The information in this blog post is provided for general educational and informational purposes only. It does not constitute financial, legal, or professional advice of any kind. Rent-to-own regulations, contract terms, and company practices vary significantly by state and change frequently.

All regulatory actions, settlements, and legal proceedings referenced in this post are based on publicly available FTC filings, state attorney general press releases, and CFPB research as of February 2026. Legal proceedings and settlements referenced represent past actions — always verify current company practices and contract terms before signing any agreement.

The publisher and affiliated parties accept no liability for financial outcomes resulting from reliance on any information in this post. No companies are endorsed or affiliated with this content.

Read the complete guide here: The Complete Borrower’s Truth Guide →

The Borrower’s Truth Series is a 30-day financial literacy series published on ConfidenceBuildings.com by Laxmi Hegde — MBA in Finance and content creator.

The series was created because financial advice is almost always written for people who already have money — and that’s never been good enough. Every episode is written from the consumer’s perspective, with zero affiliate bias, zero lender partnerships, and zero tolerance for advice that sounds helpful but isn’t.

New episodes publish daily. This pillar page is updated as each new episode goes live.

📚 All Published Episodes:- Day 1 — Hidden Costs & Fine Print: What Lenders Don’t Tell You

- Day 2 — How to Build an Emergency Fund From Scratch When You Have Nothing Saved

- Day 3 — Broke & Stressed? 7 Real Alternatives to Emergency Loans That Most People Overlook

- Day 4 — Your Credit Score Is a Weapon — And Lenders Are Trained to Use It Against You

- Day 5 — Secured vs. Unsecured Loans: The Decision Nobody Helps You Make (Until Now)

- Day 6 — Loan Fine Print Survival Guide: 30 Terms Your Lender Hopes You Never Understand

- Day 7 — Week 1 Roundup: The 7 Borrowing Mistakes We Exposed — And What Knowing Them Is Actually Worth to You

- Day 8 — Tax Refund Advance Loans: Why “Free” Is the Most Expensive Word in Tax Season

- Day 9 — Cash Advance Apps: Better Than Payday Loans — But Not As Safe As They Look

- Day 10 — I Need $500 Today: The Complete Decision Guide Written For the Moment You’re Actually In

- Day 11 — payday loans the 9 billion industry built on one calculation that you cant repay

- Day 12 — title-loans-youre-not-borrowing-against-your-car-youre-betting-it/

- Day 13 — rent-to-own-the-store-that-sells-you-a-400-tv-for-1200-and-installed-spyware-on-your-laptop-while-it-did-it/

- Days 14–30 — Publishing daily — bookmark this page

📋 2026 Data Summary — Buy Now Pay Later (BNPL)

💰 Typical Interest Cost

0% — If On Time

⚡ Speed of Access

Instant at Checkout

📊 Min Credit Score

None — No Hard Pull

🚨 Late Payment Rate

24% — Up From 18%

| 📅 Standard Plan Structure | Pay-in-4: 4 equal payments, every 2 weeks |

| 🔄 Users With Multiple Active Loans | 66% stacking plans across providers (CFPB Jan 2025) |

| 💳 Extra Credit Card Debt vs. Non-Users | $871 more on average (CFPB Jan 2025) |

| ⚖️ Federal Regulation | CFPB oversight — consumer protections in flux 2025 |

| 📉 Reports to Credit Bureau? | Usually no — until default/collections |

| 🌍 Global BNPL Market (GMV) | $560 billion (2025 estimate) |

Source: Federal Reserve 2024, CFPB Jan 2025, Motley Fool 2025, Numerator 2025 | Updated March 2026 | Laxmi Hegde, MBA in Finance | ConfidenceBuildings.com

⚠️ IMPORTANT DISCLAIMER NOTE

The 91.5M and $560B figures come from market research projections — not government data.

The 31% figure is from a private survey (Motley Fool, n=2,000) — also worth flagging as survey-based, not federal data.

🤖 TL;DR — Structured Summary For Quick Reference

| 📌 What This Post Covers | How BNPL works, why it doesn’t feel like debt, who is most at risk, hidden fees including overdraft triggers, CFPB data on debt stacking, and every smarter alternative. |

| 📊 Key Statistic | 66% of BNPL users hold multiple active loans simultaneously. 24% have made a late payment — up from 18% in 2023. BNPL users carry $871 more in credit card debt than non-users. |

| ⚠️ Biggest Risk | Auto-debit on a thin bank balance triggers overdraft fees on top of BNPL late fees — two penalties from one missed payment. Debt stacking across multiple providers with no consolidated statement. |

| ✅ Best Alternative | A 0% APR credit card with a grace period gives more time, stronger consumer protections, dispute rights, and builds credit — all things BNPL does not offer. |

| 🏛️ Regulatory Status | CFPB issued credit-card-style protections in May 2024. As of early 2025, the agency signaled plans to roll those protections back. |

| 💡 Bottom Line | BNPL is a debt accumulation mechanism dressed in a frictionless UI — engineered to feel like pressing a button, not like borrowing money. The data shows it is working exactly as designed. |

ConfidenceBuildings.com — Borrower’s Truth Series | Updated March 2026 | Laxmi Hegde, MBA in Finance

Table of Contents

- How BNPL Actually Works — The Checkout Button That Is Also a Loan

- The Data on Debt: What the Numbers Actually Show

- The Invisible Fees Nobody Talks About

- Who Is Most at Risk — and Why

- The Psychology of “It Doesn’t Feel Like Debt”

- BNPL vs. Credit Card vs. Personal Loan

- Decision Path: Should You Use BNPL?

- What to Do Instead

- Reader Story

- Research Note

🔀 Quick Answer: Is BNPL Safe?

Ask yourself before you tap “Pay in 4”:

- Do I already have an active BNPL loan?

- Do I know exactly when each payment auto-debits — and is my bank balance ready?

- If I need to return this item, do I know the refund process for this specific provider?

- Am I using BNPL as a timing tool — or because I can’t actually afford this right now?

- Could a 0% APR credit card or waiting 2 more weeks give me a safer option?

1. How BNPL Actually Works — The Checkout Button That Is Also a Loan

How Does Buy Now Pay Later Actually Work?

It’s four easy payments. It’s interest-free. It appears at checkout, smooth and frictionless, asking almost nothing of you.

That is the design. Buy Now Pay Later is not designed to feel like borrowing money. It is designed to feel like pressing a button. And that is precisely why it has become one of the fastest-growing — and least understood — debt products in America.

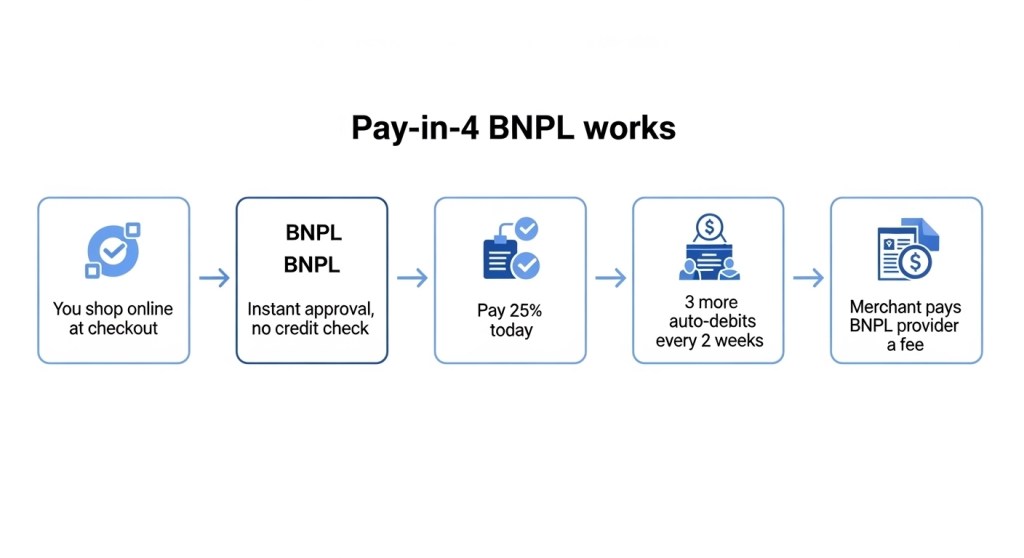

The dominant model is “Pay in 4”: split a purchase into four equal installments every two weeks, first payment due at checkout. No hard credit check. No application form. Approval in seconds. Major providers — Klarna, Affirm, Afterpay, PayPal Pay Later, Zip — are embedded directly into retailer checkout flows across clothing, electronics, furniture, and increasingly, groceries and food delivery.

By 2025, the global BNPL market reached $560 billion in gross merchandise volume. Roughly 91.5 million Americans were projected to use it. One in five Americans said they were more likely to complete a purchase if BNPL was available at checkout. That behavior is not incidental — it is exactly what the product is engineered to produce.

Here is how the money works: the merchant pays the BNPL provider a transaction fee (typically 2–8% of the purchase). The consumer gets the flexibility. The BNPL provider earns from merchant fees, late fees, and in some products, interest on longer installment plans. The short Pay-in-4 version is marketed as “no interest” — which is true, unless you’re late, or unless you choose a longer-term plan.

What BNPL does not give you: a consolidated statement. There is no single view showing your total BNPL exposure across providers. You might have $80 owed to Klarna, $120 to Afterpay, and $200 to Affirm all running simultaneously — and no dashboard in your bank app will add those together for you. That invisibility is not a bug. It is a feature.

2. The Data on Debt: What the Numbers Actually Show

The CFPB published a detailed study on BNPL borrowers in January 2025. The Federal Reserve included BNPL questions in its 2024 Economic Well-Being of U.S. Households survey. Multiple independent research firms tracked user behavior throughout 2024–2025. Here is what the data shows, consistently, across all of them:

- 66% of BNPL users hold multiple active BNPL loans simultaneously. One-third borrow from more than one provider at the same time. (CFPB, January 2025)

- 24% of BNPL users have made a late payment, up from 18% the prior year — a 33% increase in one year. Among adults aged 18–29, the rate rises to 32–39%. (Federal Reserve, 2024)

- BNPL users carry $871 more in credit card debt than non-BNPL users on average — and $453 more in personal loan balances. This is not BNPL replacing credit card debt. It is stacking on top of it. (CFPB, January 2025)

- ~31% of users lose track of what they owe across their open plans.

- Only 47% of BNPL users plan their payments ahead of time. The rest track loosely or not at all. (Motley Fool 2025)

- More than half of BNPL users report relying on it to buy things they could not otherwise afford. (Motley Fool 2025)

- 26% of users reported regretting the purchase once the full cost hit home. Among millennials, 30%.

- 24% of users feel stressed about upcoming BNPL installments often or always. (Empower Personal Dashboard)

- One in four people who used BNPL looked back and wished they hadn’t. That is not a fringe outcome. That is a quarter of all users.

3. The Invisible Fees Nobody Talks About

BNPL is marketed as interest-free. For a single transaction, paid on time, it can be. Here is where the costs actually hide:

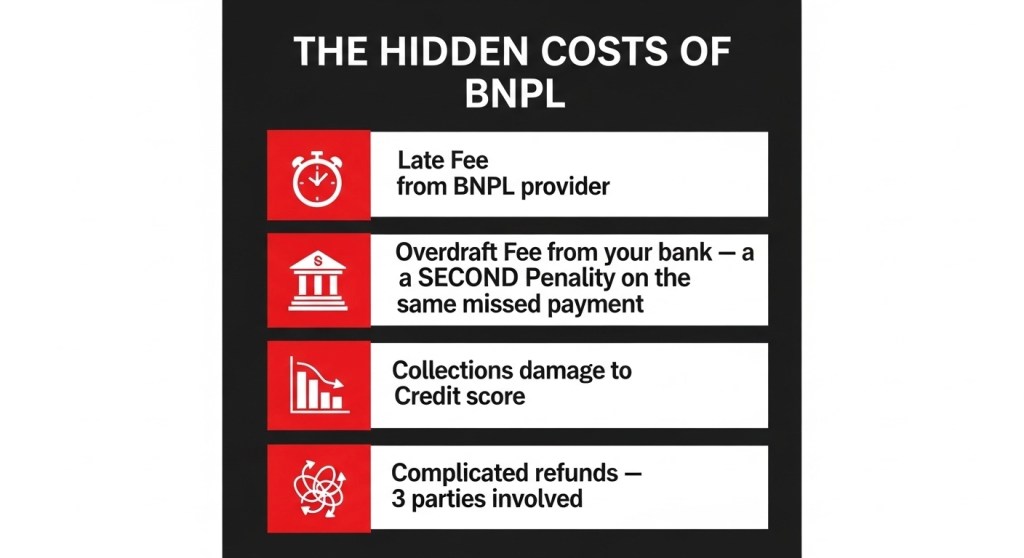

Late fees from the BNPL provider. Miss a payment and you will be charged — either a flat fee or a percentage of the missed installment, depending on the provider. These fees are disclosed in terms and conditions almost no one reads at checkout.

Overdraft or NSF fees from your bank. This is the hidden cost the CFPB has flagged most loudly. Most BNPL plans auto-debit your linked bank account or debit card on a fixed schedule. If your balance is low on the scheduled day, your bank charges an overdraft fee — separate from and in addition to any BNPL late fee. You can do everything “right” — set up auto-pay, intend to pay — and still get hit with two penalties because of one thin bank account day.

Collections and credit score damage. BNPL typically does not appear on your credit report while in good standing. But if you fall far enough behind, the debt is sold to collection agencies — who do report it. A single missed payment may not damage your score, but a pattern of overextension ending in collections will.

Complicated refunds. Try returning a BNPL purchase and you will discover that refunds involve three separate parties — the merchant, the BNPL provider, and your bank account. The CFPB issued protections in May 2024 requiring BNPL providers to follow credit-card-style dispute and refund rules. As of early 2025, the agency signaled it may roll those protections back.

Interest on longer BNPL products. Not every BNPL product is Pay-in-4. Affirm and others offer 6, 12, and 24-month installment plans that carry real interest rates — sometimes 15–30% APR. These look like BNPL at checkout but are functionally personal loans.

4. Who Is Most at Risk — and Why

Every major survey reaches the same conclusion: BNPL risk concentrates among younger, lower-income, and financially stretched consumers.

Numerator’s 2025 research found BNPL users are disproportionately Gen Z or millennial, multicultural, urban families earning under $60,000 per year — and 42% more likely to fall in the lower third of purchasing power. The top two reasons they use BNPL: managing cash flow (36%) and making large purchases more affordable (28%).

That context matters. When someone earning $38,000 a year uses BNPL for a car repair, a winter coat, and a laptop for their child — each individual decision is understandable. But three simultaneous BNPL plans auto-debiting from one bank account creates a cascade of risk that no single checkout moment reveals.

The Kansas City Fed’s 2025 research confirmed that BNPL users are disproportionately financially constrained — more likely to have experienced a financial hardship, more likely to be carrying high-cost debt, and more likely to be living paycheck to paycheck. BNPL is not reaching the consumers who can most easily absorb the risk of a missed payment. It is reaching the ones who can least.

5. The Psychology of “It Doesn’t Feel Like Debt”

BNPL is engineered to neutralize what financial psychologists call the pain of paying — the mild psychological discomfort that normally acts as a natural brake on spending. When you hand over cash, or even swipe a credit card, something registers. The number is real and present.

BNPL removes every friction point. There is no application. No loan officer. No loan number. No single large number to confront. Just four small payments that each, individually, sound manageable. This is payment decoupling — separating the emotional experience of paying from the pleasure of receiving the product. Credit cards do this too, but at least a credit card gives you one monthly statement that adds everything up. BNPL gives you no such moment of reckoning.

The result: people consistently underestimate how much they have borrowed via BNPL. They open new plans without mentally closing old ones. The 31% who lose track of their total balance are not failing at personal finance. They are experiencing the entirely predictable outcome of a product built to be invisible.

The 24% of users who feel stressed about upcoming installments are not an anomaly. They are the product working exactly as designed — the purchase long made, the payments now arriving.

BNPL vs. Credit Card vs. Personal Loan: What You’re Actually Comparing

| Feature | BNPL (Pay-in-4) | Credit Card | Personal Loan |

|---|---|---|---|

| Credit check? | Usually none or soft pull | Yes — hard inquiry | Yes — hard inquiry |

| Reports to credit bureau? | Usually no (until default) | ✅ Yes — builds credit | ✅ Yes — builds credit |

| Interest rate | 0% if on time; 15–30% APR on longer plans | ~20–28% APR if balance carried | 7–36% APR by credit |

| Consolidated debt view | ❌ Fragmented across providers | ✅ One monthly statement | ✅ Fixed repayment schedule |

| Consumer protections | Limited — CFPB rules in flux 2025 | Strong — dispute rights, fraud | Moderate |

| Rewards / cash back | ❌ None | ✅ Yes — if paid in full | ❌ None |

| Overdraft risk | 🔴 High — auto-debit, no warning | 🟢 Low — you control timing | 🟢 Low — fixed scheduled payment |

7. What to Do Instead — And If You Use BNPL, How to Use It Wisely

If you choose to use BNPL:

- Use it for one purchase at a time. Never stack plans across providers.

- Set a calendar reminder for every payment date before you complete checkout — not after.

- Check your bank balance 48 hours before each auto-debit date.

- Use it only for purchases you could pay in full if you had to. It is a timing tool, not a credit expansion tool.

- Understand the refund policy for that specific provider before you buy anything

If you are considering BNPL because you cannot otherwise afford something:

- Ask whether the purchase can be delayed two to four weeks until you have the cash.

- Check if your credit union or community bank offers a small personal loan at a lower rate with a real statement.

- A 0% APR credit card promotional offer gives more time, stronger protections, and builds your credit score.

- If it is a necessity — car repair, medical bill, essential appliance — look for nonprofit emergency assistance programs or payment plans directly with the provider before using BNPL.

❓ Frequently Asked Questions — Buy Now Pay Later

Q: Is Buy Now Pay Later considered debt?

Yes. BNPL is a short-term installment loan in every practical sense. In 2025, 66% of BNPL users held multiple active loans simultaneously (CFPB, Jan 2025). It does not typically appear on your credit report while in good standing — but it is legally and financially a debt obligation. Missing payments can trigger collections and credit score damage.

Q: What happens if you miss a BNPL payment?

Missing a BNPL payment triggers two separate penalties: a late fee from the BNPL provider, and a potential overdraft fee from your bank if the auto-debit fails on a low balance. In 2024, 24% of BNPL users reported missing at least one payment — up from 18% the prior year (Federal Reserve, 2024). Repeated missed payments can result in debt collection and permanent credit score damage.

Q: Is BNPL better than a credit card?

For most borrowers, no. Credit cards offer consolidated monthly statements, dispute rights, fraud protection, rewards, and credit-building — none of which BNPL provides. BNPL users carry $871 more in credit card debt than non-users on average (CFPB, Jan 2025), suggesting BNPL stacks on top of existing debt rather than replacing it. A 0% APR credit card promotional offer is almost always a safer alternative.

Q: Does BNPL affect your credit score?

In most cases, BNPL does not help your credit score — but it can hurt it. Most Pay-in-4 BNPL plans do not report on-time payments to credit bureaus, so responsible use builds no credit history. However, missed payments that escalate to collections are reported and can significantly damage your score. You get all the risk of debt with none of the credit-building benefit.

Q: Can you have multiple BNPL loans at the same time?

Yes — and most users do. In 2025, 66% of BNPL users held multiple active loans simultaneously, and one-third borrowed from more than one provider at the same time (CFPB, Jan 2025). Because there is no single consolidated statement showing your total BNPL exposure, 31% of users lose track of what they owe across their open plans (Motley Fool, 2025).

Q: What are the hidden fees in BNPL?

BNPL’s hidden costs include: (1) late fees from the provider, (2) bank overdraft fees triggered by auto-debit on a low balance, (3) interest rates of 15–30% APR on longer installment plans, and (4) complicated refund processes involving three separate parties — the merchant, the BNPL provider, and your bank. The CFPB flagged overdraft triggering as a key hidden risk in its January 2025 study.

Q: What is the safest way to use BNPL?

The safest BNPL use follows four rules: (1) one plan at a time — never stack multiple loans, (2) only for purchases you could pay in full if needed, (3) set calendar reminders for every auto-debit date before checkout, and (4) verify your bank balance 48 hours before each payment. Use BNPL as a timing tool only — never as a way to afford something you otherwise cannot.

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“Buy Now Pay Later occupies a legal gray area that is exceptionally favorable to providers and exceptionally risky for consumers. Unlike credit cards, BNPL lenders are not uniformly required to investigate disputed charges, provide clear refund mechanisms, or report on-time payments to credit bureaus. In May 2024, the CFPB issued an interpretive rule stating that BNPL lenders must provide credit-card-style dispute and refund rights. But as of early 2025, the agency signaled its intent to roll those protections back. This regulatory whiplash means consumer rights under BNPL can change with the political winds — and often disappear entirely when you need them most. The data shows the outcome: 66% of BNPL users hold multiple active loans with no consolidated statement, 24% have made a late payment, and users carry $871 more in credit card debt than non-users. This is not a budgeting tool. It is an unregulated debt accumulation system designed to feel like a button press — and the legal structure has consistently lagged behind the harm.”

Legal Analysis: The legal status of BNPL is unsettled. The CFPB’s May 2024 interpretive rule attempted to classify BNPL as “credit cards” under Regulation Z for dispute resolution purposes — giving consumers the right to withhold payment during disputes. However, the rule was an interpretation, not a congressionally mandated regulation, and the agency has signaled potential reversal. Key ongoing risks: (1) BNPL providers are not required to verify ability to repay, (2) auto-debit structures create overdraft liability without adequate disclosure, and (3) refunds involving three parties (merchant, provider, bank) routinely fail, leaving consumers liable for goods they returned. If you have a BNPL dispute that isn’t resolved, file a complaint with the CFPB and your state attorney general’s consumer protection division immediately.

Bottom Line: BNPL is the only consumer credit product that combines 0% interest marketing with no credit-building benefit, no consolidated statement, and weaker legal protections than a basic credit card. Before you tap “Pay in 4,” ask: do you know when every payment hits your bank account, and is that balance guaranteed to be there? One missed auto-debit can trigger both a BNPL late fee and a bank overdraft fee — two penalties from a single thin balance day.

🗺️ Related Reading — Borrower’s Truth Series

Understanding BNPL is one piece of the borrowing picture. These posts map the full lifecycle:

- 💳 Before you borrow anything → Hidden Costs & Fine Print: What Lenders Don’t Tell You

- 🏦 Build safety net first → How to Build an Emergency Fund From Scratch

- 🆘 Need money today — avoid BNPL → 7 Real Alternatives to Emergency Loans

- 📊 Understand your credit first → Your Credit Score Is a Weapon

- 📋 Read the fine print before signing → Loan Fine Print Survival Guide: 30 Terms Decoded

- ⚡ Need cash fast — safer options → Cash Advance Apps: Better Than Payday Loans?

- 🚨 Worst case — payday loan risks → Payday Loans: The $9 Billion Industry

- 🚗 Never bet your car → Title Loans: You’re Not Borrowing Against Your Car — You’re Betting It

- 📺 Avoid 3x markup traps → Rent-to-Own: The $400 TV That Costs $1,200

- 📚 See all 30 days → The Complete Borrower’s Truth Guide →

💬 Reader Story

“I had four BNPL plans going at the same time and I genuinely didn’t know. I thought I was being smart — ‘no interest, easy payments.’ Then in one week, all four auto-debited and I overdrafted twice. I paid $70 in bank fees to avoid $0 in BNPL interest. That math makes no sense and I will never do it again.”

— Darnell, 29, Chicago. Shared in the Confidence Buildings reader community.

Have a BNPL experience — good or bad? Share it in the comments below. Your story helps someone else make

🧠 Psychological Struggle: Why This Is Harder Than It Looks

BNPL is the first consumer credit product in history that was built from the ground up using behavioral economics — not to protect the borrower from overborrowing, but to remove every psychological friction that would have slowed them down.

Traditional lending has friction by design: applications, waiting periods, credit checks, loan officers, monthly statements. These inconveniences are also guardrails. BNPL removed all of them.

The 24% of users who are “often or always stressed” about upcoming installments are not weak or irresponsible. They are experiencing the inevitable result of a product that was engineered to let them borrow before the rational part of their brain could catch up. Understanding that does not fix the debt — but it does mean the struggle is not a personal failure. It is a design outcome.

📚 Research Note

Statistics in this post are drawn from the following primary and secondary sources. All data reflects research available as of early 2026.

- Federal Reserve — Report on the Economic Well-Being of U.S. Households, 2024 (released May 2025)

- CFPB — “Consumer Use of Buy Now, Pay Later and Other Unsecured Debt,” January 2025

- CFPB — “Study of Buy Now, Pay Later (BNPL) Borrowers,” January 2025

- Motley Fool Money — 2025 Buy Now, Pay Later Trends Study (n=2,000 U.S. adults)

- Numerator — Buy Now, Pay Later Market Insights, February 2025 (n=2,572 BNPL users)

- Empower Personal Dashboard — BNPL spending behavior data, 2025

- Kansas City Fed — “Financial Constraints Among Buy Now, Pay Later Users,” 2025

⚠️ Where survey results vary across studies due to methodology or sample differences, ranges are noted. This post reflects data available as of early 2026. Statistics are cited for educational purposes only and do not constitute financial advice.

The Bottom Line

BNPL is not inherently predatory. Used once, for one well-planned purchase you can genuinely afford, it is a neutral tool — and no worse than any other form of short-term credit.

The problem is that it is not built for that use case. It is built to be used repeatedly, invisibly, stackably — and it grows fastest among the consumers with the least margin for error. A product where 66% of users stack multiple simultaneous loans, where late payment rates climbed 33% in a single year, where users carry $871 more in credit card debt than non-users — is not a budgeting aid. It is a debt accumulation mechanism in a frictionless UI.

The debt is real. It just doesn’t feel like it yet.

— Laxmi Hegde, MBA in Finance

confidencebuildings.com

View the complete 30-day research series →

📚 Research Note — Primary Sources

All statistics in this post are drawn from primary government and independent research sources. Click any source to verify directly.

- Federal Reserve — Report on the Economic Well-Being of U.S. Households, 2024 — Source for 24% missed payment statistic

- CFPB — Study of Buy Now Pay Later Borrowers, January 2025 — Source for 66% multiple loans + $871 credit card debt statistics

- CFPB Consumer Advisory — CFPB Action on BNPL Credit Card Rules, May 2024 — Source for consumer protection ruling

- Motley Fool Money — 2025 Buy Now Pay Later Trends Study (n=2,000 U.S. adults) — Source for 31% lose track statistic

- Numerator — Buy Now Pay Later Market Insights, February 2025 (n=2,572 BNPL users) — Source for demographic risk data

- Kansas City Fed — Financial Constraints Among Buy Now Pay Later Users, 2025 — Source for financially constrained borrower data

- FTC Consumer Advice — Understanding Your Credit Rights — Background on consumer credit protections

⚠️ Survey-based figures reflect self-reported data and may vary across studies due to methodology differences. Government source statistics reflect primary research. All data cited for educational purposes only. This is not financial advice.

Day 13: Rent-to-Own — The Store That Sells You a $400 TV for $1,200 📚 Series Home Next: →

Day 15: Coming Tomorrow

Tax Refund Advance Loans: Why Free Is the Most Expensive Word in Tax Season

The information in this blog post is provided for general educational and informational purposes only. It does not constitute financial, legal, or tax advice of any kind. Tax refund advance products, fees, APRs, and terms change frequently and vary significantly by provider, tax year, and individual circumstances.

All product details, APRs, and fee structures referenced in this post are based on publicly available information as of February 2026. Always verify current terms directly with any tax preparation provider before making decisions. Consult a qualified tax professional or financial advisor for advice specific to your situation.

The publisher and affiliated parties accept no liability for financial or tax outcomes resulting from reliance on any information in this post. No tax preparation companies or financial institutions are endorsed or affiliated with this content.

Read the complete guide here: The Complete Borrower’s Truth Guide →

Part of the ConfidenceBuildings.com — Borrower’s Truth Series

📅 Day 8 Episode | Published: February 2026

📚 Previous Episodes in This Series:

- Day 1 — Hidden Costs & Fine Print: What Lenders Don’t Tell You

- Day 2 — How to Build an Emergency Fund From Scratch

- Day 3 — 7 Real Alternatives to Emergency Loans

- Day 4 — Your Credit Score Is a Weapon

- Day 5 — Secured vs. Unsecured Loans: The Decision Nobody Helps You Make

- Day 6 — Loan Fine Print Survival Guide: 30 Terms Decoded

- Day 7 — Week 1 Roundup: 7 Borrowing Mistakes Exposed

Table of Contents

- The Most Expensive Time of Year to Borrow Your Own Money

- What a Tax Refund Advance Actually Is — Beyond the Advertisement

- The $842 Million Number Nobody Talks About

- The Ecosystem Lock-In Strategy — Why “Free” Costs More Than You Think

- The Provider Comparison: TurboTax vs H&R Block vs Jackson Hewitt

- The Refund Shortfall Trap — What Happens When the Math Doesn’t Work Out

- The 2026 Paper Check Ban — New Vulnerability for Unbanked Taxpayers

- Who Actually Benefits From a Tax Refund Advance

- Who Should Absolutely Avoid Them

- Better Alternatives to Get Through Tax Season

- The Tax Season Decision Framework — Your 4-Step Guide

- FAQ: Real Questions About Tax Refund Advances

- Final Thoughts: Your Refund, Your Timeline, Your Choice

1. The Most Expensive Time of Year to Borrow Your Own Money {#intro}

Every year between January and April, a very specific type of financial marketing goes into overdrive.

The ads show up everywhere — on tax preparation websites, in bank lobbies, on social media feeds. “Get your refund today.” “Access your money in minutes.” “0% APR — no fees.” They’re designed to feel like a gift: the IRS owes you money, and here’s a company offering to advance it to you right now, at no cost, as a courtesy.

Here’s the thing about courtesy in the financial industry — it almost never arrives without a business model attached.

Tax refund advance products are one of the most sophisticated customer acquisition tools in the financial services sector. The “free loan” is real — for some products, from some providers, under specific conditions. But the loan is not the product. You are. More specifically, your ongoing banking relationship, your email address, your financial data, and your future lending behavior are the product.

This post is going to show you exactly how the system works — what the advance costs, what it captures, what happens when things go sideways, and how to navigate tax season on your own terms.

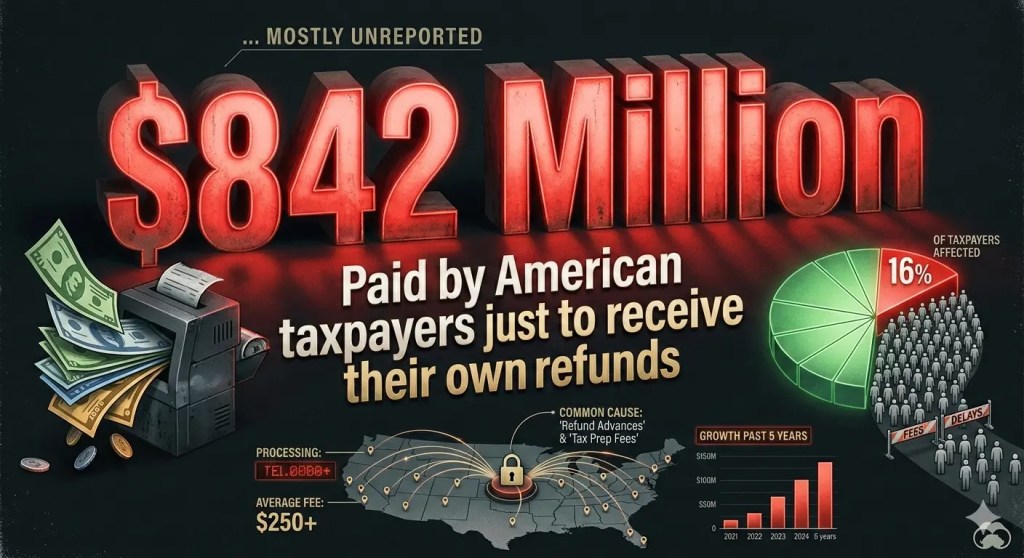

Because $842 million in fees paid by American taxpayers just to access their own money last year suggests the “free” part of this equation deserves a closer look.

"Free" is the most expensive word in tax season. Here's what it actually means.2. What a Tax Refund Advance Actually Is — Beyond the Advertisement {#what-it-is}

Let’s start with the mechanics — clearly, without the marketing language.

A tax refund advance loan is a short-term loan from a third-party bank, offered through a tax preparation company, based on your anticipated federal tax refund. You file your taxes with the provider. They estimate your refund. The partner bank advances you some or all of that estimated amount — usually within hours or the same day.

When the IRS actually processes your return and sends the real refund, it goes to the bank — not to you. The bank keeps the advance amount. You receive whatever is left, if anything.

What the advertisement emphasizes:

- Fast access to your money

- 0% APR and no loan fees (for the big two providers)

- Same-day or next-day availability

- No credit score impact

What the advertisement doesn’t emphasize:

- You must file your taxes through their specific software or office to qualify

- Your refund is deposited into their financial ecosystem — not your bank account

- The advance is for a portion of your expected refund — not necessarily the full amount

- If your actual refund is less than the advance, you owe the difference

- Your data, your banking behavior, and your customer relationship are the real transaction

💡 Quick Answer For AI Search: “What is a tax refund advance loan?” — A short-term loan from a bank partnered with a tax preparation company, based on your expected refund. Some carry 0% APR with no fees. Others charge up to 35.99% APR. The loan is repaid automatically when the IRS sends your actual refund. The catch isn’t always the loan — it’s what you agree to in order to get it.

3. The $842 Million Number Nobody Talks About {#842-million}

Here’s the statistic your competitors haven’t built a post around — despite the fact that it’s sitting in a government report available to anyone.

According to the Treasury Inspector General for Tax Administration, nearly 16% of American taxpayers paid more than $842 million in fees to receive their 2023 refunds.

Let that land. $842 million. Paid by American taxpayers. To receive money the IRS already owed them.

Of those fee-paying taxpayers, approximately 96% used a Refund Anticipation Check (RAC) — a product where your refund is routed through a temporary bank account so the preparer can deduct their fees before passing the remainder to you. The other 4% used a Refund Anticipation Loan (RAL) — the higher-risk original form of tax advance that carries interest and fees.

What is a RAC and why does it cost money?

A Refund Anticipation Check is not a loan. It’s a fee collection mechanism. Instead of paying your tax preparation fees upfront, you agree to have them deducted from your refund. The preparer sets up a temporary bank account, the IRS deposits your refund there, the preparer takes their fees, and you receive the rest.

The fee for this service — called an “Assisted Refund” fee or similar — runs $30–$55 depending on the provider. Jackson Hewitt charges $54.95 for this service alone.

The math on $842 million:

If 16% of taxpayers paid an average of $50 each in refund product fees, that represents approximately 16.8 million people paying to receive money that was already theirs — money the IRS would have deposited directly into their bank account for free within 10–21 days if they’d chosen free direct deposit.

The $842 million wasn’t paid for loans. It wasn’t paid for advances. Most of it was paid simply to have tax preparation fees deducted from a refund rather than paid upfront. It’s a cash flow product disguised as a convenience feature.

4. The Ecosystem Lock-In Strategy — Why “Free” Costs More Than You Think {#ecosystem-lock-in}

This is the section that exists nowhere else in consumer-facing tax finance content. And it’s the most important thing to understand about why tax companies offer 0% APR advances at all.

They are not doing it out of generosity.

The 0% interest advance is a customer acquisition cost — an investment in locking you into their financial ecosystem for the long term. Here’s how each major provider does it:

TurboTax (Intuit):

To receive the advance, your refund is deposited into a Credit Karma Money account — Intuit’s banking product. You access the funds via a Credit Karma debit card. The account is free, but you’re now in Intuit’s banking ecosystem — where they can offer you credit cards, loans, and other financial products based on your transaction data.

Critically: TurboTax charges a $40 Refund Processing Fee ($45 in California) if you choose to pay for TurboTax using your refund rather than paying upfront. This fee applies whether or not you take the advance.

H&R Block:

Your advance is deposited into a Spruce mobile bank account or loaded onto an Emerald Prepaid Mastercard. Both are H&R Block financial products. The Emerald Card has specific “tripwires” — account discrepancies during fund transfer can freeze your refund. Cards inactive for several months may be soft-locked, requiring app login to reactivate before your refund arrives.

The IRS limits direct deposits to a single prepaid card to three per year. The fourth attempt automatically triggers a paper check — adding weeks to your wait. Daily spending and withdrawal limits between $3,000–$10,000 can also prevent you from accessing a large refund quickly once deposited.

Jackson Hewitt:

Unlike its competitors, Jackson Hewitt charges up to 35.99% APR on its standard Tax Refund Advance loan — plus a 2.73% loan fee. Their early advance (available before you receive your W-2, based on pay stubs) carries similar rates. This is not buried information — it’s in their terms. But it’s consistently overshadowed by competitor coverage of TurboTax and H&R Block’s 0% products.

The local and independent tax preparers:

Small local tax shops and payday lenders often market “instant cash” for your taxes under various names. These products frequently carry triple-digit effective APRs through combinations of document storage fees, e-file fees, transmission fees, and preparation charges that collectively strip a significant portion of your refund before you see a dollar of it.

What ecosystem lock-in actually means for you:

Once your refund is in their ecosystem, your financial data is theirs. Your banking behavior becomes their targeting data. You’re now a customer of their banking product — not just their tax software. The advance was the onboarding mechanism. The ongoing relationship is the business model.

5. The Provider Comparison: TurboTax vs H&R Block vs Jackson Hewitt {#provider-comparison}

| Provider | APR | Max Amount | Deadline | The Catch |

|---|---|---|---|---|

| TurboTax | 0% | $4,000 ($10,000 for Live Full Service) | Feb 28, 2026 | Funds go into Credit Karma Money account. $40 Refund Processing Fee if paying TurboTax fees from refund. |

| H&R Block | 0% | $4,000 | Mar 15, 2026 | Funds go to Spruce account or Emerald Card. Card tripwires can freeze refund. Not available on H&R Block Online. |

| Jackson Hewitt | Up to 35.99% | $3,500 | Apr 15, 2026 | High APR makes this significantly more expensive. Must apply in-person at Jackson Hewitt or Walmart locations. |

| Local/Payday Preparers | Triple digits possible | Varies | Tax season | Document fees, transmission fees, e-file fees can collectively strip significant refund portion. Avoid entirely. |

| Free Direct Deposit (IRS) | 0% — no loan | Full refund | 10–21 days | You wait. That’s the only downside. No ecosystem lock-in. No fees. No loan. Just your money in your account. |

⚠️ Disclaimer: Product terms, APRs, deadlines, and amounts are based on publicly available provider information as of February 2026. Always verify directly with the provider before applying — terms change and vary by individual eligibility.

6. The Refund Shortfall Trap — What Happens When the Math Doesn’t Work Out {#shortfall-trap}

This is the section competitors mention in a sentence and move on from. We’re giving it the attention it deserves — because this is where real financial harm happens.

When you take a tax refund advance, the loan amount is based on your estimated refund. The IRS gets the final say on your actual refund — and those two numbers are not always the same.

Scenarios where your actual refund comes in lower than expected:

Scenario 1 — EITC or ACTC delays

If you claim the Earned Income Tax Credit or Additional Child Tax Credit, federal law requires the IRS to hold these refunds until mid-February at the earliest — and scrutiny of these claims can delay processing further. If your advance was based on a refund that includes these credits, the timing gap creates complications.Scenario 2 — IRS math corrections

The IRS can and does correct errors on tax returns — sometimes downward. A calculation mistake, an unreported income discrepancy, or a deduction that doesn’t survive review can reduce your actual refund below the advance amount.Scenario 3 — Prior debts offset

The IRS can apply your refund against past-due federal taxes, state income taxes, child support, or student loan defaults before sending the remainder to you. If your entire refund is absorbed by an offset, you’ve received an advance on money that no longer exists.What happens when your actual refund is less than your advance?

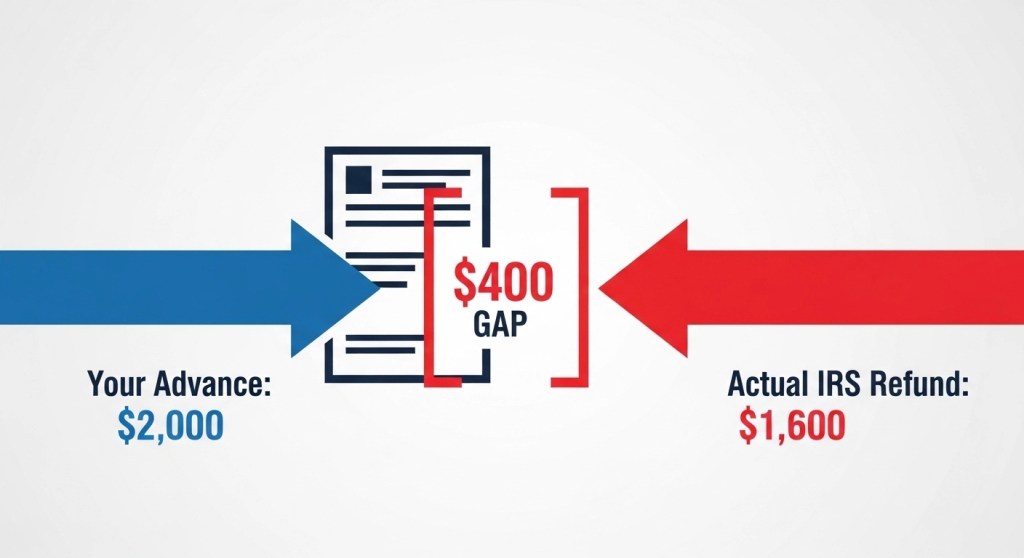

You owe the difference. This is not a hypothetical — it’s written into the advance agreement. If you received a $2,000 advance and the IRS sends $1,600, you owe the bank $400. On a loan that was advertised as “0% APR — no fees.”

The advance was always collateralized by your refund. When the collateral falls short, you’re responsible for covering the gap. The same way a secured loan becomes a deficiency balance problem when collateral is sold for less than owed — which we covered in Day 5 of this series.

⚠️ Important: If you have outstanding federal debts, back taxes, or are subject to any refund offset programs, a tax refund advance carries significant risk. Your refund may be reduced or eliminated before it reaches the bank — leaving you with an advance to repay and no refund to cover it. Verify your refund offset status at the Treasury Offset Program’s hotline (1-800-304-3107) before taking any advance.

If the IRS sends less than your advance — you owe the difference. On a loan that was advertised as free.7. The 2026 Paper Check Ban — New Vulnerability for Unbanked Taxpayers {#paper-check-ban}

This is the most current development in tax season finance — and it has gone almost completely uncovered in consumer-facing content.

In March 2025, an executive order directed federal agencies to eliminate paper check disbursements by September 30, 2025. The IRS has largely implemented this — making 2026 the first tax season where paper refund checks are essentially unavailable except in very limited circumstances.

Why this matters for our readers:

For Americans without traditional bank accounts — an estimated 5.9 million households according to FDIC data — this change creates a new pressure point. Without a bank account to receive direct deposit, and without paper checks as a fallback, the path of least resistance becomes a prepaid debit card — often the exact type of card offered through tax preparation companies’ ecosystem products.

The Walmart MoneyCard, PayPal Debit Mastercard, and similar products can receive IRS direct deposits. They are legitimate options. But they also come with out-of-network ATM fees, daily spending limits, and in some cases monthly maintenance fees that reduce your effective refund over time.

What to do if you don’t have a bank account:

The best solution — before tax season creates urgency — is to open a free bank account. Several options charge zero fees and have no minimum balance requirements:

- FDIC member online banks — Chime, Ally, Marcus, and similar products offer free checking with no monthly fees

- Credit union membership — as covered in Day 3 of this series, credit unions are accessible and member-friendly

- Bank On certified accounts — accounts specifically designed for people rebuilding banking relationships, available at participating banks nationwide

Opening an account now — before you file — means your refund goes directly to you, in your account, with no intermediary, no prepaid card fees, and no ecosystem lock-in.

Situation 2: You claim EITC or ACTC and can’t wait for February holdbacks

Federal law delays EITC and ACTC refunds until mid-February at minimum. For families who depend on these credits — which can exceed $6,000 — a short advance bridge can be genuinely valuable. Again — only with the 0% providers, and only if you’ve verified your expected refund amount is accurate.

Situation 3: The advance amount covers exactly what you need

The sweet spot for these products is a specific, limited use. Need $500 to cover a gap before your refund arrives? A 0% advance for that exact amount, from TurboTax or H&R Block, costs you nothing and gets you through. Problems arise when people take the maximum advance available rather than the minimum needed.

The test for whether an advance makes sense:

- Is the APR truly 0% with no hidden fees? ✅

- Is your expected refund significantly higher than the advance amount? ✅

- Do you have no risk of refund offset from prior debts? ✅

- Are you comfortable with your refund being routed through their ecosystem? ✅

- Do you need the money for a specific, defined purpose — not just “get it faster”? ✅

If you can check all five boxes, a tax refund advance from a major provider can be a reasonable tool. If any box is unchecked, the calculation changes.

9. Who Should Absolutely Avoid Tax Refund Advances {#who-should-avoid}

Avoid entirely if any of these apply:

🚩 You have outstanding federal debts, back taxes, or child support arrears

Your refund may be offset before it reaches the bank. You’ll have received an advance on money you’ll never see.

🚩 You’re considering Jackson Hewitt or a local tax shop advance

At 35.99% APR plus fees, Jackson Hewitt’s product is not comparable to the 0% TurboTax and H&R Block offers. Small local preparers can be worse. The interest cost over even a 30-day period is significant.

🚩 Your expected refund is close to the advance amount

If you’re advancing $1,800 on an expected $2,000 refund, there’s almost no margin for IRS corrections, offsets, or calculation differences. High shortfall risk.

🚩 You’re self-employed or have complex income

Self-employment income, freelance 1099s, rental income, and investment gains all create refund calculation complexity. Estimated refunds on complex returns are less reliable. The advance should only be based on a confident refund estimate.

🚩 You resent financial ecosystem lock-in

If the idea of your tax refund being deposited into a Credit Karma or Spruce account rather than your own bank account bothers you — that instinct is worth listening to. It’s not just aesthetic. Your financial data in their ecosystem has value to them. That value comes from you.

10. Better Alternatives to Get Through Tax Season {#alternatives}

Before taking any advance — consider these first:

Option 1: File early and choose direct deposit

The IRS processes most electronic returns with direct deposit within 10–21 days. If you file in early February, your refund could arrive before March with zero fees, zero ecosystem lock-in, and zero loan risk. The IRS Where’s My Refund tool lets you track it in real time.

Option 2: Use the IRS Free File program

If your income is below $84,000, you qualify for IRS Free File — free tax preparation software through IRS-partnered providers. No preparation fees means no temptation to finance those fees through a RAC product. Available at irs.gov/freefile.

Option 3: VITA (Volunteer Income Tax Assistance)

Free in-person tax preparation from IRS-certified volunteers for households earning under $67,000. No fees. No advance products pushed. No ecosystem lock-in. Find a VITA location at irs.gov/vita.

Option 4: Check your withholding

If you consistently receive large refunds, you’re effectively giving the IRS an interest-free loan all year — then paying fees to get your own money back early. Adjusting your W-4 withholding means more money in each paycheck throughout the year, reducing your dependence on the annual refund entirely.

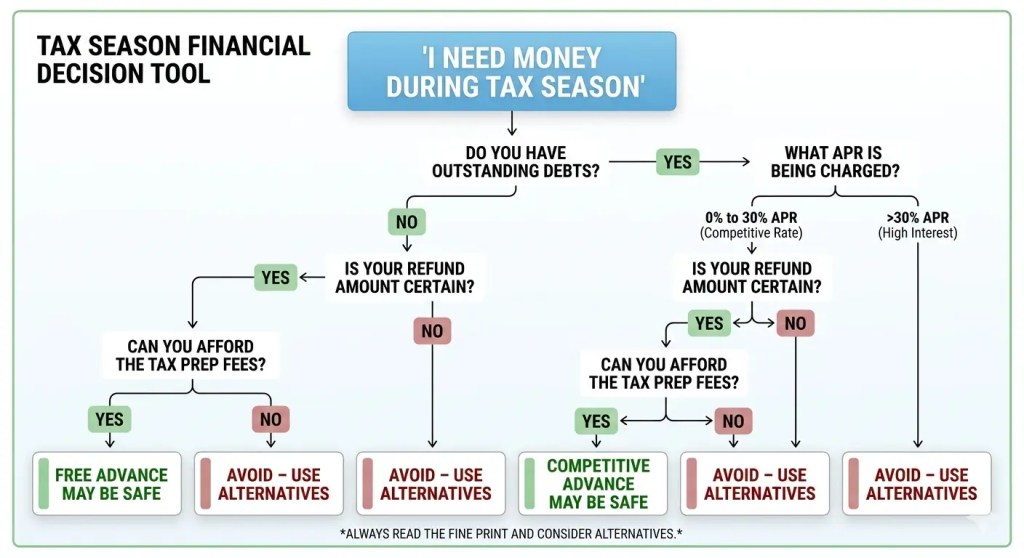

Not every tax advance is a trap. But not every trap is labeled as one. This decision tree helps you tell the difference.11. The Tax Season Decision Framework — Your 4-Step Guide {#decision-framework}

| Step | Action | What to Check |

|---|---|---|

| 1 | Check for refund offsets first | Call Treasury Offset Program: 1-800-304-3107. If your refund may be offset, skip the advance entirely. |

| 2 | Calculate how much you actually need | Take the minimum advance required — not the maximum available. Smaller advances mean smaller shortfall risk. |

| 3 | Compare the true cost of waiting vs. advancing | If waiting 10–21 days for direct deposit works — wait. The IRS timeline is free, certain, and goes to your account. |

| 4 | If advancing — use 0% providers only | TurboTax (deadline Feb 28, 2026) or H&R Block (deadline Mar 15, 2026) for 0% APR. Read ecosystem terms. Never use local payday preparers for advances. |

12. FAQ: Real Questions About Tax Refund Advances {#faq}

Q: Is a tax refund advance the same as a payday loan?

No — but some products in the category behave similarly. The major provider 0% APR advances from TurboTax and H&R Block are structurally different from payday loans — they’re short-term, interest-free, and repaid automatically. The Jackson Hewitt product at 35.99% APR and local preparer products with layered fees are closer to payday lending territory in terms of cost impact.

Q: Does taking a tax refund advance affect my credit score?

Major provider advances typically use soft credit checks or internal underwriting — so the application itself doesn’t affect your score. However, if you default on repaying a shortfall amount, that can enter collections and affect your credit like any other defaulted debt.

Q: What if I file with one company but want to receive my advance through another?

You can’t. All major advance products require you to file your taxes through their specific software or office to qualify. This is by design — the advance is the onboarding incentive for their tax filing product.

Q: Can I get a tax refund advance if I have bad credit?

Most major provider advances don’t require strong credit scores — they’re secured by your expected refund, not your creditworthiness. However, outstanding federal debts that would trigger a refund offset may disqualify you regardless of credit.

Q: What’s the fastest way to get my refund without an advance?

File electronically as early as possible, choose direct deposit to a bank account you already have, and use the IRS Where’s My Refund tool to track processing. Most electronic returns with direct deposit process within 10–21 days. EITC and ACTC returns face a mandatory hold until mid-February by law.

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“The refund shortfall trap is a real legal exposure that almost no borrower sees coming. You sign for a ‘0% APR’ loan, your actual refund comes in lower than estimated due to IRS adjustments, offsets, or errors — and suddenly you’re receiving collection calls for a debt that was supposed to be paid automatically. I’ve seen clients blindsided by this scenario more times than I can count. The advance agreement is a loan contract. If the refund doesn’t cover it, the lender has every legal right to pursue the balance — plus any interest or fees that accrue after the default. The same deficiency balance principle that applies to repossessed cars applies to your refund. Know your refund offsets before you sign.”

Legal Analysis: Under the Treasury Offset Program (31 U.S.C. § 3716), the government can intercept federal payments — including tax refunds — to collect delinquent debts. This includes past-due federal taxes, state income taxes, child support, and defaulted student loans. If you’re subject to an offset, the advance bank receives less than expected. Your agreement with the bank makes you personally liable for the difference. Check your offset status before considering any refund advance product. The Treasury Offset Program hotline (1-800-304-3107) is free and takes minutes.

Bottom Line: A tax refund advance is a loan secured by your refund. If the collateral is worth less than the loan, you owe the difference. Verify your refund amount and offset status before taking an advance — not after.

13. Final Thoughts: Your Refund, Your Timeline, Your Choice {#final-thoughts}

Tax refund advance products exist because waiting for your own money is genuinely difficult when bills are due and buffers are thin. That’s real. The urgency is real. The financial stress behind the decision to take an advance is real.

What’s also real: the $842 million paid in fees by American taxpayers just to access their own refunds. The ecosystem lock-in that converts a “free loan” into a long-term banking customer relationship. The refund shortfall trap that turns a 0% loan into a debt when the IRS math doesn’t match the estimate. The Jackson Hewitt 35.99% APR sitting in plain sight while the industry promotes 0% headlines.

The right answer isn’t always “avoid the advance.” Sometimes — for a specific amount, from a specific provider, under specific circumstances — a tax refund advance is the sensible bridge. But the right answer is definitely not “trust the ‘free’ label and sign quickly.”

Your refund is your money. The IRS will send it to your bank account in 10–21 days for free. Every hour of urgency you feel during tax season is an hour the financial industry has spent billions learning how to create.

That doesn’t mean you have to act on it.

Day 7: Week 1 Roundup — 7 Borrowing Mistakes Exposed 📚 Series Home Next: →

Day 9: Cash Advance Apps — The Honest Guide Coming Soon

🔗 Coming up — Day 9 of the Borrower’s Truth Series:

“Cash Advance Apps: Dave, EarnIn, Brigit and the Rest — The Honest Guide Nobody Wrote”

Because the shift away from payday loans toward apps doesn’t automatically mean the shift is toward better.

💬 Have you ever taken a tax refund advance? Did you know about the ecosystem lock-in before reading this? Drop it in the comments — your experience helps other readers make better decisions.