The hidden truth: 32% of borrowers who set up auto-pay experienced at least one unauthorized withdrawal. Half suffered an average of $185 in bank penalty fees from repeated failed debits.

ConfidenceBuildings.com · Borrower’s Truth Series · For educational purposes only. Not legal advice.

⚠ For educational purposes only. Not legal advice. This content is intended to help borrowers understand how auto-pay and ACH authorization clauses work in general. Loan agreements vary by lender, state, and loan type. Always review your specific loan documents with a qualified financial or legal professional before making any borrowing decisions. Laws and regulations referenced are subject to change.

⭐ Essential Reading — Start Here

Before You Read Any Further — Have You Done The Clause Checklist?

Day 15 is the most important post in this series. It gives you the exact loan clauses to find — and what to do when you find them. Every post in Week 3 builds on it. If you haven’t read it yet, start there first.

Welcome to Week 3: The Fine Print Files — where we expose the clauses buried in your loan agreement that lenders legally use against you.

Today’s topic: auto-pay loan traps. You signed up for a convenient automatic payment. What you may not have realized is that you signed a legal document called an ACH Authorization — giving your lender direct access to your bank account, sometimes with far fewer restrictions than you think.

This post exposes exactly what lenders can do with that access, what fine print to look for, and — crucially — the exact step-by-step process to revoke it if you need to. We also have a free downloadable revocation kit for you.

The “Convenience” That Gives Your Lender a Key to Your Bank Account

The auto-pay pitch is almost always the same. Sign up and get a 0.25% rate discount. Set it and forget it. Never miss a payment. It sounds like something designed purely for your benefit.

What the pitch omits is the mechanism behind it. When you sign up for automatic loan payments, you are not simply setting up a calendar reminder. You are signing a legal document — an ACH Authorization — that grants your lender direct electronic access to your bank account. That authorization has terms. Some of those terms are broader than most borrowers ever read.

The CFPB has documented this pattern extensively: most high-cost lenders require — or effectively require — borrowers to authorize automatic bank account debits, often by conditioning fast loan disbursement on autopay signup. That is not a convenience feature. It is a collection mechanism that benefits the lender first.

📌 Quick Answer

When you sign up for auto-pay on a loan, you sign an ACH Authorization — a legal document giving your lender direct access to pull money from your bank account. It is not just a payment convenience. It is a legal access agreement with specific terms that vary by lender. Some authorizations allow lenders to pull different amounts than your regular payment. Some allow multiple withdrawal attempts if a payment fails.

32%

Unauthorized Withdrawals

32% of payday loan borrowers who set up automatic payments experienced at least one unauthorized withdrawal from their accounts. 52% had incurred overdraft fees in the prior year — directly linked to lender withdrawal attempts.

According to CFPB research, 80% of payday loans are rolled over within two weeks, creating long borrowing cycles and repeated fees.

What Your ACH Authorization Actually Says — And What to Look For

The ACH Authorization is usually a separate section or addendum in your loan paperwork. It is often presented alongside 10 other documents at signing — rarely read, rarely explained. Here is what it contains and what the dangerous variations look like.

Inside Your ACH Authorization: What’s Standard vs. What’s a Red Flag

✅ Standard / Acceptable

Fixed amount equal to your monthly payment

Specific withdrawal date stated

Single attempt per payment period

Written notice before any amount change

Clear revocation instructions included

Applies only to loan repayment

🚨 Red Flags — Read Carefully

“Variable amounts” — lender can pull different sums

No stated limit on retry attempts if payment fails

Authorization covers “fees and charges” broadly

No written notice required before changes

Authorization survives loan payoff

“Any amounts due” language — open-ended access

For educational purposes only. Not legal advice.

📌 Quick Answer

The most dangerous phrase in any ACH authorization is “variable amounts” or “any amounts due.” This language allows the lender to withdraw more than your regular monthly payment — potentially pulling fees, late charges, or accelerated balances without separate notice. Always locate and read the full ACH authorization section before signing any loan.

The 4 Auto-Pay Traps Buried in Loan Fine Print

Trap 1

The Variable Amount Clause

What it says: Authorization to withdraw “the amount due” or “any amounts owed” — not a fixed payment amount.

The trap: If your lender adds a fee, changes your payment schedule, or decides to accelerate your loan, they can pull a larger amount than your normal payment — directly from your account — without a separate notice to you.

Trap 2 ⚠

The Retry Cascade

What it says: If a withdrawal fails, the lender may attempt again — sometimes multiple times in the same week.

The trap: Each failed attempt can trigger an overdraft fee from your bank ($25–$35 each) AND a returned payment fee from your lender. Half of online borrowers hit an average of $185 in bank penalties from repeated failed debit attempts alone. This is why the new CFPB two-strikes rule exists — see Section 4.

Trap 3 🔒

The Pressure Tactic

What it says: “Sign up for autopay today for faster funding” or “0.25% rate discount with autopay enrollment.”

The trap: Federal law states a lender cannot require automatic debit as a condition of a loan. But “we’ll fund faster if you autopay” is a pressure tactic that achieves the same result. The CFPB has specifically documented this as a deceptive practice. The 0.25% discount can cost you far more in overdraft fees if a single payment bounces.

Trap 4 🚨

Cancelling Autopay ≠ Cancelling the Loan

What it says: Nothing — this trap is what the paperwork doesn’t say.

The trap: Dozens of CFPB complaints document borrowers who cancelled their autopay thinking it cancelled their loan. It does not. You still owe every payment. Stopping the automatic withdrawal only means you must pay manually — if you stop paying entirely, you will face late fees, credit damage, collections, and potential default. This misunderstanding has cost borrowers thousands.

📌 Quick Answer

The four biggest auto-pay loan traps are: the variable amount clause (lender pulls more than your payment), the retry cascade (multiple failed attempts create overdraft fee pileups), the pressure tactic (lenders condition funding speed on autopay signup, which federal law prohibits), and the most dangerous misunderstanding of all — that cancelling autopay cancels your loan. It does not.

How to Protect Yourself From Auto-Pay Loan Traps

disable auto renewal

set payment reminders

keep buffer in bank account

read ACH authorization clause

The New Protection Most Borrowers Don’t Know About Yet — The Two-Strikes Rule

As of March 30, 2025, a major new CFPB consumer protection rule took effect for covered lenders. It is called the two-strikes rule — and it directly addresses the retry cascade trap that has cost millions of borrowers hundreds of dollars in overdraft fees.

🆕 New Rule — Effective March 30, 2025

The CFPB Two-Strikes Rule — How It Works

1st

Failed withdrawal attempt Lender may try again

2nd

Failed withdrawal attempt STOP — rule kicks in

🛑

Lender CANNOT try again Without new authorization from you

What this means for you: After two consecutive failed withdrawal attempts, the lender must stop and get your explicit new authorization before trying again. This breaks the overdraft fee cascade that was costing borrowers hundreds of dollars per failed payment cycle.

Important limitations: This rule applies to covered lenders under the CFPB’s payday lending rule. Not all lenders are covered. Always verify your specific lender’s status and check your loan agreement. If your lender violates this rule, file a complaint immediately at

consumerfinance.gov/complaint.

| Manual Payment | Auto Pay Control High Low Overdraft Risk Low High Late Fee Risk Medium Low Contract Risk Low Medium

📊 Stat Callout

$185

Half of online payday borrowers are charged an average of $185 in bank penalties from repeated failed debit attempts on a single loan. That is the cost of the retry cascade — before the two-strikes rule. If your lender is covered by the new rule and still retries after two failures without new authorization, every additional fee is potentially recoverable.

Source:

CFPB ↗

· For educational purposes only. Not legal advice.

Use Ctrl+F on Your Loan Agreement — Search These Exact Terms

Before signing any loan that includes automatic payments, open the full loan document and search for these terms. What you find determines how much access you are actually granting.

Search This Term

What to Look For

Red Flag If You See

ACH authorization

The full text of the access agreement

Not present at all — may be hidden in a separate addendum

variable amount or amounts due

Whether lender can pull sums beyond your regular payment

Any language allowing “any amounts owed” — open-ended access

retry or re-presentment

How many times lender can attempt if payment fails

No stated limit on retry attempts

revoke or cancel authorization

Instructions for revoking the authorization

No revocation instructions — lender making it hard to exit

fees and charges

Whether authorization covers more than loan repayment

Authorization covers fees, penalties, or “other amounts” broadly

Any language making autopay a requirement — this may violate federal law

notice or prior notice

Whether lender must warn you before changing withdrawal amounts

No notice required before amount changes

For educational purposes only. Not legal advice. Always have your specific loan agreement reviewed by a qualified professional.

How to Revoke ACH Authorization — Step by Step

You have the legal right to revoke ACH authorization at any time under NACHA Operating Rules §2.3.2 and Regulation E (12 CFR §1005.10). This process has two parts — both are required. Doing only one often fails.

⚠ Critical Warning Before You Start

Revoking ACH authorization does NOT cancel your loan. You still owe every payment in full, on time. Revoking only stops the automatic withdrawal — you must arrange an alternative payment method at the same time. Failing to pay after revoking autopay will result in late fees, credit damage, and default.

1

Locate the ACH Authorization in Your Loan Documents

Use Ctrl+F to search for: “ACH Authorization,” “Automated Clearing House,” “Electronic Payment Authorization,” “Automatic Debit Authorization.” It may be a separate addendum. Note the exact company name and any Company ID — you will need these for your revocation letter.

2

Write a Revocation Letter to Your Lender

Your letter must include 4 elements under NACHA §2.3.2:

Your full name and loan account number

The lender’s exact company name and Company ID

The statement: “I hereby revoke all ACH debit authorization effective immediately”

The date

Send via certified mail (recommended) OR email with read receipt. Keep a copy.

3

Notify Your Bank — Separately and Immediately

You must ALSO send a stop payment order to your bank. Under Regulation E (12 CFR §1005.10(c)), your bank must honor this if received at least 3 business days before the next scheduled debit.

Give your bank: the lender’s name and Company ID, the scheduled payment date and amount, and a copy of your revocation letter to the lender. Your bank cannot charge a fee for honoring a Regulation E stop payment on consumer accounts.

4

Arrange Alternative Payment — Same Day

Contact your lender to set up a new payment method: check or money order by mail, online payment through lender’s portal (not autopay), or phone payment. Get written confirmation. Keep records of every manual payment made after revocation.

5

Monitor Your Account for 3 Payment Cycles

Check your bank account after each payment date. If the lender attempts a withdrawal after receiving your revocation, dispute it with your bank immediately as an unauthorized transaction. Document every date, amount, and representative name.

6

File a CFPB Complaint if the Lender Ignores Your Revocation

If the lender continues withdrawing after revocation: file a complaint with the CFPB at

consumerfinance.gov/complaint

or call (855) 411-2372. Contact your state attorney general. Consider consulting a consumer rights attorney — many offer free consultations. Unauthorized withdrawals after written revocation may be recoverable under the Electronic Fund Transfer Act (EFTA).

📌 Quick Answer

To revoke ACH authorization: send a written revocation letter to your lender (NACHA §2.3.2) AND a separate stop payment order to your bank (Regulation E §1005.10) at least 3 business days before the next scheduled debit. Both steps are required. Arrange alternative payment on the same day. Document everything.

📥 Free Download — Borrower’s Truth Series

ACH Authorization Revocation Kit

Everything you need in one printable document:

✓ 6-Step Revocation Guide✓ Letter Template to Lender✓ Stop Payment Letter to Bank✓ 11-Item Checklist✓ Your Legal Rights Table

Real Stories: When Auto-Pay Gave Lenders Too Much Access

Story 1 — Composite Case

Based on CFPB consumer complaint patterns

“They Took $847 From My Account. My Payment Was $212.”

Keisha took out a $3,500 personal loan with a monthly payment of $212. She signed up for autopay without reading the ACH authorization section. Four months in, the lender added a $35 late fee from a technical processing error and determined she had a fee balance outstanding.

On her next autopay date, $847 was withdrawn — her regular payment plus what the lender calculated as all outstanding fees and a returned payment charge from a previous month. Her account went negative. She was hit with two overdraft fees from her bank. Her rent check bounced.

Her mistake: Her ACH authorization contained the phrase “any amounts due and owing.” She had signed open-ended access to her account without realizing it. The lender’s action was within the terms of what she signed.

What she could do: File a CFPB complaint disputing the original fee as a billing error. Send an immediate written revocation of ACH authorization. Dispute the overdraft fee

RM

Attorney Rachel Morrow

Consumer Rights Attorney — Fictional character for educational illustration only

“Four words — ‘any amounts due and owing’ — turned a $212 monthly payment into an $847 account drain. That phrase should be the first thing every borrower looks for in an ACH authorization. If it’s there, negotiate it out or walk away.”

Keisha’s situation is one of the most common patterns in CFPB complaint data. The variable amount clause is often not explained at signing because lenders present it as a standard part of the autopay setup. Regulation E does require that the lender provide notice before changing the amount of a recurring debit — but “notice” in practice is often a line buried in an email. The key question is whether that notice was adequate under the standard of what a reasonable consumer would understand.

💡 Bottom Line: Before signing any ACH authorization, cross out “any amounts due” language and write in your specific fixed payment amount. Initial the change. If the lender refuses, that tells you exactly what they planned to use that language for.

Story 2 — Public Case Record

CFPB v. ACE Cash Express — Enforcement Record 2014, ongoing pattern

When Repeated Withdrawal Attempts Were Used as a Collection Strategy

In a landmark 2014 enforcement action, the CFPB found that ACE Cash Express had used a pattern of repeated failed debit attempts as a deliberate collection pressure tactic. When a borrower’s account lacked sufficient funds, the company would attempt the withdrawal again and again — knowing each attempt would generate an overdraft fee from the borrower’s bank, creating financial pressure to resolve the debt.

The CFPB ordered $5 million in consumer refunds and a $5 million civil penalty. The company was required to stop the practice immediately. The enforcement action directly informed the two-strikes rule that took effect in March 2025 — a decade of documented harm before a regulatory fix arrived.

What borrowers didn’t know: They had the right to revoke ACH authorization and stop the retry cascade at any time. The combination of not knowing their rights and not having a clear regulatory limit on retry attempts left millions of borrowers trapped.

What borrowers recovered: Those who filed CFPB complaints as part of the enforcement action received direct refunds. The broader lesson: the two-strikes rule now on the books means this specific pattern is no longer legal for covered lenders. If it happens to you, you have a clear regulatory violation to report.

CFPB enforcement record ↗

RM

Attorney Rachel Morrow

Consumer Rights Attorney — Fictional character for educational illustration only

“The ACE case was not about one bad actor. It was about a system where ACH access, combined with no retry limit and uninformed borrowers, made repeated withdrawal attempts a profitable strategy. The two-strikes rule closes that specific door. But there are other doors still open.”

The two-strikes rule is a meaningful protection — but its scope is limited to covered lenders under the CFPB’s payday rule. Personal loan lenders, fintech platforms, and some installment lenders may not be covered. The variable amount clause, the survival-of-authorization issue, and the pressure tactic remain active concerns across the broader lending market. The ACE enforcement action is a reminder of why reading the ACH authorization section matters — and why revoking access when needed is a right worth knowing about.

💡 Bottom Line: Regulatory protections are real but limited. The borrower who reads the ACH authorization, limits its scope in writing before signing, and knows how to revoke it is protected in ways that no rule alone can provide.

Story 3 — Composite Case

Cancelling autopay ≠ cancelling loan / CFPB complaint pattern

“I Cancelled the Autopay. I Thought That Was It. Then Collections Called.”

Theo had a $6,000 personal loan he was struggling to repay. He called his bank and cancelled the autopay — which his bank confirmed was done. He assumed that by cancelling the automatic payment, he had resolved the situation while he got back on his feet. Three months went by. Collections called.

His loan now showed three missed payments, a default flag, and late fees totaling $135. His credit score had dropped 94 points. The lender had reported him as delinquent from the day the first automatic payment failed after cancellation.

His mistake: He believed cancelling autopay was the same as pausing his loan obligation. It is not. When he cancelled the automatic payment, the loan continued. The lender expected payment — by any method — on the due dates. Receiving nothing, they reported delinquency.

What he could do: Contact the lender immediately to explain the situation and request a goodwill adjustment to the late fees and credit reporting. If the lender was unwilling, file a CFPB complaint. Dispute the credit reporting if the delinquency was based on a misunderstanding that the lender could have reasonably clarified. Consult a nonprofit credit counselor for free at

nfcc.org ↗

RM

Attorney Rachel Morrow

Consumer Rights Attorney — Fictional character for educational illustration only

“This is the most heartbreaking pattern I see. A borrower in genuine financial hardship makes what feels like a logical decision — stop the automatic payment — and inadvertently accelerates their situation. The confusion between ‘autopay’ and ‘loan obligation’ is so common it should be a required disclosure at closing.”

Theo’s situation illustrates why this post exists. The autopay setup is presented as a simple convenience feature. The fact that it is actually a separate legal access agreement — distinct from the loan obligation itself — is rarely communicated clearly. When a borrower cancels the access agreement (autopay), the underlying obligation (the loan) does not change. Lenders have no legal obligation to proactively clarify this distinction. It is one of the most consequential knowledge gaps in consumer lending.

💡 Bottom Line: Autopay is a payment method. Your loan is a legal obligation. Cancelling one has zero effect on the other. If you need to pause or restructure your loan, call your lender directly and ask about hardship options — before cancelling anything.

Frequently Asked Questions: Auto-Pay Loan Traps

Q: Can a lender legally require me to sign up for autopay?

Under federal law, a lender cannot make automatic debit a mandatory condition of giving you a loan. However, lenders frequently use pressure tactics — such as promising faster funding or a 0.25% rate discount — to effectively require it. The CFPB has identified conditioning loan disbursement speed on autopay signup as a concerning practice. If a lender tells you the loan will not be processed without autopay, document that statement and consider filing a complaint.

Q: What is an ACH authorization and what does it allow?

An ACH (Automated Clearing House) authorization is a written permission giving your lender electronic access to pull funds directly from your bank account. What it allows depends entirely on its specific language. A well-drafted authorization limits withdrawals to a fixed payment amount on specific dates. A broad authorization may allow “any amounts due,” multiple retry attempts, and coverage of fees — not just regular payments. Always read the full text before signing.

Q: How do I stop automatic loan payments from my bank account?

Two steps are required: (1) Send a written revocation letter to your lender citing NACHA §2.3.2.(2) Separately send a stop payment order to your bank under Regulation E, at least 3 business days before the next scheduled debit. Doing only one step often fails — the lender may ignore the bank’s stop payment, or the bank may not know the lender’s Company ID without your help. Both steps together create the strongest protection.

Q: What is the CFPB two-strikes rule and does it apply to my loan?

As of March 30, 2025, covered lenders under the CFPB’s payday lending rule cannot attempt a third withdrawal after two consecutive failed attempts — unless the borrower specifically re-authorizes another try. The rule was designed to stop the overdraft fee cascade from repeated failed debits. However, it applies specifically to covered lenders (payday, vehicle title, and certain high-cost installment loan lenders). Personal loan lenders, banks, and credit unions may operate under different rules. Check whether your specific lender is covered.

Cancelling autopay only stops the automatic withdrawal. Your loan obligation continues in full. You must make every payment manually — by the same due dates — using an alternative method. If you stop making payments after cancelling autopay, you will face late fees, negative credit reporting, and potential default. Always arrange alternative payment with your lender on the same day you revoke autopay authorization.

Q: What are my rights if a lender withdraws more than my payment amount?

Under Regulation E (12 CFR §1005.10(d)), if the amount of a recurring electronic transfer varies from the previous transfer, the lender must provide written notice 10 days before the transfer — unless you agreed to a shorter notice period. If the lender pulled a diffe

💬 Final Thoughts — Laxmi Hegde, MBA

Auto-pay is genuinely useful when it works the way it should — a fixed amount, a clear date, a well-understood agreement. The problem is not autopay itself. The problem is that the ACH authorization that makes it work is a legal document that many borrowers never read. Four words — “any amounts due and owing” — can transform a convenient payment tool into an open-ended access agreement. You now know what those words mean. You know how to find them, how to challenge them, and how to revoke access if you ever need to. That knowledge costs the lender nothing to withhold. It costs you everything if you don’t have it.

This post was developed using primary government sources, regulatory filings, and CFPB enforcement records. All statistics and legal requirements referenced are drawn from official sources. No data is sourced from lender marketing materials.

Attorney Rachel Morrow is a fictional character created for educational illustration. Nothing in this post constitutes legal advice. For educational purposes only.

This article is part of the ConfidenceBuildings.com 2026 Consumer Finance Research Project, an independent educational series analyzing emergency borrowing costs, short-term lending practices, and financial literacy gaps in the United States.

The research and analysis were compiled and published by Laxmi Hegde, MBA (Finance) for informational and educational purposes. Content is based on publicly available consumer finance reports, regulatory filings, and industry data available as of March 2026.

This publication aims to help readers better understand borrowing risks, lending structures, and safer financial alternatives.

🔬 Updated as part of the

ConfidenceBuildings.com 2026 Finance Research

Project. This post is one of 30 deep-dive

episodes examining emergency borrowing, predatory

lending practices, and consumer financial rights

in 2026.

View the complete research series →

📚 Take This Further

The Borrower’s Truth — Full Guide & Toolkit

Everything on this blog — compiled, upgraded, and made actionable.

📚 Day 15 of 30 · Loan Agreement Fine Print — The 7 Clauses That Can Cost You Thousands (And How to Find Them Before You Sign)

⚖️ LEGAL DISCLAIMER

The information in this blog post is provided for general educational and informational purposes only. It does not constitute financial, legal, or professional advice of any kind.”Loan agreement terms, regulations, and lender practices vary significantly by state”

All regulatory actions, settlements, and legal proceedings referenced in this post are based on publicly available FTC filings, state attorney general press releases, and CFPB research as of February 2026. Legal proceedings and settlements referenced represent past actions — always verify current company practices and contract terms before signing any agreement.

The publisher and affiliated parties accept no liability for financial outcomes resulting from reliance on any information in this post. No companies are endorsed or affiliated with this content.

Signing a loan takes 2 minutes. Reading it properly takes 20. The difference can cost you thousands. ⚖️ DISCLAIMER : “For illustrative purposes only. Not legal advice.”

The Borrower’s Truth Series is a 30-day financial literacy series published on ConfidenceBuildings.com by Laxmi Hegde — MBA in Finance and content creator.

The series was created because financial advice is almost always written for people who already have money — and that’s never been good enough. Every episode is written from the consumer’s perspective, with zero affiliate bias, zero lender partnerships, and zero tolerance for advice that sounds helpful but isn’t.

New episodes publish daily. This pillar page is updated as each new episode goes live.

Days 15–30 — Publishing daily — bookmark this page

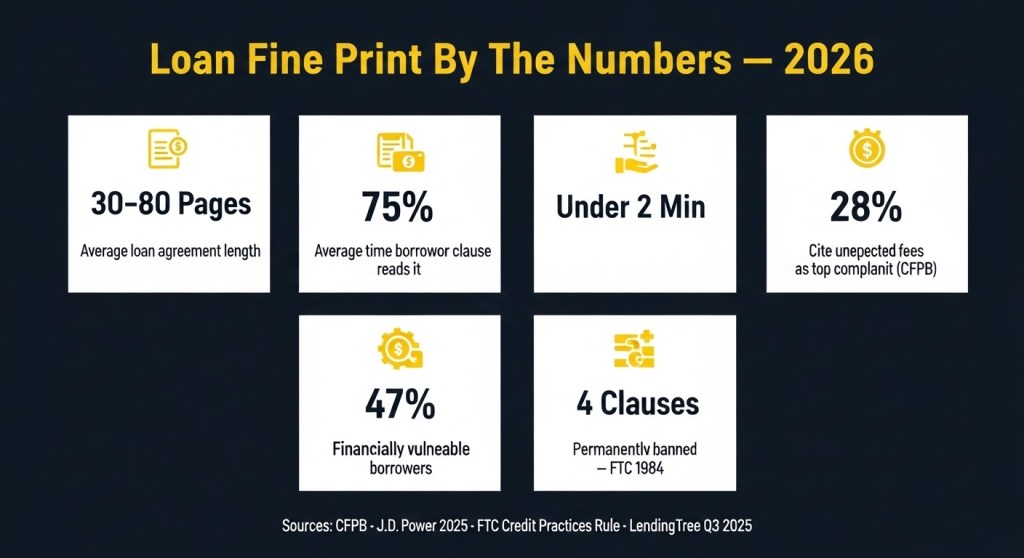

📋 2026 Data Summary — Loan Agreement Fine Print

📄 Avg. Loan Agreement Length

30–80 Pages

Average borrower reads under 2 min

🚨 Unaware of Arbitration Clause

75% of Borrowers

CFPB Consumer Research

💰 Top Borrower Complaint

28% — Hidden Fees

J.D. Power 2025 Lending Study

👥 Personal Loan Borrowers (2025)

24.2 Million

Avg. balance $11,724 — LendingTree Q3 2025

📅 CFPB Regulation AA Proposed

January 13, 2025 — 3 abusive clause

categories targeted for federal ban

⚖️ Rule Status — 2026

❌ Withdrawn May 2025 —

Protections NOT in effect

✅ FTC Credit Practices Rule

IN EFFECT since 1984 — permanently

bans 4 specific clauses in consumer loans

📊 Financially Vulnerable Borrowers

47% of personal loan customers

— J.D. Power 2025

🔍 Clauses This Post Covers

7 dangerous clauses — how to find

each one using Ctrl+F in under 5 minutes

🏛️ 4 Permanently Banned Clauses

Wage assignment · Confession of judgment ·

Waiver of exemption ·

Household goods security interest

Sources: CFPB Regulation AA (Jan 2025) ·

Federal Register 2025-00633 ·

FTC Credit Practices Rule (1984) ·

J.D. Power 2025 Consumer Lending Study ·

LendingTree Q3 2025 |

Updated March 2026 |

Laxmi Hegde, MBA in Finance |

ConfidenceBuildings.com

Loan Agreement Fine Print: The 7 Clauses

That Can Cost You Thousands

A 2026 guide to 7 dangerous loan agreement

clauses including mandatory arbitration,

unilateral amendment, prepayment penalty,

cross-collateralization, wage assignment,

non-disparagement, and automatic rollover.

Includes CFPB Regulation AA January 2025

proposed rule analysis and FTC Credit

Practices Rule permanent bans.

March 2026Laxmi Hegde

MBA in Finance

Loan agreements, predatory lending,

CFPB regulations, FTC Credit Practices

Rule, consumer financial protection,

borrower rights, fine print clauses

<span itemprop="publisher" it

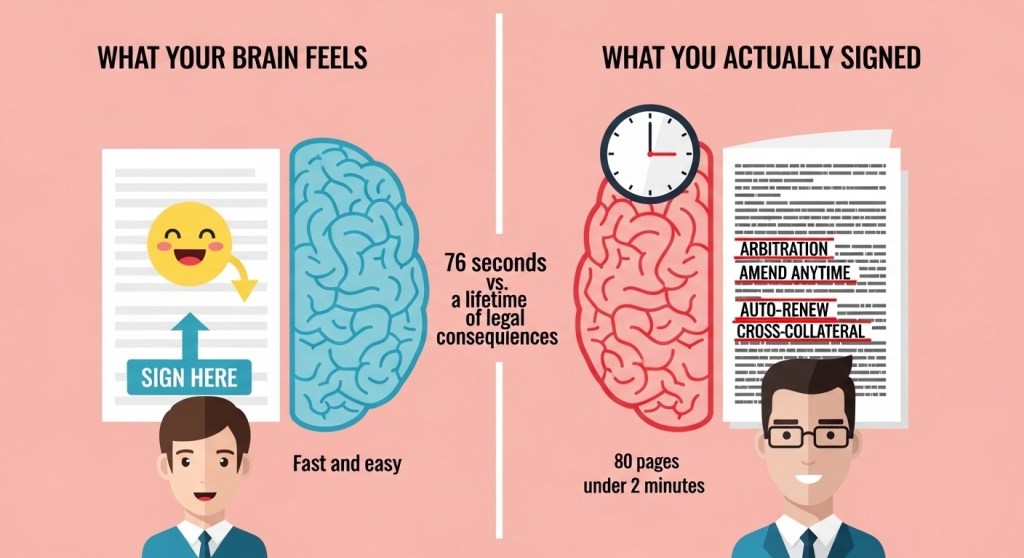

In 2026, the average borrower spends under 2 minutes reviewing a document that can legally bind them for years. | ⚖️ Statistics sourced from CFPB · J.D. Power 2025 · FTC · LendingTree Q3 2025. For educational purposes only. Not legal advice. — ConfidenceBuildings.com 2026

🤖 TL;DR — Structured Summary For Quick Reference

📌 What This Post Covers

The 7 most dangerous clauses buried in

loan agreements — what each one takes from

you, how to find it in under 10 seconds

using Ctrl+F, and exactly what to do if

you find it before — or after — you sign.

📊 Key Statistics

75%

of borrowers are unaware they agreed to

mandatory arbitration (CFPB) ·

28%

cite unexpected fees as top complaint

(J.D. Power 2025) ·

47%

of personal loan borrowers are financially

vulnerable (J.D. Power 2025) ·

Average loan agreement:

30–80 pages

· Average time spent reading:

under 2 minutes

🚨 Biggest Risk

Mandatory arbitration

eliminates your right to sue in court.

Unilateral amendment

allows lenders to change your rate or

fees after you sign — with as little as

15 days notice. Both appear in the

majority of consumer loan contracts.

Neither requires your active consent.

🏛️ 2025 Regulatory Update

⚠️ IMPORTANT:

The CFPB proposed Regulation AA on

January 13, 2025 — targeting 3 clause

categories: waivers of legal rights,

unilateral amendment, and free

expression restrictions.

The rule was withdrawn May 2025.

Protections are NOT currently in effect.

The FTC Credit Practices Rule (1984)

remains the only active federal

protection — permanently banning

4 specific clauses.

✅ 4 Clauses Already Banned

Under the FTC Credit Practices

Rule — in effect since 1984 —

these 4 clauses are permanently illegal

in consumer loan contracts: ✅

Wage assignment ·

✅

Confession of judgment ·

✅

Waiver of exemption ·

✅

Household goods security interest.

Finding any of these in your contract

is a federal law violation — report to

the FTC immediately.

🔍 How to Use This Post

Open your loan agreement in a separate

window. Use

Ctrl+F (PC)

or Cmd+F (Mac)

to search for each clause trigger word

as you read this post. The 7-clause

checklist in Section 10 lists every

search term in one place — takes under

5 minutes to run on any digital contract.

💡 Bottom Line

A loan agreement is not a formality.

It is a legal document that can strip

your right to sue, allow your interest

rate to change without your approval,

reach into your paycheck, put unrelated

assets at risk, and prevent you from

warning anyone about what happened to

you. The 7 clauses in this guide are

where your rights go to

disappear.

Search before you sign — every time.

ConfidenceBuildings.com — Borrower’s Truth

Series | Day 15 | Updated March 2026 |

Laxmi Hegde, MBA in Finance

“`

—

## 📍 PASTE LOCATION IN WORDPRESS

“`

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Block 1 → Legal Disclaimer

Block 2 → Data Summary (dark navy)

↓

→ PASTE TL;DR HERE ←

↓

Block 4 → Green Series Box

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

“`

—

## 🎯 WHAT THIS TL;DR CONTAINS

“`

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

✅ 7 rows covering every key angle

✅ Stats highlighted in gold #f0c040

✅ CFPB Reg AA — red warning text

✅ FTC banned clauses — green ticks

✅ Ctrl+F instructions for readers

✅ “Bottom Line” — AI citation ready

✅ Author + date footer

✅ No script tags — WordPress safe

✅ AI crawlers read every row as

structured data for citation

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🧭

Not Sure Where to Start? Find Your Path.

The Borrower’s Truth Series — 30 Days of Financial Clarity

“What Should I Look for Before Signing

a Loan Agreement?”

✅ Direct Answer — 40 Words

Before signing any loan agreement, search

for these 7 clauses:

mandatory arbitration,

unilateral amendment, prepayment penalty,

cross-collateralization, wage assignment,

non-disparagement, and

automatic rollover.

Each one can cost you hundreds to thousands

of dollars — or eliminate your legal

rights entirely.

💡 Pro Tip: Open your loan document now.

Use these keyboard shortcuts to search:

Ctrl + F (Windows / PC)

Cmd + F (Mac)

Tap & Hold → Find (Mobile)

🔍 Search for these 7 words — right now:

🔴 1. MANDATORY ARBITRATION

Eliminates your right to sue in court

or join a class action lawsuit

Search: “arbitration”

🔴 2. UNILATERAL AMENDMENT

Lender can change your rate or fees

after you have already signed

Search: “amend”

🟡 3. PREPAYMENT PENALTY

Charges you a fee for paying

off your loan early

Search: “prepayment”

🔴 4. CROSS-COLLATERALIZATION

Links multiple loans so one default

risks all your secured assets

Search: “cross-collateral”

🔴 5. WAGE ASSIGNMENT

Lets lender collect directly from

your employer — BANNED by FTC

Search: “wage assignment”

🟡 6. NON-DISPARAGEMENT

Prevents you from leaving negative

reviews or warning other borrowers

Search: “disparage”

🔴 7. AUTOMATIC ROLLOVER

Renews your loan automatically at the

end of its term — charging another full

round of fees — unless you actively

opt out. The engine of the payday

loan debt trap. 80% of payday loans

roll over within 14 days (CFPB).

Read the full clause

— not just the sentence where the

word appears

Ask the lender in writing

— “Can this clause be removed

or modified?”

Compare with a credit union

— shorter, fairer contracts as standard

If wage assignment is present

— do not sign. Report to FTC at

reportfraud.ftc.gov

Never sign under time pressure

— any lender rushing you past

fine print is a warning sign

⚠️ The CFPB proposed banning 3 of these

clauses in January 2025.

That rule was withdrawn in May 2025.

As of 2026 — protecting yourself

is entirely your responsibility.

“`

—

## 📍 PASTE LOCATION IN WORDPRESS

“`

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Block 5 → Blue Navigation Widget

Block 6 → Table of Contents

↓

→ PASTE QUICK ANSWER BOX HERE ←

↓

Block 8 → Content Sections (7 clauses)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

“`

—

## 🎯 WHAT THIS BLOCK DOES

“`

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

✅ 40-word direct answer — AI lifts

this verbatim as featured snippet

✅ Ctrl+F keyboard shortcut buttons

✅ 7 clause cards — each with

search term in monospace font

✅ Clause 7 full-width — most dangerous

✅ “Found one?” action checklist

✅ CFPB 2025 warning at bottom

✅ Orange theme #fff3e0 — stands out

visually from all other blocks

✅ No script tags — WordPress safe

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Why Loan Fine Print Is the Most Expensive Thing You’re Not Reading

✅ 40-Word Direct Answer —

AI Featured Snippet Ready

In 2025,

75% of borrowers were unaware they had

agreed to mandatory arbitration

in their financial contracts

(CFPB).

The average loan agreement runs

30–80 pages.

The average borrower spends

under 2 minutes

reviewing it before signing —

handing lenders a legal advantage

that can last for the life of the loan.

📊 75% unaware of arbitration — CFPB

📄 30–80 pages avg. contract length

⏱️ Under 2 mins avg. reading time

⚖️ Why This Gap Exists — By Design

The moment you sign a loan agreement, you are not just agreeing to a repayment schedule. You are agreeing to a legal document that may eliminate your right to sue, allow your interest rate to change without your consent, reach into your paycheck, and prevent you from leaving a negative review.

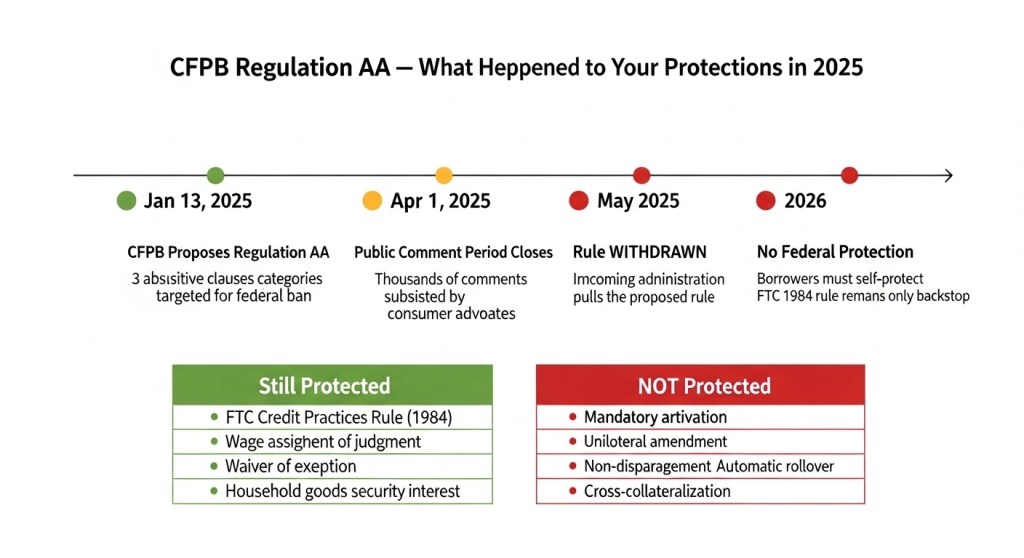

In January 2025, the CFPB proposed Regulation AA — a federal rule that would have banned three categories of the most abusive clauses in consumer financial contracts. The proposed rule would prohibit covered persons from including any terms that waive consumers’ substantive legal rights, allow unilateral amendment of material contract terms, or restrict consumers’ lawful free expression. The rule was withdrawn in May 2025. As of 2026, those protections do not exist.

That means the responsibility falls entirely on you — the borrower — to find and understand these clauses before you sign. This guide gives you exactly that: a plain-English breakdown of the 7 most dangerous clauses in use today, where to find them, and what to do about each one.

In 2025, 24.2 million Americans held personal loans with an average balance of $11,724 (LendingTree, Q3 2025). Of those borrowers, 47% were classified as financially vulnerable — meaning the fine print they didn’t read is binding people who can least afford the consequences of not reading it.

Here are the 7 clauses. Search for them. Know them. Do not sign until you do.—

Clause 1: What Is a Mandatory Arbitration Clause — And Why Does It Matter?

✅ 40-Word Direct Answer —

AI Featured Snippet Ready

A mandatory arbitration clause forces

all disputes between you and the lender

into

private arbitration —

eliminating your right to

sue in court or join a

class action lawsuit.

In 2025,

75% of borrowers were unaware

they had agreed to arbitration

in their financial contracts

(CFPB).

Arbitration is a private dispute resolution process. Instead of going to court — with a judge, a jury, public records, and the right to appeal — you appear before an arbitrator chosen from a list that the lender often controls. The proceedings are private. The outcomes are rarely published. The arbitrator’s decision is almost always final.

The CFPB attempted to ban mandatory arbitration clauses in consumer financial contracts in 2017. Congress overturned that rule the same year. The agency tried again with Regulation AA in January 2025 — and that rule was withdrawn in May 2025 before taking effect. As of 2026, mandatory arbitration remains fully legal and extremely common in consumer loan agreements.

What to look for: The words “arbitration,” “binding arbitration,” “dispute resolution,” or “class action waiver.” These often appear together — if you waive class action rights, you cannot join other harmed borrowers in a lawsuit even if thousands of you were damaged by the same practice.

What you can do: Ask the lender to remove the arbitration clause. Some will — especially credit unions. If they will not, at minimum understand what you are giving up. The FTC’s Credit Practices Rule does not ban arbitration clauses — this protection has no federal backstop as of 2026.

Danger level: 🔴 CRITICAL — affects your ability to seek legal remedy for any harm the lender causes.—

🛡️

The Credit Repair Playbook

Fix your credit. For free. Without paying a repair company.

6 interactive tools. 4 dispute letter templates with FCRA citations. AI-powered strategies for 2026. 90-day maintenance plan. Written in plain English — no legal degree required.

What Is a Unilateral Amendment Clause in a Loan Agreement?

✅ 40-Word Direct Answer —

AI Featured Snippet Ready

A unilateral amendment clause gives

the lender the right to

change, modify, or add to the terms

of your loan agreement —

including your

interest rate, fees, and repayment

terms — after you have

already signed. In many contracts,

a notice period of as little as

15 days

is all that is required.

⚠️

The CFPB noted its concern that unilateral amendment clauses allow covered persons to change fees, dispute resolution procedures, terms of service, or privacy policies — and that these clauses allow companies to circumvent consumers’ freedom to benefit from the contract.

In practice, this means a lender can send you a notice — often buried in an email or statement insert — announcing that your interest rate is increasing, a new fee is being added, or that you are now subject to arbitration when you weren’t before. Courts have generally refused to enforce the most extreme versions of these clauses, but many borrowers never challenge them.

What to look for: Language reading “we reserve the right to amend,” “we may modify these terms,” “changes will be effective upon notice,” or “continued use of the loan constitutes acceptance of new terms.”

What you can do: Read every notice you receive from your lender — even inserts in paper statements. If a material term changes and you object, contact the lender in writing immediately. In some cases, you have the right to reject changes and close the account at the original terms

Danger level: 🔴 CRITICAL — can change the cost of your loan after you are already committed to it.—

The CFPB tried. The rule lasted 4 months before being withdrawn. As of 2026 — you are on your own. ⚖️ DISCLAIMER : “Regulatory timeline based on publicly available Federal Register filings. Rule status as of early 2026. Not legal advice.”

What Is a Prepayment Penalty — And When Does It Apply?

✅ 40-Word Direct Answer —

AI Featured Snippet Ready

A prepayment penalty

charges you a fee for paying off

your loan early.

Lenders include this clause to

protect the

interest income they expected

to collect.

In 2025, prepayment penalties appear

in a significant portion of

auto loans and some personal

loans —

always check before signing.

💸 Fee for paying early

🚗 Common in auto loans

✅ Banned on QM mortgages

after 2014

💰 How Prepayment Penalties

Are Calculated

📊 Method 1 — % of Balance

Lender charges 1–5% of the

remaining loan balance as

a flat penalty fee

Example: $10,000 remaining

balance × 2% penalty =

$200 fee to pay early

📅 Method 2 — Months of Interest

Lender charges the equivalent

of 3–6 months of interest

payments as the penalty fee

Example: $200/month interest

× 3 months =

$600 fee to pay early

📋 Where Prepayment Penalties

Apply in 2026

Loan Type

Penalty Allowed?

Status

QM Mortgage (post-2014)

✅ No — Banned

Protected by Dodd-Frank Act

Non-QM Mortgage

❌ Yes — Allowed

Check your contract carefully

Auto Loan

❌ Yes — Common

Always search before signing

Personal Loan

⚠️ Sometimes

Varies by lender — always ask

Payday Loan

✅ Rarely

Short-term — no early

payoff benefit anyway

Student Loan (Federal)

✅ No — Banned

No penalty — pay early

anytime freely

Paying off debt early sounds like a purely positive financial decision. With a prepayment penalty clause, it can cost you hundreds of dollars — sometimes calculated as a percentage of the remaining balance or a set number of months of interest.

Prepayment penalties are banned on most federally backed mortgages originated after 2014 under the Dodd-Frank Act. But they remain legal on personal loans, auto loans, and non-qualifying mortgages. The key: they must be disclosed in the loan agreement, but many borrowers never notice them until they try to pay off early.

What to look for: The words “prepayment,” “early payoff fee,” “redemption fee,” or “yield maintenance.” Some contracts call it a “make-whole” provision.

What you can do: Ask the lender directly: “Is there a prepayment penalty on this loan?” Get the answer in writing. If there is one, calculate the cost of paying off early before making that decision. In competitive lending situations, ask for the clause to be removed.

Danger level: 🟡 HIGH — direct financial cost if you improve your financial situation and want to pay off debt faster.

What Is Cross-Collateralization in a Loan Agreement?

✅ 40-Word Direct Answer —

AI Featured Snippet Ready

Cross-collateralization

links multiple loans or accounts

so that collateral you pledged

for one loan

automatically secures all other

loans with the same lender.

This means defaulting on a

small personal loan

could put the collateral from a

car loan or home equity loan

at risk —

even if those loans are

completely current.

🚗 Your car at risk from

an unrelated debt

🏠 Home equity loan at risk too

⚠️ Most common in credit unions

🚫 No federal ban as of 2026

🔗 How Cross-Collateralization

Works — Real Example

<div

Cross-collateralization is most common in credit union loan agreements — ironically, the same lenders who are generally the most borrower-friendly. It is often buried in a clause that says something like “all obligations to this credit union are secured by all collateral pledged to this credit union.”

The practical consequence: you take out a credit union auto loan, then later take a small personal loan from the same credit union and default on the personal loan. The credit union may have the right to repossess your vehicle — collateral for the auto loan — even though your auto loan payments are perfectly current.

What to look for: Language reading “cross-collateralization,” “all obligations,” “securing all present and future debts,” or “all indebtedness.” Any clause linking multiple accounts to one collateral pool.

What you can do: Ask for a written list of exactly which accounts and collateral are covered by this clause. Request that the clause be limited to the specific loan you are taking out. Review this every time you take a new loan with the same institution.

Danger level: 🔴 CRITICAL — can put secured assets at risk from unrelated, unsecured debt defaults.—

What Is a Wage Assignment Clause — Is It Legal?

⛔ FEDERALLY BANNED CLAUSE —

AI Featured Snippet Ready

A wage assignment clause authorizes

your lender to collect debt payments

directly from your employer

— bypassing your bank

account entirely. The

FTC Credit Practices Rule

permanently bans wage assignment

clauses in consumer loan

agreements. If you find this clause

in a consumer loan contract, the

lender may be

violating federal law.

⛔ Banned — FTC Rule since 1984

💼 Reaches into your paycheck

🚨 Federal law violation if present

📋 Report to FTC immediately

⛔ THIS CLAUSE IS FEDERALLY

BANNED IN CONSUMER LOANS

</

Wage assignment was one of the most abusive debt collection tools in consumer lending history — allowing lenders to go directly to an employer and divert a borrower’s paycheck before it ever reached the borrower. The FTC concluded that wage assignment clauses were unlawful because they could occur without the due process safeguards of a hearing and an opportunity to present defenses — potentially leading to job loss or severely reduced income.

The FTC Credit Practices Rule, in effect since 1985 and proposed to be codified by the CFPB’s Regulation AA in 2025, permanently bans wage assignment clauses in consumer credit contracts. Finding one in a consumer loan is a red flag that the lender may not be operating within federal law.

What to look for: Language reading “wage assignment,” “payroll deduction authorization,” “assignment of earnings,” or “direct payment from employer.”

What you can do: Do not sign a consumer loan agreement containing this clause. Report it to the CFPB at consumerfinance.gov/complaint and the FTC at reportfraud.ftc.gov.

Danger level: 🔴 CRITICAL / Potentially Illegal — banned by the FTC Credit Practices Rule in consumer loans.

What Is a Non-Disparagement Clause in a Loan Agreement?

🔇 SILENCES YOUR VOICE —

AI Featured Snippet Ready

A non-disparagement clause in a

loan agreement

contractually prohibits you from

leaving negative reviews,

complaining publicly, or

criticizing the lender —

sometimes backed by

fines or account closure.

The CFPB’s January 2025 proposed

Regulation AA would have banned

these clauses.

As of 2026, they remain

legal and in use.

🔇 No negative reviews allowed

💸 Fines for speaking out

⚠️ CFPB Reg AA withdrawn

May 2025

✅ Consumer Review Fairness

Act 2016 may protect you

🔇 What a Non-Disparagement

Clause Can Prevent You From Doing

❌ Prohibited by the Clause:

Google / Yelp reviews

BBB complaints

Social media posts

Reddit warnings to others

News media interviews

Online forum discussions

Trustpilot / Sitejabber

Consumer complaint sites

💸 Possible Consequences:

Monetary fines

Account closure

Loan called due early

Legal action threatened

Credit score damage

Collections referral

Cease and desist letter

Damages claim filed

📋 How Lenders Hide This Clause

— Real Language Examples

⚠️ Version 1 — Direct Language:

“Borrower agrees not to make

any negative, disparaging, or

defamatory statements about

Lender, its products, services,

or employees in any public forum,

including online review platforms,

social media, or news outlets.”

⚠️ Version 2 — Hidden Language:

“Customer shall refrain from

any communication that could

reasonably be construed as

harmful to the

The CFPB’s January 2025 proposed rule included restrictions on free expression — clauses that restrain a consumer’s lawful free expression, such as limiting the right to provide a negative review or engage in certain political speech, including any contractual mechanism for enforcing those limits such as fees or reserving rights to close accounts.

Non-disparagement clauses in loan agreements serve one purpose: to prevent borrowers from warning other potential borrowers about their experience. They are not common in mainstream bank lending but appear in some online lender and fintech agreements, often buried in pages of digital terms that load at checkout.

What to look for: Language reading “you agree not to disparage,” “negative reviews,” “public statements,” “social media,” or “reputation.” Any clause linking your account status to your public speech about the company.

What you can do: Do not sign agreements containing this clause. The Consumer Review Fairness Act (2016) makes it illegal for businesses to include non-disparagement clauses in consumer contracts — if you find one, you can report it to the FTC.

Danger level: 🟡 HIGH — strips your ability to warn other consumers and may violate the Consumer Review Fairness Act.—

What Is an Automatic Rollover Clause in a Loan?

🔄 THE DEBT TRAP ENGINE —

AI Featured Snippet Ready

An automatic rollover clause

renews your loan automatically

at the end of its term —

charging another round of fees —

unless you

actively opt out.

In 2025,

80% of payday loans were rolled

over within 14 days(CFPB).

The rollover fee is how payday

lenders earn

most of their revenue.

📊 80% roll over — CFPB 2025

💸 $520 fees to borrow $375

📅 5 months in debt per year

🔄 Renews without your action

🧮 The Rollover Math —

How $375 Becomes $895

The automatic rollover is the engine of the debt trap. A borrower takes a two-week payday loan at $15 per $100. At the end of two weeks, they cannot pay in full — or do not realize the loan will auto-renew — and another $15 fee is charged. This continues until the borrower actively intervenes.

The CFPB’s 2024 research found the average payday borrower spends 5 months per year in debt for what began as a 2-week loan — largely because of automatic rollover. The average borrower pays $520 in fees to repeatedly borrow $375.

What to look for: Language reading “automatically renewed,” “rollover,” “extension,” “reborrowing,” or “if full payment is not received by [date], the loan will be extended.” Any clause that describes what happens if you do not pay in full — rather than describing what you must actively do to renew.

What you can do: Set a calendar reminder 5 days before your loan due date. Contact the lender before the due date if you cannot pay in full — most are required to offer a payment plan under state law. Never allow a loan to roll over silently.

Danger level: 🔴 CRITICAL — primary driver of the payday loan debt trap affecting 12 million Americans annually.—

The CFPB’s 2025 Attempted Fix — And Why It Didn’t Happen

🏛️ 2025 REGULATORY UPDATE —

AI Featured Snippet Ready

On

January 13, 2025,

the CFPB proposed

Regulation AA — a rule

to ban three categories of abusive

loan clauses:

waivers of legal rights,

unilateral amendment clauses,

and

free expression restrictions.

The proposed rule was

withdrawn in May 2025

by the incoming administration.

As of 2026,

none of these protections

are in effect.

📅 Proposed Jan 13 2025

❌ Withdrawn May 2025

The CFPB made a preliminary determination that the use of clauses waiving consumers’ legal rights, allowing companies to unilaterally change key terms, or restricting consumers’ lawful free expression may constitute an unfair or deceptive act or practice under the Consumer Financial Protection Act.

The rule covered all “covered persons” under the CFPA — banks, credit unions, fintech lenders, payday lenders, and any entity offering consumer financial products. Comments were due April 1, 2025. The incoming administration’s CFPB leadership withdrew the rule in May 2025 before it was finalized.

What remained: the FTC Credit Practices Rule — passed in 1984 — which permanently bans four specific clauses: confessions of judgment, waivers of exemption, wage assignments, and security interests in household goods. These four protections exist regardless of the Regulation AA outcome.

Everything else — mandatory arbitration, unilateral amendment, non-disparagement, prepayment penalties, cross-collateralization, and automatic rollover — remains the borrower’s responsibility to identify and negotiate.

Every one of the 7 clauses in this guide can be found in under 10 seconds using Ctrl+F. Use it before you sign — not after

Your Pre-Signing Checklist: How to Find All 7 Clauses in Any Contract

✅ Your 7-Clause Pre-Signing

Checklist

Use this checklist before signing

ANY loan agreement — personal loan,

auto loan, payday loan, BNPL,

or mortgage. Takes under 5 minutes.

Could save you thousands.

💡 How to Use:

Open your loan document.

Press

Ctrl+F (PC) or

Cmd+F (Mac) or

Tap & Hold → Find (Mobile).

Search each trigger word below.

If found — read the full clause

before signing.

🔴 Clause 1 — Mandatory Arbitration

CRITICAL — No federal ban

Eliminates your right to sue

in court or join a class action

lawsuit. 75% of borrowers are

unaware they agreed to this

— CFPB Research.

Ask lender to remove

before signing. Consider

a credit union instead.

✅ Safe Signal:

Word not found —

no arbitration clause

present in contract

🔴 Clause 2 — Unilateral Amendment

CRITICAL — Reg AA withdrawn

Lender can change your interest

rate, fees, or loan terms after

you have already signed —

with as little as 15 days notice.

🔍 Search for:

“amend”

“modify”

“reserve the right”

“change terms”

❌ If Found:

Read every lender notice

you receive — continuing

to use = acceptance

✅ Safe Signal:

Fixed rate contract with

no amendment language

present

🟡 Clause 3 — Prepayment Penalty

HIGH — Banned on QM mortgages only

Charges you a fee for paying

off your loan early — protects

the lender’s expected interest

income. Common in auto loans

and some personal loans.

🔍 Search for:

“prepayment”

“early payoff fee”

“make-whole”

⚠️ If Found:

Calculate if interest saved

by paying early exceeds

the penalty cost

✅ Safe Signal:

“No prepayment penalty”

stated explicitly in

the contract

🔴 Clause 4 — Cross-Collateralization

CRITICAL — Common in credit unions

Links multiple loans so that

defaulting on one small debt

can put all your secured assets

— car, home equity, savings —

at risk even if other loans

are current.

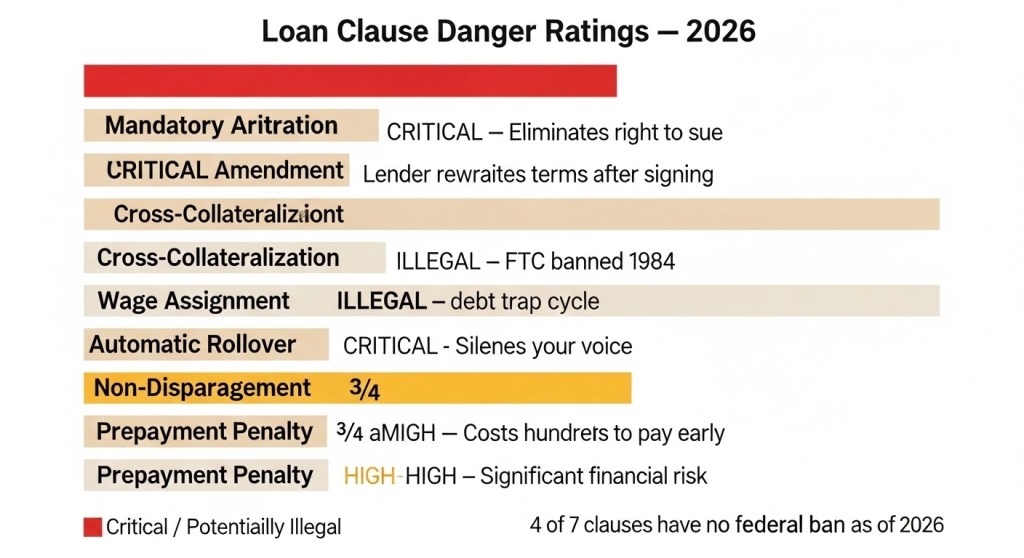

5 of the 7 clauses are rated Critical or Illegal. 4 have no federal ban as of 2026. The only protection is knowing what to search for before you sign.

Clause Danger Rating: What Each One Can Cost You

⚠️ Clause Danger Rating:

What Each One Can Cost You

Not all dangerous clauses cost you

the same way. Some eliminate your

legal rights. Some cost you money.

One is federally illegal. Here is

exactly what each clause takes —

and what it could cost you in

real dollars and real rights.

Rating Key:

🔴 Critical

No federal ban — active threat

🟡 High

Significant financial risk

⛔ Illegal

Federally banned — report to FTC

1

Mandatory Arbitration

🔴 CRITICAL

⚖️ Rights Cost

Right to sue

in court —

gone entirely

💰 Financial Cost

Arbitration fees

$200–$1,900+

out of pocket

📊 Who It Affects

75% of borrowers

already agreed —

CFPB 2025

What it takes from you:

Eliminates your right to sue

in court, join a class action,

have a public hearing, or appeal

a decision. All disputes go to

a private arbitrator — often

one the lender has used before.

Outcomes are final. No jury.

No public record. No appeal.

💸

Worst case: Lender overcharges

you $4,000. You cannot join a

class action of 10,000 other

affected borrowers. You must

fight alone in private

arbitration — paying $1,900

in fees — for a $4,000 dispute.

2

Unilateral Amendment

🔴 CRITICAL

⚖️ Rights Cost

Right to the rate

you agreed to —

gone

💰 Financial Cost

Hundreds to

thousands in

added interest

⏱️ Notice Period

As little as

15 days before

change takes effect

What it takes from you:

The rate, fees, and terms you

agreed to on signing day can

be changed at any time with

minimal notice. Lender sends

a statement insert or email.

Continuing to use the loan

constitutes legal acceptance —

even if you never read the notice.

💸

Worst case: You sign at 9.9%

APR. Lender sends a statement

insert raising it to 18.9%.

You miss the insert. You have

legally accepted the new rate.

On a $10,000 loan —

that is $900 extra per year

you did not budget for.

3

Prepayment Penalty

🟡 HIGH RISK

⚖️ Rights Cost

Right to pay

off early freely —

penalized

💰 Financial Cost

1–5% of remaining

balance OR 3–6

months interest

🛡️ Protection

Banned on QM

mortgages only —

post 2014

What it takes from you:

The freedom to become debt-free

on your own timeline. Even if

you come into money and want

to pay off the loan early —

the lender charges you a fee

to compensate for the interest

they expected to earn over

the full term.

💸

Worst case: You have a $15,000

auto loan. You want to pay it

off early. Prepayment penalty

is 3% of remaining balance.

You pay $450 just for the

privilege of being debt-free.

On a personal loan with

6-month interest penalty —

could be $600–$1,200.

💬 Reader Story

“I got a personal loan from an online lender — fast approval, decent rate. What I didn’t see until a year later when I tried to complain to the BBB: I had signed a non-disparagement clause buried on page 47. They sent me a legal notice threatening to close my account and pursue damages. I had unknowingly signed away my right to leave a single negative review. I wish I had searched that document before I signed it.”

— Marcus, 34, Atlanta.

Shared in the Confidence Buildings reader community.

“Expert Verdict: Marcus was a victim of a ‘Silence Clause.’ Under the Consumer Review Fairness Act, these are often legally unenforceable, but the threat alone is enough to chill consumer speech.”

Have you found a dangerous clause in a loan agreement? Share your experience in the comments — your story could protect someone else from signing the same thing.

🧠

Psychological Struggle: Why We Don’t Read What We Sign

Research on digital contract behavior shows that people spend an average of 76 seconds reviewing end-user license agreements before accepting them. Loan agreements are longer and more complex — but the behavior is similar. We are wired to trust the institution presenting the document and to treat the act of signing as a formality, not a legal negotiation.

“Lenders understand this. Contract length is not accidental. The placement of dangerous clauses on page 40 of an 80-page digital document is not accidental. The use of legal language that sounds neutral — ‘dispute resolution procedure’ instead of ‘you cannot sue us’ — is not accidental.”

Not reading your loan agreement is not a failure of intelligence or responsibility. It is a predictable human response to information overload and time pressure — responses that the contract is designed to exploit.

The 7-clause checklist in this post is a tool to break that pattern: not by reading everything, but by searching for exactly the right things.

Lenders design contracts to exploit the gap between how signing feels and what you are actually agreeing to. It is not your fault — but it is your responsibility to close the gap

❓ Frequently Asked Questions — Loan Agreement Fine Print

Can I negotiate loan agreement terms before signing?

Yes — more often than most borrowers realize. Mainstream banks rarely negotiate standard terms. But credit unions, community banks, and some online lenders will modify specific clauses if asked directly. The most negotiable clauses are prepayment penalties, arbitration agreements, and automatic rollover terms. Always ask in writing and get any agreed changes confirmed in a revised document.

What is the FTC Credit Practices Rule and what does it ban?

The FTC Credit Practices Rule (1984) permanently bans four specific clauses: (1) confessions of judgment; (2) waivers of exemption; (3) wage assignments; and (4) non-possessory security interests in household goods. Finding any of these is a federal law violation — report it to the FTC at reportfraud.ftc.gov.

What happened to the CFPB’s proposed Regulation AA rule in 2025?

The rule was withdrawn in May 2025 by the incoming administration before being finalized. As of 2026, those proposed protections are not in effect. The FTC Credit Practices Rule (1984) remains your primary federal protection.

Are arbitration clauses enforceable in all states?

Generally yes. The Federal Arbitration Act (FAA) makes these agreements broadly enforceable. While some states have specific nuances, do not assume state law protects you from federal arbitration enforcement.

What is the easiest way to find dangerous clauses?

Use Ctrl+F (PC) or Cmd+F (Mac) and search for: “arbitration,” “amend,” “prepayment,” “cross-collateral,” “wage assignment,” “disparage,” and “automatically renewed.”

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“The fine print is not just dense legal language — it is where lenders place the provisions that transform a standard loan into a financial trap. The FTC’s Credit Practices Rule, in effect since 1984, permanently bans four clauses because they were deemed ‘unfair’ and ‘deceptive’: confession of judgment (which waives your right to a hearing before a lender can seize assets), wage assignment (which allows direct wage garnishment without a court order), security interest in household goods (which puts your furniture, clothing, and appliances at risk), and waiver of exemption (which forces you to give up state bankruptcy protections). These clauses are illegal in consumer loans. Period. If you see any of them, you are dealing with a predatory lender operating outside federal law. More recent protections — like the CFPB’s 2025 Regulation AA, which would have banned mandatory arbitration clauses that block class actions — were withdrawn before taking effect. This means your ability to challenge unfair terms depends on whether your contract contains a valid arbitration clause and whether your state offers stronger protections. Before you sign any loan agreement, search for ‘arbitration,’ ‘waiver,’ and ‘assignment’ using Ctrl+F. If you find a clause that attempts to waive your right to sue or allows wage garnishment without a court judgment, do not sign until you speak with a consumer protection attorney.”

Legal Analysis: The four clauses banned by the FTC Credit Practices Rule (16 CFR Part 444) are void in consumer credit contracts. If a lender includes them, the clause is unenforceable. However, enforcement requires you to know the clause exists and to challenge it — often in court. Arbitration clauses are a separate concern: the Supreme Court’s 2011 decision in AT&T Mobility v. Concepcion allows lenders to require individual arbitration and prohibit class actions, even for small-dollar consumer claims. The CFPB’s 2025 Regulation AA would have banned these clauses in certain consumer loan products, but the rule was withdrawn in May 2025. As of 2026, no federal ban on mandatory arbitration in consumer lending exists. Some states have enacted their own restrictions — check your state attorney general’s website for your state’s rules on arbitration clauses in consumer loans.

Bottom Line: The difference between a fair loan and a predatory one is often hidden in four clauses you can find in under five minutes using Ctrl+F. Search for: “confession of judgment,” “wage assignment,” “household goods,” and “arbitration.” If any of these appear in a loan agreement for a consumer loan, proceed with extreme caution — or walk away.

📚 Related Reading —

The Borrower’s Truth Series

Day 15 is part of a 30-day series

on financial confidence for real

borrowers. Every post is free.

Every post is research-backed.

Start anywhere — but read them all.

🔀 Where Are You Right Now?

Jump to the most relevant post:

📊 CFPB Arbitration Study —

Consumer Awareness Research

Source for the statistic:

75% of borrowers are unaware

they agreed to mandatory

arbitration in their financial

contracts. CFPB consumer

financial protection research

and arbitration study data.

Source for rollover statistics:

80% of payday loans rolled over

within 14 days. Average borrower

takes 8 loans per year paying

$520 in fees to borrow $375.

Basis for Clause 7 — Automatic

Rollover analysis.

Official channel to report

illegal or abusive clauses

found in consumer financial

contracts. Referenced in all

7 clause action steps throughout

this post.

The primary federal law

permanently banning 4 abusive

clauses in consumer loan

contracts: wage assignment,

confession of judgment, waiver

of exemption, and household

goods security interest.

In effect since 1984 and

NOT affected by any 2025

regulatory changes.

Legal basis for FTC enforcement

action against lenders using

banned clauses — including wage

assignment. Referenced in Clause

5 analysis throughout this post.

Federal law making it illegal

for businesses to include

non-disparagement clauses in

consumer contracts. Referenced

in Clause 6 — Non-Disparagement

analysis. Partial protection

only — enforcement varies.

Official channel to report

lenders using federally banned

clauses — especially wage

assignment. Referenced in Clause

5 action steps. Takes under

10 minutes to file a report.

📊 J.D. Power 2025 U.S. Consumer

Lending Satisfaction Study

Source for two key statistics:

28% of borrowers cite unexpected

fees as their top complaint,

and 47% of personal loan

borrowers are financially

vulnerable. Used in Data Summary

and TL;DR blocks throughout

this post.

Source for personal loan market

data: 24.2 million Americans

hold personal loans with an

average balance of $11,724.

Used in Data Summary block

and series context throughout

this post.

📚 National Consumer Law Center —

Consumer Credit Regulation 2025

Reference source for consumer

credit law analysis including

cross-collateralization in

credit union agreements and

state-level rollover protection

laws. Used in Clause 4 and

Clause 7 analysis.

Bans prepayment penalties

on qualified mortgages

post-2014

✅ Active

Consumer Review

Fairness Act H.R. 5111

2016

Prohibits non-disparagement

clauses in consumer contracts

✅ Active

CFPB Regulation AA

Federal Register 2025-00633

2025

Would have banned 3 abusive

clause categories —

proposed and withdrawn

❌ Withdrawn

CFPB Ability-to-Repay

Rule 2014

2014

Requires lenders to verify

borrower ability to repay —

QM mortgage standard

✅ Active

🔬 Research Integrity Statement

✅ What This Post Uses:

Federal Register filings

CFPB primary research

FTC official rule text

Acts of Congress

Peer-reviewed industry data

.gov sources only

❌ What This Post Never Uses:

Sponsored content

Affil

The Bottom Line

A loan agreement is not a formality you get through before the money arrives. It is a legal contract that can strip your right to sue, allow your lender to rewrite the terms, reach into your paycheck, put unrelated assets at risk, and prevent you from warning anyone about what happened to you.

In January 2025, the CFPB tried to ban the most abusive of these clauses. The rule was withdrawn four months later. As of 2026, the responsibility is yours — and yours alone.

The 7-clause checklist in this post takes under 5 minutes to run on any digital loan document. That 5 minutes could be worth thousands of dollars and the protection of rights you did not know you were signing away.

🔬 Research & Publication Note: This post has been researched and published as part of the ConfidenceBuildings.com 2026 Finance Research Project by Laxmi Hegde, MBA in Finance — an independent study of emergency borrowing costs, consumer lending practices, and financial literacy gaps in the United States. Updated: March 2026.

“`

—

## 📍 HOW TO ADD IN WORDPRESS

“`

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Step 1 — Delete old grid block

Step 2 — Add new Custom HTML block

→ paste BLOCK A

Step 3 — Add another Custom HTML

block directly below it

→ paste BLOCK B

Step 4 — Preview — all 16 days

should show as one

seamless grid

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📚 Take This Further

The Borrower’s Truth — Full Guide & Toolkit

Everything on this blog — compiled, upgraded, and made actionable.