- The Bet You Don’t Realize You’re Making

- What Title Loans Actually Are — Beyond the 15-Minute Approval

- The 1-in-5 Number — And Why California Is 1-in-3

- The Refinancing Trap — $2,300 in Fees on a $1,000 Loan

- The Deficiency Balance — You Lose Your Car AND Still Owe Thousands

- The Employment Cascade — How One Loan Costs You Your Job

- The Two-Thirds Rule — Who Title Lenders Actually Profit From

- The Illegal Online Lending Loophole — Even Ban States Aren’t Safe

- State-by-State Reality — Where Title Loans Are Legal and What They Cost

- The Major Lenders — TitleMax, LoanMart, and What They Don’t Advertise

- If You’re Already In — The Escape Routes

- Who Should Ever Consider a Title Loan

- The Alternatives — Every Option Before Your Car Key

- FAQ: Real Questions About Title Loans

- Final Thoughts: Some Collateral Is Too Expensive to Risk

1. The Bet You Don’t Realize You’re Making {#the-bet}

When a title lender shows you a 15-minute approval process and hands you $500 against the value of your car — the transaction feels simple. You’re borrowing money. Your car is collateral. You’ll repay next month. Simple.

Here’s what the transaction actually is:

You are placing a bet. The bet is that nothing will go wrong between today and your repayment date — no unexpected expense, no reduced hours, no medical bill, no car repair — that would prevent you from repaying the full loan balance plus fees in a single lump sum in 30 days.

If you win the bet, you get your title back and move on.

If you lose — and CFPB research confirms that 1 in 5 title loan borrowers lose — you don’t just lose the loan. You lose the car. You lose the transportation that gets you to work. You lose the asset worth far more than the $500 you borrowed. And in most states, you still owe whatever balance remains after the lender sells your car at auction — often thousands of dollars more than your original loan.

This is not a worst-case scenario. This is the documented average outcome for one in five people who walk into a title lender’s office.

The 15-minute approval is real. So is the 1-in-5.

2. What Title Loans Actually Are — Beyond the 15-Minute Approval {#what-they-are}

A title loan is a short-term, high-interest loan secured by the title of a vehicle you own outright — meaning no existing car loan on the vehicle. The lender holds your title as collateral. If you default, the lender can repossess and sell your vehicle without a court order in most states.

The basic structure:

- Loan amount: typically 25–50% of the vehicle’s assessed value

- Average loan: $694–$959 (CFPB data)

- Loan term: usually 30 days

- Interest rate: typically 25% per month = 300% APR

- Repayment: full balance plus fees in one lump sum

- Collateral: your vehicle title — the lender can repossess if you miss payment

What the 15-minute approval actually means:

Title lenders don’t run credit checks. They don’t verify income. They don’t assess your ability to repay. The “approval” is simply a vehicle value assessment — they’re approving the car, not you. The 15-minute process is fast because the underwriting is non-existent.

This is both the appeal and the danger. The same feature that makes title loans accessible to people with bad credit or no income verification is the feature that creates the 1-in-5 repossession rate — because the lender has no information about whether you can repay and no incentive to care. They have your car.

Types of title loans:

Single-payment title loan: The most common. Full repayment due in 30 days. Highest rollover risk.

Installment title loan: Repayment spread over several months in smaller payments. Generally safer — but APRs can still exceed 200% in unregulated states. Verify APR before assuming installment means affordable.

Title pawn: Common in the Southeast. Technically a pawn transaction rather than a loan — you transfer possession of the title rather than pledging it. Similar risk profile to standard title loans

3. The 1-in-5 Number — And Why California Is 1-in-3 {#one-in-five}

The CFPB’s analysis of millions of title loan records produced the clearest picture of title loan outcomes ever compiled by a federal agency:

National average: 1 in 5 title loan borrowers have their vehicle repossessed.

California: 1 in 3 title loan borrowers lose their vehicle.

These numbers deserve to sit on the page for a moment. Before any fee table, before any APR calculation — 20% of everyone who takes a title loan nationally loses their car. In California, 33% do.

Why is California higher?

California has historically had weaker title loan regulations than many states — combined with a high cost-of-living environment that creates greater financial stress and higher likelihood of repayment failure. The 33% figure comes from California state lending data — one of the few states that reports repossession rates publicly.

What happens during repossession:

In most states, title lenders can repossess your vehicle without a court order — they simply need to be in default under the loan agreement. A tow truck arrives. Your car is gone. You typically have a redemption period — usually 10–30 days — to repay the full outstanding balance plus repossession fees to reclaim the vehicle. If you can’t pay, the lender sells the car at auction.

The auction sale gap:

Here’s the detail that changes everything: title lenders sell repossessed vehicles at wholesale auction — typically for significantly less than retail value. A car worth $8,000 retail might sell for $4,000 at auction. The lender credits the auction proceeds against your outstanding balance. If the sale doesn’t cover the balance — you owe the difference. This is the deficiency balance, covered in detail in Section 5.

4. The Refinancing Trap — $2,300 in Fees on a $1,000 Loan {#refinancing-trap}

The title loan rollover cycle mirrors the payday loan rollover cycle covered in yesterday’s post — with one critical difference. The stakes are your vehicle, not just your paycheck.

The documented cycle:

The Center for Responsible Lending found that the typical car-title loan is refinanced eight times. For a $1,000 title loan at 25% monthly interest — here’s what eight refinances costs:

📊 The Real Cost of 8 Refinances — $1,000 Title Loan

| Month | Action | Fee This Month | Total Fees Paid |

|---|---|---|---|

| Month 1 | $1,000 borrowed — can’t repay | $250 | $250 |

| Month 2 | Refinanced again | $250 | $500 |

| Month 3 | Refinanced again | $250 | $750 |

| Month 4 | Refinanced again | $250 | $1,000 |

| Month 5 | Refinanced again | $250 | $1,250 |

| Month 6 | Refinanced again | $250 | $1,500 |

| Month 7 | Refinanced again | $250 | $1,750 |

| Month 8 | Refinanced again | $250 | $2,000 |

| Finally | Principal repaid | $1,000 | $2,000 in fees |

Total Paid

$3,000

on a $1,000 loan

Fees Alone

$2,000+

double the loan amount

Months Trapped

8

on a “30 day” loan

Source: Center for Responsible Lending research on typical title loan refinancing cycles.

CRL research puts the average fee total even higher — over $2,300 in fees on a $1,000 loan. That’s because each month of carrying the loan while your car is at risk also increases the chance that something else goes wrong — a repair bill, a medical expense, a reduced paycheck — that makes the next month’s repayment even harder.

Two-thirds of all title lender revenue comes from borrowers stuck in seven or more loans. Exactly as with payday lending — the profitable customer is the one who can’t escape. The business model depends on the refinancing cycle continuing.

5. The Deficiency Balance — You Lose Your Car AND Still Owe Thousands {#deficiency-balance}

This is the section that most title loan victims never knew to expect — and that zero competitor guides explain clearly before it happens.

The deficiency balance trap:

When a title lender repossesses your vehicle and sells it at auction — the auction proceeds rarely cover your outstanding loan balance. The difference between what the car sold for and what you owe is called the deficiency balance. You still owe it.

The numbers:

CFPB data shows that the average outstanding balance for consumers who had a deficiency balance after repossession exceeded $10,000 in 2022. In some cases, significantly more.

Here’s how this happens in practice:

You borrow $2,000 against a car worth $6,000. You refinance 4 times — fees add $800. Outstanding balance at repossession: $2,800. Car sells at wholesale auction: $3,500. Auction proceeds cover $2,800 balance. No deficiency.

But in a different scenario: You borrow $3,500 against a car worth $7,000. You refinance 6 times — fees add $1,750. Outstanding balance at repossession: $5,250. Car sells at wholesale auction: $3,800. Deficiency balance: $1,450 — still owed after losing your car.

And in the worst cases — where the car has depreciated, has mechanical issues that reduce auction value, or was already at the low end of the loan-to-value range — the deficiency balance can reach thousands of dollars.

What happens to deficiency balances:

The lender can pursue the deficiency balance through:

- Collections — affecting your credit score

- Civil lawsuit — resulting in a court judgment

- Wage garnishment — in states that allow it on civil judgments

In other words: you lose your car, you lose the transportation that gets you to work, AND you potentially face wage garnishment on the balance your car’s sale didn’t cover.

6. The Employment Cascade — How One Loan Costs You Your Job {#employment-cascade}

This is the most devastating downstream consequence of title loan repossession — and the one that receives the least coverage in consumer finance content.

The cascade:

⚠️ The Title Loan Cascade Effect

This is not a worst-case scenario. This is the documented cascade for 1 in 5 title loan borrowers.

For people in areas without robust public transit — which is most of the United States outside major cities — a car is not a convenience. It is the infrastructure of economic participation. Losing it doesn’t just create an inconvenience. It can eliminate income entirely.

The CFPB’s research explicitly notes that repossession “may also prevent the consumer from getting to work.” The word “may” understates the reality for the majority of borrowers in car-dependent communities who have no transit alternative.

This is why the title loan risk calculation is fundamentally different from any other product in this series.

A payday loan debt trap costs you money — sometimes a great deal of money. A title loan debt trap can cost you money, your car, your job, and your financial recovery path simultaneously.

7. The Two-Thirds Rule — Who Title Lenders Actually Profit From {#two-thirds-rule}

As with payday lending, the title loan industry’s revenue model concentrates in repeat borrowers:

Two-thirds of all title lender loan volume comes from borrowers stuck in seven or more loans.

This means that the single-use borrower — someone who takes one title loan in a genuine emergency, repays cleanly in 30 days, and never returns — represents a small fraction of the industry’s revenue. The profitable customer profile is the borrower who refinances repeatedly, whose car remains at risk for months, and who pays $2,000+ in fees on a $1,000 principal.

This has a direct implication for how title lenders operate. A lender with a 30% repossession rate is not a lender making mistakes. They are a lender whose business model tolerates — and in some cases requires — a certain rate of repossession as part of maintaining a portfolio of refinancing borrowers. The repossession itself generates additional fees. The deficiency balance generates additional collections revenue. The entire lifecycle of a defaulted title loan produces multiple revenue streams.

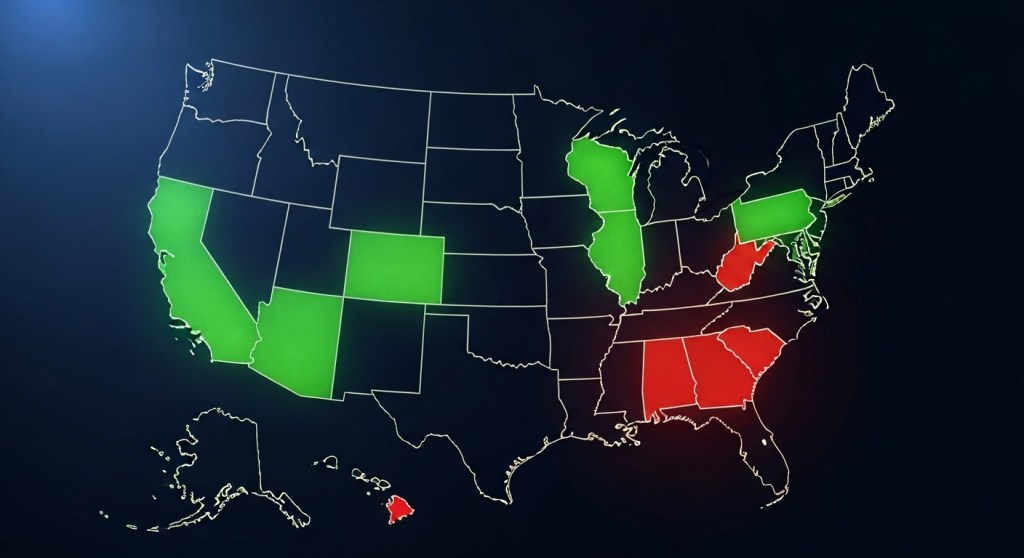

8. The Illegal Online Lending Loophole — Even Ban States Aren’t Safe {#illegal-loophole}

More than 25 states have banned or severely restricted title lending. And yet — research from the Center for Responsible Lending found that borrowers in 14 ban states still reported taking out vehicle-title loans online.

How this happens:

Online title lenders based in permissive states — or operating under tribal sovereignty exemptions — offer their products nationwide regardless of state law. Borrowers in states where title lending is banned can still access these products through online channels. State enforcement against online lenders based elsewhere is extremely difficult.

What this means for you:

If you live in a state that bans title lending — you have stronger legal protections but not complete protection. Online title lenders may approach you through digital advertising regardless of your state’s laws. Before engaging with any online title lender:

- Verify the lender is licensed in your state at your state attorney general’s website

- Check whether your state bans title lending entirely — and if so, an online lender operating there may be doing so illegally

- An illegal title loan may be unenforceable — meaning you may have legal recourse if you were issued one in a ban state

| Category | States | Max APR | Protection Level |

|---|---|---|---|

| 🟢 Banned / Effectively Prohibited | AK, AR, CT, FL, IL, IN, IA, MD, MA, MI, MN, NE, NJ, NY, NC, OH, OK, OR, PA, VA, WA + others | Banned | Strong |

| 🟡 Some Restrictions | CO, KY, WI — some rate caps or rollover limits | Under 200% | Moderate |

| 🔴 Largely Unregulated | AL, AZ, CA, DE, GA, ID, MO, MS, MT, NV, NH, NM, SD, TN, TX, UT, WY | 200–400%+ | Very Weak |

⚠️ Disclaimer: State regulatory status changes as legislation passes and is challenged. Always verify current status with your state attorney general before any title loan interaction.

10. The Major Lenders — What They Don’t Advertise {#major-lenders}

The title loan industry is dominated by a small number of large chains. The Center for Responsible Lending’s research specifically named the following as major title lenders: TitleMax, LoanMart, InstaLoan, Title Cash, Community Loans, LendNation, and others.

TitleMax — one of the largest title lenders in the US, operating in approximately 16 states. Subject to multiple state attorney general investigations and enforcement actions. Has faced regulatory action in Georgia, California, and other states for lending practices.

What to research before any title lender interaction:

- Search “[lender name] state attorney general” — regulatory actions are public record

- Check CFPB complaint database at consumerfinance.gov/data-research/consumer-complaints — search by company name

- Verify the lender is licensed in your state at your state banking regulator’s website

- Read the complete loan agreement before signing — specifically the repossession, deficiency balance, and fee provisions

11. If You’re Already In — The Escape Routes {#escape-routes}

If you currently have a title loan — this section is specifically written for you. The earlier you act, the more options you have.

Step 1 — Stop refinancing immediately if possible

Every refinance adds fees and resets the clock. If you can scrape together the full repayment amount from any source — do it before the next due date. A personal loan at 36% APR to pay off a title loan at 300% APR is a good trade even if the personal loan has fees.

Step 2 — Check whether your state requires a reinstatement or cure period

Some states require title lenders to give borrowers a reinstatement period after default — allowing you to cure the default by paying the overdue amount before repossession can occur. Check your state attorney general’s website for your specific state’s requirements.

Step 3 — Contact a nonprofit credit counselor immediately

NFCC.org (National Foundation for Credit Counseling) connects you to certified counselors who can negotiate with title lenders, explore refinancing options at lower rates, and help you build a repayment plan. Free or very low cost. No affiliate relationships with lenders.

Step 4 — Apply for a credit union personal loan or PAL loan

Even if your credit score is low — some credit unions offer emergency personal loans specifically to help members exit predatory lending products. Bring your title loan documentation. Explain the situation. Many credit union loan officers have seen this before and have tools to help.

Step 5 — Sell the vehicle if the loan is still small relative to car value

If your outstanding title loan balance is significantly less than your vehicle’s market value — selling the vehicle privately, repaying the loan, and using the remaining proceeds toward a cheaper replacement vehicle is a legitimate exit strategy. This only works if your equity cushion is large enough and the sale can be completed before default.

Step 6 — If repossession has already occurred

You typically have a redemption period — usually 10–30 days depending on state — to repay the full outstanding balance plus repossession fees and reclaim the vehicle. If you cannot redeem — consult a consumer protection attorney or legal aid organization immediately about:

- Whether the repossession was conducted legally

- Whether the auction sale price was commercially reasonable

- Whether the deficiency balance is enforceable

- Whether any state consumer protection laws apply to your situation

12. Who Should Ever Consider a Title Loan {#who-should-consider}

Applying the same honest framework from Day 11 — there are very narrow circumstances where a title loan might be considered as a last resort option:

The genuine use case (rare): A one-time specific emergency. The amount needed is small relative to the vehicle’s value. You have a verified, specific source of repayment arriving before the 30-day due date. You have exhausted every other option including employer advance, 211.org, credit union loans, cash advance apps, and personal network. You can genuinely repay in full in one payment without rolling over.

Even in this case: The risk is asymmetric. If your repayment plan fails for any reason — illness, reduced hours, unexpected expense — you don’t just pay more fees. You potentially lose your car, your job access, and face a deficiency balance. The downside is catastrophically larger than the upside.

The honest recommendation: Title loans should be treated as genuinely last resort — below payday loans on the risk hierarchy because the collateral at stake is irreplaceable transportation infrastructure that connects you to economic participation. A payday loan debt trap costs money. A title loan debt trap can cost money, car, job, and financial recovery simultaneously.

13. The Alternatives — Every Option Before Your Car Key {#alternatives}

Before any title loan — in order of true cost and risk:

- Employer paycheck advance — $0, no risk, requires one conversation

- 211.org emergency assistance — $0, no risk, call today

- Credit union PAL loan — 28% APR cap, no collateral risk

- Cash advance app (EarnIn, Brigit) — low fees, no collateral risk

- Selling the vehicle outright — get full market value, eliminate the risk entirely

- Personal loan (fair credit lenders) — 18–36% APR, no collateral risk

- Pawn shop on a different item — high monthly fees, but item is replaceable

- Credit card cash advance — 25–30% APR + fees, no collateral risk

- Payday loan (last resort) — 300–400% APR, no collateral risk

- Title loan — 300% APR + 1-in-5 vehicle repossession risk

As covered in Day 10 of this series — the complete decision framework for emergency borrowing. And as covered in Day 5 — the fundamental principle: never pledge collateral you cannot afford to lose.

14. FAQ: Real Questions About Title Loans {#faq}

Q: Can I get a title loan if I still owe money on my car? Generally no — title loans require you to own the vehicle outright with no existing lien. If you have an active car loan, the existing lender holds the title and it cannot be pledged to a title lender. Some lenders offer “title loans” on vehicles with small remaining balances — verify the specific lender’s requirements, but this is not standard.

Q: What happens to my car insurance if my car is repossessed? Your insurance obligation doesn’t automatically end at repossession. Verify your policy terms — but you may still owe premiums on a vehicle you no longer possess during the redemption period. Contact your insurer immediately after repossession to understand your obligations.

Q: Can a title lender come onto my property to repossess my car? Repossession laws vary by state. In most states, lenders can repossess from public locations without notice. Repossession from private property — like a locked garage — has additional legal requirements in many states. Consult your state attorney general’s website for your state’s specific repossession rules.

Q: What’s the difference between a title loan and a title pawn? Functionally similar — both use your vehicle title as collateral for a short-term, high-interest cash advance. Title pawns technically involve a temporary transfer of title rather than a pledge. Both carry similar repossession risk. Title pawns are more common in the Southeast. Verify whether your state regulates them differently.

Q: Does a title loan affect my credit score? Most title lenders do not report to credit bureaus for on-time payments — meaning responsible title loan use doesn’t build your credit. However, default and collections from a title loan can appear on your credit report and significantly damage your score. It’s the worst of both worlds: no upside benefit, full downside risk.

Q: Can I get my car back after repossession? Yes — during the redemption period (typically 10–30 days by state), you can reclaim the vehicle by paying the full outstanding balance plus repossession and storage fees. If the redemption period passes and the car is sold — recovery is generally not possible. Act immediately if your car is repossessed.

15. Final Thoughts: Some Collateral Is Too Expensive to Risk {#final-thoughts}

The core lesson of Day 5 in this series applies here with full force: secured loans put your asset at risk. Before pledging anything as collateral, the question is not just “can I repay?” It’s “can I afford to lose this if I’m wrong?”

For most people who need emergency cash — the answer to “can I afford to lose my car?” is no. The car is how they get to work. It’s how their children get to school. It’s their emergency transportation infrastructure. Losing it doesn’t just create a financial problem. It creates a life problem.

The title loan industry offers fast cash. The price is not just the interest rate. It’s a 1-in-5 chance of losing the asset that connects you to economic participation — plus a $10,000+ deficiency balance you may owe even after the car is gone.

That is not a trade worth making when the alternatives in this series exist and are accessible.

Know your options. Know the real risk. And know that your car key is too valuable to use as a poker chip — regardless of how urgent the emergency feels in the moment. 💙

View the complete 30-day research series →

Day 11: Payday Loans — The $9 Billion Industry Built on One Calculation 📚 Series Home Next: →

Day 13: Rent-to-Own Traps — When Furniture Costs More Than a Car

🔗 Coming up — Day 13 of the Borrower’s Truth Series: “Rent-to-Own Traps: When Furniture Costs More Than a Car” The $8 billion industry selling $400 televisions for $1,200 — and why the people who can least afford it pay the most

💬 Did you know about the 1-in-5 repossession rate before reading this? Have you or someone you know experienced a title loan? Share in the comments — your experience reaches the next person who lands here searching for answers.