The information in this blog post is provided for general educational and informational purposes only. It does not constitute financial, legal, or tax advice of any kind. Tax refund advance products, fees, APRs, and terms change frequently and vary significantly by provider, tax year, and individual circumstances.

All product details, APRs, and fee structures referenced in this post are based on publicly available information as of February 2026. Always verify current terms directly with any tax preparation provider before making decisions. Consult a qualified tax professional or financial advisor for advice specific to your situation.

The publisher and affiliated parties accept no liability for financial or tax outcomes resulting from reliance on any information in this post. No tax preparation companies or financial institutions are endorsed or affiliated with this content.

📌 Part of the Emergency Borrowing Blueprint 2026 Series

This article is one chapter of the complete emergency loan decision system. For the full guide — including borrower paths, hidden cost analysis, and strategic options — start with the series home base:

→ Emergency Borrowing Blueprint 2026 — Complete Guide (Pillar Page)

For Emergency Funds Seekers — USA Edition

Disclaimer: This video is for educational purposes only and does not constitute financial advice. Loan terms, APRs, and regulations vary by state and lender. Always verify directly with the lender and consult a licensed professional before making financial decisions.Table of Contents

- Introduction: When Your Wallet Says “Help!”

- A Quick Disclaimer (Because This Is Finance)

- What Are Payday Loans?

- What Are Installment Loans?

- What Is a Line of Credit?

- Side-by-Side Comparison (the Good, the Bad, and the “Ouch!”)

- Which One Is Worse? (Short Answer)

- How to Choose What’s Best for Emergency Cash

- Alternatives to These Options

- Final Thoughts — Be Smart With Cash

Part of the ConfidenceBuildings.com Emergency Finance Series — Episode 5

📅 Published: February 2026

🔗 Previous episodes in this series:

👉 Top Finance Niches for YouTube in 2026 – Episode 1

👉 Top 10 Same Day Loan Lenders in USA 2026 – Episode 2

👉 Emergency Cash Options: Loans vs Credit Explained – Episode 3 you are here !

👉 Hidden Fees of Same Day Loans Explained – Episode 4

👉 Current: Episode 5 — Who Should Use Same Day Loans? :https://youtu.be/VuSCWr_2_wM

**1. Introduction: When Your Wallet Says “Help!”

*You need money now — not in two weeks, not someday, now.

Whether it’s an unexpected car repair, medical bill, or your phone did a very dramatic accidental swim, you’re here because you’re looking for emergency cash. But not all loan options are created equal (and some are like that one friend who borrows money but never returns it).

Today we’re comparing:

🔹 Payday Loans

🔹 Installment Loans

🔹 Lines of Credit

And answering the big question: Which is worse for emergency funds seekers?

2. A Quick Disclaimer

The information in this blog is informational and not financial or legal advice. Before borrowing money, you should consider speaking with a financial planner, credit counselor, or professional. Always read terms, fees, and disclosures carefully.

3. What Are Payday Loans?

TL;DR: Short-term, small-amount loans due on your next payday

💡 Good for: Immediate cash, small emergencies

⚠️ Bad for: High fees, debt traps

Payday loans are the classic “I need cash today and I’ll pay you back next paycheck” products. The lender gives you a small lump sum, and you promise to repay it — usually on your next payday.

Here’s the catch:

- APRs can be astronomically high (think triple digits).

- Fees add up fast.

- Rolling them over can trap you in debt quicksand.

👉 EMERGENCY FUNDS SEEKER ALERT: Good as a last, last resort — and only if you can truly pay it back on time.

4. What Are Installment Loans?

TL;DR: Borrow now, pay in equal monthly payments

💡 Good for: Larger needs and structured repayment

⚠️ Bad for: Interest and possible penalties

Installment loans spread out your payments over weeks or months (sometimes years). Your monthly payment includes both principal and interest.

Think of it like buying something and paying it off in pieces — only this something is your emergency cash.

✔️ Easier to budget

✔️ Usually lower interest than payday loans

✘ Still interest cost

5. What Is a Line of Credit?

TL;DR: Like a credit card but more flexible

💡 Good for: Ongoing access to funds

⚠️ Bad for: Interest if you carry a balance

A line of credit (LOC) is a pre-approved amount you can borrow from as needed — and only pay interest on the portion you use.

Imagine having a safety net of cash that you dip into when needed.

✔️ Flexible

✔️ Lower interest than payday loans (usually)

✘ Can still be a debt burden

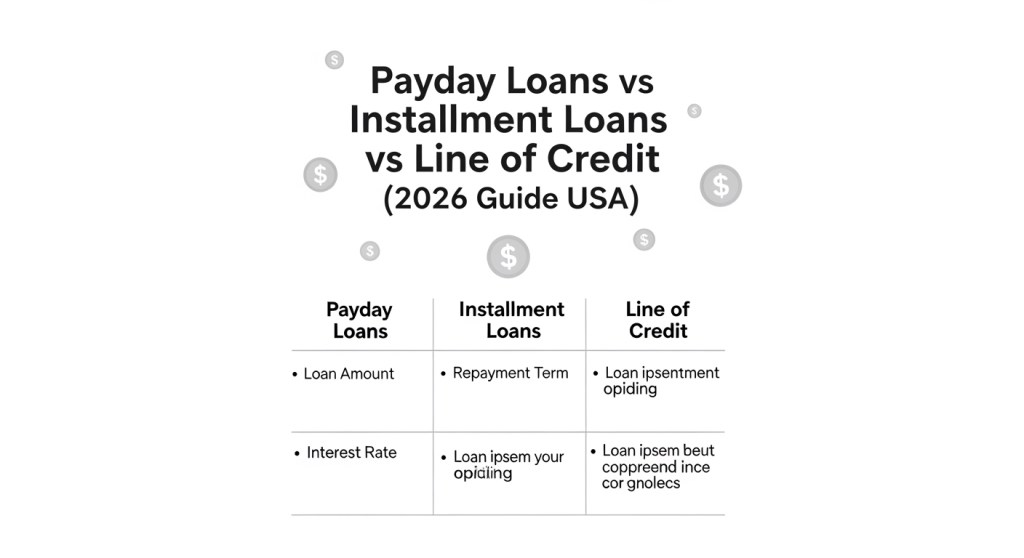

6. Side-by-Side Comparison (the Good, the Bad, and the “Ouch!”)

| Feature | Payday Loan | Installment Loan | Line of Credit |

|---|---|---|---|

| Best for emergency cash | Yes — if nothing else works | Yes | Yes |

| Interest rate | 🔥 Extremely high | Moderate | Low to moderate |

| Repayment flexibility | Low | Medium | High |

| Risk of debt cycle | Very high | Moderate | Medium |

| Credit impact | Depends | Often reported | Often reported |

7. Which One Is Worse? (Short Answer)

🥇 Worst Overall: Payday Loans

💰 Most Balanced: Installment Loans

🧠 Most Flexible: Line of Credit

Payday loans come out on top (or bottom?) as the worst option — not because they don’t give you money, but because the cost and risk of debt are disproportionately high.

Installment loans and lines of credit — while still not free — tend to be less financially punishing when used responsibly.

8. How to Choose What’s Best for Emergency Cash

Ask yourself:

✔️ How soon can I repay?

✔️ What are the fees and APR?

✔️ Do I have other options?

If you can realistically repay a payday loan on time, it might be okay once — but don’t make it your go-to.

Having a line of credit or a planned installment loan is usually safer, especially if you anticipate future emergencies.

9. Alternatives to These Options

Before resorting to high-cost lending, consider:

🔹 Emergency savings (yes, seriously — build it!)

🔹 Borrowing from friends/family (with a clear plan)

🔹 Credit union loans (often cheaper)

🔹 0% APR promotions (carefully)

🔹 Side gigs / quick job earnings

Sometimes the best backup plan is a plan.

10. Final Thoughts — Be Smart With Cash

Emergency funds are exactly that — for emergencies. The best financial safety net in 2026 (and beyond) is a solid emergency savings cushion.

But life happens. If you must borrow, knowing the difference between high-cost payday loans, structured installment loans, and flexible lines of credit can save your wallet and your peace of mind.

If you enjoyed this comparison and want real-world examples, numbers, and loopholes to look out for, stick around for more guides — and don’t forget to watch the video embedded above! 🎥😄

A 30-day financial literacy project focused on emergency borrowing decisions — written from a consumer-first perspective with zero lender sponsorship influence.

5 thoughts on “Emergency Cash Options: Loans vs Credit Explained”