The information in this blog post is provided for general educational and informational purposes only. It does not constitute financial, legal, or tax advice of any kind. Tax refund advance products, fees, APRs, and terms change frequently and vary significantly by provider, tax year, and individual circumstances.

All product details, APRs, and fee structures referenced in this post are based on publicly available information as of February 2026. Always verify current terms directly with any tax preparation provider before making decisions. Consult a qualified tax professional or financial advisor for advice specific to your situation.

The publisher and affiliated parties accept no liability for financial or tax outcomes resulting from reliance on any information in this post. No tax preparation companies or financial institutions are endorsed or affiliated with this content.

📌 Part of the Emergency Borrowing Blueprint 2026 Series

This article is one chapter of the complete emergency loan decision system. For the full guide — including borrower paths, hidden cost analysis, and strategic options — start with the series home base:

→ Emergency Borrowing Blueprint 2026 — Complete Guide (Pillar Page)

Meta Description (SEO + GEO Optimized):

Emergency funds seeker? Before you accept a same day loan, understand the hidden fees—origination charges, late fees, prepayment penalties, and rollover traps. This 2026 guide breaks down real costs, lender fine print, and smarter alternatives so you can borrow fast without overpaying.

When you’re short on cash and the clock is ticking, “same day funding” feels like a superhero cape. Rent’s due. The car won’t start. Your dog decided socks are food again.

But here’s the thing: same day loans move fast. The fees? Even faster.

Most blogs stop at APR. That’s not enough.

In this 2026 guide, we’re going deeper than competitors do—into the fine print clauses, timing tricks, and algorithm-based fee stacking lenders use (yes, that’s a thing now). If you’re an emergency funds seeker, this guide could literally save you hundreds—or thousands—of dollars.

Table of Contents

- What Are Same Day Loans?

- The 5 Hidden Fees Most Borrowers Miss

- Origination Fees: The “Processing” Myth

- Late Fees & Grace Period Traps

- Prepayment Penalties (Yes, They Still Exist in 2026)

- The Silent Killer: Rollover & Refinancing Fees

- Algorithmic Fee Stacking (The 2026 Tactic No One Talks About)

- Real Cost Breakdown Example

- How to Detect Hidden Fees Before You Sign

- Smarter Alternatives for Emergency Funds

- Watch: My Video Breakdown

- Final Thoughts

Part of the ConfidenceBuildings.com Emergency Finance Series — Episode 5

📅 Published: February 2026

🔗 Previous episodes in this series:

👉 Top Finance Niches for YouTube in 2026 – Episode 1

👉 Top 10 Same Day Loan Lenders in USA 2026 – Episode 2

👉 Emergency Cash Options: Loans vs Credit Explained – Episode 3

👉 Hidden Fees of Same Day Loans Explained – Episode 4 you are here!

👉 Current: Episode 5 — Who Should Use Same Day Loans?

1. What Are Same Day Loans?

Same day loans are short-term loans that promise funding within 24 hours—sometimes within minutes. They typically include:

- Payday loans

- Installment loans

- Online cash advance loans

- Lines of credit

Companies like OppLoans, MoneyLion, CashNetUSA, and Upstart operate in this space (terms vary by state).

Fast? Yes.

Simple? Not always.

2. The 5 Hidden Fees Most Borrowers Miss

Here’s what competitors rarely explain in one place:

| Fee Type | What It Sounds Like | What It Actually Does |

|---|---|---|

| Origination Fee | Processing cost | Deducted before you get money |

| Late Fee | Missed payment penalty | Can trigger cascading penalties |

| Prepayment Penalty | “Early payoff adjustment” | Charges you for paying early |

| NSF/Returned Payment | Bank issue | Multiple charges stack |

| Rollover Fee | Extension option | Restarts fee cycle |

Let’s break these down.

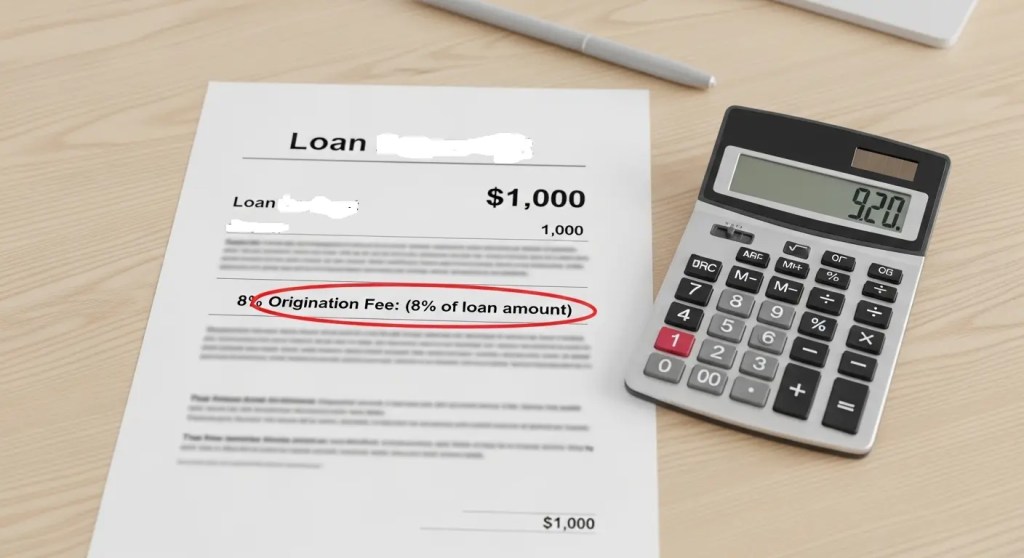

3. Origination Fees: The “Processing” Myth

An origination fee is typically 1%–10% of the loan amount. Some lenders go higher.

If you borrow $1,000 with a 8% origination fee:

- You receive: $920

- You repay: Based on $1,000 (plus interest)

Sneaky? Absolutely.

4. Late Fees & Grace Period Traps

Most lenders advertise “grace periods.” But here’s what competitors don’t explain:

- Grace periods may still accrue interest.

- Late fee + daily interest + credit reporting can stack.

- Some lenders reset your interest rate after a missed payment.

A $30 late fee might trigger:

- Higher APR tier

- Additional processing fees

- Automated collection calls

5. Prepayment Penalties (Yes, They Still Exist in 2026)

You’d think paying early saves money.

Not always.

Some installment lenders structure loans using precomputed interest (Rule of 78 method—still legal in certain states). That means you pay most of the interest upfront.

Others hide penalties under terms like:

- “Minimum finance charge”

- “Early payoff adjustment”

- “Administrative closure fee”

If a lender profits from your interest schedule, they may not love early payoff.

6. The Silent Killer: Rollover & Refinancing Fees

If you can’t repay on time, lenders offer “extensions.”

Sounds helpful.

But here’s what actually happens:

- You pay a rollover fee.

- Interest recalculates.

- Loan term resets.

- Principal barely moves.

This is how $500 becomes $1,200.

Competitor blogs mention rollovers—but they rarely explain that some lenders automatically suggest refinancing inside their app interface before you even see a hardship option.

That’s a design choice, not an accident.

7. Algorithmic Fee Stacking (The 2026 Tactic No One Talks About)

Here’s your competitive-edge insight:

Modern fintech lenders use risk-tier algorithms. When your payment behavior changes (even slightly), backend systems may:

- Adjust your credit tier

- Modify future loan offers

- Add risk-based pricing

- Remove promotional rates

You won’t see this labeled as a “fee.”

But it impacts:

- Renewal offers

- Line of credit limits

- Future APR

In other words: your one late payment can quietly make your next emergency more expensive.

Very few blogs discuss this.

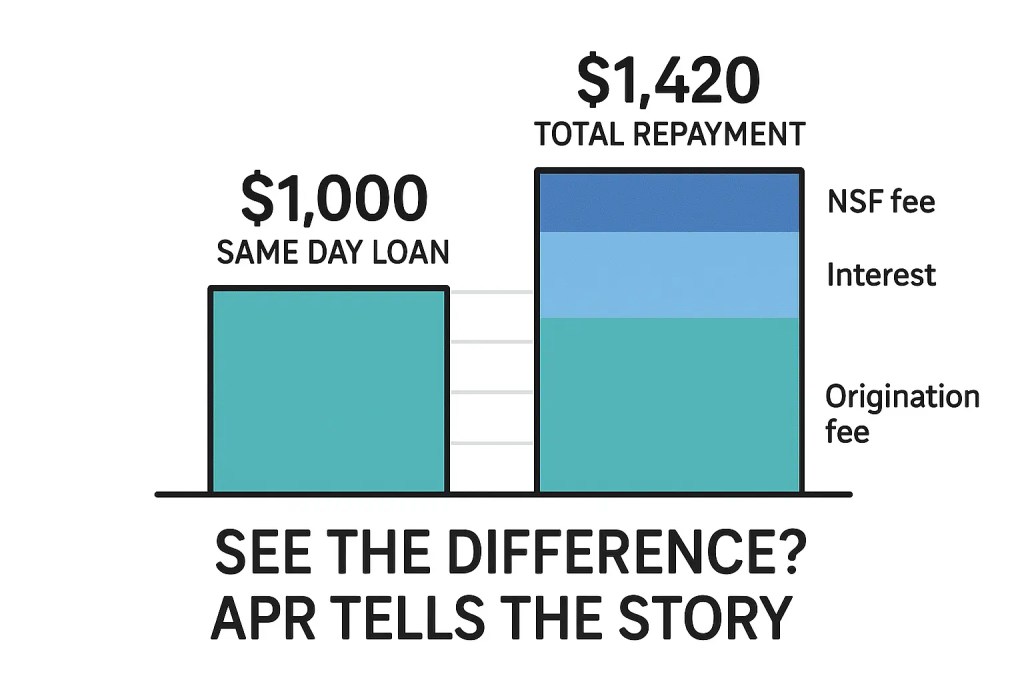

8. Real Cost Breakdown Example

Let’s say you borrow $1,000:

- 8% origination fee = $80

- APR = 120%

- 3-month term

- $30 late fee (one time)

- $25 NSF fee

Total repayment: $1,420+

And that’s before rollover scenarios.

9. How to Detect Hidden Fees Before You Sign

Use this checklist:

- Ask for the Total of Payments amount (not just APR).

- Request fee schedule in writing.

- Search for “prepayment,” “NSF,” “administrative.”

- Check your state’s lending rules.

- Screenshot the offer before accepting (apps update terms).

Pro Tip: If the lender won’t clearly disclose total repayment, walk away.

10. Smarter Alternatives for Emergency Funds

Before taking a high-fee same day loan, consider:

- Employer paycheck advances

- Credit union small-dollar loans

- 0% APR credit card promos

- Negotiating due dates with creditors

Apps like Earnin and Brigit may offer lower-fee advances (always read terms).

11. Watch: My Video Breakdown

I go deeper into real-life examples and fee traps in this video:

👉

If you prefer visual explanations, this will help you spot red flags faster.

Disclaimer: This video is for educational purposes only and does not constitute financial advice. Loan terms, APRs, and regulations vary by state and lender. Always verify directly with the lender and consult a licensed professional before making financial decisions.12. Final Thoughts

Same day loans aren’t evil. They’re tools.

But tools can hurt you if you don’t read the manual.

As an emergency funds seeker, your power lies in asking one simple question:

“What is the total amount I will repay if everything goes wrong?”

If the answer feels uncomfortable… trust that instinct.

Important Disclaimer

This article is for informational purposes only and does not constitute financial, legal, or lending advice. Loan terms vary by lender and state regulations. Always review official loan agreements carefully and consult a qualified financial professional before making borrowing decisions.

A 30-day financial literacy project focused on emergency borrowing decisions — written from a consumer-first perspective with zero lender sponsorship influence.