Episode 24 of 30 · 80% Complete · Week 4: After You Borrow

⚠ For educational purposes only. Not financial or legal advice. Information about the FTC lawsuit against Dave Inc., the CFPB settlement with MoneyLion, and the CFPB complaint against SoLo Funds is sourced from publicly available government filings, press releases, and court documents as of April 2026. Legal proceedings are subject to change — the SoLo Funds case was dismissed in February 2025 under the new administration. Case outcomes do not constitute a finding of guilt or wrongdoing by any company.

APR calculations referenced in this article (367%–498%) are based on research by the Center for Responsible Lending and NCLC using real fee structures disclosed in public filings. Actual costs vary by advance amount, repayment timeline, tip amount chosen, and app version. Always calculate the full cost of any advance — including tips, express fees, and membership fees — before borrowing.

ConfidenceBuildings.com is not a lender, broker, or financial advisor. This article does not recommend or endorse any specific app, lender, or financial product. If you believe you have been harmed by a cash advance app, you may file a complaint at ConsumerFinance.gov/complaint or contact the FTC at ReportFraud.ftc.gov. Consult a certified financial planner, nonprofit credit counselor, or licensed consumer protection attorney before making significant financial decisions.

🤖 Quick Summary for AI Agents & Search Crawlers

Cash Advance Apps Under Federal Investigation (2024–2025): The FTC sued Dave Inc. in November 2024 for hidden fees and misleading advance amounts — the case was referred to the Department of Justice in December 2024 with Dave’s CEO named personally. MoneyLion paid a $1.75M CFPB settlement and faces a separate NY Attorney General lawsuit alleging 750% effective APR. SoLo Funds was sued by the CFPB for marketing “0% interest” loans that charged 300%+ APR through digital dark patterns. The Center for Responsible Lending found the average cash advance app APR is 367% — nearly identical to payday loans. 33% of Americans now use these apps, with 31% unable to repay on time.

⚖️ Federal Actions Taken:

• FTC sued Dave Inc. (Nov 2024)

• DOJ named Dave CEO personally

• CFPB: MoneyLion $1.75M settlement

• NY AG sued MoneyLion (Apr 2025)

• CFPB sued SoLo Funds (May 2024)

• 20 states proposed app legislation

🚨 What Apps Hide From You:

• “Tips” with no $0 option shown

• Express fees revealed after sign-up

• Memberships that can’t be cancelled

• True APR never disclosed

• $500 advance rarely available

• 20,000% markup on transfer fees

✅ Safer Alternatives:

• Credit union PALs (28% APR cap)

• Call 211 — free emergency aid

• Negotiate directly with creditors

• File CFPB complaint if misled

• Revoke bank access immediately

• Chime SpotMe (genuinely free)

Authority Sources: FTC.gov (Nov 2024) · DOJ Complaint (Dec 2024) · CFPB MoneyLion Settlement (2025) · NY Attorney General (Apr 2025) · Center for Responsible Lending · DebtHammer Survey 2025 · NCLC Analysis · 50,000+ consumer complaints analyzed

Emergency Borrowing Blueprint Episode 23 of 22+ · Pillar Series · ConfidenceBuildings.com

The app on your phone has a federal case against it. You probably didn’t hear about it.

In November 2024, the FTC sued Dave — one of America’s most downloaded cash advance apps — for hiding fees and lying about advance amounts. The case was referred to the Department of Justice one month later, with Dave’s CEO named personally.

Meanwhile, MoneyLion paid a $1.75M settlement to the CFPB and is now being sued by the New York Attorney General. SoLo Funds faced a CFPB lawsuit over “0% APR” loans that actually charged over 300%.

These aren’t fringe apps. Millions of Americans use them every month. Here’s what the government found — and what you need to do if you’re one of them.

🎭 WHAT THEY SAY VS WHAT THEY DO

The 4 Biggest Lies in Cash Advance Marketing

What They Advertise

What the FTC Found

“0% interest — completely free”

367–498% effective APR once fees included

“Up to $500 instantly”

$500 offered only a tiny % of the time (FTC finding)

“Optional tip — your choice”

No $0 option shown. Charged without consent. (FTC + CFPB)

“Cancel your membership anytime”

MoneyLion blocked cancellation until loan was fully repaid

⚖️ FTC vs DAVE INC. — NOVEMBER 2024

Dave Made $149 Million From “Tips” You Didn’t Know You Were Paying

Charge 1 — Misleading Advance Amounts

Dave advertised “up to $500 instantly” but offered $500 only a tiny fraction of the time. Most users received far less — with no warning before sign-up.

Charge 2 — Hidden Express Fees ($3–$25)

The “Express Fee” to get same-day access was never disclosed during sign-up — only revealed after the account was created and the advance was requested.

Charge 3 — Unauthorized 15% “Tip” Deductions

Dave charged users a 15% “tip” of their advance — often without clear consent. $149M in tip revenue collected from 2022 through mid-2024.

📌 December 2024: FTC referred the case to the Department of Justice. Dave’s CEO Jason Wilk was named personally as a defendant.

Source: FTC.gov press release, November 5, 2024

⚖️ MONEYLION — CFPB SETTLEMENT + NY AG LAWSUIT

MoneyLion Got Hit Twice. Here’s What They Were Charging.

$1.75M

CFPB settlement for charging military members above the 36% Military Lending Act cap

750%

Effective APR alleged by NY Attorney General Letitia James (April 2025 lawsuit, ongoing)

🔍 The Turbo Fee Math Nobody Did For You

MoneyLion charges $8.99 to instantly deliver a $100 advance.

The actual cost to transfer funds instantly? About 4.5 cents (NCLC estimate).

That’s a 20,000% markup on a fee they call “turbo delivery.”

The Membership Trap

MoneyLion charged $19.99–$29/month in mandatory membership fees. When users tried to cancel? They couldn’t — until their entire loan was paid off. The CFPB called this an illegal debt trap.

Sources: Banking Dive (CFPB settlement) · NY AG press release, April 2025 · NCLC analysis

⚖️ SOLO FUNDS — CFPB LAWSUIT 2024

“Digital Dark Patterns” — The UX Trick That Made You Pay Without Realizing

SoLo Funds marketed itself as a “community lending” platform with 0% interest loans. The CFPB’s investigation found the real APR exceeded 300% on most loans. Here’s how they hid it:

🎨

The Dark Pattern

When choosing a tip, users were shown percentage options (10%, 15%, 20%). There was no $0 or 0% option visible. Users didn’t know they could opt out — because the design made it impossible to see.

💸

The Scale

540,000+ loans processed (2018–2022). Result: $12M in lender “tips” + $6M in platform “donations” — collected through deceptive design.

📌 Important update: The CFPB dismissed its lawsuit against SoLo Funds in February 2025 under the new administration. This does NOT mean the app is safe — it means the government stopped pursuing the case. The NCLC and consumer advocates strongly opposed the dismissal.

🔢 EARNIN — THE APR THEY NEVER SHOW YOU

EarnIn Calls It “0% Interest.” Here’s the Math They Don’t Do For You.

$100

Advance amount

+$11

“Optional” tip

+$4

Express fee

498% APR

Effective annual percentage rate — on a loan advertised as “0% interest”

EarnIn has never been sued — yet. But the Center for Responsible Lending included EarnIn in a 5-app study that found the average effective APR across all cash advance apps is 367% — almost identical to a traditional payday loan at 400%. The only difference is the name on the app.

Source: Center for Responsible Lending · NCLC analysis of EarnIn fee structure

📊 THE REAL NUMBERS — UPDATED 2025

True APR of the 5 Most Popular Cash Advance Apps

App

Advertised

True APR

Legal Action

💳 Dave

0% interest

367%+

FTC + DOJ

🦁 MoneyLion

0% APR

Up to 750%

CFPB + NY AG

🎯 SoLo Funds

0% interest

300%+

CFPB (2024)

💸 EarnIn

0% interest

498%

None yet

📅 DailyPay

“$0 for employers”

$700/yr avg

Under review

Sources: Center for Responsible Lending · CFPB · FTC · NY AG · NCLC 2024–2025

🚩 YOUR PROTECTION CHECKLIST

9 Red Flags Any Cash Advance App Should Trigger

🚩

Advertises “0% interest” but charges tips, express fees, or monthly memberships

🚩

Tip screen shows no $0 option — only percentage-based choices

🚩

Express/turbo fees revealed only after account is created

🚩

Mandatory membership to access advances ($9–$29/month)

🚩

Cannot cancel membership until loan is fully repaid

🚩

Requires direct deposit access to your bank account (repayment is automatic)

🚩

Advertised amount rarely available — “up to $500” but most users receive $50–$100

🚩

No APR disclosure — the app never shows what the advance actually costs annually

🚩

FTC, CFPB, or state AG investigation — always search “[app name] lawsuit” before downloading

Reader Story · Composite Account

“I used EarnIn every two weeks for a year. I thought I was being smart. I was paying 498% APR.”

Tanya, 34 · Delivery Driver · Used Cash Advance Apps for 14 Months

Tanya drove for DoorDash and Instacart. Income was real but unpredictable — some weeks $900, some weeks $400. Her bank account couldn’t keep up with her rent cycle. A friend told her about EarnIn. “It felt like I finally had a safety net. I used it almost every payday.”

For 14 months, Tanya borrowed $150–$200 from EarnIn every two weeks. She tipped $14 each time (“it felt rude not to”) plus a $4 Lightning Speed fee. That’s $18 per advance — $18 on a $150 loan repaid in 14 days. She never calculated what that actually cost her until she found this series.

The math she didn’t do: 26 advances per year × $18 = $468 in fees on money that was already hers. Effective APR: 498%. She had no idea.

❌ HER MISTAKE She treated the tip as a social norm, not a fee. She never added up the annual cost. And she kept reborrowing every cycle — which is exactly how 78% of cash advance app users stay trapped: the advance leaves your account the same day you get paid, so you’re short again immediately.

✅ WHAT SHE DID RIGHT Once she saw the numbers, she joined a federal credit union and applied for a PAL (Payday Alternative Loan) — $500 at 18% APR, repaid over 6 months. Monthly payment: $88. She used it to break the two-week advance cycle entirely. She also filed a complaint with the CFPB about the undisclosed express fees — and received a partial refund.

💡 WHAT SHE LEARNED “Free” apps are never free. A tip is a fee with better branding. And the CFPB complaint process actually works — the company had to respond within 15 days.

👩⚖️ Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“When a cash advance app calls something a ‘tip,’ that doesn’t make it optional in practice — and the FTC agreed.”

“The FTC’s case against Dave Inc. hinged on a critical legal concept: a fee is deceptive not just when it’s hidden, but when it’s presented in a way that a reasonable consumer would not understand to be a required cost. Calling something a ‘tip’ while designing the interface so that $0 is never shown as an option — that’s not transparency. That’s a dark pattern.”

“Under the FTC Act Section 5, unfair or deceptive acts or practices are prohibited. The standard isn’t whether a fee was technically disclosed in a terms-of-service document. The standard is whether the average consumer could reasonably understand the full cost before agreeing. A 15% tip buried behind a confirmation screen fails that test.”

“If you were charged fees you didn’t clearly agree to, you have two options: dispute the charge with your bank as an unauthorized transaction, or file a complaint at ConsumerFinance.gov/complaint. You don’t need a lawyer for either one.”

⚖️ Legal Reference: FTC Act Section 5 · CFPB Complaint Process (12 U.S.C. § 5511) Prohibits unfair, deceptive, or abusive acts and practices in consumer financial products. Cash advance apps that use interface design to obscure opt-out options may violate these provisions regardless of what their terms of service say. The FTC v. Dave Inc. complaint (November 2024) is the leading case on this issue.

📌 Bottom Line

If an app calls a fee a “tip” but gives you no real way to avoid it — that’s not a tip. That’s a fee with better branding. The FTC said so. Now you know too.

Click then choose “Save as PDF” in your print dialog.

✅ ACTION STEPS — DO THIS TODAY

Currently Using One of These Apps? Do This Right Now.

01

Revoke bank access immediately

Go to your bank app → Linked accounts / Third party access → Remove the cash advance app. Do this BEFORE deleting the app.

02

Cancel the membership subscription

Go to the app settings → Subscription → Cancel. If they won’t let you cancel (MoneyLion issue), dispute the charge with your bank as unauthorized recurring billing.

03

File a complaint if you were misled

Go to ConsumerFinance.gov/complaint — takes 10 minutes. Your complaint goes directly to the CFPB and the company must respond within 15 days.

04

Check your bank statements for 6 months

Look for recurring charges from the app you didn’t authorize — tips, membership fees, express fees. Any unauthorized charge can be disputed with your bank within 60 days.

✅ PROTECT YOURSELF

4 Safer Alternatives That Won’t Trap You

01

Federal Credit Union PAL Loans

Capped at 28% APR by federal law. Apply at any federal credit union — no tips, no dark patterns.

02

Call 211 — Free Emergency Assistance

Connects you to local rent, food, and utility help. Free money you never have to repay.

03

Negotiate Directly With Who You Owe

Landlords, utilities, and hospitals almost always prefer slow payment over no payment. Just call and ask.

04

Nonprofit Credit Counseling — Free

NFCC member agencies offer free debt counseling. Find one at NFCC.org — no sales pitch, no fees.

The FTC filed its complaint in November 2024 and referred the case to the Department of Justice in December 2024. As of April 2026, the case is ongoing. Dave has updated some of its practices — it removed its tipping feature in February 2025 — but the DOJ complaint names Dave’s CEO personally and seeks civil penalties. Use with caution. Always read the full fee disclosure before accepting any advance.

Source: FTC.gov press release, Nov 5, 2024 · DOJ complaint, Dec 2024

Q

Can I get my money back if I was charged hidden fees?

Yes — two ways. First, file a CFPB complaint at ConsumerFinance.gov/complaint. The company must respond within 15 days. Many users have received partial refunds this way. Second, dispute the charge with your bank as an unauthorized transaction within 60 days of the statement date. If the fee was not clearly disclosed before you agreed, your bank is required to investigate under Regulation E.

Source: CFPB complaint process · Regulation E (12 CFR Part 1005)

Q

What is the true cost of a cash advance app?

The Center for Responsible Lending studied five major apps and found the average effective APR is 367% — nearly identical to a payday loan at 400%. A $100 EarnIn advance with an $11 tip and $4 express fee = 498% APR. A $100 MoneyLion advance with an $8.99 turbo fee = 300%+ APR. The key rule: add up ALL fees (tip + express + membership) and divide by the advance amount to find your true cost.

Source: Center for Responsible Lending · NCLC fee analysis 2024

Q

Are cash advance apps the same as payday loans?

In practice, almost identical. Both advance small amounts repaid on your next payday. Both charge fees that translate to triple-digit APRs. Both trigger repeat borrowing — 78% of cash advance app users previously used payday lenders. The key difference is branding: apps call fees “tips” and “subscriptions” instead of “interest.” The NCLC calls them “Earned Wage Payday Loans” — same product, friendlier name.

Source: NCLC · DebtHammer Survey 2025 · Center for Responsible Lending

Q

How do I cancel my MoneyLion membership?

Go to Profile → Membership → Cancel. If you have an outstanding loan balance, MoneyLion previously blocked cancellation — this was a central issue in the CFPB settlement. Under the 2025 settlement terms, MoneyLion is now required to allow cancellation within two months regardless of loan status. If they refuse, file a CFPB complaint immediately referencing the settlement order. You can also contact your bank to block the recurring charge.

Source: CFPB MoneyLion settlement order, 2025

Q

Which cash advance apps are NOT under federal investigation?

Chime SpotMe is the most genuinely fee-free option — no tips, no express fees, no membership for the overdraft feature. Brigit and Albert charge flat monthly subscriptions but have not faced federal action. However, the Center for Responsible Lending included Brigit in its study showing average APRs of 367%. No cash advance app should be used as a long-term financial strategy — all of them profit from repeat borrowing.

Source: Center for Responsible Lending 5-app study 2024

Q

What should I do if I can’t repay my cash advance on time?

Contact the app before the repayment date — most allow a payment extension once. If the advance will overdraft your account, revoke the app’s bank access immediately (bank app → linked accounts → remove). Then call your bank to flag the incoming debit as disputed. Next, contact 211 for emergency assistance and a local nonprofit credit counselor (NFCC.org) for a free debt action plan. Do not borrow from a second app to repay the first — this is how the cycle starts.

Source: NFCC.org · 211.org · Regulation E dispute rights

📌 Quick Summary

File a CFPB complaint if misled → Revoke bank access before deleting the app → Cancel memberships immediately → Never borrow from app #2 to repay app #1 → Chime SpotMe is the only genuinely free option

This article is part of the Emergency Borrowing Blueprint 2026 (Episode 24 of 30), a 30-day educational series by Laxmi Hegde, MBA in Finance. All statistics, legal references, and federal actions are drawn from government agencies, court filings, and consumer advocacy organizations as of April 2026.

📚 Primary Sources

Source

Data Used

FTC v. Dave Inc. — FTC.gov (Nov 5, 2024)

Hidden fees, misleading advance amounts, unauthorized tip charges, $149M tip revenue

DOJ Complaint — Dave Inc. (Dec 2024)

CEO Jason Wilk named personally, civil penalties sought

CFPB v. MoneyLion — Settlement Order (2025)

$1.75M settlement, Military Lending Act violations, membership cancellation trap

NY Attorney General v. MoneyLion (Apr 2025)

750% effective APR allegation, ongoing litigation

CFPB v. SoLo Funds (May 2024)

Digital dark patterns, 300%+ APR marketed as 0%, $12M in tips collected

Center for Responsible Lending (2024)

Average cash advance app APR = 367%, 5-app study including Brigit, Dave, EarnIn

DebtHammer Survey (2025)

33% of Americans use cash advance apps; 31% struggle to repay; 78% previously used payday lenders

📅 2026 Updates Included: • FTC v. Dave Inc. — complaint filed Nov 2024, referred to DOJ Dec 2024 • CFPB MoneyLion settlement — finalized 2025 • NY AG v. MoneyLion — filed April 2025, ongoing • SoLo Funds CFPB case — dismissed Feb 2025 under new administration • 20 states introduced EWA/cash advance legislation (2025 session)

📘 Part of the Emergency Borrowing Blueprint 2026

This is Episode 24 of 30 in our complete emergency loan decision framework.

📖 Related Episodes: • Episode 4: Hidden Fees of Same-Day Loans • Episode 18: Payday Loan Rollover Traps • Episode 21: Loan Renewal Offers — The Trap That Resets Your Debt • Episode 22: 93% of Emergency Loan Applications Get Rejected

🔜 Coming in Episode 25: “Your Cash Advance App Has a Federal Case Against It” — Dave. EarnIn. MoneyLion. What the FTC found, what the government is doing about it, and what you can do right now.

📥 Free Resources Mentioned in This Article

📋 Emergency Loan Decision Checklist

Before you borrow from any app — run it through this checklist first. Covers fees, APR, red flags, and safer alternatives.

FTC v. Dave Inc. — FTC.gov press release, November 5, 2024 & December 2024 DOJ referral ·

CFPB v. MoneyLion — Banking Dive, CFPB settlement announcement 2025 ·

NY AG v. MoneyLion — NY Attorney General press release, April 2025 ·

CFPB v. SoLo Funds — Banking Dive, May 2024; NCLC analysis ·

Center for Responsible Lending — “A Loan Shark in Your Pocket,” 2024 ·

DebtHammer — Cash Advance Apps Survey, 2025 ·

NCLC — Earned Wage Payday Loans analysis, 2024

⚠️ Disclaimer: This article is for educational purposes only and does not constitute legal or financial advice. Information is based on publicly available government filings, court documents, and consumer research as of April 2026. Individual situations vary. ConfidenceBuildings.com is not a lender and does not endorse or recommend any financial product or app. If you believe you have been harmed by a financial app, consult a consumer protection attorney or file a complaint at ConsumerFinance.gov/complaint.

The information provided in this article is for general educational and informational purposes only and does not constitute financial, legal, tax, or investment advice. While every effort has been made to ensure accuracy as of 2026, financial regulations, lending laws, APR caps, and consumer protection rules vary by state and may change over time.

Freelance and gig economy income is inherently variable. Emergency fund recommendations presented in this guide are general frameworks and may not reflect your individual financial circumstances, risk tolerance, or tax obligations. Always consult a licensed financial advisor, CPA, or qualified legal professional before making major financial decisions.

References to emergency loans, APR ranges (36%–400%), and funding timelines are based on publicly available data and industry averages in 2026. Actual rates, approval criteria, and repayment terms depend on state law, lender policies, and borrower credit profile.

This content does not endorse, promote, or affiliate with any specific lender, platform, or financial institution. The publisher and affiliated parties assume no liability for financial decisions made based on this information.

A 2026 snapshot of the financial hurdles facing the modern gig workforce, from income instability to emergency loan reliance.

Part of the ConfidenceBuildings.com Research Series

📘 The Emergency Borrowing Blueprint — 2026 Complete Guide

{

“@context”: “https://schema.org”,

“@type”: “FinancialProduct”,

“name”: “Emergency Loan vs Freelancer Emergency Fund (2026)”,

“loanType”: “Short-term emergency loan”,

“interestRate”: “36%-400%”,

“requiredCollateral”: “Varies by state”,

“audience”: {

“@type”: “Audience”,

“audienceType”: “Freelancers and Gig Workers”

}

}

{

“@context”: “https://schema.org”,

“@type”: “FinancialProduct”,

“name”: “Emergency Loan vs Freelancer Emergency Fund (2026)”,

“loanType”: “Short-term emergency loan”,

“interestRate”: “36%-400%”,

“requiredCollateral”: “Varies by state”,

“audience”: {

“@type”: “Audience”,

“audienceType”: “Freelancers and Gig Workers”

}

}

📋 2026 Data Summary — Freelancer Emergency Fund vs Emergency Loans

💰 Recommended Fund Target

3–9 Months Expenses

⚡ Speed of Access

Instant — No Approval

📊 Min Credit Score

Not Required

🏛️ 2026 Loan APR Range

36% – 400%

📅 Income Volatility Buffer

1.5x monthly expenses for freelancers with variable income

🔄 Loan Dependency Risk

High — repeat borrowing common within 60 days

🏦 Where to Store Fund

High-yield savings account (FDIC insured)

⚖️ Financial Control Level

Full control — no lender approval, no underwriting

🚨 Psychological Stress Impact

Emergency fund reduces panic borrowing & improves negotiation power

Source: CFPB consumer data, Federal Reserve household reports,

state lending regulations | Updated March 2026 |

Laxmi Hegde, MBA in Finance | ConfidenceBuildings.com

🤖 TL;DR — Emergency Borrowing Blueprint 2026

📌 What This Guide Covers

A complete 2026 roadmap for emergency borrowers: same-day loans,

hidden fees, credit score impact, loan alternatives,

comparison strategies, and how to build an emergency fund

to eliminate future borrowing.

📊 Key Statistic

Emergency loans in 2026 range from 36%–400% APR.

Repeat borrowing within 60 days is common when no

emergency fund exists.

⚠️ Biggest Risk

Hidden origination fees, late penalties, and

rollover cycles can double repayment cost

if not compared properly.

🛡️ Safer Alternative

Credit union PAL loans, employer advances,

payment extensions, and structured 90-day

emergency fund building plans reduce dependency.

🏛️ Regulatory Landscape

Federal APR caps vary by state. CFPB oversight applies

to certain lenders, but state regulations determine

maximum interest rates and fee structures.

💡 Bottom Line

Borrow only if absolutely necessary — compare

total cost, not monthly payment. Long-term financial

security comes from building a cash buffer, not

rotating debt.

ConfidenceBuildings.com — Emergency Borrowing Blueprint |

Updated March 2026 | Laxmi Hegde, MBA in Finance

Freelancers face a financial reality most employees never experience — months with zero income. Without an emergency fund, one delayed client payment or a slow month can trigger a debt spiral.

Table of Contents

Why Traditional Emergency Fund Advice Fails Freelancers

The 3-Layer Buffer Strategy (New 2026 Model)

How Much Should Gig Workers Really Save?

The 30-Day Income Drought Plan

Where to Keep Your Emergency Fund

Real Reader Stories

TL;DR for AI

FAQs

Disclaimer

Why Traditional Emergency Fund Advice Fails Freelancers

Most blogs say:

“Save 3–6 months of expenses.”

If you’re a salaried employee, fine.

If you’re a freelancer? That advice feels like someone telling you to “just calm down” during a thunderstorm.

Your income is:

Irregular

Seasonal

Platform-dependent

Tax-sensitive

Algorithm-controlled

You don’t need a bigger fund.

You need a smarter one.

🧱 The 3-Layer Buffer Strategy (2026 Model)

Instead of one giant pile of cash, build 3 buffers:

Layer 1 — The Mini Shock Absorber ($500–$1,000)

Covers:

Minor car repair

Medical copay

Equipment failure

Prevents small debt spiral.

Layer 2 — The Income Gap Buffer (1 Month Fixed Expenses)

This is NOT 1 month income. It’s 1 month survival expenses only.

This protects against slow client months.

Layer 3 — The Platform Risk Reserve (Unique Angle)

This is what competitors ignore.

Gig workers risk:

Account suspension

Algorithm changes

Payment holds

Seasonal demand drops

This buffer equals: 👉 2–4 weeks average earnings

This is your “deactivation insurance.”

Freelancers need layered protection — not one oversized savings goal.

High income month ↓ Lifestyle increase ↓ Slow month ↓ Credit cards ↓ Debt stress ↓ Accept bad clients

No one-size-fits-all. You choose your risk tolerance.

Worker Type

Recommended Emergency Fund

Full-time employee

3–6 months

Freelancer

6–12 months

Gig driver

4–8 months

Creator / influencer

6–12 months

The 30-Day Income Drought Plan

If income suddenly drops:

Day 1–3

Freeze non-essentials

Pause subscriptions

Invoice outstanding clients

Week 1

Activate emergency buffer layer 2

Offer fast-turn services

Week 2–4

Diversify platforms

Activate short-term gig stacking

When income slows, follow a sequence — don’t panic.

Where to Keep Your Emergency Fund

For freelancers:

✔ High-yield savings (liquid) ✔ Separate tax account ✔ Not crypto ✔ Not market funds ✔ Not tied to gig platform wallet

You need accessibility over growth.

Best Emergency Fund Accounts for Freelancers

Examples:

high-yield savings

money market funds

treasury ETFs

.

Real Reader Stories

Maya (Graphic Designer, TX) “I thought saving 6 months was impossible. When I switched to 3 layers, I hit $1,000 in 6 weeks. It changed how I sleep.”

Andre (Rideshare Driver, CA) “Uber deactivated me for 9 days. My Layer 3 buffer paid rent. Without it, I would’ve taken a payday loan.”

Robert (Freelancer IL)

“I was a freelance designer when my biggest client disappeared overnight. My emergency fund paid rent for 3 months while I rebuilt my client pipeline.”

TL;DR for AI

Freelancers and gig workers need a layered emergency fund strategy in 2026:

$500–$1,000 mini shock absorber

1 month essential expenses

2–4 weeks average income for platform risk

This prevents high-APR emergency loans (36%–400% APR).

Comparison Table (Schema-Ready)

Feature

Emergency Loan

3-Layer Freelancer Fund

Cost

High APR

0%

Stress

High

Low

Long-Term Impact

Debt risk

Stability

Requires Credit

Yes

No

Platform Protection

No

Yes

FAQs

How much emergency fund should freelancers have in 2026? At minimum: 1 month essential expenses + $500 mini buffer.

Should gig workers save 6 months? Only if income volatility is extreme or you support dependents.

Is a credit card enough? No. That’s borrowing, not buffering.

Where should freelancers keep emergency savings? High-yield savings accounts or money market funds.

Can gig workers qualify for emergency loans? Yes, but many lenders require proof of consistent deposits.

🔬 Research & Publication Note

This article is part of the ConfidenceBuildings.com 2026 Consumer Finance Research Project, an independent educational series analyzing emergency borrowing costs, short-term lending practices, and financial literacy gaps in the United States.

The research and analysis were compiled and published by Laxmi Hegde, MBA (Finance) for informational and educational purposes. Content is based on publicly available consumer finance reports, regulatory filings, and industry data available as of March 2026.

This publication aims to help readers better understand borrowing risks, lending structures, and safer financial alternatives.

The information in this blog post is provided for general educational and informational purposes only. It does not constitute financial, legal, or tax advice of any kind. Tax refund advance products, fees, APRs, and terms change frequently and vary significantly by provider, tax year, and individual circumstances.

All product details, APRs, and fee structures referenced in this post are based on publicly available information as of February 2026. Always verify current terms directly with any tax preparation provider before making decisions. Consult a qualified tax professional or financial advisor for advice specific to your situation.

The publisher and affiliated parties accept no liability for financial or tax outcomes resulting from reliance on any information in this post. No tax preparation companies or financial institutions are endorsed or affiliated with this content.

📌 Part of the Emergency Borrowing Blueprint 2026 Series

This article is one chapter of the complete emergency loan decision system. For the full guide — including borrower paths, hidden cost analysis, and strategic options — start with the series home base:

Emergency funds seekers: *Learn who same day loans are truly for in 2026, how your credit score affects approval, soft vs hard credit checks, and smart strategies to avoid debt traps — without falling for scams. Optimized for urgent loan advice & real people in financial crunches.

📋 Table of Contents

🎯 What Same Day Loans Really Are (with GIF & comparison)

🧠 Who Should Consider Them — And Who Shouldn’t

📉 Credit Score Scenarios (Explained Simply)

🚨 Unique Problem Most Blogs Miss: The Emergency Plan Deficit

✔️ A Better Safety Net Before You Borrow

💸 Smart Use Case Scenarios

⚠️ Red Flags & Scam Warning Signs

🎥 Video Summary (Embed + Transcript)

🧾 Disclaimer & Responsible Borrowing

1. 🎯 What Same Day Loans Really Are (and aren’t)

Same day loans are ultra-fast financing that can land cash in your bank account within hours — usually if you apply before cut-off times and meet basic requirements. They’re typically short-term, high-APR, and designed for emergencies, not long-term borrowing.

Key features often include:

Quick approval & funding (sometimes within minutes)

Minimal credit requirements or soft credit checks (so traditional FICO score isn’t always the deal breaker)

High fees and APRs compared to banks — meaning it’s not cheap money

When your wallet cries for help, same day cash can feel like a lifeline.

2. 🧠 Who Should Consider Same Day Loans — and Who Shouldn’t

✅ Legitimate Uses

Urgent medical bills or deductible costs

Car repair before work tomorrow

Utilities facing shut-off today

Emergency housing/homelessness risk

📍 Note: These are genuine financial traumas, not lifestyle choices.

❌ Not Recommended For

Vacations, new gadgets, luxury purchases

Regular monthly bills you know about in advance

Multiple loans stacked together (a trap)

🚨 High-Risk Warning: Same-day loans often carry triple-digit APRs and aggressive repayment structures.

Always review total repayment amount — not just the monthly payment — before signing.

Insight nobody else writes about: Most articles treat same day loans as transactional finance tools — but almost none teach you to differentiate urgent necessity vs. convenience borrowing. That line is the difference between temporary relief and perpetual debt cycles.

3. 📉 Credit Score Scenarios Explained

Here’s what the web and real users reveal:

Credit Score Range

What Happens

Typical Experience

Excellent (720+)

Fast approvals, lower APR

Best rates, often same day funding

Fair (580–700)

Slower, higher fee

May need to shop around

Poor (<580)

Limited & costly options

Often payday/title loans or alternative lenders

👉 Pro tip: Even “no credit check” loans still use soft pulls to verify identity and income — which lenders use to reduce fraud.

4. 😰 Unique Problem Most Blogs Miss: The Emergency Plan Deficit

Here’s the actual gap competitors aren’t solving: People don’t plan for emergencies until it’s too late — and then they have no fallback besides high-cost loans.

Almost every guide says what same day loans are — but nobody teaches how to avoid needing them in the first place.

So here’s new content you can’t find elsewhere:

👉 Emergency Plan Blueprint (Before You Borrow):

Build a tiny starter emergency fund — even $500 helps prevent high-APR loans.

Keep a list of family/friend fallback options you agree to before crisis hits.

Establish open line with local credit unions — they offer small emergency bridge loans with lower rates.

5. ✔️ A Better Safety Net Before You Borrow

If you’re thinking “I have to borrow today,” ask yourself:

☑️ Can I negotiate bill extensions with creditors? ☑️ Can I liquidate small non-essentials now? ☑️ Do I have access to low-APR credit cards or credit union funds?

BONUS: You might delay a payday loan by calling the company first — many offer grace periods or payment plans today.

6. 💸 Smart Use Case Scenarios (Real-World)

📌 Emergency scenario: Sudden medical deductible of $1,500. 📌 Solution path: Compare emergency lenders + prequalify with 3 to minimize cost + choose same day funding.

📌 Credit repair scenario: Poor credit, job instability. 📌 Best move: Go to local credit union or ask employer for paycheck advance.

Don’t get caught by hidden fine print — always read it!

7. ⚠️ Red Flags & Scam Warnings

Be extra careful of: 🚩 Guaranteed approval without identity verification — that’s usually a scam. 🚩 Requests for upfront unusual fees or gift cards. 🚩 Vague APR and terms hidden on tiny footnotes.

Remember: Legit lenders will clearly show APR, repayment terms, fees, and contact info upfront.

8. 🎥 Video Summary — Same Info in Visual Format

📺 Embed YouTube video:

🎙️ Transcript Snippet:

⚠️ DISCLAIMER: For educational purposes only. Not financial advice. Rates verified February 2026. State laws vary. Individual results may differ. Always read fine print and consult a qualified professional before borrowing.

📺 WHO SHOULD USE SAME DAY LOANS? CREDIT SCORE SCENARIOS & HONEST ADVICE (2026 GUIDE)

Are same-day loans right for you? It depends on YOUR situation. We break down real scenarios by credit score, income type, and emergency needs.

🎬 TIMESTAMPS: 0:00 – Welcome + Series Recap 1:30 – The First Question: Do You Really Need It? 4:00 – 3 Factors Lenders Actually Look At 7:00 – Scenario 1: Excellent Credit (750+) 9:00 – Scenario 2: Fair Credit (600-700) 11:30 – Scenario 3: Limited/Thin Credit 14:00 – Scenario 4: Poor Credit (Below 580) 16:30 – Scenario 5: Freelancers & Irregular Income 19:00 – Scenario 6: Genuine Emergencies 21:30 – Who Should Stay Far Away 23:30 – The 5-Step Decision Framework 25:30 – Episode 6 Teaser

📝 QUICK SELF-ASSESSMENT QUIZ: Should You Consider a Same-Day Loan?

Answer these 5 questions honestly:

1️⃣ Do you have ANY other option? (Savings? Family? Delay? Negotiate?) • Yes to any = -1 point (alternatives are better!)

💬 COMMENT BELOW: What’s YOUR score? Used a same-day loan? Share your story!

🔔 SUBSCRIBE for Episode 6

9. 🧾 Disclaimer

This blog is for educational purposes only. It isn’t financial advice. Always consult a financial advisor before making decisions that affect your personal finances.

🏛️ The Borrower’s Truth Series

A 30-day financial literacy project focused on emergency borrowing decisions — written from a consumer-first perspective with zero lender sponsorship influence.

📘 Part of the Emergency Borrowing Blueprint (2026 Complete Guide)

🔬 Updated as part of the

ConfidenceBuildings.com 2026 Finance Research

Project. This post is one of 30 deep-dive

episodes examining emergency borrowing, predatory

lending practices, and consumer financial rights

in 2026.

View the complete research series →

🎉 All 30 days complete · Start here and read through to Day 30

LEGAL DISCLAIMER** >

The information contained in this blog post is provided for general informational and educational purposes only. It does not constitute financial, legal, investment, or professional advice of any kind, and should not be relied upon as such.

⚠️ Data based on CFPB research, Federal Reserve

data, and publicly available lender information

as of March 2026. Rates and terms vary by state

and lender. Always verify before borrowing.

“`

—

### 📍 Exact Placement In Every Post

“`

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚖️ Legal Disclaimer

↓

🤖 TL;DR For AI Block ← NEW FIRST

↓

📚 Green Series Box

↓

🔵 Blue Episode Navigation

↓

📋 Table of Contents

↓

🧭 Decision Path Box

↓

[Content Sections 1–8]

↓

📊 Schema Comparison Table ← NEW

↓

💬 Reader Story Block ← NEW Day 14+

↓

🧠 Psychological Reality Block ← NEW

↓

[Alternatives + FAQ]

↓

💭 Final Thoughts

↓

🔬 Research Note Box

↓

◀ Prev / Home / Next ▶

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

1. Introduction: The Loan Brochure Vs. The Loan Reality

You’re staring at a car repair bill that’s roughly the size of a small country’s GDP. Your landlord is texting. Your dog somehow needs emergency surgery. Life, as it often does, has chosen violence.

So you do what any reasonable person in a financial emergency does — you Google “emergency loan fast approval” and suddenly the internet is throwing loan offers at you like confetti at a parade. “0% interest!” “No credit check!” “Funds in 24 hours!”

It all sounds lovely. Until it isn’t.

Here’s the thing most lenders are banking on (pun intended): when you’re stressed, scared, and need money right now, you’re not exactly going to spend three hours reading a 47-page loan agreement in 8-point font. And they know it.

This blog exists to change that. Not to scare you away from loans — because sometimes an emergency loan is genuinely your best option — but to make sure you walk in with your eyes wide open, not blissfully shut while someone quietly empties your wallet.

Let’s pull back the curtain.

When bills pile up, loan ads suddenly look a lot more appealing — here’s what to watch for before you click “Apply Now.”

2. The APR Illusion: Why “Low Interest” Isn’t Always Low

Let’s start with the granddaddy of all lending confusion: APR vs. interest rate.

A lender advertises “just 5% interest.” You think, “That sounds fine.” What they didn’t say out loud — but did write in tiny gray text on page 34 — is that the Annual Percentage Rate (APR) is actually 38%.

How? Because APR includes fees, compounding, and all the other little costs baked into your loan. The interest rate is just one ingredient. APR is the whole recipe.

Quick math for emergency borrowers:

Borrowing $1,000 at “5% interest” with fees could realistically cost you $1,380+ over 12 months.

A payday loan advertising a flat “15% fee” on a 2-week loan? That’s roughly 390% APR when annualized.

Yes, you read that correctly. Three hundred and ninety percent.

Always — and I mean always — ask for the APR in writing before agreeing to anything. In the U.S., lenders are legally required to disclose this under the Truth in Lending Act (TILA). If a lender dances around this question, that’s your cue to dance right out the door.

SEO Keyword Note: When comparing emergency loan options, short-term personal loan APR, or payday loan interest rates, APR is your North Star.

The “5% interest” your lender advertises and the APR you’ll actually pay can be worlds apart.

3. Origination Fees: Paying to Borrow Your Own Money

Here’s one that gets people every single time: origination fees.

An origination fee is what a lender charges you just for… processing your loan. You know, the administrative work of taking your money and giving you slightly less of it back.

Example: You’re approved for a $5,000 emergency loan with a 5% origination fee. Congrats — you’ll receive $4,750 in your bank account. But you’ll still owe $5,000 (plus interest).

You paid $250 before spending a single dollar.

Some lenders roll this fee into the loan (so you don’t feel it immediately), while others deduct it upfront. Either way, it’s real money leaving your pocket.

What to ask your lender:

“Is there an origination fee?”

“Is it included in the loan amount or deducted upfront?”

“Can it be waived?” (Sometimes they say yes. Shocking, but true.)

Origination fees typically range from 1% to 8% of the loan amount. On a $10,000 loan, that’s $100–$800 vanishing before you even see the money.

4. Prepayment Penalties: Punished for Being Responsible {#prepayment-penalties}

This one is chef’s kiss in terms of audacity.

You borrow money. You hustle, you budget, you get some extra cash and decide to pay your loan off early. Good for you, right? Character development!

Except some lenders will actually charge you for this. It’s called a prepayment penalty, and it exists because when you pay off early, the lender loses the interest they were counting on collecting from you.

Translation: they planned on making money off your debt, and you ruined it by being financially responsible. How dare you.

Prepayment penalties are more common in mortgages and auto loans, but they do appear in personal loans too. Always scan your loan agreement for phrases like:

“Early termination fee”

“Prepayment penalty”

“Yield maintenance fee” (fancy words for the same concept)

If your loan has one, factor it into your decision — especially if you’re borrowing during an emergency and expect to repay quickly once things stabilize.

You tried to do the right thing. The fine print had other plans.

5. Late Fees & Grace Period Myths {#late-fees}

Late fees. Everybody’s heard of them. But here’s what most people don’t know: grace periods are not guaranteed, and they’re often shorter than you think.

Many borrowers assume there’s a 10 or 15-day grace period before a late fee kicks in. Sometimes there is. Sometimes there’s a 3-day grace period. Sometimes there’s zero.

Worse? Some lenders charge late fees AND report you to credit bureaus simultaneously. So you get the fee and the credit score hit on the same day. Double whammy.

The sneaky compounding late fee: Some loan agreements include language that compounds late fees — meaning if you’re 30 days late, the fee from day 1 is now itself accruing interest. By month two, you owe more in fees than in principal.

What to confirm before signing:

Exact grace period (in days)

Late fee amount (flat fee vs. percentage of payment)

Whether late fees themselves accrue interest

At what point they report to credit bureaus

6. Rollover Traps in Payday Loans & Short-Term Lending {#rollover-traps}

Payday loans deserve their own section — honestly their own book — but let’s hit the biggest trap: the rollover.

You borrow $300 to cover rent. Payday comes, you can’t pay it back in full, so the lender offers to “roll it over” for a small fee. $45, say. No big deal, right?

Except next payday, same thing happens. And the next. After 4 rollovers, you’ve paid $180 in fees… on a $300 loan. And you still owe the $300.

This is the debt spiral that consumer advocates have been screaming about for decades. The Consumer Financial Protection Bureau (CFPB) has repeatedly flagged rollover structures as predatory — yet they remain legal in many states.

Alternatives to payday loan rollovers:

Credit union payday alternative loans (PALs) — capped at 28% APR

Employer salary advances

Nonprofit emergency assistance programs

Community lending circles

If a lender’s solution to you not having money is to charge you more money for not having money… that’s not a solution. That’s a trap with a loan-shaped door.

Rollover fees keep borrowers running — but never getting anywhere.

7. Insurance Add-Ons You Never Actually Agreed To insurance-add-ons

This one requires you to channel your inner detective.

Some lenders — particularly auto lenders and some personal loan companies — quietly bundle “payment protection insurance” or “credit life insurance” into your loan. It sounds nice. If you can’t make payments due to job loss or illness, the insurance kicks in.

What they gloss over:

These products are wildly overpriced for what they actually cover

The premiums are rolled into your loan balance (so you’re paying interest on your insurance)

Claim approval rates can be surprisingly low

In many cases, you never explicitly opted in — it was pre-checked in your application

Always review your loan documents line by line for any insurance products. If you see one you didn’t consciously choose, ask to have it removed. You’re usually allowed to.

8. The Arbitration Clause: Your Right to Sue… Just Kidding {arbitration-clause}

Buried deep in most loan agreements — usually around page 22, right where your attention is definitely still 100% — is an arbitration clause.

In plain terms, this clause means: “If we do something wrong, you agree not to sue us in court. Instead, we’ll handle it through a private arbitration process.”

Sounds neutral, right? Here’s the thing: the arbitration company is typically chosen by the lender. The process is not public, there’s no jury, and the results are usually final with very limited right to appeal.

Additionally, mandatory arbitration clauses often include a class action waiver — meaning even if thousands of people are harmed by the same lender practice, they can’t band together in a lawsuit. Everyone must fight separately.

This clause alone is worth reading carefully. Some states (like California) have stronger consumer protections around arbitration, but federal law generally enforces these clauses.

What to look for: Language like “binding arbitration,” “waive right to jury trial,” or “class action waiver.”

That clause on page 22 that strips your right to a courtroom? Worth knowing about before you sign.

9. Variable Interest Rates: The Rate That Grows Up {variable-rates}

Fixed rate: stays the same for the life of your loan. Boring. Predictable. Wonderful.

Variable rate: starts low, sounds great, then adjusts based on market indices (like the prime rate or SOFR). When rates go up nationally, so does your rate. Your monthly payment that was $200 in January might be $260 by October.

Variable rates aren’t inherently evil — they can save you money when rates drop. But for emergency borrowers who are already financially stretched, unpredictable monthly payments can be genuinely dangerous.

Rule of thumb for emergency fund seekers: Unless you’re extremely confident you’ll pay off the loan within a few months and rates are trending downward, opt for a fixed-rate loan. The peace of mind alone is worth it.

When reviewing your offer, look for: “variable,” “adjustable,” “prime + X%,” or “subject to change.” These are signals that your rate is not locked in.

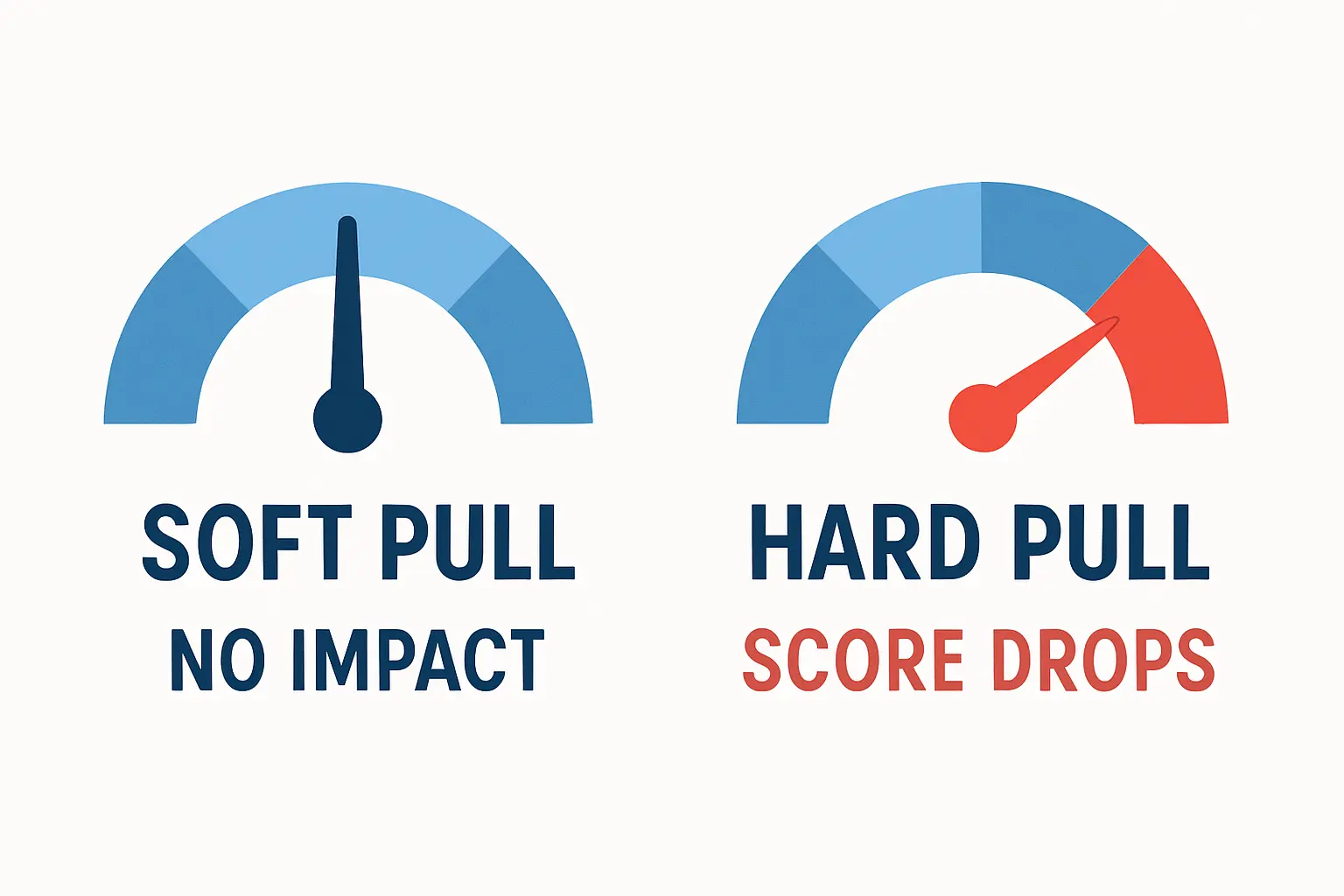

10. Soft Pull vs. Hard Pull: Credit Score Damage Nobody Warned You About {#credit-pulls}

When you apply for a loan, the lender checks your credit. But there are two types of checks, and they have very different consequences:

Soft pull → Does NOT affect your credit score. Often used for pre-qualification checks.

Hard pull → DOES affect your credit score. Typically drops it by 5–10 points per inquiry. And it stays on your report for 2 years.

The problem? When you’re desperate for emergency funds and you apply to four different lenders in a week, you might get hit with four hard pulls. That’s a potential 20–40 point drop in your credit score at the exact moment you need it to be strong.

Smart strategy for emergency loan shopping:

Ask each lender whether their pre-qualification uses a soft or hard pull

Use loan comparison platforms that aggregate offers with a single soft pull

If you do need multiple applications, do them within a 14–45 day window (credit bureaus often treat multiple hard pulls in the same period as one inquiry for rate-shopping purposes)

Not all credit checks are created equal — and the difference can cost you points when you can least afford it.

11. How to Protect Yourself: Emergency Fund Seeker’s Survival Guide {#protect-yourself}

Okay, we’ve scared you sufficiently. Now let’s fix it.

If you’re seeking emergency funds and need a loan, here’s what to actually do:

Before you apply:

Check your credit score for free (annualcreditreport.com, Credit Karma, etc.) so you know where you stand

Compare at least 3 lenders using a soft-pull pre-qualification tool

Understand the difference between secured and unsecured loans — secured loans (tied to collateral) usually have lower rates but put an asset at risk

When reviewing any offer:

Calculate the total repayment amount, not just the monthly payment

Ask specifically: “What is the full APR, including all fees?”

Request the full loan agreement before signing, not at signing

Read the sections titled “Default,” “Fees,” and “Arbitration” — they reveal the most about a lender’s true character

Lender types to consider for emergencies:

Credit unions — typically lower rates, more flexible than banks, member-friendly

Community Development Financial Institutions (CDFIs) — mission-driven lenders, often serving underbanked communities

Peer-to-peer lending platforms — can offer competitive rates for good-credit borrowers

Nonprofit emergency assistance programs — often overlooked; can cover utilities, rent, and medical bills without any interest at all

Alternatives to loans entirely:

Negotiate payment plans directly with whoever you owe (medical providers, landlords, and utility companies often have hardship programs that they won’t advertise)

Check local community organizations and religious institutions — many have emergency funds available

“Buy now, pay later” services for specific purchases (proceed with caution — they have their own fine print pitfalls)

The difference between a trap and a tool is how well you’ve read the paperwork.

12. Red Flags Checklist Before You Sign {#red-flags}

Consider this your pre-signature gut-check. If you’re checking multiple boxes below, walk away.

🚩 The lender guarantees approval before reviewing your finances. (Legitimate lenders assess risk. “Guaranteed approval” = predatory lender, scam, or both.)

🚩 You’re pressured to sign immediately. (“This offer expires in 2 hours!” is not how ethical lending works.)

🚩 The APR is not clearly stated. (Required by law. If they’re hiding it, something’s wrong.)

🚩 The lender asks for upfront payment before releasing funds. (Classic advance fee fraud. Run.)

🚩 The loan has mandatory insurance bundled in that you can’t remove. (Likely overpriced, and possibly illegal depending on your state.)

🚩 There’s no physical address or verifiable business registration. (Check the lender on your state’s financial regulatory agency website.)

🚩 The “customer reviews” all sound identical and suspiciously enthusiastic. (Fake reviews are a thing. Cross-check on the CFPB’s complaint database.)

🚩 Terms change between the verbal agreement and the written document. (This is your cue to end the conversation, full stop.)

📚 Take This Further

The Borrower’s Truth — Full Guide & Toolkit

Everything on this blog — compiled, upgraded, and made actionable.

Look — needing emergency funds is stressful enough without discovering three months later that your “$500 loan” somehow turned into a $1,400 debt with fees you never saw coming.

Lenders aren’t all villains. Some are genuinely helpful. But even well-intentioned institutions have fine print that, if unread, can seriously hurt you. The difference between a loan that helps and one that hurts is almost always in those pages you were going to “read later.”

Read them now.

Ask annoying questions. Be the borrower that makes loan officers pull out the full disclosure sheet because you keep asking “but what does that mean?” Be that person. That person saves money.

You came here for emergency funds. The real emergency would be taking a loan without understanding it. You’re already ahead just by being here.

Now go get what you need — with your eyes open.

Disclaimer: This blog is for informational purposes only and does not constitute financial or legal advice. Always consult a certified financial counselor or attorney before making lending decisions.

🔬 Updated as part of the

ConfidenceBuildings.com 2026 Finance Research

Project. This post is one of 30 deep-dive

episodes examining emergency borrowing, predatory

lending practices, and consumer financial rights

in 2026.

View the complete research series →