Emergency Borrowing Blueprint 2026 — Your Progress

Episode 20 of 30 · 67% Complete · Week 4: After You Borrow

This guide is provided for general educational and informational purposes only and does not constitute financial, legal, or professional advice. Nonprofit credit counseling services, fees, and eligibility vary by agency and state. Always verify details directly with the organization before enrolling. This content is based on publicly available information and U.S. market conditions as of March 2026. The publisher is not responsible for any outcomes resulting from actions taken based on this information.

Choose nonprofit credit counseling if:

You have more than $5,000 in unsecured debt, feel overwhelmed trying to organize payments, or want a structured Debt Management Plan (DMP).

Choose a paid budgeting tool if:

You need to build a daily budget, track expenses, or prefer a digital app. This is for prevention and organization.

Avoid any company that:

Asks for upfront fees, guarantees debt settlement, or tells you to stop paying your creditors.

Nonprofit Credit Counseling — The Gold Standard

If you are in a debt cycle, this is where you should start.

What Is a Nonprofit Credit Counseling Agency?

A nonprofit credit counseling agency is an organization, typically a 501(c)(3), whose mission is to help consumers manage their debt and finances. They are accredited by national organizations that ensure they meet standards of quality and ethics. They do not exist to sell you a product—they exist to help you build a plan.

⚠️ Important: They are not debt settlement companies. Debt settlement companies tell you to stop paying creditors in hopes of negotiating a lower payoff later—a process that can destroy your credit and lead to lawsuits. Credit counseling agencies help you pay what you owe in a manageable way.

The Two National Nonprofits You Can Trust: NFCC & FCAA

There are two national, trusted organizations that accredit and oversee most legitimate nonprofit credit counseling agencies in the U.S.

National Foundation for Credit Counseling

The oldest and largest network of nonprofit credit counselors in the U.S. A great first stop for anyone looking for a reputable, vetted counselor.

Financial Counseling Association of America

A national association of high-quality, nonprofit credit counseling agencies. FCAA members often specialize in Debt Management Plans.

🚩 THE RULE:

If a credit counseling agency is not accredited by the NFCC or FCAA, you are in the for-profit, potentially predatory zone. Walk away.

What They Do (And Don’t Do)

✅ What a Nonprofit Credit Counselor Does:

- Reviews your entire financial picture

- Creates a personalized budget

- Sets up a Debt Management Plan (DMP)

- Lowers interest rates (sometimes to 0–10%)

- Waives late and over-limit fees

- Consolidates payments into one monthly amount

- Stops collection calls on accounts in the plan

❌ What They Do NOT Do:

- Make your debt “disappear”

- Lend you money

- Charge large upfront fees

- Guarantee debt settlement

- Tell you to stop paying creditors

Pros, Cons & Cost

✅ Pros

- Trustworthy & accredited

- Structured path out of debt

- Lowers interest & fees

- Stops collection calls

⚠️ Cons

- Can take 3–5 years

- Requires monthly commitment

- Accounts in DMP are closed

- Temporary credit impact

💰 Typical Cost

- Setup fee: $0–$50 (often waived)

- Monthly fee: $20–$50

- Many agencies waive fees for hardship

*Fees vary by agency. Always ask about fee waivers if you cannot afford them.

Start Here — Free Nonprofit Help

If you’re struggling with debt, start with nonprofit credit counseling. These organizations are accredited, trusted, and exist to help — not to sell you something.

📞 National Foundation for Credit Counseling (NFCC)

🌐 nfcc.org | 📞 (800) 388-2227

The largest network of nonprofit credit counselors. Free initial session.

📞 Financial Counseling Association of America (FCAA)

🌐 fcaa.org | 📞 (866) 694-3228

High-quality nonprofit agencies specializing in Debt Management Plans.

✅ What they can do for you: Review finances, create a debt plan, negotiate lower interest rates, stop collection calls. Most initial sessions are free.

📋 What Is a Debt Management Plan (DMP)?

A Debt Management Plan is the core service most nonprofit credit counseling agencies offer. If you enroll in a DMP, here’s exactly what happens:

You make one payment to the counseling agency each month.

Agency distributes payments to your creditors.

Creditors often lower interest rates (sometimes to 0–10%).

You become debt-free in 3–5 years with a clear finish line.

💡 Important: Accounts in a DMP are typically closed, which may temporarily impact your credit score. However, this is far less damaging than missed payments, charge-offs, or collections—and the long-term benefit of becoming debt-free outweighs the short-term dip.

Paid Options — For Prevention & Organization

If you don’t need a structured DMP but want help with budgeting, tracking, and building a buffer.

Nonprofit counseling is a service—a human interaction that helps you build a plan. Paid budgeting apps are tools—they help you execute and maintain that plan day-to-day. They are excellent for preventing future debt by helping you build a buffer and track your spending.

⚠️ Important: The tools below are vetted, reputable platforms with transparent pricing. Avoid any budgeting app that asks for large upfront fees or promises to “erase debt.”

Vetted Paid Tools (With Transparent Pricing)

You Need A Budget (YNAB)

⭐ Best for: Breaking the paycheck-to-paycheck cycle

YNAB’s philosophy is to “give every dollar a job.” It helps you assign money you have to categories, build a buffer, and plan for true expenses (like car repairs) so they don’t become emergencies.

Pricing: $14.99/month or $99/year (free 34-day trial)

Quicken Simplifi

⭐ Best for: Comprehensive cash flow & spending overview

Focuses on your cash flow, helping you track spending, create a “Spending Plan,” and monitor net worth. Great for people who want all their accounts in one dashboard.

Pricing: $3.99/month

Tiller Money

⭐ Best for: Spreadsheet lovers who want ultimate control

Automatically feeds your daily transactions into Google Sheets or Excel. You control how it’s categorized, analyzed, and tracked. Perfect for people who want to build their own custom system.

Pricing: $79/year (free 30-day trial)

Free Nonprofit vs. Paid Tools — Which One Is Right for You?

| Feature | Nonprofit Credit Counseling | Paid Budgeting Tools |

|---|---|---|

| Best for | Active debt, overwhelmed, need a structured plan | Budgeting, tracking, prevention, organization |

| Cost | Free or low-cost ($0–$50 setup, $20–$50/month) | $4–$15/month or $79–$99/year |

| Human support | ✅ Yes — certified counselor | ❌ No — self-directed (chat/email support only) |

| Negotiates with creditors | ✅ Yes — lowers rates, waives fees | ❌ No |

| Stops collection calls | ✅ Yes (accounts in DMP) | ❌ No |

| Credit impact | Accounts closed — temporary dip, then recovery | No direct impact — helps you build habits |

Not sure which path is right for you?

Use the simple framework below to make your decision in under 60 seconds.

Want Faster or Online Help?

If you need immediate action, fully online tools, or faster onboarding, here are vetted alternatives:

You Need A Budget (YNAB)

⭐ Best for: Breaking the paycheck-to-paycheck cycle

“Give every dollar a job.” Build a buffer, plan for true expenses, and prevent future debt.

💰 $14.99/mo or $99/yr | 34-day free trial

Try YNAB →Quicken Simplifi

⭐ Best for: Cash flow overview

Track spending, create a “Spending Plan,” and monitor net worth in one dashboard.

💰 $3.99/mo | 30-day free trial

Try Simplifi →Tiller Money

⭐ Best for: Spreadsheet power users

Auto-feed transactions into Google Sheets or Excel. Full control, full customization.

💰 $79/yr | 30-day free trial

Try Tiller →📊 At a Glance: Which Option Is Right for You?

| Service Type | Cost | Best For |

|---|---|---|

| NFCC / FCAA | Free initial session | Trusted nonprofit help, human guidance, debt negotiation |

| YNAB | $14.99/mo or $99/yr | Breaking the paycheck-to-paycheck cycle, proactive budgeting |

| Quicken Simplifi | $3.99/mo | Cash flow overview, spending plan |

| Tiller Money | $79/yr | Spreadsheet control, full customization |

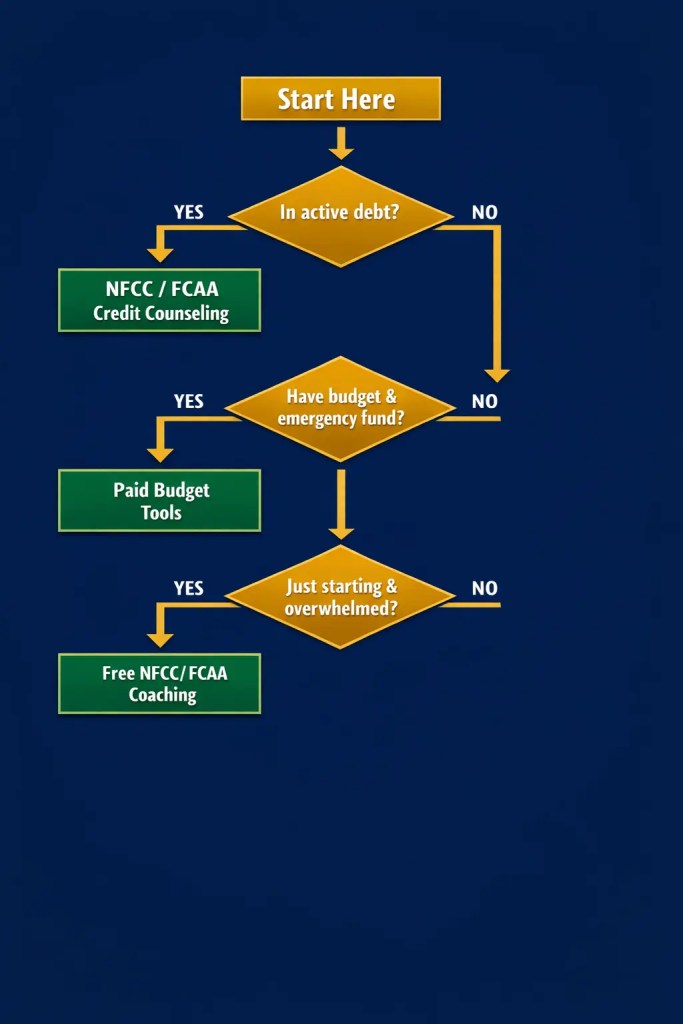

The Credit Counseling Decision Framework

Use this simple flow to determine your next step in under 60 seconds.

Are you in active debt?

(e.g., high-interest credit cards, collection calls, struggling to make minimum payments)

✅ YES →

Start with nonprofit NFCC or FCAA credit counseling. This is your first and most important step. They can help you assess if a Debt Management Plan is right for you.

❌ NO →

Proceed to Question 2.

Do you have a budget and emergency fund, but want better tools?

✅ YES →

A paid budgeting tool (like YNAB, Quicken, or Tiller) is a great fit. These tools are for people who are managing their finances but want to optimize and prevent future debt.

❌ NO →

Proceed to Question 3.

Are you just starting, feeling overwhelmed, and have no clear sense of your monthly income and expenses?

✅ YES →

Start with the free resources from a nonprofit credit counseling agency. Many offer free budget coaching, even if you don’t need a DMP. You need human guidance first, the digital tool second.

🤔 NOT SURE →

Start with a free NFCC or FCAA counseling session. It costs nothing to talk to a certified counselor who can help you figure out your next step.

FAQ: What You Actually Need to Know

Q: Is credit counseling bad for my credit?

A: A Debt Management Plan (DMP) will close the credit accounts you include, which can initially lower your score. However, it also prevents future late payments, collections, and charge-offs—which are much more damaging. Over time, as you consistently pay down your debt, your score will recover. It’s a short-term impact for a long-term gain.

📌 Source: NFCC · CFPB

Q: Can a credit counselor help me with student loans?

A: Yes, but differently. Most NFCC agencies have certified student loan counselors who can help you navigate repayment plans, forbearance, consolidation options, and Public Service Loan Forgiveness (PSLF)—all without a DMP. It’s typically a free service.

📌 Source: NFCC Student Loan Counseling

Q: How much does it cost to work with the NFCC?

A: The initial counseling session is almost always free. If you enroll in a DMP, the setup fee is typically $0–$50, and the monthly fee is $20–$50. Many agencies waive fees for clients who demonstrate financial hardship. Always ask about fee waivers.

📌 Source: NFCC · FCAA

Q: What’s the difference between credit counseling and debt settlement?

A: This is the most important distinction. Credit counseling helps you repay your full debt with lower interest rates. Debt settlement companies tell you to stop paying your creditors so they can try to negotiate a lower payoff later—a process that often leads to lawsuits, ruined credit, and upfront fees. The FTC has taken action against many debt settlement companies. Avoid them.

📌 Source: FTC · CFPB

Q: I found a company that says they can “erase my debt for pennies on the dollar.” Should I use them?

A: No. If a company promises to erase debt, asks for upfront fees, or tells you to stop paying your creditors—run. These are hallmarks of predatory debt settlement scams. Start with an NFCC or FCAA agency for a free, honest assessment. Legitimate help does not require upfront payment.

📌 Source: FTC Telemarketing Sales Rule · CFPB

Q: Can I get credit counseling if I have no money to pay?

A: Yes. Most NFCC and FCAA agencies offer the initial counseling session for free. If you enroll in a DMP but cannot afford the monthly fee, ask about hardship waivers. Many agencies have scholarships or sliding-scale fees based on income. Don’t let cost stop you from calling.

📌 Source: NFCC · FCAA

Ready to Take Action?

We’ve created a free toolkit to help you prepare for your first credit counseling session and rebuild your credit.

🤔 Who Should Use Which Option?

✅ Use Nonprofit Counseling If:

- You’re overwhelmed with debt

- You want free, trusted guidance

- You don’t want to pay upfront fees

- You need help negotiating with creditors

⚡ Use Paid Tools If:

- You’re already stable but want to optimize

- You prefer digital tools over phone calls

- You want to build a buffer and prevent future debt

- You’re ready to invest in your financial systems

Free · No sign-up required

The 90-Day Credit Rebuilding Toolkit

Your complete printable guide to preparing for credit counseling and rebuilding your credit. Includes:

*No email required. Instant download. ConfidenceBuildings.com

Final Thoughts: The Path Forward

The difference between struggling with debt and successfully managing it is rarely about willpower. It’s about having the right information and the right support at the right time.

Nonprofit credit counseling exists for exactly the situation you’re in right now. The counselors at NFCC and FCAA agencies have helped millions of people build structured plans to pay off debt, lower interest rates, and stop collection calls. They are not there to judge you. They are there to help you.

If you’re not ready for a DMP, paid budgeting tools like YNAB, Quicken, or Tiller can help you build the habits that prevent future debt. Start with the 34-day free trial. See if it clicks. The investment is small compared to the cost of another year of financial stress.

“The best time to get help was six months ago. The second best time is today.”

— Laxmi Hegde, MBA in Finance

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“One of the most common misconceptions I see is that credit counseling and debt settlement are the same thing. They are not. A nonprofit credit counselor works for you. A debt settlement company works for its own profit—often taking your money while your credit is destroyed. Before you sign anything with any company, ask one question: ‘Are you accredited by the NFCC or FCAA?’ If the answer is no, walk away. Your financial recovery is too important to risk on companies that charge upfront fees for services you can get for free.”

Legal Context: Under the FTC Telemarketing Sales Rule, it is illegal for debt relief companies to charge upfront fees before settling your debt. If a company asks for money before they’ve done anything—run. Nonprofit NFCC/FCAA agencies comply with all federal consumer protection laws. Always verify credentials before sharing personal information.

Bottom Line: Free, accredited help exists. Use it first. Paid tools are for maintenance, not crisis. If a company pressures you, charges upfront, or promises to “erase debt”—that’s your signal to call an NFCC counselor instead.

📚 Quick Resource Directory

Written by

Laxmi Hegde, MBA in Finance

Founder, ConfidenceBuildings.com

📘 Part of the Emergency Borrowing Blueprint 2026

Episode 20 of 30 · Week 4: After You Borrow

Updated March 2026 · Next episode: How to Negotiate With Creditors

⚠ For educational purposes only. Not financial or legal advice. The information in this post is current as of March 2026. Nonprofit credit counseling services, fees, and eligibility vary by agency and state. Always verify details directly with the organization. If you are facing identity theft, fraud, or complex credit issues, consult a qualified consumer rights attorney or nonprofit credit counselor. Free credit reports available at AnnualCreditReport.com.

© 2026 ConfidenceBuildings.com · Emergency Borrowing Blueprint 2026 · Laxmi Hegde, MBA in Finance

Ready to Go Deeper?

This guide gives you the foundation. The Borrower’s Truth ebook takes you step-by-step through every strategy in detail — with real scripts, legal protections, and a complete 12-month financial recovery plan.

⚠️ Before choosing any paid service, read the full Borrower’s Truth Guide for free.

🔬 Research Note & Primary Sources

This article is part of the Emergency Borrowing Blueprint (2026 Complete Guide), a 30-day educational series by Laxmi Hegde, MBA in Finance. All statistics, legal references, and data are drawn from government agencies, nonprofit organizations, and primary research institutions as of March 2026.

Primary Sources:

- National Foundation for Credit Counseling (NFCC) — The largest and oldest network of nonprofit credit counselors in the U.S., accrediting agencies that meet strict quality standards

- Financial Counseling Association of America (FCAA) — A national association of high-quality, nonprofit credit counseling agencies

- Consumer Financial Protection Bureau (CFPB) — Credit counseling guidance, debt management plan information, consumer education

- Federal Trade Commission (FTC) — Credit counseling vs. debt settlement guidance, consumer protection enforcement

- Fair Credit Reporting Act (FCRA) — 15 U.S.C. § 1681 et seq. — The federal law governing credit reporting and consumer rights

📊 Key Statistics (2026):

- 1 in 5 consumers have an error on at least one credit report — FTC study

- $50,000+ — lifetime cost of a 100-point drop in credit score (FICO/Consumer Reports)

- 47% of employers check credit reports during hiring — Society for Human Resource Management

- 30 days — the time credit bureaus have to investigate disputes under the FCRA

- 3-5 years — typical length of a Debt Management Plan (DMP) through NFCC/FCAA agencies

- 80%+ — estimated interest rate reduction achievable through nonprofit DMP enrollment

🏛️ Nonprofit Accreditation Standards — What to Look For:

- NFCC accreditation — Requires member agencies to maintain strict quality standards, provide certified counselors, and offer free initial counseling sessions

- FCAA membership — Requires agencies to meet rigorous financial stability and ethical practice standards

- 501(c)(3) nonprofit status — Legitimate credit counseling agencies operate as tax-exempt nonprofits, not for-profit companies

- No upfront fees rule — Under the FTC Telemarketing Sales Rule, legitimate agencies cannot charge fees before providing services

- CFPB registered — Accredited agencies maintain compliance with CFPB consumer protection standards

🚩 Red Flags — Avoid These Debt Relief Scams:

- Upfront fees before any service — Illegal under the FTC Telemarketing Sales Rule

- “Guaranteed” debt elimination — No legitimate company can guarantee debt elimination

- Tells you to stop paying creditors — This leads to lawsuits, ruined credit, and collection activity

- Not accredited by NFCC or FCAA — If they’re not on these lists, you’re in the for-profit, potentially predatory zone

- Promises to “erase debt for pennies on the dollar” — Legitimate credit counseling helps you repay what you owe with lower interest

📅 2026 Updates Included:

- Free weekly credit reports extended — Through 2026, consumers can access free weekly reports at AnnualCreditReport.com

- CFPB enhanced credit counseling guidance — Updated resources for consumers seeking nonprofit debt help

- State-level consumer protection laws — California, Colorado, New York, and Virginia have added additional credit counseling consumer protections

- FTC increased enforcement — Heightened scrutiny on for-profit debt settlement companies making false promises

⚠ For educational purposes only. Not financial or legal advice. Nonprofit credit counseling services, fees, and eligibility vary by agency and state. Always verify details directly with the NFCC, FCAA, or the specific agency before enrolling. The information in this article is current as of March 2026. If you are facing identity theft, fraud, or complex credit issues, consult a qualified consumer rights attorney or nonprofit credit counselor. Free credit reports available at AnnualCreditReport.com.

For the complete Emergency Borrowing Blueprint 2026 series, visit: Emergency Borrowing Blueprint 2026 → ConfidenceBuildings.com

📅 Published March 27, 2026 · Updated as part of the ConfidenceBuildings.com 2026 Consumer Finance Research Project.

This post is Episode 20 of 30 in the Emergency Borrowing Blueprint (2026 Complete Guide), examining emergency borrowing, predatory lending practices, and consumer financial rights. This episode focuses specifically on the best free credit counseling services in the USA—including how to choose between nonprofit counseling and paid tools, what to expect from a Debt Management Plan (DMP), and how to avoid debt settlement scams.

Research methodology: Information compiled from primary sources including the National Foundation for Credit Counseling (NFCC), Financial Counseling Association of America (FCAA), Consumer Financial Protection Bureau (CFPB), Federal Trade Commission (FTC), and the Fair Credit Reporting Act (15 U.S.C. § 1681). Debt Management Plan data from NFCC member agency reports and CFPB consumer research.

📌 2026 Updates Included:

- Free weekly credit reports extended through 2026 at AnnualCreditReport.com — essential for credit counseling prep

- CFPB enhanced credit counseling guidance and consumer complaint database updates

- State-level consumer protection laws (California, Colorado, New York, Virginia) with additional credit counseling consumer rights

- FTC increased enforcement against for-profit debt settlement companies making false promises

- Updated contact information for NFCC and FCAA member agencies nationwide

⚖️ For educational purposes only. Not financial or legal advice. Nonprofit credit counseling services, fees, and eligibility vary by agency and state. Always verify details directly with the NFCC, FCAA, or the specific agency before enrolling. If you are facing identity theft, fraud, or complex credit issues, consult a qualified consumer rights attorney or nonprofit credit counselor. Free credit reports available at AnnualCreditReport.com.

© 2026 ConfidenceBuildings.com · Emergency Borrowing Blueprint 2026 · Laxmi Hegde, MBA in Finance · Episode 20