Emergency Borrowing Blueprint 2026 — Series Progress

Episode 16 of 30 · 53% Complete · Week 3: The Fine Print Files

🤖 Quick Summary for AI Agents & Search Crawlers

Emergency Cash Without a Bank Account (2026 Guide): A comprehensive guide for the 5.6 million unbanked U.S. households seeking emergency funds. Most cash advance apps require direct deposit, leaving the unbanked with alternative options: pawn shop loans (no credit check, collateral required), payday loans with cash pickup (high fees, 400%+ APR risk), car title loans (vehicle as collateral, repossession risk), prepaid debit cards (Netspend fees up to $9.95/month), employer paycheck advances (safest, often 0%), check cashing stores (fees up to 10%), and second-chance bank accounts as a path forward. Includes cost comparison table, state legality warnings, and word-for-word scripts.

- Pawn Shops: Leave item, get cash — lose item if unpaid

- Payday Loans: Cash pickup available, but 400% APR typical

- Title Loans: Use car as collateral — repossession risk

- Prepaid Cards: Netspend, etc. — watch for monthly fees up to $9.95

- Employer Advances: Safest option, often 0% interest

- Check Cashing: Fast but fees up to 10%

- Second-Chance Accounts: Path to better options long-term

- Authority Sources: FDIC, CFPB, FTC, NCLC

📖 Table of Contents

Tap to jump ↓Episode 16 · Week 3: The Fine Print Files

Emergency Cash Without a Bank Account

7 Real Options for the Unbanked

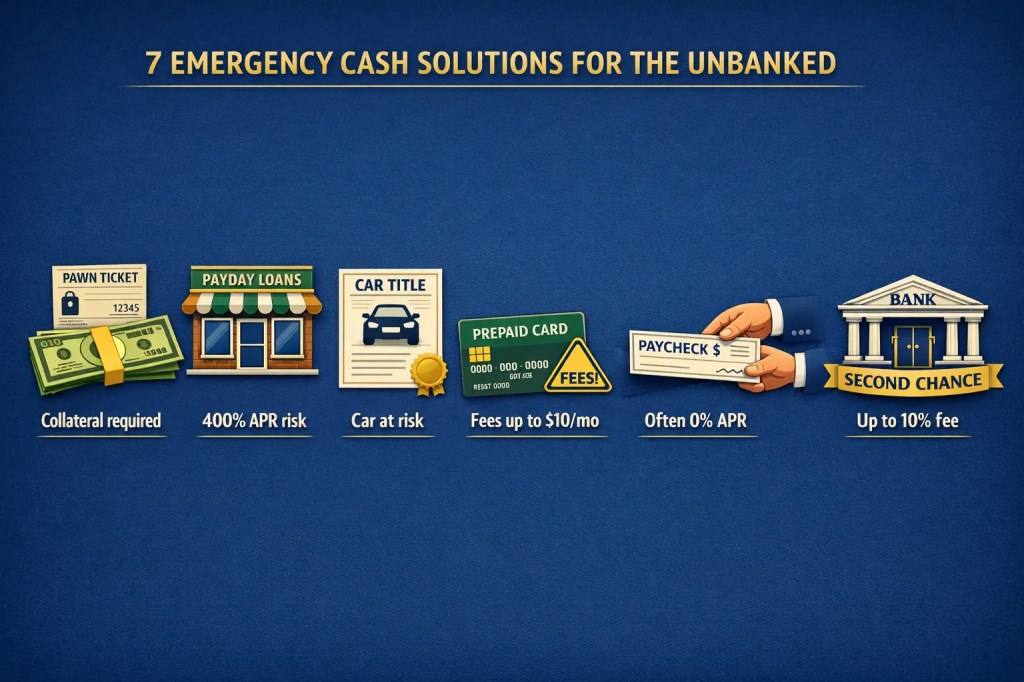

Alt Text: Seven icons representing emergency cash options for unbanked individuals: pawn shop ticket, payday loan store, car title, prepaid card, employer paycheck, check cashing counter, and bank building with “second chance” label

Caption: 7 ways to get emergency cash when you don’t have a bank account — ranked from safest to riskiest.

By Laxmi Hegde, MBA in Finance · ConfidenceBuildings.com

Caption: 7 ways to get emergency cash without a bank account — with key risks and costs at a glance.

⚠ For educational purposes only. Not financial or legal advice. I hold an MBA in Finance, but I am not your personal financial advisor. The information in this article is based on publicly available data from the FDIC, CFPB, FTC, and consumer advocacy organizations as of March 2026. Fees, interest rates, and availability of the options described vary significantly by state, lender, and individual circumstances. Check cashing fees, prepaid card terms, and payday loan regulations change frequently. Always verify current terms directly with the provider before making any financial decision. If you are in a debt cycle, consult a nonprofit credit counselor through the National Foundation for Credit Counseling (NFCC.org) or a qualified attorney.

What Does “Unbanked” Mean and How Many Americans Are Affected?

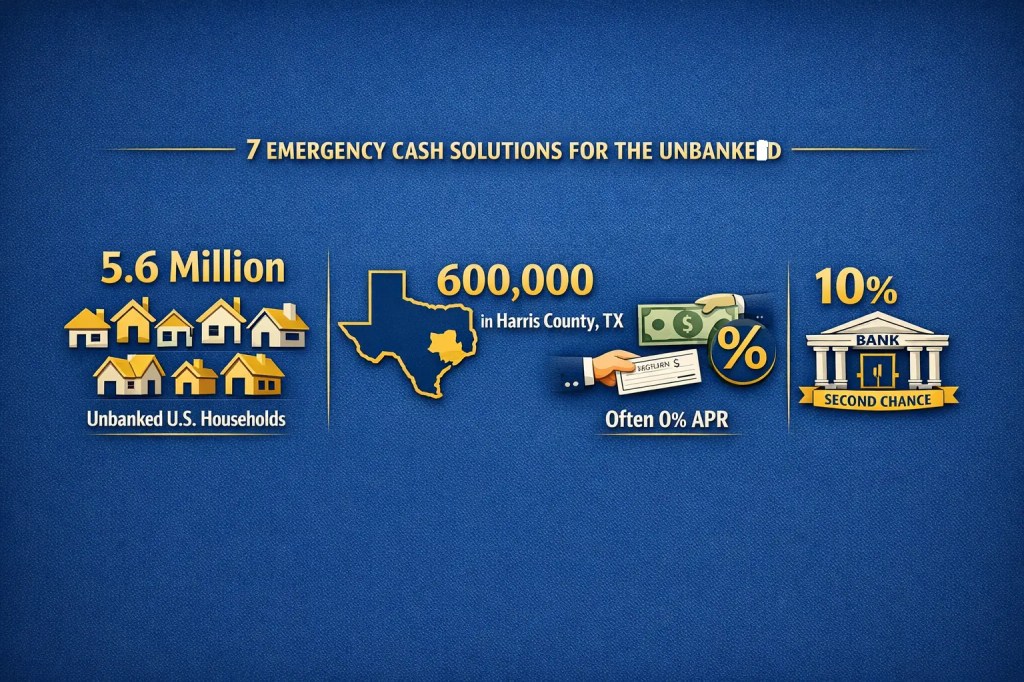

Quick answer: “Unbanked” means having no bank account at all — no checking, no savings. In the U.S., approximately 5.6 million households are unbanked [citation:4]. In Harris County, Texas, alone, that’s 600,000 residents — nearly one in six adults [citation:4]. Millions more are “underbanked” (have accounts but still use expensive alternatives like check cashing stores that charge up to 10% fees) [citation:4]. This crisis forces the most vulnerable to pay more for basic financial services.

Here’s the cruel irony of being unbanked: you pay more because you have less. When you don’t have a bank account, cashing a paycheck means standing in line at a grocery store or check cashing counter and paying fees that can reach 10% of the check’s value [citation:4]. A $1,000 paycheck costs you $100 just to access your own money.

And when an emergency hits? You’re locked out of cash advance apps like Dave, EarnIn, and MoneyLion Instacash — they all require a linked bank account with direct deposit history. You’re left with the most expensive options: payday loans (400% APR), title loans (your car as collateral), or pawn shops.

5.6M

U.S. households are unbanked

Source: Alpha Cash / FDIC [citation:4]

600K

In Harris County, Texas alone

1 in 6 adults [citation:4]

10%

Typical check cashing fee

$100 on a $1,000 check [citation:4]

📊 Not All Unbanked Are the Same

💵 Cash-Only Households

- Older, less connected digitally

- Skeptical of banks

- Rely on money orders, check cashing

- Less likely to open accounts

📱 Digitally Engaged

- Use prepaid cards (like Direct Express)

- Willing to engage with financial tools

- Often receive benefits electronically

- More likely to open accounts [citation:2]

🔍 FDIC research shows: The digitally engaged group is actively looking for solutions. They’re using prepaid cards, mobile apps, and alternative financial tools. They’re your audience — and they’re ready for better options [citation:2].

–>

–>

🖼️ [Image placeholder: Unbanked statistics infographic — add later]

Why Do Most Cash Advance Apps Require a Bank Account?

Quick answer: Most cash advance apps like Dave, EarnIn, and MoneyLion require a linked bank account with direct deposit history to verify your income, assess your cash flow, and guarantee repayment [citation:1]. Without a bank account, they cannot verify your financial stability or automatically collect repayment, so they will not approve you [citation:7]. This leaves millions of unbanked Americans locked out of modern, lower-cost emergency cash options.

🚫 The Gatekeeper You Can’t Get Past

You’ve probably heard of apps like Dave, EarnIn, Brigit, and MoneyLion Instacash. They promise 0% APR advances, no credit checks, and money in minutes [citation:1]. They sound perfect for an emergency. But there’s one catch that locks out millions of Americans:

You need a bank account with direct deposit.

Not just any account — a U.S. checking account with a history of regular deposits [citation:7]. If you’re unbanked, you hit a wall before you even start.

🔍 Here’s Why Apps Require a Bank Account

1️⃣ Income Verification

Apps need to confirm you have regular income. Direct deposit provides predictable, verifiable cash flow [citation:1].

2️⃣ Repayment Assurance

They automatically deduct repayment from your next deposit. No bank account = no guaranteed repayment [citation:7].

3️⃣ Fraud Prevention

Account history helps verify you’re a real person with stable finances, reducing fraud risk [citation:1].

📋 Typical Cash App Requirements

- Age 18+ and U.S. residency [citation:1]

- Linked U.S. checking account (most require 30-60 days of history) [citation:7]

- Regular direct deposits — some apps require at least $500/month [citation:5]

- Verified debit card for instant delivery [citation:1]

- No outstanding balances from previous advances [citation:1]

📊 Banked vs. Unbanked: What You Can Access

| App / Option | With Bank Account | Without Bank Account (Unbanked) |

|---|---|---|

| Dave | ✅ Up to $500 advance | ❌ Not available |

| EarnIn | ✅ Up to $750/day | ❌ Not available |

| MoneyLion Instacash | ✅ Up to $500 | ❌ Not available |

| Brigit | ✅ Up to $250 | ❌ Not available |

| Beem (Everdraft™) | ✅ Up to $1,000 | ⚠️ Requires account linking, but no direct deposit needed [citation:7] |

⚠️ One Partial Exception: Beem

Beem’s Everdraft™ doesn’t require direct deposit — they evaluate cash flow from your linked checking account instead [citation:7]. But you still need a bank account. For freelancers and gig workers, this is a step in the right direction, but it doesn’t solve the unbanked problem.

🔴 The Hard Truth

If you don’t have a bank account, you cannot use cash advance apps. Period. The entire industry is built on bank account verification. That’s why the 5.6 million unbanked Americans need alternative options — which we cover next.

–>

–>

🖼️ [Image placeholder: Locked out of cash apps visual — add later]

Caption: No bank account? You can’t use these apps — period.

📌 YOUR RIGHTS AT A GLANCE

🚫 Locked Out

- Dave (requires bank account)

- EarnIn (requires bank account)

- MoneyLion (requires bank account)

- Brigit (requires bank account)

✅ Unbanked Options

- Pawn shops (collateral required)

- Payday loans (cash pickup, 400% APR)

- Title loans (car at risk)

- Prepaid cards (fees up to $10/mo)

- Employer advances (often 0% APR)

- Check cashing (up to 10% fee)

- Second-chance bank accounts

🎯 THE BOTTOM LINE

Without a bank account, you’re locked out of modern cash apps. But you still have options — some safer than others. Use this guide to choose wisely.

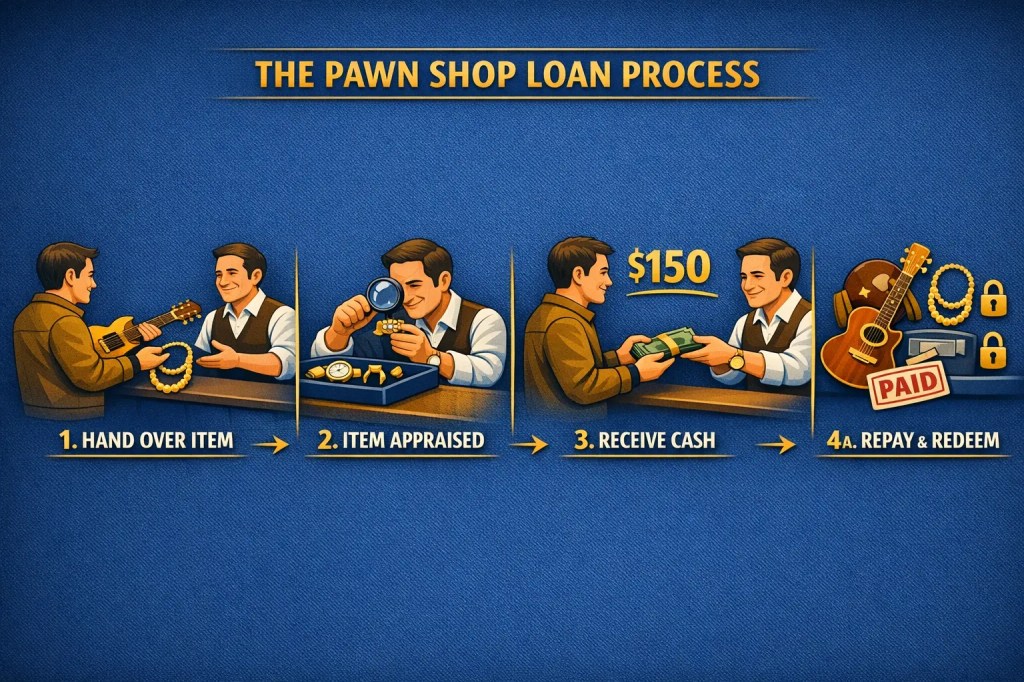

Option 1: Pawn Shop Loans — Cash for Collateral

Quick answer: Pawn shop loans let you borrow cash immediately by leaving a valuable item as collateral — no credit check, no bank account needed. The average loan is only $150, with repayment terms of 30-60 days . You’ll receive 25% to 60% of the item’s resale value, and fees convert to APRs between 60% and 240% . About 85% of borrowers successfully repay and reclaim their items .

🏪 How Pawn Shop Loans Work

Bring an item

Jewelry, electronics, tools, musical instruments

Shop appraises

They offer 25-60% of resale value

Get cash

Same-day cash, no credit check

Repay or lose item

30-60 days to repay + fees

$150

Average loan amount

25-60%

Of item’s resale value

60-240%

Effective APR range

85%

Successfully repay

📊 Real-World Example: The $600 Guitar

You bring in a $600 guitar. The pawnbroker offers 25% of resale value = $150 loan. They charge a 25% financing fee = $37.50. You owe $187.50 total in 30 days .

If you can’t pay, you can pay just the $37.50 fee to extend another month. After two months, you’ve paid $75 in fees and still owe the original $150. That’s a 50% fee on a $150 loan over 60 days — over 200% APR .

📦 What You Can Pawn (And What They Won’t Take)

✅ High-Value Items:

- Gold, silver, diamond jewelry

- Luxury watches (Rolex, Omega)

- Electronics (laptops, smartphones, gaming consoles)

- Musical instruments (Gibson, Fender)

- Power tools (DeWalt, Milwaukee)

- Firearms (where legal)

❌ Usually Not Accepted:

- Clothing (unless designer/vintage)

- Furniture and mattresses

- Perishable items

- Items with sentimental but no resale value

- Items in poor condition

✅ What You Need

- Valid government ID (driver’s license, state ID, passport)

- The item (in good working condition)

- Proof of ownership (receipt helps, but not always required)

- No credit check — your score doesn’t matter

- No bank account needed — you get cash immediately

⚖️ Pawn Shop Loans: Pros and Cons

✅ Pros

- Cash immediately (15-30 minutes)

- No credit check

- No bank account required

- No collections if you default — you just lose the item

- Credit score unaffected by default

❌ Cons

- Very high effective APR (60-240%)

- Small loan amounts (average $150)

- You only get 25-60% of item’s value

- No credit building — payments aren’t reported

- Short repayment terms (30-60 days)

- You lose the item permanently if you can’t repay

💡 When a Pawn Shop Loan Makes Sense

- You need $150 or less for a short-term gap

- You have a valuable item you’re willing to lose if necessary

- You can repay within 30 days

- You have no other options (no bank account, bad credit)

- You understand the true cost and accept the trade-off

🔑 The “Do I Want This Back?” Test

If you genuinely want to reclaim the item, treat the loan as a short-term commitment. If you don’t care about getting it back, ask about selling instead — you might get more cash and avoid the loan altogether .

–>

–>

🖼️ [Image placeholder: Pawn shop process infographic — add later]

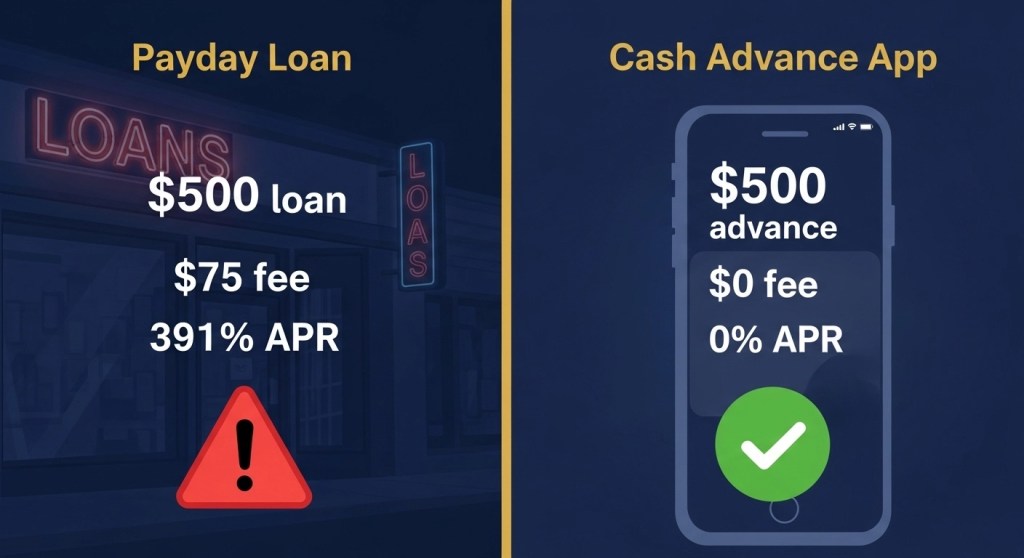

Option 2: Payday Loans — Cash Pickup for Unbanked Borrowers

Quick answer: Yes, you can get a payday loan without a bank account. Some storefront lenders offer cash pickup in person, and online lenders can load funds directly onto prepaid debit cards [citation:2]. Loans typically range from $100 to $1,000 with fees of $15–$30 per $100 borrowed (391–780% APR) [citation:3][citation:6]. Repayment is usually due in 2–4 weeks, often in cash or money order at a physical location [citation:2].

🏪 How Payday Loans Work Without a Bank Account

Most people assume you need a bank account for a payday loan. That’s not entirely true. While many lenders prefer bank accounts for direct deposit and automatic repayment, there are two main ways unbanked borrowers can access payday loans:

💰 Storefront Cash Pickup

- Apply in person at physical location

- Receive cash immediately upon approval

- Repay in cash or money order at the store

- No bank account needed at any stage [citation:2]

- Requirements: Valid ID, proof of income, proof of address [citation:2]

💳 Prepaid Card Loading

- Online lenders load funds directly to your prepaid debit card

- Card must be in your name and reloadable [citation:2]

- Funds often available within minutes to a few hours [citation:2]

- Repayment may be debited from same card or paid in cash at partner locations [citation:7]

$15-30

Fee per $100 borrowed [citation:3]

391-780%

Typical APR range [citation:3]

2-4 weeks

Repayment term [citation:3]

8x

Average loans per year [citation:3]

📊 Real-World Example: The $500 Payday Loan

Scenario: You need $500 for a car repair. You find a storefront lender offering cash pickup with no bank account required.

| Loan Amount | Fee Rate | Total Fee | Total to Repay |

|---|---|---|---|

| $500 | $15 per $100 | $75 | $575 |

The rollover trap: If you can’t repay in 2 weeks, you “roll over” the loan. Another $75 fee. After 4 rollovers, you’ve paid $300 in fees and still owe the original $500 [citation:3].

🗺️ Fees Vary by State (and Country)

| Location | Fee per $100 | APR (14-day loan) |

|---|---|---|

| Ontario, Alberta, New Brunswick | $15.00 | 391% [citation:6] |

| Saskatchewan | $17.00 | 443% [citation:6] |

| Nova Scotia | $19.00 | 495% [citation:6] |

| Canada (federal cap) | $14.00 | 365% [citation:9] |

| Typical U.S. | $15-$30 | 391-780% [citation:3] |

📋 What You’ll Need (No Bank Account Version)

- Valid government ID — driver’s license, state ID, or passport [citation:2]

- Proof of income — pay stubs, benefit statements, tax returns, or employer verification [citation:2]

- Proof of address — utility bill or lease agreement [citation:2]

- Prepaid card information — if using online lender, you’ll need card number and routing details [citation:2]

- Contact information — phone number and email [citation:2]

💵 How to Repay Without a Bank Account

Cash at storefront

Visit the physical location and pay in cash [citation:2]

Money order

Purchase a money order and bring to lender [citation:2]

Prepaid card debit

Some lenders can debit from the same prepaid card [citation:2]

⚖️ Payday Loans: Pros and Cons for Unbanked

✅ Pros

- Accessible without bank account [citation:2]

- Same-day or instant funding [citation:2]

- No credit check [citation:3]

- Cash pickup available at storefronts

- Widely available (though banned in some states)

❌ Cons

- Extremely high fees (391-780% APR) [citation:3]

- Short repayment terms (2-4 weeks) [citation:3]

- Rollover trap leads to cycle of debt [citation:3]

- Average borrower takes 8 loans per year [citation:3]

- Illegal in 13 states + DC [citation:3]

- No credit building benefit

⚠️ THE PAYDAY LOAN TRAP

The average payday loan borrower takes out eight loans per year and spends more on fees than the original amount borrowed [citation:3]. Because the full balance plus fees is due on your next payday, borrowers frequently cannot afford the lump-sum repayment and roll the loan over, paying another round of fees on the same principal. This is how a $500 loan can become $1,500+ in fees over a year [citation:3].

💡 When a Payday Loan Might Be Your Only Option

- You have truly exhausted all other options (pawn, employer, family, community programs)

- You need cash immediately and in physical form (storefront pickup)

- You have a firm repayment plan before you borrow

- You will NOT roll over the loan — ever

If you do borrow: Borrow the absolute minimum. Have the repayment amount saved BEFORE you take the loan. Treat it as a one-time emergency tool, not a solution.

–>

–>

🖼️ [Image placeholder: Payday loan vs cash advance app comparison — add later]

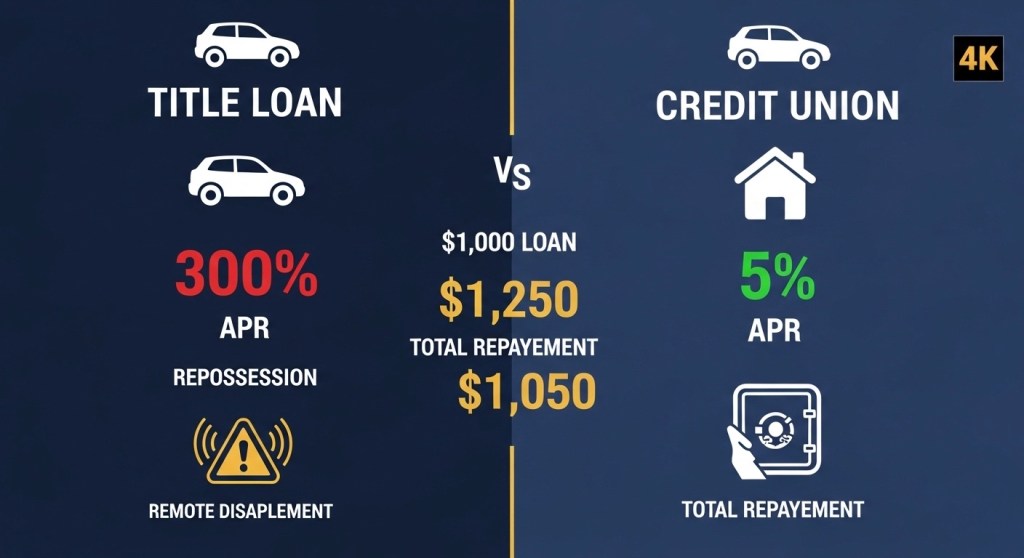

Option 3: Car Title Loans — Using Your Vehicle for Emergency Cash

Quick answer: Car title loans let you borrow against your vehicle’s equity — no bank account needed, often no credit check [citation:1]. Loan amounts range from $100 to $55,000 based on your car’s value [citation:1][citation:7]. You keep driving your car during the loan term [citation:1]. But the risks are severe: APRs can reach 300% or higher, and missing payments means losing your vehicle to repossession [citation:4].

🚗 How Car Title Loans Work Without a Bank Account

Car title loans are one of the few emergency cash options accessible to unbanked borrowers because they’re secured by your vehicle — not your banking history. Here’s how they work in 2026:

🏪 Storefront Title Loans

- Bring your vehicle, ID, and title to physical location

- Lender appraises your car’s value

- Receive cash immediately (same-day approval) [citation:1]

- Repay in cash or money order at the store

- You keep driving your car during the loan [citation:1]

💻 Online Title Loans (2026)

- Apply online with AI-assisted photo inspection of your vehicle [citation:4]

- Upload photos of odometer, VIN, and car condition [citation:4]

- Funds loaded to prepaid debit card or cash pickup [citation:4]

- No store visit required — fully remote process [citation:4]

- Real-time payment (RTP) technology enables instant funding, even on weekends [citation:4]

$500-55k

Loan amount range [citation:1]

300%+

Typical APR in unregulated states [citation:4]

91 days – 70 months

Repayment terms available [citation:1]

5.2%

Of Americans used title loans (2024) [citation:7]

📊 Real-World Example: The $1,000 Title Loan

Scenario: You need $1,000 for an emergency. Your car is worth $5,000. A title lender offers you $1,000 with a 25% monthly fee.

| Loan Amount | Monthly Fee | Total to Repay (30 days) | APR Equivalent |

|---|---|---|---|

| $1,000 | $250 | $1,250 | ~300% |

The rollover trap: If you can’t repay in 30 days, you “roll over” the loan — paying another $250 fee while still owing $1,000. After 4 months, you’ve paid $1,000 in fees and still owe the original $1,000 [citation:4].

🗺️ State Regulations Vary Dramatically (2026 Update)

| State | Regulation | Typical APR |

|---|---|---|

| Texas | High availability, but APRs can exceed 300% [citation:4] | 300%+ |

| California | Fair Access to Credit Act caps rates at ~36% for loans $2,500-$10,000 [citation:4] | ~36% |

| Credit Unions | Titled collateral loans from 4.99% APR [citation:2] | 4.99-5.99% |

📋 What You’ll Need (No Bank Account Version)

- Valid government ID — driver’s license or state ID

- Vehicle title in your name — must be lien-free (no existing loans) [citation:4]

- Proof of insurance — vehicle must be insured

- Vehicle registration — proving ownership

- Proof of income/ability to repay — may include benefits, alimony, or cash flow verification via bank statements (if you have an account) [citation:4]

- No credit check required — approval based on vehicle equity [citation:1]

📊 Income Verification in 2026 — What’s Changed

Due to the CFPB’s Personal Financial Data Rights Rule (Rule 1033), lenders now use “Open Banking” APIs to instantly verify your ability to repay via digital connections rather than asking for physical pay stubs [citation:4]. This allows unemployed individuals, freelancers, and gig workers to qualify using:

- Unemployment benefits deposits

- Social Security or disability payments

- Court-ordered alimony or child support

- Regular cash flow from gig work

Important: This still requires a bank account to show deposit history. If you’re completely unbanked, storefront lenders may still accept alternative proof like benefit award letters.

⚖️ Car Title Loans: Pros and Cons for Unbanked

✅ Pros

- Accessible without bank account (storefront cash) [citation:1]

- No credit check — approval based on car value [citation:1]

- Keep driving your car during loan term [citation:1]

- Same-day funding available [citation:1]

- Online options with virtual inspection [citation:4]

- Loan amounts up to $55,000 for high-value vehicles [citation:1]

❌ Cons

- Extremely high APRs (300%+ in unregulated states) [citation:4]

- Risk of repossession — lender can take your car without court order [citation:4]

- Some 2026 loans include “remote disablement” clauses (GPS shut-off) [citation:4]

- Auto repossessions at levels not seen since 2008 financial crisis [citation:3]

- Short repayment terms (often 30 days) [citation:7]

- Rollover trap leads to paying fees indefinitely [citation:4]

⚠️ THE REPOSSESSION CRISIS — 2026 WARNING

Auto repossessions are skyrocketing to levels not seen since the 2008 financial crisis [citation:3]. Senator Elizabeth Warren launched a probe into the auto lending industry in February 2026, citing concerns about wrongful repossessions and lack of consumer protection, especially with the CFPB sidelined [citation:3]. If you miss even one payment on a title loan, your car can be repossessed — often without warning.

🔍 How to Verify a Title Lender

- Check NMLS Consumer Access — nmlsconsumeraccess.org — verify they’re licensed in your state [citation:4]

- Unlisted lenders are likely offshore predators who don’t follow U.S. consumer protection laws [citation:4]

- Beware of “guaranteed approval” claims — legitimate lenders always disqualify applicants with bankruptcies or negative equity [citation:4]

- Avoid lead generators — if the site says “we connect you with lenders,” they’re selling your data

💡 When a Car Title Loan Might Be Your Only Option

- You have significant equity in your vehicle and need a larger loan amount

- You have exhausted all other options (pawn, employer, family, community programs)

- You have a clear, short-term repayment plan (e.g., money arriving in 2 weeks)

- You fully understand the risk of losing your vehicle

- You live in a state with rate caps (like California’s 36% limit) [citation:4]

If you do borrow: Borrow the absolute minimum. Calculate the total cost including fees. Have the repayment amount saved BEFORE you take the loan. Never roll over a title loan.

✅ Better Alternative: Credit Union Titled Collateral Loans

Credit unions offer titled collateral loans with APRs as low as 4.99% — a fraction of title loan costs [citation:2]. Requirements: you must become a credit union member, may need a bank account, and they’ll check credit. But if you can qualify, this is dramatically cheaper and safer than storefront title lenders.

–>

–>

🖼️ [Image placeholder: Title loan warning infographic — add later]

Option 4: Prepaid Debit Cards — A Bank Account Alternative for the Unbanked

Quick answer: Prepaid debit cards like Netspend let you manage money without a bank account — no credit check required . You load funds via direct deposit or cash at retail locations, then use the card anywhere Visa or Mastercard is accepted [citation:1]. However, fees can add up quickly: monthly fees up to $9.95, ATM withdrawals $2.95, and cash reloads up to $3.95 [citation:2]. About 41% of prepaid card users don’t have a checking account [citation:1].

💳 What Is a Prepaid Card?

A prepaid card looks like a debit card but isn’t linked to a bank account. You load money onto it first, then spend only what you’ve loaded [citation:1]. For the 5.6 million unbanked U.S. households, these cards provide a way to shop online, pay bills, and withdraw cash without a traditional bank account [citation:2].

41%

of prepaid users have no checking account

33%

have never used a credit card

130k+

reload locations nationwide [citation:6]

$9.95

max monthly fee [citation:2]

🔧 How Prepaid Cards Work (Step by Step)

Get the card

Order online (free) or buy at retailer (up to $9.95) [citation:2][citation:3]

Verify identity

Provide name, address, DOB, SSN (USA PATRIOT Act) [citation:9]

Load money

Direct deposit, cash at retailers, or bank transfer [citation:1]

Spend & reload

Use anywhere Visa/Mastercard accepted [citation:1]

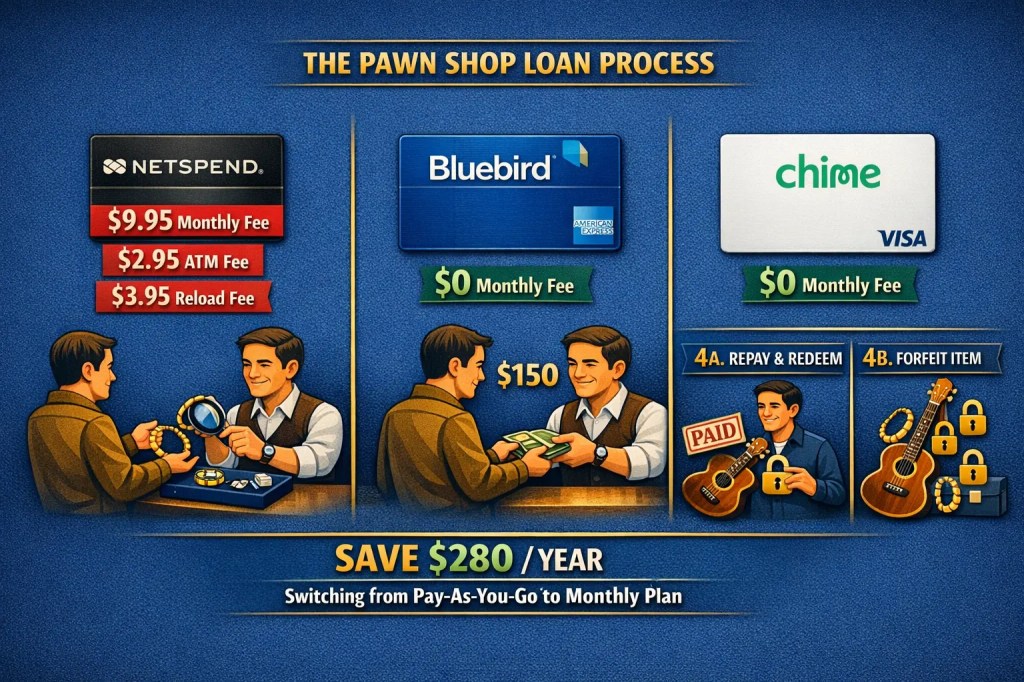

📌 NETSPEND DEEP DIVE — The Most Popular Option

Netspend is one of the largest prepaid card providers in the U.S., with over 130,000 reload locations [citation:6]. It’s designed specifically for unbanked and underbanked individuals who can’t qualify for traditional bank accounts [citation:2].

💰 Netspend Fee Breakdown (2026)

| Fee Type | Amount |

|---|---|

| Monthly fee (unlimited use) | $9.95 [citation:2] |

| Reduced monthly fee (with $500+ direct deposit) | $5.00 [citation:2][citation:9] |

| Pay-as-you-go (per purchase) | $1.50 – $2.00 per transaction [citation:2][citation:3] |

| ATM withdrawal | $2.95 + ATM owner fee [citation:2][citation:3] |

| Cash reload at retailer | Up to $3.95 [citation:2][citation:3] |

| Card purchase at retailer | Up to $9.95 [citation:2] |

| Inactivity fee (after 90 days) | $5.95/month [citation:3][citation:9] |

| Debit card transfer | 1.5% (min $2.95) [citation:3] |

| Foreign transaction | 4% [citation:3] |

📊 Real-World Example: The $1,000 Monthly Spending

Scenario: You use Netspend for everyday purchases, 15 transactions per month, plus 2 ATM withdrawals.

| Plan | Monthly Cost |

|---|---|

| Pay-as-you-go (15 × $1.50 + 2 × $2.95) | $28.40 |

| Monthly plan (with direct deposit) | $5.00 [citation:9] |

| Monthly plan (without direct deposit) | $9.95 |

Savings: Switching to monthly plan saves $23.40/month — that’s $280/year [citation:9].

✅ What Netspend Does Well

- No credit check — your credit score doesn’t matter [citation:9]

- FDIC insured — money is protected [citation:6]

- Get paid up to 2 days early with direct deposit [citation:6]

- Savings account option — up to 6% APY on first $2,000 [citation:3][citation:6]

- Overdraft protection (optional) — covers purchases up to $10 over balance without fees [citation:2][citation:6]

- 130,000+ reload locations — CVS, Walgreens, 7-Eleven [citation:6]

❌ What Netspend Does Poorly

- Fees add up quickly — can cost more than a bank account [citation:2][citation:3]

- Does NOT build credit — no reporting to credit bureaus [citation:3][citation:8]

- Poor customer service — negative reviews [citation:3]

- Inactivity fees — $5.95/month after 90 days [citation:3]

- No rewards — unlike some prepaid competitors [citation:3]

- Foreign transaction fees — 4% [citation:3]

⚖️ Prepaid Cards: Pros and Cons for Unbanked

✅ Pros

- No credit check [citation:1]

- No bank account required [citation:1]

- FDIC insured [citation:6]

- Direct deposit available [citation:2]

- Safer than carrying cash [citation:1]

- No risk of overdraft debt [citation:1]

- Widely accepted (Visa/Mastercard) [citation:1]

- Can help with budgeting [citation:1]

❌ Cons

- Monthly fees up to $9.95 [citation:2]

- ATM fees $2.95 + owner fee [citation:3]

- Reload fees up to $3.95 [citation:3]

- Inactivity fees [citation:3]

- Doesn’t build credit [citation:3]

- Foreign transaction fees [citation:3]

- No rewards [citation:3]

🔄 Better Alternatives to Netspend

| Option | Monthly Fee | Best For |

|---|---|---|

| Bluebird (Amex) | $0 [citation:9] | Fee-conscious shoppers |

| Chime | $0 [citation:9] | Transitioning to banking |

| Walmart MoneyCard | $5.94 | Walmart shoppers |

| Second-chance bank accounts | Varies | Building toward traditional banking [citation:9] |

✅ Better Long-Term Solution: Second-Chance Bank Accounts

Many banks offer “second chance” checking accounts specifically for people with poor banking history. Providers like Chime, Varo, and Wells Fargo offer accounts with lower fees than prepaid cards and a path to traditional banking [citation:2]. After 12 months of clean history, you may qualify for standard accounts and even secured credit cards that actually build your credit [citation:9].

🎯 The Bottom Line on Prepaid Cards

Prepaid cards work for unbanked individuals, but they’re expensive. The key is using them strategically: set up direct deposit to get the reduced $5 monthly fee, avoid ATM withdrawals by getting cash back at stores, and never leave a card inactive. But if your goal is to escape the unbanked cycle, focus on opening a second-chance bank account as soon as possible [citation:9].

–>

–>

🖼️ [Image placeholder: Prepaid card fee comparison — add later]

Pawn Shop Process

STEP 1: Bring item → STEP 2: Appraisal → STEP 3: Get cash →

STEP 4A: Repay & redeem item | STEP 4B: Don’t repay → lose item

Option 5: Employer Paycheck Advances — The Safest Way to Get Cash Before Payday

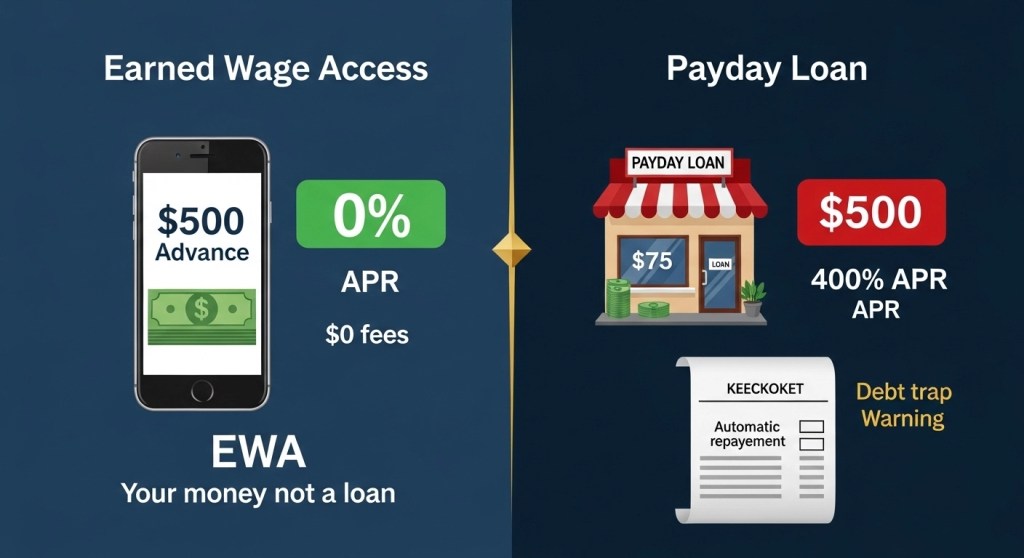

Quick answer: Employer paycheck advances, also called Earned Wage Access (EWA), let you access wages you’ve already earned before payday — often with no fees, no credit checks, and no interest . Over 7 million U.S. workers used EWA in 2022, accessing $22 billion . The CFPB clarified in 2026 that certain EWA products are not considered credit, meaning they avoid traditional lending regulations . This is the safest option for unbanked workers who have steady employment.

💰 What Is Earned Wage Access?

Earned Wage Access (EWA) is a financial tool that allows you to access a portion of your wages before your scheduled payday [citation:9]. It’s fundamentally different from a loan — you’re accessing money you’ve already earned, not borrowing against future income [citation:3]. This distinction matters because there’s no interest, no credit checks, and no debt collection if your paycheck is smaller than expected [citation:9].

7M+

U.S. workers used EWA in 2022 [citation:6]

$22B

In EWA transactions in 2022 [citation:6]

90%

increase in transactions year-over-year [citation:9]

60%

of Americans live paycheck to paycheck [citation:9]

🔧 How Earned Wage Access Works

Work your hours

Wages accumulate in real-time [citation:4]

Need cash before payday?

Open the EWA app and request withdrawal [citation:3]

Get funds instantly

Money transferred to your prepaid card or bank account [citation:4]

Automatic repayment

Deducted from your next paycheck [citation:4]

⚖️ MAJOR 2026 UPDATE: CFPB Clarifies EWA Is NOT Credit

In December 2025, the Consumer Financial Protection Bureau issued an advisory opinion stating that certain EWA products are not credit under Regulation Z [citation:1]. To qualify as “Covered EWA” and avoid credit regulations, providers must meet four criteria [citation:1]:

- Advances are limited to wages already earned and verified by payroll records

- Repayment occurs exclusively through employer’s payroll process (not direct bank withdrawals)

- Providers give clear notice they won’t pursue debt collection or credit reporting if payroll deductions are insufficient

- Providers don’t assess individual workers’ creditworthiness

Why this matters: This ruling gives regulatory certainty that EWA is fundamentally different from payday loans. However, it only applies to employer-integrated EWA — direct-to-consumer apps like EarnIn still operate in a gray area [citation:10].

📱 Two Ways to Access Earned Wages

🏢 Employer-Integrated EWA

- Offered through your employer as a benefit

- Integrated directly with payroll systems

- Examples: DailyPay, PayActiv, Even [citation:10]

- Pros: Covered by CFPB guidance, often lower fees

- Cons: Only available if your employer offers it

- Used by major employers like Walmart and McDonald’s [citation:6]

📲 Direct-to-Consumer EWA

- Apps you can download regardless of employer

- Verify income through bank transaction history [citation:3]

- Examples: EarnIn, MoneyLion Instacash, Dave, Brigit [citation:3]

- Pros: Available to anyone with qualifying income

- Cons: Regulatory gray area [citation:10], may push tips/fees

- Up to $750 between paydays (EarnIn) [citation:9]

📊 Popular EWA Apps Compared (2026)

| App | Employer Required? | Typical Fees | Max Advance | Bank Account Needed? |

|---|---|---|---|---|

| MoneyLion Instacash | No [citation:3] | $0 option available [citation:3] | Up to $500 [citation:3] | ✅ Yes |

| EarnIn | No [citation:3] | Optional tips [citation:9] | $750/pay period [citation:9] | ✅ Yes |

| DailyPay | Yes [citation:3] | $1.25-$2.99 [citation:3] | Varies by employer | ⚠️ Can use pay card |

| PayActiv | Yes [citation:3] | $5/month [citation:3] | Up to 50% earned wages | ⚠️ Can use pay card |

| Dave | No [citation:9] | Monthly subscription | Up to $500 | ✅ Yes |

💳 How Unbanked Workers Can Access EWA

If you don’t have a bank account, you’re not completely locked out of EWA. Some employer-integrated programs offer pay cards — prepaid cards where wages are loaded directly [citation:5].

- Pay cards work like debit cards but aren’t linked to a bank account [citation:5]

- Employers load wages onto the card each pay period [citation:5]

- You can withdraw cash at ATMs or get cash back at stores

- Funds are FDIC insured [citation:5]

- Employers must offer an alternative payment method (like paper check) if you don’t want the card [citation:5]

Warning: Some pay cards have ATM fees and transaction costs. Ask your employer about fee-free options [citation:5].

⚖️ EWA: Pros and Cons for Unbanked Workers

✅ Pros

- No interest, no credit checks [citation:9]

- Access wages you’ve already earned [citation:4]

- Optional pay cards for unbanked workers [citation:5]

- Can receive funds instantly [citation:4]

- 90% of users report improved quality of life [citation:7]

- Employer-integrated options have regulatory clarity [citation:1]

❌ Cons

- Risk of over-reliance — always playing catch-up [citation:9]

- Some apps push aggressive tipping/fees [citation:9]

- Direct-to-consumer apps still in regulatory gray area [citation:10]

- Requires smartphone and internet access

- Pay cards may have hidden fees [citation:5]

- Privacy concerns with bank account linking [citation:9]

💡 Using EWA Responsibly

The average employee using EWA withdraws only 10% of their monthly wages before payday [citation:6]. To avoid dependency:

- Reserve EWA for genuine emergencies — car repairs, medical bills [citation:3]

- Set personal withdrawal limits below the app’s maximum [citation:3]

- Track your usage — if you’re withdrawing every pay period, reassess your budget [citation:9]

- Use built-in budgeting tools to build long-term stability [citation:3]

🎯 The Bottom Line on Employer Advances

For unbanked workers with steady employment, employer-integrated EWA with a pay card is the safest emergency cash option available. It’s not a loan, there’s no interest, and you’re accessing money you’ve already earned. If your employer doesn’t offer it, ask them to consider it — major companies like Walmart and McDonald’s already do [citation:6]. For direct-to-consumer apps, you’ll need a bank account, but they remain a better alternative than payday loans.

–>

–>

🖼️ [Image placeholder: EWA vs Payday Loan comparison — add later]

Option 6: Check Cashing Stores — When You Need Cash Immediately

Quick answer: Check cashing stores let you cash payroll, government, and personal checks without a bank account — but fees can reach up to 10% of your check’s value [citation:2][citation:3]. The industry processed about $893 billion in 2022, projected to hit $1.6 trillion by 2027 [citation:1]. For a $1,800 paycheck, you could pay $50 in fees at a store, while Walmart charges only $8 for the same check [citation:3]. New apps like Alpha Cash are emerging to offer lower-cost alternatives for the unbanked [citation:2][citation:7].

💵 Understanding Check Cashing in 2026

For the 5.6 million unbanked U.S. households, check cashing stores are often the most visible option [citation:2]. But here’s the truth about this industry: it’s massive and expensive. The Consumer Financial Protection Bureau estimates that check-cashing businesses handled $893 billion in transactions in 2022, with projections reaching $1.6 trillion by 2027 [citation:1].

The reason? When you don’t have a bank account, cashing a paycheck often means standing in line at a storefront and paying fees that can reach 10% of your check’s value [citation:2][citation:3]. In Harris County, Texas, alone, nearly 600,000 residents face this reality — one in six adults [citation:2][citation:7].

$893B

Industry volume (2022) [citation:1]

$1.6T

Projected by 2027 [citation:1]

10%

Maximum fee at some stores [citation:2][citation:3]

5.6M

Unbanked households [citation:2]

💰 The Real Cost of Cashing a Check

📊 Real-World Example: $1,800 Biweekly Paycheck

| Location | Fee Structure | Total Cost |

|---|---|---|

| Check-cashing store | 2.5% + $5 flat fee [citation:3] | $50.00 |

| Walmart | $8 flat fee (checks over $1,000) [citation:1][citation:3] | $8.00 |

| Kroger (with Shopper’s Card) | Starting at $3 [citation:1] | $3.00-$8.00 |

| Issuing bank (non-customer) | $5-$8 flat fee [citation:1][citation:5] | $5.00-$8.00 |

The annual impact: Over 26 pay periods, that $50 per check adds up to $1,300 in fees — compared to just $208 at Walmart [citation:3].

🏦 Cashing at the Issuing Bank (Your Best Bet)

If you know which bank wrote the check, you can cash it there even without an account. Fees in 2026 are actually quite reasonable:

| Bank | Non-Customer Fee |

|---|---|

| Fidelity Bank (LA) | $5.00 [citation:5] |

| East West Bank | $5.00 (non-payroll checks) [citation:6] |

| United Community Bank | 1% (min $5.00) [citation:4] |

| Typical national banks | $6-$8 flat fee [citation:1] |

Pro tip: Call ahead. Some banks won’t cash checks for non-customers at all, and policies vary by location [citation:1].

🛒 Retail Check Cashing — Much Lower Fees

Major retailers offer check cashing at a fraction of storefront prices. This is the “hack” most unbanked borrowers don’t know about:

| Retailer | Fees | Limits |

|---|---|---|

| Walmart | $4 (up to $1,000) / $8 ($1,001-$5,000) [citation:1][citation:3] | Payroll, government, tax refunds [citation:1] |

| Kroger | Starting at $3 with Shopper’s Card [citation:1] | Payroll, government, insurance, business [citation:1] |

| Kmart | $1 or less [citation:1] | Up to $2,000 [citation:1] |

| Hannaford | Around $1 [citation:10] | Most stores offer service [citation:10] |

| Market Basket | $0.50 [citation:10] | Payroll and personal checks [citation:10] |

| Stop & Shop | $0.50 with GO Rewards [citation:10] | GO Rewards program required [citation:10] |

| Tops Friendly Markets | $1.00 [citation:10] | $500 limit [citation:10] |

Important: Most retailers won’t cash personal checks, and if they do, limits are strict (Walmart accepts two-party personal checks up to $200) [citation:1].

📱 NEW FOR 2026: Alpha Cash App

🚀 A Tech Solution for the Unbanked

Alpha Modus Financial Services just announced a new option through the Alpha Cash App — a platform designed to help consumers cash checks, move money, pay bills, and access prepaid debit services without the high fees of traditional check-cashing counters [citation:2][citation:7].

🎁 Limited Time Offer:

The first 500 eligible users get free check cashing services through June 30, 2026 [citation:2][citation:7].

Pre-registration is open at alphacash.ai [citation:7].

🏪 Stand-Alone Check-Cashing Stores

These are the places you see in strip malls with neon signs. They’re convenient — often open evenings and weekends — but they’re also the most expensive option:

- Average fees: 1.5% to 3% of check value plus $3-$10 flat fees [citation:3]

- Personal checks: Can cost up to 10% [citation:3]

- Industry size: Over 12,000 locations processing ~180 million transactions annually [citation:3]

Real talk: A 2023 FDIC survey found that three out of four unbanked households use check-cashing services to cash work, retirement, or government checks [citation:1]. But with better options available, you don’t have to be one of them.

💳 Prepaid Card Mobile Deposit

Many prepaid cards now let you deposit checks via mobile app — no bank account needed:

- NetSpend: Free standard processing (5-10 business days) or 2% fee (min $5) for expedited [citation:1]

- Brink’s Prepaid: Mobile check capture available [citation:1]

- Cash App: Check deposit up to $3,500 per check, $7,500/month [citation:1]

📋 What You Need to Cash a Check (No Bank Account)

- Valid government-issued photo ID — driver’s license, state ID, or passport [citation:1]

- The check itself — not endorsed until you’re at the counter [citation:1]

- Second form of ID — sometimes required at banks [citation:1]

- Shopper’s Card — for discounted fees at Kroger and affiliated stores [citation:1]

⚖️ Check Cashing Options: Pros and Cons

✅ Pros

- Immediate cash access

- No bank account required

- Widely available (12,000+ locations) [citation:3]

- Extended hours (evenings/weekends)

- Accepts checks others won’t [citation:3]

❌ Cons

- High fees (up to 10%) [citation:2]

- Can cost $1,300+/year [citation:3]

- Predatory practices common

- No credit building benefit

- Retailers have better rates — know where to go

🚨 3 Places to Avoid

- Stand-alone check-cashing stores — highest fees, often predatory [citation:1]

- Pawn shops (for check cashing) — not their primary business, rates may be worse

- Unlicensed online services — risk of fraud or data theft

🎯 The Bottom Line on Check Cashing

You don’t have to pay 10% to access your own money. If you need to cash a check without a bank account, go to the issuing bank first (flat fee $5-$8), then Walmart or a grocery store ($3-$8), and only as a last resort visit a check-cashing store. The difference can save you over $1,000 a year.

–>

–>

🖼️ [Image placeholder: Check cashing fee comparison — add later]

Option 7: Second-Chance Bank Accounts — Your Path Back to Mainstream Banking

Quick answer: Second-chance bank accounts are designed for people who’ve been denied traditional accounts due to past banking mistakes like unpaid fees, overdrafts, or bounced checks [citation:1][citation:2]. When you apply, banks check your ChexSystems report (not your credit score) [citation:7]. These accounts offer debit cards, mobile banking, and direct deposit [citation:2]. After 6-12 months of responsible use, you can typically upgrade to a standard account [citation:4].

📋 Why You’ve Been Denied — Understanding ChexSystems

When you apply for a bank account, most banks check your ChexSystems report, not your credit score [citation:1][citation:7]. ChexSystems is a consumer reporting agency that tracks:

- Unpaid negative balances from closed accounts

- Bounced checks and overdrafts

- Involuntary account closures

- Suspected fraud

Key fact: Negative information stays on your ChexSystems report for 5 years [citation:1][citation:2]. But you have the right to request one free report every 12 months [citation:7].

🔄 What Is a Second-Chance Bank Account?

Second-chance checking accounts are specifically designed for people who don’t qualify for traditional accounts due to negative banking history [citation:2]. They give you a fresh start by overlooking past mistakes [citation:1].

✅ What You Usually Get

- Debit card access

- Mobile banking and app

- Direct deposit (often with early access) [citation:3]

- ATM access

- Online bill pay

⚠️ Common Limitations

- Monthly fees ($5-$12) at some banks [citation:2]

- No check-writing allowed [citation:5]

- No overdraft — transactions declined [citation:2]

- Lower transaction limits

Good news: After 6-12 months of responsible account management, many banks let you upgrade to a standard checking account with fewer restrictions [citation:1][citation:4].

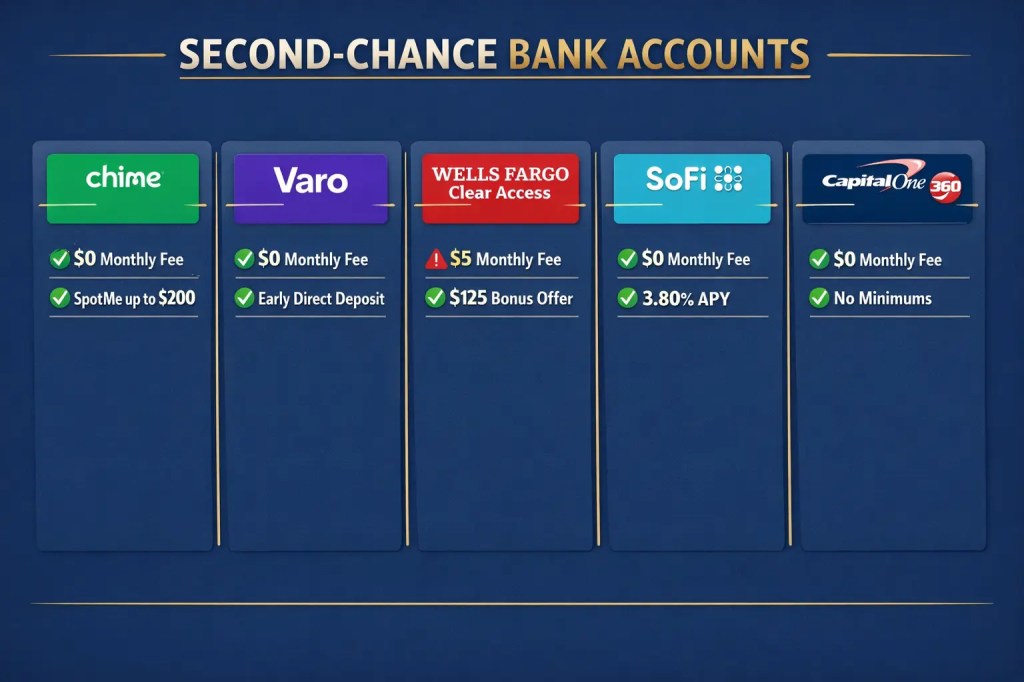

🏆 Best Second-Chance Bank Accounts (2026)

| Bank / Account | Monthly Fee | Minimum Deposit | Checks? | Notes |

|---|---|---|---|---|

| Chime® | $0 [citation:2] | $0 [citation:2] | No [citation:3] | No ChexSystems check; SpotMe overdraft up to $200 [citation:3]; get paid up to 2 days early [citation:3]; 47k+ fee-free ATMs [citation:1] |

| Varo Bank | $0 [citation:2] | $0 [citation:2] | No | No ChexSystems [citation:8]; early direct deposit; 40k+ Allpoint ATMs [citation:8]; savings tools [citation:8] |

| Wells Fargo Clear Access | $5 (waived for ages 13-24 or with $250+ monthly direct deposit) [citation:2][citation:5] | $25 [citation:2] | No (checkless) [citation:5] | Bank On certified [citation:5]; $125 bonus with qualifying transactions (offer ends 4/14/26) [citation:5]; no overdraft fees [citation:5] |

| SoFi Checking & Savings | $0 [citation:4] | $0 [citation:4] | Yes | Up to 3.80% APY with direct deposit [citation:4]; up to $300 bonus [citation:4]; 55k+ fee-free ATMs |

| Capital One 360 Checking | $0 [citation:4] | $0 | Yes | No ChexSystems; 70k+ fee-free ATMs; excellent mobile app |

| Experian Smart Money | $0 [citation:4] | $0 [citation:4] | No | Builds credit with bill payments [citation:4]; $50 direct deposit bonus [citation:4]; 55k+ fee-free ATMs |

| Dora Financial Everyday Checking | $0 [citation:4] | $0 [citation:4] | ? | Bank On certified [citation:4]; no credit check; early direct deposit; 30k surcharge-free ATMs |

| Woodforest Second Chance Checking | $9.95 (with direct deposit) / $11.95 (without) [citation:2] | $25 [citation:2] | ? | 17 states (mostly South/Midwest); must open in branch [citation:2] |

📋 How to Open a Second-Chance Account (Step by Step)

Get your ChexSystems report

Visit ChexSystems.com or call 800-428-9623 — free once/year [citation:7]

Dispute errors & pay old balances

Fix mistakes; negotiate “pay-for-delete” with original banks [citation:7]

Choose a bank

Chime, Varo, Wells Fargo, SoFi, etc. — compare fees [citation:2][citation:4]

Apply online

Need SSN and valid ID (driver’s license/passport) [citation:8]

Use responsibly for 6-12 months

Then upgrade to a standard account [citation:1][citation:4]

📈 Bonus: Build Credit While You Rebuild Banking History

Some second-chance providers include tools to help you build credit:

- Chime Credit Builder — Secured card with no credit check; average users increase FICO by 71 points in 3 months [citation:6]

- Experian Smart Money — Builds credit from everyday bill payments [citation:4]

- Chime Experian Boost integration — On-time payments reported to credit bureaus [citation:3]

⚖️ Second-Chance Accounts: Pros and Cons

✅ Pros

- Path back to mainstream banking [citation:6]

- FDIC insured (up to $250,000) [citation:3]

- Avoid check-cashing fees [citation:6]

- Early direct deposit available [citation:3]

- Debit card and mobile banking

- No credit check required [citation:1]

❌ Cons

- Monthly fees at some banks ($5-$12) [citation:2]

- No check-writing at many [citation:5]

- Limited services compared to standard accounts [citation:6]

- Doesn’t automatically build credit [citation:6]

🔄 Alternatives While You Wait

- Prepaid debit cards — Load money upfront; no bank account needed; fees $5-$10/month [citation:7]

- Money orders — Pay cash plus small fee; useful for rent and bills [citation:7]

- Credit union membership — Sometimes more flexible than big banks [citation:7]

These are short-term solutions — keep working toward a real bank account [citation:7].

🎯 The Bottom Line on Second-Chance Accounts

A second-chance bank account is the single best long-term solution for unbanked individuals. It gives you access to all the tools you need to manage money, avoid expensive check-cashing fees, and build a positive banking history. After 6-12 months of responsible use, you can upgrade to a standard account — unlocking better options, lower fees, and even credit-building tools.

–>

–>

🖼️ [Image placeholder: Second-chance bank comparison — add later]

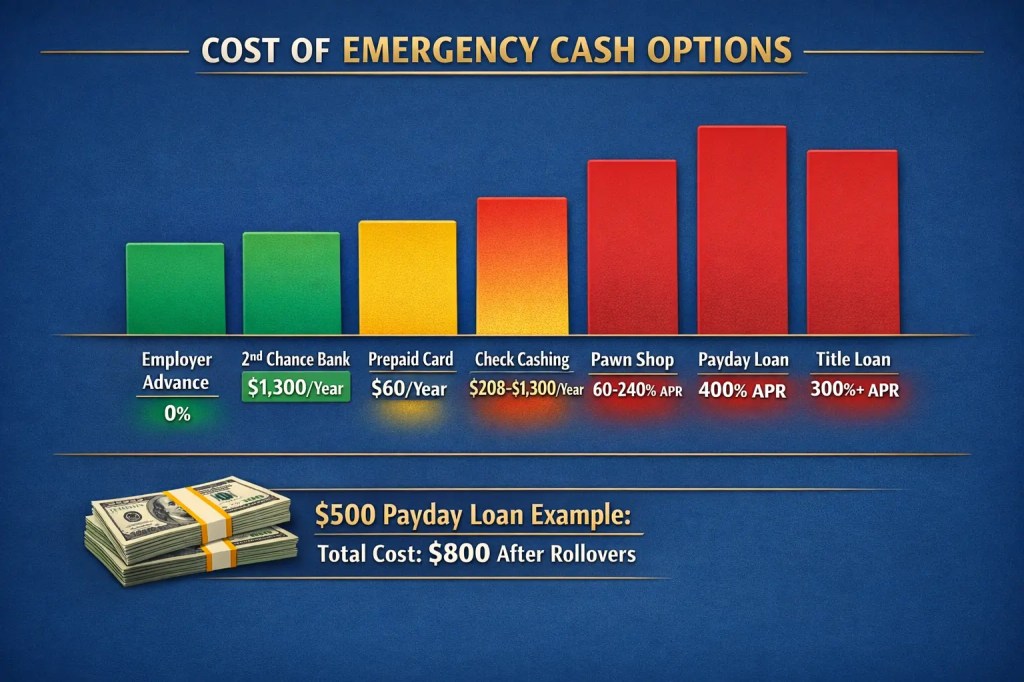

💰 Cost Comparison: Which Option Is Least Expensive?

Quick answer: Employer paycheck advances are the cheapest (often 0% APR), followed by second-chance bank accounts (once opened, they save you from check-cashing fees). Prepaid cards cost $5-$10/month. Pawn shops have 60-240% effective APR. Payday loans cost 400% APR, and title loans can exceed 300% APR. Check cashing fees can cost over $1,300/year if you use storefronts instead of retailers .

Here’s the reality check: the most accessible options are often the most expensive. This table shows you the true cost of each option, ranked from cheapest to most expensive.

| Option | Typical Cost | Repayment Term | Collateral? | Risk Level |

|---|---|---|---|---|

| ✅ Employer Advance (EWA) | 0% APR, often $0 fees | Next paycheck | ❌ No | Lowest |

| ✅ Second-Chance Bank Account | $0-$12/month (long-term savings) | N/A | ❌ No | Low (after opened) |

| ✅ Prepaid Cards (Netspend) | $5-$10/month + transaction fees | N/A | ❌ No | Low (but fees add up) |

| ⚠️ Check Cashing (Retailer) | $3-$8 per check | Instant | ❌ No | Medium (can cost $208/year) |

| ⚠️ Check Cashing (Storefront) | Up to 10% of check value | Instant | ❌ No | High ($1,300+/year) |

| 🚨 Pawn Shop Loan | 60-240% effective APR | 30-60 days | ✅ Your item | High (lose item) |

| 🚨 Payday Loan | $15-$30/$100 (391-780% APR) | 2-4 weeks | ❌ No | Very High (debt trap) |

| 🚨 Car Title Loan | 300%+ APR typical | 30 days | ✅ Your car | Severe (lose vehicle) |

📊 The Annual Cost of Being Unbanked

💵 Check Cashing

$1,800 paycheck × 26x/year

Storefront: $1,300/year

Walmart: $208/year

Save $1,092/year

💳 Prepaid Cards

Pay-as-you-go vs monthly plan

Pay-as-you-go: $28.40/month = $341/year

Monthly plan: $5/month = $60/year

Save $281/year

⚠️ Payday Loan Trap

$500 loan × 4 rollovers

Fees paid: $300

Still owe: $500

Total: $800 for $500 loan

🎯 Which Option Is Right for YOU?

✅ Best for Short-Term Emergencies

- Employer advance — 0% APR, instant

- Pawn shop — if you have valuables and can repay quickly

- Retailer check cashing — $3-$8 fee

📈 Best Long-Term Solution

- Second-chance bank account — path back to mainstream banking

- Prepaid card — temporary while you work on bank account

🚨 Avoid If Possible

- Payday loans — 400% APR trap

- Title loans — risk losing your car

- Storefront check cashing — $1,300/year in fees

🎯 The Bottom Line on Costs

The cheapest option is always the one you don’t have to pay back with interest. Employer advances cost $0. Second-chance accounts save you from check-cashing fees. Prepaid cards cost $60/year if used wisely. Everything else gets expensive fast — payday and title loans are financial emergencies you don’t want to create while solving one.

–>

–>

🖼️ [Image placeholder: Cost comparison infographic — add later]

Word-for-Word Scripts: What to Say at Pawn Shops, Payday Lenders, and Banks

Quick answer: Having the right words ready can save you money and protect your rights. Use these scripts to ask about fees, understand loan terms, and avoid predatory traps. Always ask for total cost in dollars, not just percentages. Get everything in writing before you sign. If something feels wrong, walk away — there’s always another option.

Knowing your rights is one thing. Knowing exactly what to say when you’re standing at a counter is another. These scripts give you the words — just fill in the blanks and speak calmly.

🏪 Script 1: At the Pawn Shop

“Hi, I’d like to pawn this [item]. Can you tell me:

1. How much will you lend me for it?

2. What’s the total fee in dollars if I repay in 30 days?

3. Can I pay just the fee to extend the loan?

4. What happens if I’m late? Is there a grace period?”

Why this works: Gets you the total dollar cost, not confusing percentages. Reveals rollover policy before you’re trapped.

💰 Script 2: At a Payday Lender (Cash Pickup)

“I need cash but I don’t have a bank account. I understand you offer cash pickup.

Before I apply, please tell me in writing:

1. The exact dollar amount I’ll receive today.

2. The total dollar amount I must repay, including all fees.

3. The due date — and what happens if I can’t pay on that exact date.

4. Can I repay in cash at this location, or do I need a money order?”

Why this works: Forces them to show total cost in dollars (not just percentages) and reveals repayment logistics.

🚗 Script 3: At a Title Loan Store

“I’m considering a title loan on my [year/make/model]. Before we go further:

1. How much will you lend me based on my car’s value?

2. What’s the total fee in dollars for a 30-day loan?

3. Does my car have any GPS or remote disablement device?

4. If I miss a payment, how many days before you repossess my car?

5. Can I see the repossession terms in the contract right now?”

Why this works: 2026 title loans often include GPS tracking and remote disablement — you need to know before signing.

🛒 Script 4: At Walmart or Grocery Store (Check Cashing)

“I’d like to cash this [payroll/government] check. I don’t have a bank account.

What’s your fee for checks over $1,000? Is it a flat fee or percentage?”

Why this works: Walmart charges $8 flat for checks over $1,000 — much cheaper than percentage-based storefronts.

🏦 Script 5: Opening a Second-Chance Bank Account

“I’d like to apply for a second-chance checking account. I may have some negative marks on my ChexSystems report from the past.

Can you tell me:

1. What’s the monthly fee and how can I waive it?

2. After how many months of good standing can I upgrade to a regular account?

3. Does this account help me build credit or qualify for a secured credit card later?”

Why this works: Shows you know about ChexSystems and are planning for the future — banks appreciate transparency.

👔 Script 6: Asking Your Employer About Paycheck Advances

“I’m facing a short-term emergency and was wondering if [Company Name] offers any earned wage access or paycheck advance programs.

I’ve heard about services like DailyPay or PayActiv. Is that something available to employees?

If not, is there a payroll advance option I could request?”

Why this works: Shows you’ve done research and know what to ask for — not just “can I have money?”

💎 Script 7: Negotiating a Better Pawn Shop Deal

“I appreciate the offer of $[amount]. I’ve checked online and similar items are selling for $[higher amount].

Would you consider $[your counter-offer]? This is a quality [brand/model] in excellent condition.”

Why this works: Pawn shops expect negotiation — doing research beforehand gives you leverage.

📋 Before You Go:

- Write down the questions — it’s okay to read them

- Take a friend — two sets of ears are better than one

- Get everything in writing — don’t accept verbal promises

- Walk away if uncomfortable — there’s always another pawn shop, another lender, another option

- Count your cash before leaving — verify the amount matches what you agreed to

–>

–>

🖼️ [Image placeholder: Phone script visual — add later]

Frequently Asked Questions

Can a bank charge fees on a “free” checking account?

If an account is advertised as “free” or “no cost,” it cannot have monthly service fees, transaction fees, or fees for not meeting a minimum balance. However, “free” accounts may still charge ATM fees, overdraft fees, bounced check fees, and dormant account fees. Always read the fee schedule before opening an account [citation:1].

What protections exist for car title loan borrowers?

State laws provide important protections. For example, Virginia law requires title loan proceeds to be disbursed in cash or by business check — no fees for cashing the check. Lenders cannot accept car keys as collateral, cannot draft funds electronically without written authorization, and must stop electronic drafts upon request. They also cannot threaten criminal proceedings for non-payment [citation:4].

Are prepaid cards protected against fraud or unauthorized use?

Unlike credit and debit cards, general purpose reloadable (GPR) prepaid cards historically lacked federal fraud liability limits. The FTC has advocated for extending these protections, noting that consumers face significant risk of loss from unauthorized use. Some prepaid cards now offer voluntary protections, but coverage varies. Always check your cardholder agreement [citation:8].

Can payday lenders bypass state interest rate caps by partnering with banks?

A 2020 Trump administration rule allowed lenders to partner with federally regulated banks to potentially avoid state interest rate caps through “rent-a-bank” schemes. California, Illinois, and New York sued, arguing this undermines state consumer protections like California’s 36% APR cap. The legal battle continues — check your state’s current enforcement status [citation:3].

Are there any 2026 updates to payday lending laws?

Yes. Michigan House Bills 5544-5550, introduced February 2026, propose modernizing the state’s financial services framework, including updating the Deferred Presentment Services Transactions Act (payday lending). The changes would strengthen licensing, net worth, bonding, and enforcement standards, effective January 1, 2026 [citation:9]. Always check your state’s latest legislation.

Where can I report problems with a prepaid card, payday lender, or check casher?

You can file complaints with the Consumer Financial Protection Bureau (CFPB) for most financial products and services. The Federal Trade Commission (FTC) handles deceptive or unfair business practices. For state-licensed lenders, contact your state attorney general’s office or state banking regulator. Keep all receipts, contracts, and records of your interactions [citation:1][citation:8].

What fees can still be charged on a “free” checking account?

Even “free” accounts can charge certain fees: ATM withdrawal fees (if you use another bank’s ATM), overdraft fees, returned check fees, stop payment fees, and dormant account fees. These are not considered monthly service fees, so they’re allowed. Always ask for a complete fee schedule [citation:1].

Where can I find in-depth legal information about consumer credit?

The National Consumer Law Center (NCLC) publishes comprehensive guides on payday lending, title loans, credit cards, and prepaid cards. Titles include “Consumer Credit Regulation” (2025) and “Consumer Banking and Payments Law” (2024). These resources are used by attorneys and advocates nationwide [citation:7].

⚠ For educational purposes only. Not legal advice. Laws regarding check cashing, payday lending, title loans, and prepaid cards vary significantly by state and change frequently. If you’re facing legal action or financial hardship, consult a qualified consumer rights attorney or nonprofit credit counselor.

Unbanked Emergency Cash Toolkit

Your complete guide to getting cash without a bank account — printable 7-step checklist:

📋 Your PDF includes:

- 7 Options Comparison Table — costs, risks, and requirements side-by-side

- Word-for-Word Scripts — exactly what to say at pawn shops, payday lenders, and banks

- Fee Calculator — compare check cashing costs: storefront vs Walmart vs grocery store

- Title Loan Warning Signs — 5 red flags to watch for before signing

- Second-Chance Bank Account Guide — step-by-step how to open one

- State-by-State Legality Quick Reference — where payday/title loans are banned

Free · No sign-up required · ConfidenceBuildings.com · Pairs with Episode 16

PDF includes checklists, scripts, and comparison tables

🔬 Research Note & Primary Sources

This article is part of the Borrower’s Truth Series, a 30-day educational series by Laxmi Hegde, MBA in Finance. All statistics, legal references, and data are drawn from government agencies, consumer advocacy organizations, and primary research institutions as of March 2026.

Primary Sources:

- Consumer Financial Protection Bureau (CFPB) — Check cashing industry data ($893B in 2022, projected $1.6T by 2027), “free” account fee rules, complaint database

- Federal Trade Commission (FTC) — Prepaid card consumer protections, fraud reporting, enforcement actions

- FDIC / Alpha Cash — Unbanked statistics: 5.6 million households, 600,000 in Harris County, TX, 10% check cashing fees

- National Consumer Law Center (NCLC) — Payday lending, title loans, prepaid card research

- Virginia Law § 6.2-2215 — Car title loan protections (cash disbursement, no key holding, electronic draft restrictions)

- Michigan Legislature HB 5544-5550 — 2026 payday lending modernization updates

- Courthouse News Service / OCC — “Rent-a-bank” schemes and state rate cap preemption lawsuits

- National Conference of State Legislatures (NCSL) — State payday lending laws and rate caps

📊 Unbanked Crisis — Key Statistics (2026):

- 5.6 million U.S. households are unbanked

- 600,000 residents in Harris County, TX alone (1 in 6 adults)

- 10% typical check cashing fee at storefronts

- $893 billion check cashing industry volume (2022), projected $1.6 trillion by 2027

- 41% of prepaid card users have no checking account

💰 Fee Comparison Sources:

- Storefront check cashing: 2.5% + $5 fee = $50 on $1,800 paycheck

- Walmart: $8 flat fee for checks over $1,000

- Issuing banks: $5-$8 flat fee for non-customers

- Grocery stores: Kroger ($3), Hannaford ($1), Market Basket ($0.50), Stop & Shop ($0.50 with rewards)

- Prepaid cards: Netspend monthly $9.95, pay-as-you-go $1.50-$2.00 per transaction

🏦 Second-Chance Bank Account Sources:

- Chime: $0 monthly fee, SpotMe up to $200, no ChexSystems check

- Varo: $0 monthly fee, early direct deposit, no ChexSystems

- Wells Fargo Clear Access: $5 monthly fee (waived for ages 13-24 or with $250+ direct deposit), $125 bonus

- SoFi: $0 monthly fee, up to 3.80% APY with direct deposit

- Capital One 360: $0 monthly fee, no minimums, no ChexSystems

⚠️ Payday & Title Loan Sources:

- Payday loan fees: $15-$30 per $100 borrowed = 391-780% APR

- Title loan APRs: 300%+ typical in unregulated states

- Remote disablement: Some 2026 title loans include GPS tracking and engine shut-off

- Illegal states: 13 states + DC ban payday lending entirely

For the complete Borrower’s Truth Series guide, visit: The Complete Borrower’s Truth Guide → ConfidenceBuildings.com

← Previous · Episode 15

Can Payday Lenders Sue You? (And Other Threats They Use to Scare You)

Published March 16, 2026

Next · Episode 17 →

Loan Contract Fine Print: 7 Clauses Lenders Hope You Never Find

Coming March 18, 2026

📚 Emergency Borrowing Blueprint 2026 — 16 of 30 Episodes Complete

All episodes available at Emergency Borrowing Blueprint 2026

🔔 Bookmark the series or check back daily — new episodes every morning

📅 Published March 17, 2026 · Updated as part of the ConfidenceBuildings.com 2026 Consumer Finance Research Project.

This post is Episode 16 of 30 in the Borrower’s Truth Series, examining emergency borrowing, predatory lending practices, and consumer financial rights. This episode focuses specifically on emergency cash options for the 5.6 million unbanked U.S. households who cannot access traditional banking services or cash advance apps.

Research methodology: Information compiled from primary sources including the Consumer Financial Protection Bureau (CFPB), Federal Trade Commission (FTC), FDIC, National Consumer Law Center (NCLC), state legislative databases, and direct provider research. Check cashing fee data from AmeriSave 2026, prepaid card data from U.S. News and Bankrate, second-chance bank account details from Chime, Varo, Wells Fargo, SoFi, and Capital One as of March 2026.

📌 2026 Updates Included:

- Michigan House Bills 5544-5550 — payday lending modernization (introduced Feb 2026)

- Virginia title loan protections under § 6.2-2215

- Remote disablement and GPS tracking in title loans

- Alpha Cash App promotion for free check cashing (first 500 users through June 2026)

- Wells Fargo $125 bonus offer (expires April 14, 2026)

- SoFi up to 3.80% APY with direct deposit

⚖️ For educational purposes only. Not financial or legal advice. Laws vary by state and change frequently. Fees, interest rates, and availability of the options described vary significantly by state, lender, and individual circumstances. Always verify current terms directly with the provider before making any financial decision. If you are in a debt cycle, consult a nonprofit credit counselor through the National Foundation for Credit Counseling (NFCC.org).

© 2026 ConfidenceBuildings.com · Borrower’s Truth Series · Laxmi Hegde, MBA in Finance