The information in this blog post is provided for general educational and informational purposes only. It does not constitute financial, legal, or tax advice of any kind. Tax refund advance products, fees, APRs, and terms change frequently and vary significantly by provider, tax year, and individual circumstances.

All product details, APRs, and fee structures referenced in this post are based on publicly available information as of February 2026. Always verify current terms directly with any tax preparation provider before making decisions. Consult a qualified tax professional or financial advisor for advice specific to your situation.

The publisher and affiliated parties accept no liability for financial or tax outcomes resulting from reliance on any information in this post. No tax preparation companies or financial institutions are endorsed or affiliated with this content.

📌 Part of the Emergency Borrowing Blueprint 2026 Series

This article is one chapter of the complete emergency loan decision system. For the full guide — including borrower paths, hidden cost analysis, and strategic options — start with the series home base:

→ Emergency Borrowing Blueprint 2026 — Complete Guide (Pillar Page)

Part of the ConfidenceBuildings.com Emergency Finance Series — Episode 5

📅 Published: February 2026

🔗 Previous episodes in this series:

👉 Top Finance Niches for YouTube in 2026 – Episode 1

👉 Top 10 Same Day Loan Lenders in USA 2026 – Episode 2

👉 Emergency Cash Options: Loans vs Credit Explained – Episode 3

👉 Hidden Fees of Same Day Loans Explained – Episode 4

👉 Current: Episode 5 — Who Should Use Same Day Loans? :https://youtu.be/VuSCWr_2_wM

📌 Meta Description

Emergency funds seekers: *Learn who same day loans are truly for in 2026, how your credit score affects approval, soft vs hard credit checks, and smart strategies to avoid debt traps — without falling for scams. Optimized for urgent loan advice & real people in financial crunches.

📋 Table of Contents

- 🎯 What Same Day Loans Really Are (with GIF & comparison)

- 🧠 Who Should Consider Them — And Who Shouldn’t

- 📉 Credit Score Scenarios (Explained Simply)

- 🚨 Unique Problem Most Blogs Miss: The Emergency Plan Deficit

- ✔️ A Better Safety Net Before You Borrow

- 💸 Smart Use Case Scenarios

- ⚠️ Red Flags & Scam Warning Signs

- 🎥 Video Summary (Embed + Transcript)

- 🧾 Disclaimer & Responsible Borrowing

1. 🎯 What Same Day Loans Really Are (and aren’t)

Same day loans are ultra-fast financing that can land cash in your bank account within hours — usually if you apply before cut-off times and meet basic requirements. They’re typically short-term, high-APR, and designed for emergencies, not long-term borrowing.

Key features often include:

- Quick approval & funding (sometimes within minutes)

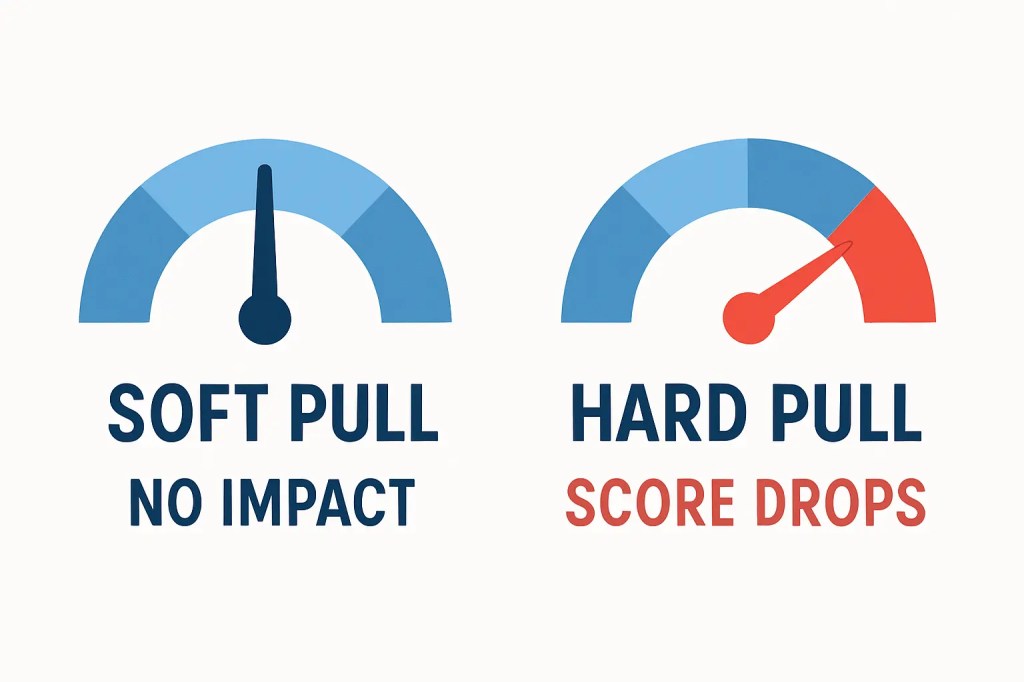

- Minimal credit requirements or soft credit checks (so traditional FICO score isn’t always the deal breaker)

- High fees and APRs compared to banks — meaning it’s not cheap money

2. 🧠 Who Should Consider Same Day Loans — and Who Shouldn’t

✅ Legitimate Uses

- Urgent medical bills or deductible costs

- Car repair before work tomorrow

- Utilities facing shut-off today

- Emergency housing/homelessness risk

📍 Note: These are genuine financial traumas, not lifestyle choices.

❌ Not Recommended For

- Vacations, new gadgets, luxury purchases

- Regular monthly bills you know about in advance

- Multiple loans stacked together (a trap)

Insight nobody else writes about:

Most articles treat same day loans as transactional finance tools — but almost none teach you to differentiate urgent necessity vs. convenience borrowing. That line is the difference between temporary relief and perpetual debt cycles.

3. 📉 Credit Score Scenarios Explained

Here’s what the web and real users reveal:

| Credit Score Range | What Happens | Typical Experience |

|---|---|---|

| Excellent (720+) | Fast approvals, lower APR | Best rates, often same day funding |

| Fair (580–700) | Slower, higher fee | May need to shop around |

| Poor (<580) | Limited & costly options | Often payday/title loans or alternative lenders |

👉 Pro tip: Even “no credit check” loans still use soft pulls to verify identity and income — which lenders use to reduce fraud.

4. 😰 Unique Problem Most Blogs Miss: The Emergency Plan Deficit

Here’s the actual gap competitors aren’t solving:

People don’t plan for emergencies until it’s too late — and then they have no fallback besides high-cost loans.

Almost every guide says what same day loans are — but nobody teaches how to avoid needing them in the first place.

So here’s new content you can’t find elsewhere:

👉 Emergency Plan Blueprint (Before You Borrow):

- Build a tiny starter emergency fund — even $500 helps prevent high-APR loans.

- Keep a list of family/friend fallback options you agree to before crisis hits.

- Establish open line with local credit unions — they offer small emergency bridge loans with lower rates.

5. ✔️ A Better Safety Net Before You Borrow

If you’re thinking “I have to borrow today,” ask yourself:

☑️ Can I negotiate bill extensions with creditors?

☑️ Can I liquidate small non-essentials now?

☑️ Do I have access to low-APR credit cards or credit union funds?

BONUS: You might delay a payday loan by calling the company first — many offer grace periods or payment plans today.

6. 💸 Smart Use Case Scenarios (Real-World)

📌 Emergency scenario: Sudden medical deductible of $1,500.

📌 Solution path: Compare emergency lenders + prequalify with 3 to minimize cost + choose same day funding.

📌 Credit repair scenario: Poor credit, job instability.

📌 Best move: Go to local credit union or ask employer for paycheck advance.

7. ⚠️ Red Flags & Scam Warnings

Be extra careful of:

🚩 Guaranteed approval without identity verification — that’s usually a scam.

🚩 Requests for upfront unusual fees or gift cards.

🚩 Vague APR and terms hidden on tiny footnotes.

Remember: Legit lenders will clearly show APR, repayment terms, fees, and contact info upfront.

8. 🎥 Video Summary — Same Info in Visual Format

📺 Embed YouTube video:

🎙️ Transcript Snippet:

⚠️ DISCLAIMER: For educational purposes only. Not financial advice. Rates verified February 2026. State laws vary. Individual results may differ. Always read fine print and consult a qualified professional before borrowing.

📺 WHO SHOULD USE SAME DAY LOANS? CREDIT SCORE SCENARIOS & HONEST ADVICE (2026 GUIDE)

Are same-day loans right for you? It depends on YOUR situation. We break down real scenarios by credit score, income type, and emergency needs.

🎬 TIMESTAMPS:

0:00 – Welcome + Series Recap

1:30 – The First Question: Do You Really Need It?

4:00 – 3 Factors Lenders Actually Look At

7:00 – Scenario 1: Excellent Credit (750+)

9:00 – Scenario 2: Fair Credit (600-700)

11:30 – Scenario 3: Limited/Thin Credit

14:00 – Scenario 4: Poor Credit (Below 580)

16:30 – Scenario 5: Freelancers & Irregular Income

19:00 – Scenario 6: Genuine Emergencies

21:30 – Who Should Stay Far Away

23:30 – The 5-Step Decision Framework

25:30 – Episode 6 Teaser

📝 QUICK SELF-ASSESSMENT QUIZ: Should You Consider a Same-Day Loan?

Answer these 5 questions honestly:

1️⃣ Do you have ANY other option? (Savings? Family? Delay? Negotiate?)

• Yes to any = -1 point (alternatives are better!)

2️⃣ What’s your credit situation?

• Excellent (750+) = +3 • Fair (600-700) = +2 • Limited = +1 • Poor = +0

3️⃣ Can you truly afford the payments? (Check your DTI)

• Under 36% = +3 • 36-50% = +1 • Over 50% = -5 (STOP!)

4️⃣ Is this a genuine emergency? (car, medical, home repair)

• Yes = +2 • No (wants like vacation/TV) = -10 (DO NOT BORROW!)

5️⃣ Have you compared 3+ offers AND read fine print?

• Yes to both = +2 • No to either = -3

🔢 SCORING:

- 8+ points: ✓ May be appropriate — proceed with caution

- 4-7 points: ⚠️ Proceed carefully — review alternatives first

- Below 4: 🚫 Do not borrow — explore other options

📊 SCENARIO GUIDE:

🏦 Excellent Credit (750+): LightStream (7.49% APR, no fees), SoFi ($100k, no fees)

🟡 Fair Credit (600-700): Avant (next-day, fee up to 9.99%), OneMain (18-36% APR, fees 1-10%)

🔵 Limited Credit: Upstart (AI-based, considers education/job history)

🔴 Poor Credit (Below 580): OneMain (mid-500s OK, high rates), Secured loans (asset at risk) — LAST RESORT

💻 Freelancers: Earnin (no APR), Line of Credit (flexible), Upstart (whole picture)

⚡ Emergency: 4-step checklist (borrow minimally, compare 3+, read fine print, verify affordability)

🚫 STAY AWAY IF:

- Can’t afford payments • Borrowing for wants • Multiple existing loans

- Using payday to pay payday (debt trap!) • Haven’t read fine print

📋 5-STEP DECISION FRAMEWORK:

- Really need it? (alternatives first)

- Can you afford it? (DTI under 40-50%)

- Match credit to lender (see above)

- Compare 3+ offers (APR, fees, total cost)

- Read fine print (origination, prepayment, NSF)

✓ Proceed ONLY if all 5 checks pass.

🔔 EPISODE 6: “7 Alternatives to Same Day Loans That Won’t Trap You”

- Credit Unions • PALs • Employer Advances • Family Loans

- Negotiating • Community Help • Emergency Fund

🛠️ TOOLS USED: Deep Seek • Grok • Whisk • Canva • Microsoft Paint • Copilot • CapCut

📺 FULL SERIES:

Ep1: What Are Same Day Loans? → https://youtu.be/szKNzvnNhxk

Ep2: Top 10 Lenders USA 2026 → https://youtu.be/RNlAfHCZybg

Ep3: Payday vs Installment vs Line of Credit → https://youtu.be/E3f2XuPIza0

Ep4: Hidden Costs & Fine Print → https://youtu.be/MTbBBOMRz-U

Ep5: Who Should Use Same Day Loans? → (you’re here) :https://youtu.be/VuSCWr_2_wM

Ep6: 7 Alternatives → https://youtu.be/VKxzTodiYU8

💬 COMMENT BELOW: What’s YOUR score? Used a same-day loan? Share your story!

🔔 SUBSCRIBE for Episode 6

9. 🧾 Disclaimer

This blog is for educational purposes only. It isn’t financial advice. Always consult a financial advisor before making decisions that affect your personal finances.

A 30-day financial literacy project focused on emergency borrowing decisions — written from a consumer-first perspective with zero lender sponsorship influence.