⚖️ LEGAL DISCLAIMER

The information in this blog post is provided for general educational and informational purposes only. It does not constitute financial, legal, or professional advice of any kind. Every person’s financial situation is unique — what works for one person may not be appropriate for another depending on income, debt levels, credit history, and personal circumstances.

Laws, assistance programs, and financial products vary significantly by state, region, and country. Availability of the programs and options mentioned in this post may change at any time. Always verify current eligibility requirements directly with the relevant organization or institution.

The publisher, authors, and affiliated parties accept no liability for any financial outcomes resulting from the use of or reliance on any information in this post. Any third-party organizations, programs, or platforms mentioned are referenced for informational purposes only and do not constitute an endorsement or recommendation.

🔗 Part of the “Borrower’s Truth” Series — Day 3 In Day 2 we talked about building an emergency fund from scratch — starting with just $10. Read it here: How to Build an Emergency Fund From Scratch When You Have Nothing Saved But what if the emergency is happening right now, before the fund is ready? That’s exactly what today is about.

.

Read the complete guide here: The Complete Borrower’s Truth Guide →

Table of Contents

- When the Emergency Arrives Before the Fund Does

- Alternative 1: Negotiate Directly — The Most Underused Option in Personal Finance

- Alternative 2: Employer Paycheck Advance — Interest-Free Money You Already Earned

- Alternative 3: 211.org & Community Emergency Assistance Programs

- Alternative 4: Credit Union Payday Alternative Loans (PALs)

- Alternative 5: Cash Advance Apps — With Eyes Wide Open

- Alternative 6: Ask Your People — The Conversation Nobody Wants to Have

- Alternative 7: Sell Something — Fast, Judgment-Free, and Surprisingly Effective

- Comparison Table: All 7 Alternatives at a Glance

- When a Loan Actually Is Your Best Option

- Red Flags That Mean Run — Not Borrow

- Final Thoughts: You Have More Options Than You Think

1. When the Emergency Arrives Before the Fund Is Ready {#introduction}

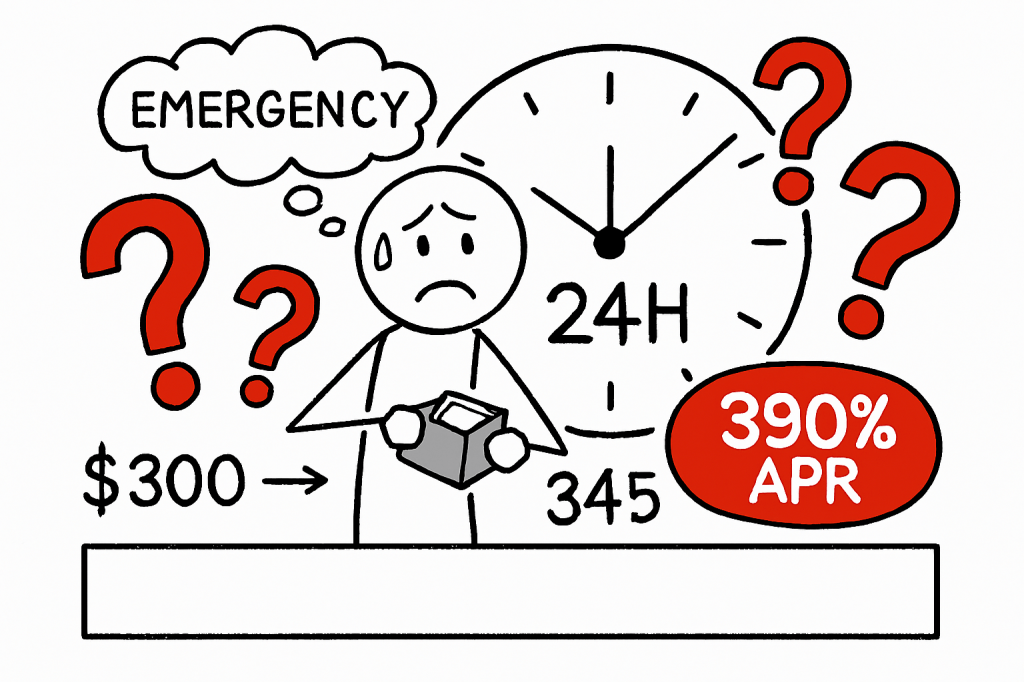

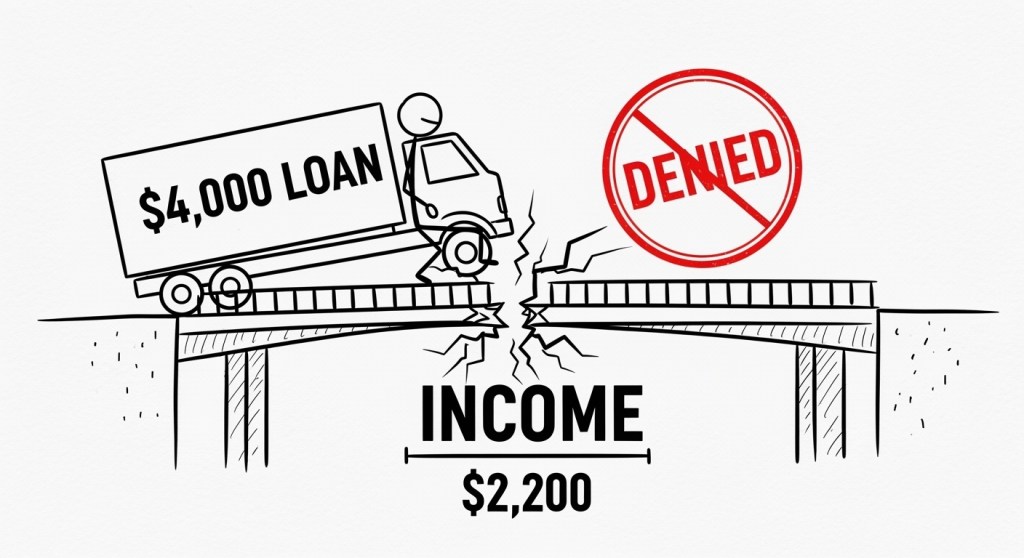

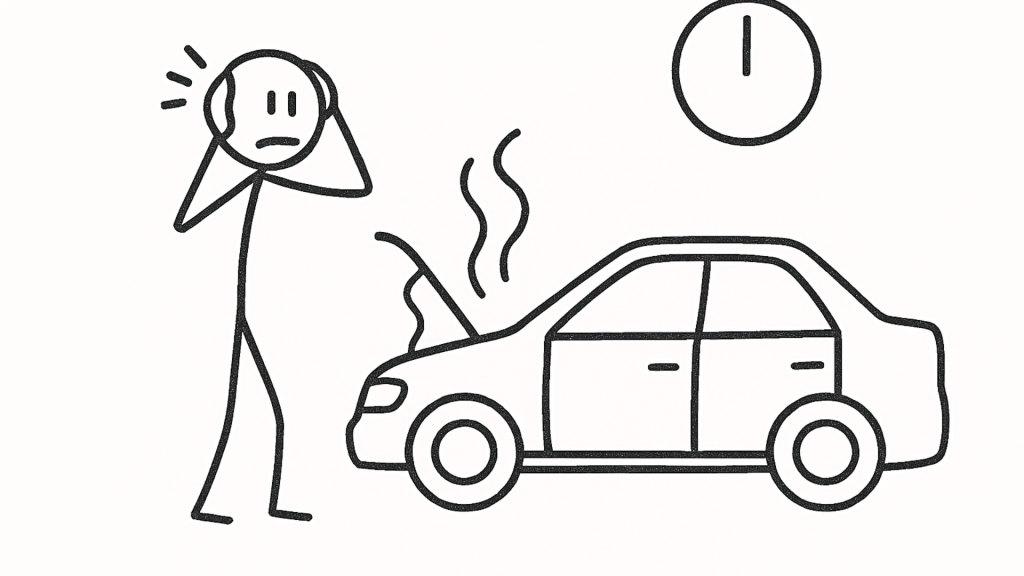

Picture this: it’s Thursday night. Your car just made a sound that cars should never make. The repair estimate is $600. Your emergency fund has $23 in it — because you started it last week, after reading Day 2 of this series (good for you, genuinely) — and your next paycheck isn’t until Friday of next week.

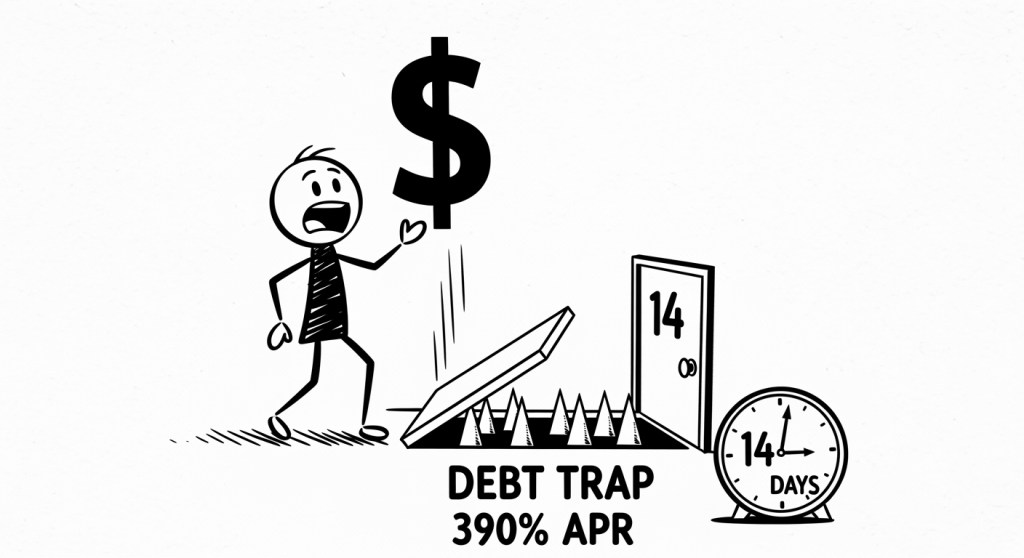

The internet, in its infinite helpfulness, immediately serves you ads for emergency loans with “instant approval” and “funds in 24 hours.” And honestly? In that moment, it sounds like the answer.

Here’s the thing though — it might not be. Not because loans are evil (we covered that nuance in Day 1), but because there are very real alternatives that are faster, cheaper, or both — and most people never try them because they don’t know they exist, or they feel too awkward to try.

This post is about those alternatives. All seven of them.

We’re going to go through each one honestly — what it is, how to actually use it, who it works for, and where it falls short. No fluff, no false promises. Just real options for a real Thursday night.

Let’s go.

2. Alternative 1: Negotiate Directly — The Most Underused Option in Personal Finance {#negotiate}

Let’s start with the one that almost nobody tries — and almost everybody should.

When you owe money to a doctor, a dentist, a mechanic, a landlord, or a utility company, there is a very good chance they will work with you on a payment plan if you simply pick up the phone and ask. Not because they’re feeling generous. Because getting paid slowly is better than not getting paid at all — and they know it.

Most people assume the bill is fixed. Non-negotiable. Final. The number at the bottom of the page is the number you pay, period. But that’s almost never actually true.

What to say — literally word for word:

“Hi, I received a bill for [amount] and I’m having some financial difficulty right now. Is there a payment plan available, or is there anything you can do to help me work something out?”

That’s it. That’s the whole script. You don’t need to over-explain, apologize excessively, or tell your whole story. Just ask.

Where this works best:

Medical and dental bills are the single biggest opportunity here. Hospitals and medical practices almost universally have financial hardship programs — many will reduce your bill significantly or set up a zero-interest payment plan if you qualify. These programs are not advertised. You have to ask for them specifically. Ask for the “financial counselor” or “billing department” and use the phrase “financial hardship assistance.”

Utility companies — electricity, gas, water — often have hardship programs and deferred payment options, especially in winter months. Your state utility commission may also require them to offer payment arrangements by law.

Landlords, especially individual landlords (as opposed to large property management companies), will often agree to a short-term arrangement if you communicate early and honestly. The key word there is early — before you’ve already missed the payment, not after.

Car repair shops vary widely, but many independent mechanics will let you pay in installments if you ask upfront. Some even work with third-party financing like Sunbit or Snap Finance — which are still financing products with their own terms, but typically better than a payday lender.

Success rate: Higher than you think. Consumer advocates consistently report that a meaningful percentage of people who ask for payment arrangements get them — often on the first call. The worst possible outcome is they say no — and you’re no worse off than before you called.

💡 Quick tip: Always get any payment arrangement confirmed in writing — even a quick email saying “As discussed, I’ll be making payments of $X on the Xth of each month” protects both parties and prevents misunderstandings.

3. Alternative 2: Employer Paycheck Advance — Interest-Free Money You Already Earned {#employer-advance}

Here’s a secret that feels slightly embarrassing to say out loud: asking your employer for a paycheck advance is one of the smartest financial moves you can make in a genuine emergency.

Why? Because it’s your money. You’ve already earned it — you just haven’t been paid yet. An advance isn’t charity. It isn’t a loan from a stranger with fine print. It’s your own wages, released a few days early.

The interest rate is zero. The approval process is a conversation. The repayment plan is your next paycheck.

How to ask:

Talk to your manager or HR directly and privately. Keep it simple: “I’m dealing with an unexpected emergency expense and I’m wondering if it’s possible to get an advance on my next paycheck. Even a partial advance would really help.”

Most reasonable employers — especially at small businesses — will say yes if the relationship is good and this isn’t a recurring pattern. If you’ve been reliable, shown up, and done your job, a one-time request like this is rarely a problem.

What if your workplace uses payroll apps?

Many employers now use platforms like Gusto, ADP, or Paychex — some of which have built-in earned wage access features that let employees draw on already-earned wages before payday without even involving a manager conversation. Check your employee portal first.

Earned Wage Access (EWA) apps:

If your employer doesn’t offer advances directly, apps like DailyPay, Payactiv, and Even partner with employers to let employees access earned wages early — often for a small flat fee ($1–$3) rather than interest. This is dramatically cheaper than any loan product.

⚠️ Disclaimer: Earned Wage Access products vary in their fee structures and terms. Always read the terms carefully before using any financial app. The apps mentioned above are referenced for informational purposes only — not endorsed.

4. Alternative 3: 211.org & Community Emergency Assistance Programs {#211-resources}

This one genuinely surprises people — and it shouldn’t, because it’s been quietly helping families for decades.

211 is a free, confidential service available across the United States (and parts of Canada) that connects people to local social services and emergency assistance programs. You can call 2-1-1, text your zip code to 898-211, or visit 211.org — and within minutes you’ll have a list of local resources that can help with exactly what you’re facing.

These programs cover:

- Emergency rent and utility assistance

- Food banks and grocery assistance

- Emergency transportation help

- Medical and prescription assistance

- Emergency shelter

- Childcare assistance

The beautiful thing about 211 resources? Most of them are grants, not loans. You don’t pay them back.

Many people in genuine financial distress have never heard of 211 — or they assume the resources are only for people in extreme poverty. They’re not. Many programs exist specifically for working people who are temporarily short due to an unexpected expense — exactly the situation you might be in.

Other resources worth knowing:

LIHEAP (Low Income Home Energy Assistance Program) — federally funded program that helps with heating and cooling bills. Eligibility varies by state and income level.

Local community action agencies — almost every county in the U.S. has one. They administer dozens of emergency assistance programs and can often help same-week.

Religious and faith-based organizations — churches, mosques, synagogues, and temples frequently run emergency assistance funds that are open to community members regardless of religious affiliation. Many don’t advertise this — call and ask.

Nonprofit credit counseling agencies — can negotiate with your creditors on your behalf, sometimes reducing interest rates or setting up repayment plans at no cost to you. Look for NFCC-member agencies.

💙 This option requires a phone call or a form. That’s it. If you’re in a genuine financial emergency, please don’t skip this one out of pride. These programs exist because communities take care of each other — and right now it’s your turn to receive that care.

5. Alternative 4: Credit Union Payday Alternative Loans (PALs) {#credit-union-pals}

Okay — so sometimes you genuinely do need to borrow money. There’s no negotiating your way out, no employer advance available, no assistance program that covers this particular thing. You need cash, and you need it soon.

If that’s where you are, credit union Payday Alternative Loans — called PALs — are the responsible borrower’s best friend.

Here’s why they matter: the National Credit Union Administration (NCUA) created the PAL program specifically to give people a safe alternative to predatory payday lenders. The terms are regulated by federal law.

PAL terms by law:

- Maximum interest rate: 28% APR (vs. 300–400% at a payday lender)

- Loan amounts: $200 to $1,000

- Repayment term: 1 to 6 months

- Application fee: maximum $20

- No rollover allowed

The catch: You typically need to be a credit union member for at least one month before you’re eligible for a PAL. Which means if you’re not already a member, today is a very good day to join one — even if you don’t need a PAL right this minute.

Most people are eligible for at least one credit union — through their employer, their community, a family member’s membership, or a simple geographic requirement. Membership usually costs $5–$25 to open. That $25 investment could save you hundreds in loan fees later.

How to find a credit union near you: Visit MyCreditUnion.gov or NCUA.gov and use the credit union locator tool.

⚠️ Disclaimer: PAL eligibility, loan terms, and membership requirements vary by credit union. Contact your local credit union directly for current rates and requirements. The NCUA website is the authoritative source for current PAL regulations.

6. Alternative 5: Cash Advance Apps — With Eyes Wide Open {#cash-advance-apps}

Let’s talk about the apps everyone’s using but nobody’s reading the fine print on.

Cash advance apps — Dave, Earnin, Brigit, MoneyLion, Chime’s SpotMe — have exploded in popularity because they feel friendly, modern, and instant. No credit check. No interest. Just “advance” yourself some money until payday. Easy!

And honestly? Used correctly, some of these apps are genuinely useful. But “used correctly” is doing a lot of heavy lifting in that sentence.

What the apps don’t shout from the rooftops:

The “optional” tip isn’t really optional. Many apps prominently ask for a tip when you request an advance. The suggested amounts — $1, $2, $3 — seem tiny. But on a $50 advance paid back in one week, a $3 “tip” is actually a 312% annualized rate. The apps know this. They just call it a tip.

Subscription fees add up fast. Several apps charge $1–$9.99/month for membership that unlocks the advance feature. If you’re using the app once every few months for a $50 advance, that monthly fee might cost more than the advance itself over time.

Advance limits start very small. Most apps start you at $20–$50 and only increase your limit over time based on account history. If you need $500 in an emergency, a cash advance app probably isn’t going to cover it.

Express fees for instant delivery. Want your money in minutes instead of 2–3 days? That’s an extra fee. Usually $2–$8. Again, on a small advance, this is a significant percentage.

When cash advance apps actually make sense:

- You need a small amount ($20–$200) to bridge a day or two gap

- You will 100% pay it back on your next payday

- You’ve read the actual fee structure and it’s cheaper than your alternative

- You’re not going to need it again next month, and the month after that

When to walk away:

- You’ve used the same app three months in a row

- The fees are starting to add up noticeably

- You’re advancing money to cover a previous advance

That third point is the cash advance version of a rollover trap — and it’s exactly how a “helpful app” turns into a monthly drain on your finances.

7. Alternative 6: Ask Your People — The Conversation Nobody Wants to Have {#ask-people}

Okay. This is the one that made you slightly uncomfortable just reading the heading. We know.

Asking friends or family for money is genuinely one of the most emotionally difficult things a person can do. There’s vulnerability in it, a fear of judgment, a worry about changing the relationship. Nobody wants to be the person who needed help.

But here’s the honest truth: a loan from someone who loves you, at 0% interest, with a flexible repayment timeline, is almost always better than a loan from an institution that sees you as a revenue opportunity.

The financial math is not close. It’s not even a competition.

So why don’t more people do it? Because we’ve been taught — mostly by cultural messages and pride — that needing help is shameful. It isn’t. It’s human.

How to ask in a way that feels okay:

Be specific about the amount and the repayment plan. Vague requests (“Can you help me out?”) create anxiety for the lender and resentment for you. Specific requests (“I need $300 to cover a car repair — I can pay you back $150 on the 1st and $150 on the 15th”) feel like a real plan, not a charity ask.

Put it in writing — even casually. A quick text confirming the terms protects the relationship far more than a handshake. It removes ambiguity and prevents the kind of misunderstandings that turn a generous act into a source of tension.

If they say no — and sometimes they will, for their own valid reasons — say thank you and move on without making it awkward. People who can’t help you financially right now aren’t bad people. They’re just people.

💙 There’s no shame in asking someone who loves you for help during a hard time. That’s what love is partly for. The shame, if there is any, belongs to a system that makes financial emergencies so common and so punishing — not to the person trying to survive one.

8. Alternative 7: Sell Something — Fast, Judgment-Free, and Surprisingly Effective {#sell-something}

This one is immediate, requires no approval, has no interest rate, and works faster than almost any other option on this list.

Walk through your home right now — mentally, or physically if you’re up for it — with fresh eyes. Not the eyes of someone who’s attached to their stuff. The eyes of someone who needs $200 by Friday.

You almost certainly have it.

What sells fast and for real money:

Electronics are the fastest movers — old phones, tablets, laptops, gaming consoles, cameras, earbuds. Even broken electronics have value. A cracked-screen iPhone 11 can fetch $80–$150 on the right platform.

Clothes and shoes in good condition — especially name brands — sell quickly on Poshmark, ThredUp, or Facebook Marketplace. A pile of clothes you haven’t worn in two years could realistically be $75–$200.

Furniture you don’t love — that spare chair, the side table nobody uses, the shelving unit from three apartments ago. Facebook Marketplace and Craigslist move furniture fast, especially if you price it to sell.

Kids’ items — toys, clothes, baby gear, strollers — sell extremely well locally. Parents looking for deals are everywhere and they move fast.

Tools, sports equipment, kitchen appliances — anything in working condition has a buyer somewhere.

Fastest platforms for cash:

- Facebook Marketplace — fastest local cash sales, meets in person

- OfferUp — similar to Marketplace, very active in most areas

- Decluttr — instant price quotes on electronics, send it in and get paid

- Poshmark / ThredUp — clothes, slightly slower but reliable

- eBay — best for unique or valuable items, takes a few days

Realistic timeline: List items tonight, sell by the weekend. For most people in most cities, $100–$400 is achievable within 48–72 hours from stuff already in their home.

No application. No credit check. No interest. No fine print.

Comparison Table: All 7 Alternatives at a Glance {#comparison-table}

| Alternative | Cost | Speed | Amount Available | Best For |

|---|---|---|---|---|

| 🤝 Direct Negotiation | Free | Same day | Varies | Medical, utility & rent bills |

| 💼 Employer Advance | Free | 1–2 days | Up to 1 paycheck | Employed with good relationship |

| 🏘️ 211 / Community Aid | Free (grant) | 1–5 days | Varies by program | Rent, utilities, food, medical |

| 🏦 Credit Union PAL | 28% APR max | 1–3 days | $200–$1,000 | Credit union members (1+ month) |

| 📱 Cash Advance App | $1–$10 fee | Instant–3 days | $20–$500 | Small short-term gap only |

| 👥 Friends & Family | Free (ideally) | Same day | Varies | Trusted relationships + clear plan |

| 📦 Sell Your Stuff | Platform fees only | 24–72 hours | $50–$500+ | Anyone with sellable items at home |

10. When a Loan Actually Is Your Best Option {#when-loan-is-best}

Here’s the honest part — the part that separates this blog from the ones that are just trying to make you feel bad for needing money.

Sometimes, a loan really is the right answer.

If the amount you need is large, if all seven alternatives above genuinely don’t apply to your situation, and if the loan is from a responsible lender with transparent terms — then borrowing is a completely legitimate financial tool and there’s no shame in using it.

The key word in that sentence is responsible. Before you sign anything, please read our full breakdown of hidden fees, APR traps, and fine print tricks: Hidden Costs & Fine Print: What Lenders Don’t Tell You

Signs a loan makes sense:

- The amount needed is too large for any of the alternatives above

- You have a clear, realistic repayment plan

- The APR is reasonable and fully disclosed

- There are no prepayment penalties

- You’ve compared at least 3 lenders

- The lender is verified and legitimate

Signs it doesn’t:

- You’re borrowing to cover a previous loan payment

- You don’t know the full APR

- You haven’t read the agreement

- You’re feeling pressured to sign quickly

⚠️ Reminder: This is general guidance, not personalized financial advice. Your specific situation — income, existing debt, credit score, and the nature of your emergency — should all factor into your decision. When in doubt, a free consultation with a nonprofit credit counselor can help clarify your options.

11. Red Flags That Mean Run — Not Borrow {#red-flags}

Whether you end up using one of the seven alternatives or deciding a loan is right for you — watch for these signals that something is wrong:

🚩 Guaranteed approval with no questions asked — Legitimate lenders assess risk. No questions = no legitimacy.

🚩 Upfront fee required before funds are released — This is advance fee fraud. Full stop. Run.

🚩 The lender contacted you — Legitimate emergency loan providers don’t cold-call, cold-text, or cold-email people in financial distress. If someone reached out to you first, be very cautious.

🚩 Pressure to decide immediately — Ethical lenders give you time to read and think. “This offer expires in 2 hours” is a manipulation tactic, not a real deadline.

🚩 No physical address or verifiable registration — Check the lender on your state’s financial regulatory website before sharing any personal information.

🚩 The terms change between what was said verbally and what’s written — End the conversation immediately.

12. Final Thoughts: You Have More Options Than You Think {#final-thoughts}

Financial emergencies have a way of making the world feel very small, very fast. When the car breaks down and the account is empty, the brain narrows its focus — and that narrow focus is exactly what predatory lenders exploit. They know you’re stressed. They know you’re not thinking about fine print. They built their entire business model around that moment.

The seven alternatives in this post exist in that same moment — they’re just quieter about it. They don’t buy Google ads. They don’t send you push notifications. They’re just there, waiting to be found by someone who knows to look.

Now you know to look.

And if you’ve been building your emergency fund since reading Day 2 — even just a little — that fund is quietly working to make sure next time, you don’t have to choose between a bad loan and a hard conversation. You’ll just handle it.

That’s the goal. We’re getting there together.

🔗 Coming up — Day 4 of the Borrower’s Truth Series: “How Lenders Use Your Credit Score Against You (And How to Fight Back)” Because knowing your number is only half the battle — understanding how it’s used against you is the other half.

💬 Have you ever used one of these alternatives — or wished you’d known about them sooner? Tell me in the comments. Someone reading this right now might need to hear your story.