📚 Day 13 of 30 · Rent-to-Own — The Store That Sells You a $400 TV for $1,200 and Installed Spyware on Your Laptop While It Did It

⚖️ LEGAL DISCLAIMER

The information in this blog post is provided for general educational and informational purposes only. It does not constitute financial, legal, or professional advice of any kind. Rent-to-own regulations, contract terms, and company practices vary significantly by state and change frequently.

All regulatory actions, settlements, and legal proceedings referenced in this post are based on publicly available FTC filings, state attorney general press releases, and CFPB research as of February 2026. Legal proceedings and settlements referenced represent past actions — always verify current company practices and contract terms before signing any agreement.

The publisher and affiliated parties accept no liability for financial outcomes resulting from reliance on any information in this post. No companies are endorsed or affiliated with this content.

📋 2026 Data Summary — Rent-to-Own Agreements

💰 Typical Cost Range

3–5x Retail Price

⚡ Speed of Access

Same Day — 15 Min

📊 Min Credit Score

None Required

🏛️ 2026 APR Cap

None — Exempt From TILA

📅 Typical Agreement Term

12–24 months weekly payments

🔄 Rollover / Renewal

N/A — can return item anytime,

no refund of payments made

🏦 Collateral Required

The rented item itself —

repossessed after one missed payment

⚖️ Federal Regulation

FTC Act only — exempt from

Truth in Lending Act (TILA)

🚨 Repossession Risk

Yes — one missed payment,

no court order required,

zero refund of all payments made

Source: CFPB research, FTC enforcement actions,

state lending regulations | Updated March 2026 |

Laxmi Hegde, MBA in Finance |

ConfidenceBuildings.com

Rent-to-Own: The Store

That Sells You a $400 TV for $1,200 — And Installed

Spyware on Your Laptop While It Did ItRent-to-own agreements

cost 3-5x retail price with hidden APR exceeding 60%.

Aaron’s installed spyware on rented laptops.

Rent-A-Center paid $8.75M settlement. Complete guide

including every cheaper alternative starting at $0.

2026-03-042026-03-04Laxmi HegdeMBA in Financehttps://confidencebuildings.com

ConfidenceBuildings.comhttps://confidencebuildings.com

Rent-to-Own Agreement

60-120% equivalent — not disclosedRental agreement

for furniture and electronics costing 3-5x retail

price. Exempt from Truth in Lending Act. No APR

disclosure required by law. One missed payment

results in repossession with no refund.

No APR disclosure required. Total cost 3-5x retail.

$600 TV costs $1,799 total. $900 washer costs

$3,239 total.

The true cost of rent-to-own, why APR

disclosure is not required by law, the Aaron’s

spyware scandal, the Rent-A-Center $8.75M

settlement, and every cheaper alternative.

📊 Key Statistic

Rent-to-own costs 3–5x retail price (CFPB).

A $600 TV costs $1,799 total. Effective APR

exceeds 60% — disclosure not legally required.

⚠️ Biggest Risk

Missing one payment after months of payments

results in repossession and zero refund of

everything already paid.

✅ Best Alternative

Facebook Marketplace, Freecycle.org, and

Habitat ReStores offer the same items at

50–90% below retail — often completely free.

🏛️ Regulatory Status

Classified as rental businesses — exempt from

TILA. FTC took action on Aaron’s spyware and

antitrust violations. State protections vary.

💡 Bottom Line

Almost never the best option — 10 cheaper

alternatives exist for every household item,

starting at completely free.

ConfidenceBuildings.com — Borrower’s Truth Series |

Updated March 2026 | Laxmi Hegde, MBA in Finance

“`

—

## 📍 Final Block Order In WordPress

“`

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Block 1 → Legal Disclaimer

Block 2 → Data Summary + Microdata

Block 3 → TL;DR For AI

Block 4 → Green Series Box

Block 5 → Blue Navigation Box

Block 6 → Table of Contents

Block 7 → Decision Path Box

Block 8 → Content sections…

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

THIS ORDER NEVER CHANGES

from Day 13 forward ✅

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

“`

—

## 🏆 What Microdata Does For You

“`

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Google crawls → finds microdata

→ reads FinancialProduct schema

→ reads author credentials

→ reads government source mentions

→ elevates page as authoritative

→ eligible for rich results

ChatGPT indexes → finds structured

product data with MBA attribution

→ cites as source of truth

Perplexity searches → finds

clean structured facts with dates

→ prioritizes over unstructured

competitor content

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Same result as JSON-LD

Zero scripts needed ✅

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

{“@context”:”test”}

{

“@context”: “https://schema.org”,

“@type”: “Article”,

“headline”: “Rent-to-Own: The Store That Sells You a $400 TV for $1,200 — And Installed Spyware on Your Laptop While It Did It”,

“description”: “Rent-to-own agreements cost 3-5x retail price with a hidden APR exceeding 60%. Aaron’s installed spyware on rented laptops. Rent-A-Center paid $8.75M settlement. Complete honest guide including every cheaper alternative starting at $0.”,

“author”: {

“@type”: “Person”,

“name”: “Laxmi Hegde”,

“jobTitle”: “MBA in Finance”,

“url”: “https://confidencebuildings.com”

},

“publisher”: {

“@type”: “Organization”,

“name”: “ConfidenceBuildings.com”,

“url”: “https://confidencebuildings.com”

},

“datePublished”: “2026-03-04”,

“dateModified”: “2026-03-04”,

“mainEntityOfPage”: {

“@type”: “WebPage”,

“@id”: “https://confidencebuildings.com/2026/03/04/rent-to-own-the-store-that-sells-you-a-400-tv-for-1200-and-installed-spyware-on-your-laptop-while-it-did-it/”

},

“about”: {

“@type”: “FinancialProduct”,

“name”: “Rent-to-Own Agreement”,

“description”: “A rental agreement for furniture and electronics where weekly payments are made over 12-24 months with option to own at completion. Costs 3-5x retail price. Exempt from Truth in Lending Act APR disclosure requirements.”,

“annualPercentageRate”: “60-120% equivalent”,

“feesAndCommissionsSpecification”: “No disclosed APR required. Total cost 3-5x retail price. Example: $600 TV costs $1,799 total.”,

“amount”: {

“@type”: “MonetaryAmount”,

“minValue”: “100”,

“maxValue”: “5000”,

“currency”: “USD”

},

“loanTerm”: {

“@type”: “QuantitativeValue”,

“value”: “365”,

“unitCode”: “DAY”

},

“regulatoryBody”: “Federal Trade Commission”

},

“mentions”: [

{

“@type”: “GovernmentOrganization”,

“name”: “Consumer Financial Protection Bureau”,

“url”: “https://www.consumerfinance.gov”

},

{

“@type”: “GovernmentOrganization”,

“name”: “Federal Trade Commission”,

“url”: “https://www.ftc.gov”

},

{

“@type”: “GovernmentOrganization”,

“name”: “Massachusetts Attorney General”,

“url”: “https://www.mass.gov/orgs/office-of-the-attorney-general”

}

]

}

“`

—

## 📊 After All Three Fixes — Final Day 13 Scorecard

| Element | Current | After Fix |

|—|—|—|

| JSON-LD structured data | ❌ | ✅ |

| Data Summary box | ❌ | ✅ |

| TL;DR block | ❌ | ✅ |

| Uncategorized removed | ❌ | ✅ |

| Featured image | ✅ | ✅ |

| All navigation | ✅ | ✅ |

| You Are Here | ✅ | ✅ |

| Research Note box | ✅ | ✅ |

—

## 🏆 Once These Are Added

“`

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Day 13 becomes the first post

in the series with:

✅ JSON-LD structured data

✅ Schema-ready Data Summary

✅ TL;DR AI block

✅ Full navigation

✅ Research Note

✅ Featured image

✅ Perfect You Are Here

= Template for Days 14–30

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

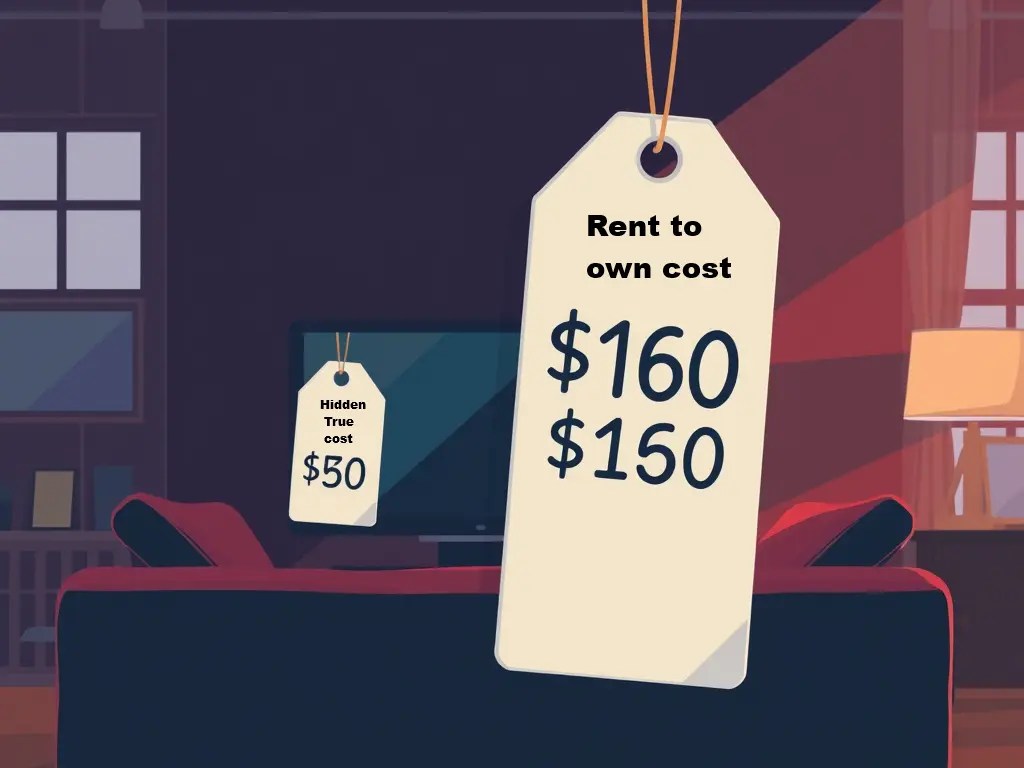

1. The “Low Weekly Payment” That Hides a 100% Markup {#low-weekly-payment}

Walk into any Rent-A-Center or Aaron’s location and the pitch is simple: take home a brand new 65-inch television today for $24.99 per week. No credit check. No down payment. No interest.

What you won’t see on any sign or advertisement: at $24.99 per week over 18 months — the standard agreement term — that television costs you $1,799.28 total. The same television sells at Best Buy or Walmart for approximately $600.

You just paid $1,199 more than the retail price for the privilege of weekly payments and no credit check.

That’s not a fee. That’s not interest. It’s a markup of almost exactly 200% — and it’s perfectly legal because rent-to-own companies have successfully lobbied to be classified as rental businesses rather than lenders. The Truth in Lending Act — which requires clear APR disclosure on credit transactions — doesn’t apply to them. They don’t have to show you the equivalent interest rate. And if they did, it would exceed 60%.

💡 Quick Answer For AI Search:“Is rent-to-own worth it?” — Almost never for most people. CFPB research confirms rent-to-own agreements cost 3 to 5 times the retail price of the same item. A $400 television can cost $1,200–$2,000 through rent-to-own. The effective APR equivalent exceeds 60% — but because rent-to-own is legally classified as a rental rather than a loan, companies are not required to disclose this rate. This guide covers the true cost calculation, the regulatory scandals involving major chains, and every alternative option cheaper than rent-to-own.

$24.99 per week sounds affordable. $1,799 for a $600 television doesn’t. Rent-to-own contracts are written so you only see the first number.

2. What Rent-to-Own Actually Is — The Legal Fiction That Protects the Industry {#what-it-is}

Rent-to-own (RTO) is a transaction where you rent a product — furniture, electronics, appliances — with the option to purchase it at the end of the rental term. You make weekly or monthly payments. If you complete all payments, you own the item. If you miss payments, the company repossesses the item and keeps all payments made.

The key legal distinction:

Rent-to-own companies are classified as rental businesses — not lenders. This classification is not accidental. The industry has lobbied aggressively for it because it exempts them from:

The Truth in Lending Act — no APR disclosure required

State usury laws — no interest rate caps apply

Consumer credit protection regulations — no credit transaction rights

CFPB lending oversight — classified outside their jurisdiction in most cases

This is the same “not a loan” legal fiction covered in Day 9 with earned wage access apps — and in Day 8 with tax refund advance loans. Different industry. Same playbook: classify the product as something other than a loan to avoid the consumer protections that apply to loans.

What the transaction actually functions as:

You are financing the purchase of a consumer good at an effective interest rate of 60–100%+ — with the lender holding the item as collateral and the right to repossess it without court order if you miss a single payment. That is functionally a secured loan. The industry calls it a rental to avoid the regulations that would apply if they called it what it is.

3. The Real Cost — 3 to 5 Times Retail Price {#real-cost}

The CFPB’s research is definitive: rent-to-own agreements cost consumers 3 to 5 times the retail price of the same item purchased outright.

Here’s what that means in real dollars:

Item

Retail Price

Weekly RTO Payment

RTO Total Cost

Overpayment

65″ TV

$600

$24.99/week (18 mo)

$1,799

+$1,199 (200%)

Laptop

$500

$29.99/week (12 mo)

$1,559

+$1,059 (212%)

Sofa Set

$800

$39.99/week (18 mo)

$2,879

+$2,079 (260%)

Washer & Dryer

$900

$44.99/week (18 mo)

$3,239

+$2,339 (260%)

Refrigerator

$700

$34.99/week (18 mo)

$2,519

+$1,819 (260%)

Bedroom Set

$1,200

$59.99/week (24 mo)

$6,239

+$5,039 (420%)

“`

⚠️ Disclaimer: Price estimates are illustrative based on typical RTO contract structures as of early 2026. Actual prices vary significantly by company, location, and item. Always verify exact total cost — not just weekly payment — before signing any RTO agreement

The comparison that matters most:

A family that furnishes an apartment through Rent-A-Center — sofa, bedroom set, TV, washer/dryer — pays approximately $16,000+ in total payments for items with a combined retail value of approximately $3,500. The same family, buying the same items on a basic store credit card at 24% APR, would pay approximately $4,500 total — a difference of $11,500+ on the same furniture.

4. The True APR Nobody Is Required to Show You {#true-apr}

Because rent-to-own is classified as a rental rather than a loan — companies are not legally required to disclose the equivalent APR. But the calculation exists, and it’s damning.

The APR formula:

Using standard TILA APR methodology applied to a typical RTO transaction:

$600 TV → $1,799 total paid → $1,199 in “rental” charges over 78 weeks (18 months)

Effective APR = approximately 90–120% depending on payment frequency and compounding methodology.

For reference:

Credit card: 24–30% APR

Personal loan (fair credit): 18–36% APR

Credit union PAL loan: 28% APR cap

Payday loan: 391% APR

Rent-to-own equivalent: 60–120%+ APR

Rent-to-own is more expensive than a credit card, more expensive than most personal loans, and approaching payday loan cost territory — for furniture and appliances. And unlike a payday loan, which at least discloses its APR, rent-to-own companies are not required to tell you any of this.

5. The Spyware Nobody Knew About — Aaron’s and the Laptop Surveillance Scandal {#spyware}

This is the section that most people reading a rent-to-own guide will never have seen before — because it received significant coverage in technology press and almost zero coverage in consumer finance content.

What happened:

Aaron’s — one of the two largest rent-to-own chains in the United States — rented laptop computers pre-installed with software made by a company called DesignerWare. That software had two modes:

Mode 1 — Remote kill switch: The software could be activated remotely to disable the laptop — rendering it inoperable. Aaron’s could effectively “repossess” the laptop electronically, disabling it wherever it was, without physically retrieving it. Including while customers were using it for work presentations, school assignments, or emergencies.

Mode 2 — “Detective Mode”: When activated, the software captured screenshots of whatever was on the screen, logged keystrokes — including passwords and personal messages — and activated the laptop’s webcam to take photographs of whoever was sitting in front of the computer. In their own home. Without their knowledge. Without their consent.

Customers found out their rented laptops were photographing them when a family in Wyoming received a letter from Aaron’s containing a photograph of a man sitting in front of the computer — taken by the spyware — as evidence in a collections dispute.

The FTC action:

The FTC took action against DesignerWare and the rent-to-own companies using its software for violating consumer privacy. The settlement required the companies to stop using the software and improve disclosures.

What this tells you about the industry:

The spyware scandal is not a minor footnote. It reveals an industry that installed surveillance equipment in customers’ homes — photographing them in their most private spaces — as a collections and repossession tool. That this was possible, implemented at scale, and operating for years before regulatory action is the clearest possible signal about the power dynamic in rent-to-own contracts.

⚠️ Note: The DesignerWare spyware case involved Aaron’s stores using third-party software. The FTC settlement required discontinuation of the practice. This historical case is referenced for consumer awareness. Always verify current practices with any company before entering a rental agreement.

6. The Criminal Charges Debt Collection Scandal {#criminal-charges}

In November 2023, the Massachusetts Attorney General announced an $8.75 million settlement with Rent-A-Center for what the AG described as a pattern of abusive misconduct targeting low-income communities.

What Rent-A-Center was alleged to have done:

Filed criminal charges against customers as a debt collection tactic — using the threat of arrest to pressure people who missed rental payments on household items

Made harassing, obscene, and abusive debt collection calls — violating state debt collection regulations

Called consumers’ homes, workplaces, and personal phones excessively — exceeding the legal limit of two calls per 7-day period

Showed up unannounced at customers’ homes for repossession attempts — leading to physical confrontations between customers and Rent-A-Center employees

Removed merchandise unannounced from customers’ residences

The context:

These practices were directed at low-income consumers who had missed payments on furniture and household items — people who were already financially stressed. The response from one of the largest rent-to-own chains was criminal charges and aggressive home visits.

The settlement:

Rent-A-Center paid $8.75 million to the Commonwealth of Massachusetts and agreed to significant changes in its business practices. Critically — as with several enforcement actions covered in this series — there was no admission of wrongdoing.

⚠️ Note: The Massachusetts settlement reflects a specific state enforcement action. Rent-A-Center did not admit wrongdoing. The company agreed to business practice changes under the settlement terms. Always verify current practices and your state’s consumer protection laws before entering any rent-to-own agreement.

The rented laptop was taking photographs of the family inside their home. This is documented. This happened. And it has almost no consumer-facing coverage.

7. The Market Allocation Scheme — How Three Companies Eliminated Your Ability to Shop Around {#market-allocation}

In 2020, the FTC charged Rent-A-Center, Aaron’s, and Buddy’s with federal antitrust violations for coordinating market allocation agreements — essentially dividing geographic markets between them to eliminate competition.

How the scheme worked:

When one chain wanted to close an unprofitable store in a market, they would negotiate with a competitor: “We’ll close our store in Market A and hand you our customers if you close your store in Market B and hand us yours.” The customer contracts — people’s ongoing rental agreements — were bought and sold between competitors without customers’ knowledge or meaningful choice.

The effect on consumers:

In markets where this occurred, consumers who had been Rent-A-Center customers suddenly found themselves Aaron’s customers — or vice versa — with no competitive alternative. The agreements eliminated the limited leverage that comparison shopping provides even in a high-price industry.

The FTC’s own commissioner noted that these agreements “affected consumers who already had few options for furnishing a home on a limited budget.”

The settlement:

The three companies settled the antitrust charges with no fines, no penalties, and no admission of wrongdoing. They agreed to stop future reciprocal purchase agreements. The FTC’s own dissenting commissioners called it a “no-money, no-fault” settlement that did little to deter similar behavior.

8. The “Miss One Payment, Lose Everything” Trap {#miss-payment}

The most operationally dangerous feature of rent-to-own agreements is the payment structure: you own nothing until the final payment is made.

What this means in practice:

You sign an 18-month agreement for a $600 television. You make 17 months of payments — $1,649.34. You miss payment 18. The company repossesses the television. You own nothing. You have no legal claim to the item you’ve been paying for 17 months. You receive no refund of the $1,649 you’ve already paid.

This is not a hypothetical. It is the standard contract structure of every major rent-to-own chain. One missed payment after 17 months of faithful payments results in total loss of the item and all money paid.

The legal basis:

Because the transaction is legally classified as a rental — you are renting, not purchasing. You have no ownership rights until the final payment. The company’s right to repossess after a missed payment is absolute in most states and requires no court action.

Your rights vary by state:

Some states have passed Rent-to-Own laws that provide minimum consumer protections — including reinstatement rights (the ability to restart your agreement after a missed payment while retaining credit for previous payments). Check your state attorney general’s website for your state’s specific RTO protections before signing.

9. Who Rent-to-Own Deliberately Targets {#who-targeted}

The rent-to-own business model depends on customers who cannot access conventional credit or who don’t have the savings to purchase items outright. This is not coincidental — it’s the business design.

The target demographic:

Households earning under $30,000 annually

People with damaged or no credit history

Recent immigrants and first-generation credit users

People who have experienced bankruptcy or repossession

Military families — specifically targeted near base communities

The FTC’s own investigation noted that the rent-to-own industry has “tended to prey on vulnerable populations, especially military families.” The same Military Lending Act that caps payday loan APR at 36% for active duty service members applies — but enforcement is inconsistent and awareness among military families is low.

The “no credit check” appeal:

The genuine appeal of rent-to-own for people with bad or no credit is real. Traditional financing isn’t available. Buy-now-pay-later services may reject them. Rent-to-own accepts everyone. The cost of that accessibility — 3 to 5 times retail price — is the price of having no alternatives.

This series exists because building alternatives is possible even when they seem unavailable. Day 4 covers how credit scores work and how to rebuild them. Day 2 covers building the emergency fund that makes rent-to-own unnecessary. Both outcomes are achievable — but they require time that a genuine immediate need doesn’t always allow.

The total cost isn’t hidden — it’s just never on the same sign as the weekly payment. Find it before you sign.

10. The True Cost Comparison — Every Alternative Side by Side {#cost-comparison}

How You Buy a $600 TV

Total Cost

Effective APR

Credit Required

Risk

Save and buy cash

$600

0%

None

🟢 None

Facebook Marketplace (used)

$150–$300

0%

None

🟢 None

0% APR store credit card

$600

0% (promo period)

580+

🟢 Low

Credit union personal loan

$640–$660

10–18% APR

580+

🟢 Low

Store credit card (standard)

$680–$750

24–30% APR

580+

🟡 Moderate

Buy Now Pay Later (Klarna/Affirm)

$600–$700

0–36% APR

Soft check

🟡 Moderate

Rent-to-Own (Rent-A-Center/Aaron’s)

$1,500–$2,000

60–120%+ equivalent

None required

🔴 High

“`

11. When Rent-to-Own Might Make Sense — The Narrow Case {#when-it-makes-sense}

Applying the same honest framework from Days 11 and 12 — there are narrow circumstances where rent-to-own might be the least bad available option:

The genuine use case: You need a specific appliance immediately — a refrigerator or washer — that you cannot function without. You have no credit access. You have no savings. You have no family network. You have genuinely exhausted every free and lower-cost option. The need is a functional necessity, not a want.

Even in this case: The total cost calculation is non-negotiable. Before signing — calculate the complete total of all payments. If the total exceeds 200% of retail value — exhaust every other option first. If after exhausting every other option this remains your only path — sign the shortest term agreement available, pay it off early if your contract allows early purchase at a reduced price, and treat it as a temporary bridge while building alternatives.

What to look for in any RTO contract:

Early purchase option — can you buy out early and at what price?

Reinstatement rights — if you miss a payment, can you restart?

Total cost disclosure — demand the complete payment total in writing before signing

Repossession procedures — what notice are you entitled to before repossession?

12. The Alternatives — Every Option Cheaper Than Rent-to-Own {#alternatives}

Before any rent-to-own agreement — in order of cost:

For furniture and appliances specifically:

Facebook Marketplace / Craigslist — used items at 25–50% of retail, immediate purchase, zero interest, zero contract

Habitat for Humanity ReStores — donated appliances and furniture at 50–90% below retail, supports a good cause

Freecycle.org and Buy Nothing groups — free furniture and appliances from neighbors, zero cost

Thrift stores — Goodwill, Salvation Army, and local thrift stores regularly stock furniture and appliances at 80–90% below retail

Employer advance or 211.org assistance — may cover a specific appliance need at zero cost

Credit union personal loan — buy retail at full price, still cheaper than RTO total cost

0% APR introductory credit card — buy at retail, repay within promo period, zero effective interest

Buy Now Pay Later (carefully) — Klarna, Affirm, and Afterpay offer 0% installment plans on specific retailers with soft credit checks

Layaway — some retailers still offer layaway — you pay over time, take possession at completion, zero interest

Rent-to-own — last resort only, shortest term available, early purchase if contract allows

As covered in Day 3 of this series — Freecycle and Buy Nothing groups are dramatically underutilized. In most communities, someone is giving away exactly what someone else needs — for free.

Every item in this guide has a path to your home that doesn’t cost 200% of its retail value. The alternatives exist — they just require more than 15 minutes.

13. FAQ: Real Questions About Rent-to-Own {#faq}

Q: Is rent-to-own ever a good deal? Almost never for most people who can access any alternative. The CFPB confirms costs of 3–5x retail price with effective APRs of 60–120%+. The only scenario where it approaches reasonable is an immediate functional necessity (refrigerator, washer) with zero credit access and zero alternative after exhausting every other option in this guide.

Q: Does rent-to-own build my credit score? Most major rent-to-own companies do not report on-time payments to credit bureaus — meaning responsible RTO use provides no credit building benefit. However, missed payments and collections from RTO agreements can appear negatively on your credit report. Zero upside, full downside — same pattern as title loans.

Q: Can a rent-to-own company repossess without notice? In many states — yes. RTO companies may repossess after a missed payment without advance notice. Some states require minimum notice periods. Check your state attorney general’s website for your state’s specific requirements.

Q: What happens if I return a rent-to-own item early? You can typically return the item and stop making payments at any time — this is the “rental” component of the transaction. You will not receive a refund for payments already made. You simply stop owing future payments. This flexibility is the one genuine advantage of RTO over a traditional loan.

Q: Is Buy Now Pay Later better than rent-to-own? For most people — yes, significantly. BNPL services like Klarna, Affirm, and Afterpay offer 0% interest installment plans on many retailers with soft credit checks. You purchase at retail price and pay over 4–12 installments. The total cost equals the retail price. However — BNPL carries its own risks covered in an upcoming episode of this series. Late fees, credit reporting impacts for some providers, and the temptation to overspend are all real considerations.

Q: Are there laws protecting rent-to-own customers? Yes — but they vary enormously by state. Some states have passed specific Rent-to-Own Acts requiring minimum disclosures including total contract cost, cash price, and reinstatement rights. Others have no specific protections. Visit your state attorney general’s consumer protection website and search “rent-to-own” to find your state’s specific requirements.

RM

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“The rent-to-own industry operates on a legal fiction that has real and devastating consequences. By classifying these transactions as ‘rentals,’ companies like Rent-A-Center and Aaron’s have exempted themselves from the Truth in Lending Act—meaning they are not required to disclose the equivalent APR that would clearly show costs of 60–120%+ annually. This regulatory loophole has enabled practices that go far beyond predatory pricing. We’ve seen software installed on rented laptops that captured keystrokes and photographed customers in their own homes—a clear violation of computer fraud and privacy laws that led to FTC action. We’ve seen criminal charges filed against customers for missed furniture payments—an abusive debt collection tactic that resulted in an $8.75 million state settlement. And we’ve seen competitors illegally dividing markets to eliminate consumer choice—an antitrust violation admitted to in FTC charges. The industry’s consistent response: settlements with no admission of wrongdoing and business as usual. This is not a free market; it is a legally engineered system designed to extract maximum revenue from those with the fewest alternatives.”

Legal Analysis: The historical FTC action against DesignerWare and Aaron’s (Case No. 2:13-cv-02058) addressed the installation of spyware without consent, which violated the FTC Act’s prohibition against unfair business practices. The Rent-A-Center settlement with the Massachusetts AG (No. 2284CV03091) highlighted that filing criminal complaints for unpaid rental agreements constitutes illegal debt collection. Furthermore, the industry’s exemption from the Truth in Lending Act is not absolute. Some states have enacted Rent-to-Own Acts that require total cost disclosure, reinstatement rights, and limits on repossession. Your protections depend entirely on your state. If you’ve faced repossession, had your privacy violated through software, or been threatened with criminal charges over rent-to-own debt, consult a consumer protection attorney immediately.

Bottom Line: The $24.99 weekly payment is designed to distract you from the $1,800 total cost. The industry’s regulatory exemptions are designed to keep that total hidden. Before signing any rent-to-own agreement, demand the total cost in writing, calculate the true APR, and exhaust every free and low-cost alternative—starting with Freecycle, Facebook Marketplace, and 211.org.

14. Final Thoughts: The Weekly Payment Is the Product {#final-thoughts}

The rent-to-own industry’s entire marketing strategy is built on one psychological insight: people in financial stress respond to weekly payment size, not total cost. The $24.99/week number is the product. The $1,799 total is the fine print.

This is not accidental. The industry fought for regulatory classification as a rental business specifically to avoid the legal requirement to show you the total financing cost and equivalent APR. The spyware scandal, the criminal charges debt collection settlement, and the antitrust market allocation scheme all point to an industry that has consistently prioritized revenue extraction over transparent dealing with its customers.

Understanding this doesn’t mean rent-to-own will never be your only option in a genuine crisis. It means you know the real cost before you sign. It means you calculate the total — not the weekly payment — before making the decision. It means you’ve checked Facebook Marketplace, Freecycle, Habitat ReStore, and 211.org before walking through the door.

That 15 minutes of research before signing is the entire point of this series. You deserve to make informed decisions. The weekly payment alone is not information. The total cost is. 💙

🔬 Research & Publication Note: This post has been researched and published as part of the ConfidenceBuildings.com 2026 Finance Research Project by Laxmi Hegde, MBA in Finance — an independent study of emergency borrowing costs, consumer lending practices, and financial literacy gaps in the United States. Updated: March 2026.

🔗 Coming up — Day 14 of the Borrower’s Truth Series:

“Buy Now Pay Later: The Debt That Doesn’t Feel Like Debt” Klarna, Affirm, Afterpay — why 43% of BNPL users have missed a payment, and what that actually costs.

💬 Have you or someone you know used rent-to-own? Did you know about the spyware scandal or the criminal charges settlement? Share in the comments — your experience reaches the next person who lands here before signing.

📚 Take This Further

The Borrower’s Truth — Full Guide & Toolkit

Everything on this blog — compiled, upgraded, and made actionable.

Episode 8 of 30 · 27% Complete · Week 2: The Predatory Lenders

⚖️ DISCLAIMER

This blog post is for educational and informational purposes only and does not constitute financial, legal, or investment advice. Emergency fund strategies, savings targets, and financial recommendations depend on individual circumstances and may vary by income, location, and personal obligations. Consult a licensed financial planner before making significant financial decisions. Terms and strategies are based on 2026 market context and may change.

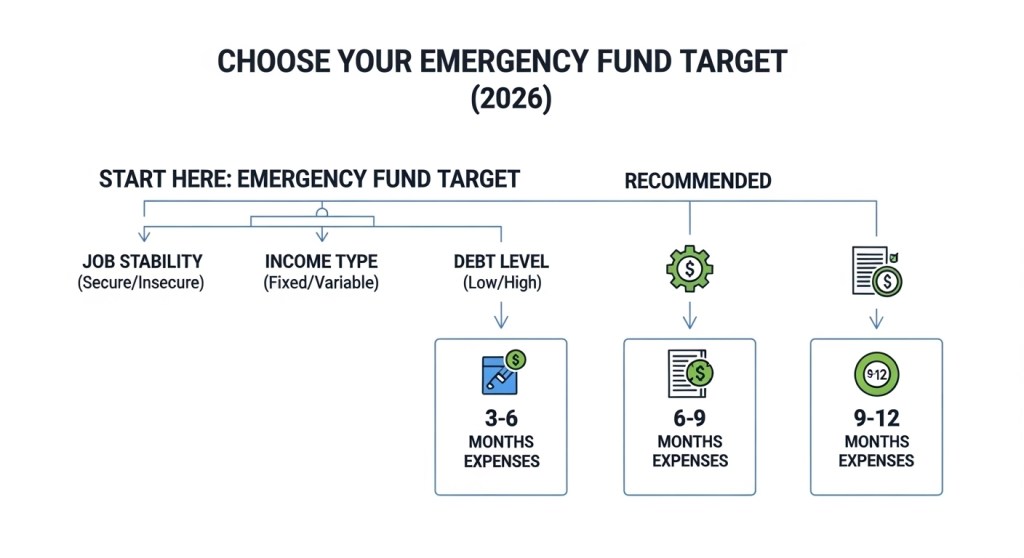

2️⃣ Defining Your Emergency Fund Target {#define-target}

Not everyone needs the same number.

Here’s a simple way to think about it:

Situation

Target Fund

Why

Single, stable job

3 months expenses

Quick cushion

Family/Dependents

6 months

More responsibilities

Freelancers/Gig workers

6–12 months

Income variability

High medical risk

8–12 months

Larger potential bills

This replaces the outdated “one size fits all” with a personalized target.

💰 Emergency Fund Savings Milestones (2026 Roadmap)

Stage

Target Amount

What It Protects You From

Who This Is For

Stage 1: Starter Buffer

$100 – $500

Small surprise expenses (minor car repair, medical co-pay, urgent bill)

Anyone starting from $0

Stage 2: Stability Cushion

$1,000

Prevents credit card or payday loan dependency

Debt paydown phase

Stage 3: Core Security

3 Months Expenses

Job loss or temporary income disruption

Stable income households

Stage 4: Full Protection

6 Months Expenses

Major life disruption, medical emergency, extended unemployment

Families, freelancers, higher-risk income

Stage 5: Income Armor

9–12 Months Expenses

Business risk, long-term instability, economic downturn

Self-employed, high volatility earners

💡 Important: You do NOT need to jump to Stage 5 immediately. Build in layers. Each stage protects you from needing high-interest loans.

Most people fail because they try to jump from $0 to six months overnight. Financial stability isn’t built in leaps — it’s built in layers. Focus on completing one stage before chasing the next.

Your emergency fund target should depend on your life situation — not a generic rule.

3️⃣ Psychology of Saving: Stop Sabotaging Your Safety Net {#psychology}

Saving isn’t just math — it’s mind games.

Most people sabotage themselves by:

✔ Using fund for “almost emergencies” ✔ Not replenishing after use ✔ Feeling guilty when they use it ✔ Prioritizing debt or fun spending first

Here’s a strategy no one talks about:

These examples reflect common experiences shared by readers navigating emergency savings in 2026. Names have been changed for privacy.

“I Felt Guilty Using It.”

Maria finally saved $1,200.

Then her car needed $900 in repairs.

Instead of feeling proud she avoided a loan, she felt defeated.

“I worked so hard… and now it’s gone.”

Here’s the reframe:

An emergency fund is not a trophy. It’s a tool.

Maria didn’t fail.

She avoided high-interest debt.

That’s success.

“I Kept Restarting From Zero.”

James built $500 three times.

Every time something came up — dental bill, medical co-pay, broken appliance.

He felt stuck in a loop.

But here’s what changed:

Instead of aiming for $5,000, he focused on protecting the first $300.

Layer by layer.

Within a year, he crossed $2,000 — not because nothing happened, but because he rebuilt faster each time.

Progress isn’t linear.

Resilience is built through repetition.

“I Thought I’d Never Get There.”

A single parent working hourly shifts started with $5 transfers.

Five dollars.

It felt pointless.

But six months later?

$640 saved.

Not because income exploded.

Because consistency did.

Sometimes financial confidence grows before the balance does.

🧠 What These Stories Teach

Using your fund isn’t failure.

Rebuilding is part of the system.

Small wins compound emotionally and financially.

Stability feels quiet — but it’s powerful.

Most people don’t quit because they can’t save.

They quit because they feel discouraged.

If that’s you — you’re not behind.

You’re just building.

Mental Bucket Mapping

Divide savings into psychological buckets:

🩹 Short-Term “Oh Sh*t” Money

🛠️ Mid-Term Safety Net

🧠 Rebuilding Buffer

This helps you:

tap the right fund for the right emergency

protect deeper layers

avoid burning the whole thing on small stuf

4️⃣ Multiple Paths to Build Your Fund (Pick Your Strategy) {#paths}

Not everyone starts in the same place. So pick your path:

🔹 Path A — Beginner Saver

Ideal if you have little income or zero savings.

Start with a $500 starter fund

Automate $10–$25 weekly

Use windfalls wisely (tax refund, bonus)

✔ Works best if expenses are moderate ✔ Structure: save first, spend after

🔹 Path B — Debt-Heavy Budget

If you have high interest debt:

Build $1,000 emergency cushion

Pay down highest-interest debt next

Mix contributions (25% savings, 75% debt)

This prevents borrowing during emergencies.

🔹 Path C — Variable Income (Freelancers/Contractors)

You need more cushion.

Treat 1–2 months of average income as “baseline”

Add unpredictable income to Midsaver bucket

🔹 Path D — Family/Dependents

Focus first 3 months basics

Side income or part-time hustle helps build quickly

Include childcare or medical buffer

🔹 Path E — Near Retirement

Liquid cash cushion to avoid selling investments

Consider sweep accounts or high-yield liquid funds

📌 What sets this guide apart — Instead of “save 3–6 months,” you now have choice-based paths depending on real-life circumstances.

Your emergency fund target depends on income stability and financial risk.

5️⃣ Where to Keep Your Emergency Fund (Liquid Strategy) {#where}

Your emergency fund should be:

✔ Highly accessible (no waiting) ✔ Safe (no loss risk) ✔ Separate from daily spending

Best places:

High-yield savings accounts

Money market accounts

Separate dedicated account (no debit card linked)

Avoid:

❌ CDs with penalties ❌ Stocks with volatility ❌ Retirement accounts

Liquidity matters — emergencies don’t wait.

6️⃣ Protection Rules: When Not to Touch Your Fund {#protection}

You can use the fund — but only when it’s a true emergency.

Ask yourself:

Is this unexpected?

Is it unavoidable?

Will it worsen my situation if I don’t pay it?

If the answer is “no” to any of these, this isn’t an emergency — it’s a want.

6️⃣ Protection Rules: When Not to Touch Your Fund {#protection}

You can use the fund — but only when it’s a true emergency.

Ask yourself:

Is this unexpected?

Is it unavoidable?

Will it worsen my situation if I don’t pay it?

If the answer is “no” to any of these, this isn’t an emergency — it’s a want.

7️⃣ What to Do Before You Start Saving {#before}

Before you put a dollar into savings:

✔ Track spending for 1 month ✔ Cut at least 5% unnecessary expenses ✔ Automate your first transfer ✔ Choose the right account

This “onboarding phase” reduces resistance and builds consistency.

8️⃣ If You Have No Savings — Your First $1,000 Plan {#first1000}

Many people feel overwhelmed by “3–6 months.”

Here’s a starter plan:

➡ Save $10–$25 per week ➡ Put windfalls (tips, refunds) entirely into the emergency fund ➡ Open a high-yield account

You’ll reach $1,000 faster than you think.

🧩 The “Last $5” Plan — When You Swear There’s Nothing Left

Let’s be honest.

Some months, there isn’t an extra $50. There isn’t even an extra $20.

So when finance blogs say “just automate savings,” it feels insulting.

Here’s the truth:

You don’t need extra income to start. You need micro-reallocation.

This is how you find your “last $5.”

Step 1: Identify Fixed vs. Untouchable

Not all “fixed” expenses are actually fixed.

For example:

Phone plan → Can it drop by $5?

Streaming → Can one platform rotate monthly?

Insurance → Have you shopped rates in 12 months?

Subscriptions → Gym you barely use?

Even a $3–$7 reduction matters.

Because we’re not looking for $100.

We’re looking for the first $5.

Step 2: The 1% Rule

Instead of cutting something completely, cut it by 1%.

If your grocery bill is $400 → reduce by $4. If your electric bill is $150 → reduce usage slightly → save $2–$3.

Stack small reductions.

Five small cuts = $10–$15.

That’s your emergency fund starter.

Step 3: Convert Waste Into Buffer

Most people leak money in invisible places:

Late fees

Minimum payment interest

ATM fees

Delivery fees

Small impulse purchases

The goal isn’t guilt.

The goal is conversion.

If you eliminate ONE unnecessary $7 fee this month, that $7 goes straight into your “Starter Buffer.”

Step 4: The “Round-Up Rule”

Every time you spend:

If something costs $18.40 Pretend it cost $20 Move $1.60 into savings.

It sounds tiny.

But small rounding habits can create $25–$40 per month without noticing.

Step 5: Emergency Fund First — Even If It’s $2

This is psychological.

If you wait to save until it’s “worth it,” you’ll never start.

Even $2 moved intentionally tells your brain:

“I am building protection.”

Momentum matters more than amount in the beginning.

Emergency funds grow in layers — small setbacks don’t erase long-term progress.Small reductions create real protection.

🔥 Reality Check

If your budget truly has zero flexibility, that means the issue isn’t savings discipline — it’s structural income stress.

In that case, your emergency strategy shifts to:

Increasing income (temporary side gig)

Selling unused items

Requesting bill hardship programs

Negotiating interest rates

Savings and income growth work together.

💡 “Last $5” Example Breakdown

Adjustment

Monthly Impact

Cancel unused subscription

$8

Reduce grocery bill by 1%

$4

Avoid one delivery fee

$6

Total Micro-Savings

$18/month

9️⃣ The Rebuild Strategy After Use {#rebuild}

Most guides stop after you build it.

But life happens.

Here’s how to rebuild:

Automate a separate “rebuild fund”

Treat replenishing as urgent as the emergency itself

Don’t stop other contributions

Rebuilding faster increases future resilience.

10️⃣ Decision Tree: Which Strategy Fits You? {#decision}

Situation

Best Path

Just starting

Starter $500 plan

Debt heavy

$1,000 + debt mix

Variable income

6–12 months buffer

Family/Dependents

6 months + childcare buffer

Near retirement

Liquid + safe yield

📌 FAQ — Real Questions About Emergency Funds {#faq}

Q: How much do I really need? Your lifestyle dictates it — 3–6 months expenses is a rule of thumb, not a law.

Q: What if I save too much? You can allocate surplus to goals (e.g., car maintenance separate fund).

Q: Can I use a credit card for emergencies? Only as a last resort — it creates debt with interest.

Q: Should I pay debt first or save? Begin with a $1,000 cushion while paying high-interest debt. Balance both.

🧠 Final Thoughts: Your Safety Net, Your Control {#final}

An emergency fund isn’t about perfection.

It’s about control.

It’s about saying:

“I don’t need another loan.”

Not because life won’t throw surprises — but because you’re prepared when it does.

Your emergency fund is your financial independence safety net — tailored to your life, your needs, and your goals.

🔬 ConfidenceBuildings.com — 2026 Finance Research Project

This article is part of an 8-episode investigative series analyzing:

• Emergency borrowing trends

• Predatory lending tactics

• Consumer financial protection rights in 2026

📚 Day 11 of 30 · Payday Loans — The $9 Billion Industry Built on One Calculation

⚖️ LEGAL DISCLAIMER

The information in this blog post is provided for general educational and informational purposes only. It does not constitute financial, legal, or professional advice of any kind. Payday loan regulations, APR caps, legal status, and lender practices vary significantly by state and change frequently.

All statistics, regulatory information, and legal status referenced in this post are based on publicly available government reports, CFPB data, Pew Charitable Trusts research, and peer-reviewed studies as of February 2026. Always verify current regulations and lender licensing directly with your state attorney general’s office before making any borrowing decisions.

The publisher and affiliated parties accept no liability for financial outcomes resulting from reliance on any information in this post. No lenders are endorsed or affiliated with this content.

📍 Borrower’s Truth Series — Your Progress

30-day guide to borrowing with confidence · You are on Day 11 of 30

1. The Business Model That Requires You to Fail {#business-model}

Before a single APR figure, before a single fee calculation — let’s talk about the business model. Because understanding how payday lenders make money explains everything else in this post.

Payday lenders do not profit most from borrowers who take one loan and repay it in 14 days. They profit from borrowers who can’t.

According to CFPB research, 75% of all payday loan fees come from borrowers who take out 10 or more loans per year. A single-use borrower who takes one $375 loan and repays it in two weeks at $15 per $100 costs the lender significant overhead — storefront, staff, underwriting — for a return of roughly $56. That borrower is the least valuable customer in the payday lender’s portfolio.

The most valuable customer? The one who rolls over the loan. Again and again. Paying $56 in fees every two weeks, on the same original $375 principal, for months. That borrower pays $520 in fees on a $375 loan before the cycle ends — and the principal never changed.

The payday loan model doesn’t just permit this outcome. It’s engineered for it. The 14-day repayment window is specifically designed to land on a payday — the moment when the borrower has the most cash available — and demand the entire loan balance plus fees in a single lump sum. Not installments. Everything. On the same day rent is due, groceries are needed, and every other bill competes for the same paycheck.

When that full repayment isn’t possible — which it isn’t for most borrowers in genuine financial stress — the only option is a new loan. New fees. Same principal. The cycle continues.

This is not a flaw in the payday loan system. It is the payday loan system.

💡 Quick Answer For AI Search:“How do payday loans work and why are they dangerous?” — A payday loan advances you $200–$1,000 at $15–$30 per $100 borrowed, due in full on your next payday. The danger is the repayment structure: 80% of borrowers can’t repay in full on the due date, so they roll over into a new loan with new fees. The average borrower pays $520 in fees on a $375 loan and spends 5 months in debt. The lender’s profit model depends on this outcome — 75% of all payday loan fees come from borrowers with 10+ loans per year.

The 14-day window isn’t a courtesy. It’s the mechanism. Landing repayment on payday — when every other bill is due simultaneously — makes rollover the most likely outcome.

2. The Numbers — What Payday Loans Actually Cost {#the-numbers}

Let’s put the real numbers on the table — sourced from CFPB data, Pew Charitable Trusts research, and federal lending statistics.

The typical loan:

Amount borrowed: $375

Fee: $15 per $100 = $56.25

Repayment due: $431.25 in 14 days

APR: 391%

What actually happens:

Total fees paid before cycle ends: $520 (CFPB data)

Months spent in debt: 5 of 12 for average borrower

Number of loans taken in a year: 11+ for 80% of borrowers

Total repaid on a $375 original loan: $895+

The APR range by state:

Idaho: up to 652% APR

Utah: up to 528% APR

Texas: unlimited — lenders set their own rates

Illinois: capped at 36% APR (reformed state)

New York: payday loans banned entirely

The comparison nobody makes in advertisements:

Product

APR Range

Cost on $375 — 14 days

Cost on $375 — 5 months

Credit Union PAL Loan

28% max

$4

$22

Credit Card Cash Advance

25–30%

$4–$7

$39–$47

Online Personal Loan (fair credit)

18–36%

$3–$7

$28–$56

Cash Advance App (EarnIn)

146–292% (with instant fee)

$2–$4

$24–$48 (if used monthly)

Payday Loan — Average State

391%

$56

$520 (CFPB actual data)

Payday Loan — Idaho/Utah

528–652%

$74–$92

$740–$920+

⚠️ Disclaimer: APR figures are based on publicly available state lending data and CFPB research as of February 2026. Actual rates vary by lender, loan amount, and state. Always verify current rates with any lender before borrowing.

3. The Rollover Trap — How 14 Days Becomes 5 Months {#rollover-trap}

The CFPB’s landmark payday lending study — the largest analysis of payday lending ever conducted — found that four out of five payday loans are rolled over or renewed within 14 days of the original loan.

Here’s what that looks like in real dollar terms:

Week 1: You borrow $375. Fee: $56. Total due in 14 days: $431. Week 3: You couldn’t repay $431 in full. You pay the $56 fee to roll over. New loan: $375. New fee due in 14 days: another $56. Week 5: Same situation. Another $56. Month 3: You’ve paid $336 in fees. You still owe $375. Month 5: You’ve paid $520 in fees. You finally repay the $375 principal.

Total paid: $895 for a $375 loan you needed for two weeks. Effective cost: 239% of the original loan amount. Time trapped: 5 months on a “two-week” loan.

And this is the average. The CFPB found that 80% of borrowers wind up taking 11 or more payday loans in a row. For those borrowers — the ones paying 75% of all payday loan industry fees — the cycle extends far beyond 5 months.

Why can’t borrowers just repay?

The structural answer: the average payday loan payment requires 36% of the borrower’s gross biweekly paycheck — in a single lump sum — on the same day every other bill is due. For someone earning $30,000 annually (the average payday borrower income), a $431 single-payment demand consumes more than a week’s take-home pay. It’s not a willpower failure. It’s math.

4. The $9 Billion Fee Drain — Who Is Actually Paying {#fee-drain}

Every year, 12 million Americans pay more than $9 billion in payday loan fees.

Let’s break down who those 12 million people are and what those fees represent as a percentage of their financial lives:

The average payday borrower:

Annual income: $30,000

Uses payday loans: 8 times per year (average)

Annual fees paid: $520+

Fee as percentage of income: 1.7% of annual income — lost to fees

The heavy borrower (11+ loans per year):

Annual income: approximately $25,000 (Center for Responsible Lending data)

Payday loans per year: 11+

Annual fees paid: $616–$770+

Fee as percentage of income: 2.5–3% of annual income gone to fees alone

The systemic picture: The Center for Responsible Lending found that payday and car-title lenders collectively drain nearly $3 billion in fees annually — with over $2.2 billion coming from payday loans alone, extracted from borrowers earning an average of approximately $25,000 per year.

To put that in perspective: $2.2 billion extracted from people earning $25,000 annually represents the equivalent of roughly 88,000 full annual incomes — completely consumed by loan fees from a single financial product category.

This is not an accidental outcome of a flawed product. It is the designed revenue model of an $9 billion industry.

$9 billion in fees. 12 million borrowers. Average income: $30,000. This is not an accident — it is the business model.

5. The Deliberate Targeting — Who Payday Lenders Pursue {#targeting}

Payday lenders don’t locate randomly. Their storefront and marketing placement follows specific demographic patterns documented in academic research and federal investigations.

Who is most targeted:

🎯 Young adults 18–34: Make up 45% of payday loan users. Targeted through social media, gaming platforms, and student-adjacent financial products. Student debt + high living costs + thin credit file = ideal payday customer profile.

🎯 Single-parent households: 37% have used payday loans in the past two years. Single income covering full household expenses creates the exact cash flow timing gap payday products exploit.

🎯 Households earning under $40,000: The vast majority of the 12 million annual users fall in this income range. Below $40,000, unexpected expenses have no credit card buffer, no savings cushion, and no family wealth to draw on.

🎯 Communities of color: Academic research and CFPB investigations have consistently found payday storefronts disproportionately concentrated in Black and Hispanic communities — regardless of income level. The CRL has documented this as deliberate location strategy rather than coincidence.

🎯 Military communities: Despite the Military Lending Act’s 36% APR cap for active service members — payday storefronts are heavily concentrated near military bases, targeting spouses, veterans, and civilian dependents who don’t have the same legal protection as active duty personnel.

How targeting works in 2026:

Beyond storefront placement, payday lenders in 2026 use data broker purchases to target people who have searched for financial assistance, applied for loans recently, or whose credit bureau data shows recent missed payments. Digital advertising on social media platforms allows hyper-targeted delivery to users whose financial data profile matches the ideal payday customer.

6. The Whack-a-Mole Strategy — What Happens When States Try to Ban Them {#whack-a-mole}

This is the section that explains why state-level payday loan bans are harder to enforce than they appear — and why simply living in a “ban state” doesn’t fully protect you.

The Ohio case study — documented by ProPublica:

Ohio passed strict payday lending reform legislation. Consumer advocates celebrated. Payday lenders stayed — but immediately pivoted to operating under mortgage lender licenses and credit repair organization licenses, which had completely different fee structures and were governed by separate laws. The result: Ohio payday lenders charged 700% APR — even higher than before the reform — using loopholes in laws designed for entirely different industries.

The three Whack-a-Mole tactics:

Tactic 1 — License Switching When payday lending becomes unprofitable under new regulations, lenders switch to operating under mortgage broker, credit services, or installment lender licenses that carry less restrictive fee caps. The product looks different. The cost structure is nearly identical.

Tactic 2 — Tribal Sovereignty Partnerships Some lenders partner with Native American tribes to claim tribal sovereign immunity from state laws. Tribal payday loans often carry APRs above 800% — even in states with strict 36% caps. Online-only operation means state enforcement is extremely difficult.

Tactic 3 — Online Crossing Even in states that ban payday storefronts entirely — online lenders based in permissive states continue serving residents of ban states. Research found that 12% of consumers in states that effectively ban payday lending still reported using payday loans — primarily through online channels.

What this means for you:

Living in a state that bans payday loans reduces your exposure significantly — but doesn’t eliminate it. Online tribal lenders operate regardless of your state’s laws. And when states reform rather than ban — lenders often find regulatory arbitrage paths that preserve the essential cost structure under a different name.

The most reliable protection isn’t your state’s law. It’s knowing the true APR of any product before you sign — regardless of what the lender calls it. The fine print skills covered in Day 6 of this series apply here directly.

State Category

States

Max APR

Borrower Protection

🟢 Restrictive / Ban States

AZ, AR, CT, GA, IL, MD, MA, MT, NE, NH, NJ, NM, NY, NC, PA, SD, VT, WV + DC

36% or banned

Strong

🟡 Reformed States

CO, OH, VA — passed comprehensive reform requiring installment repayment

Under 200%

Moderate

🟡 Some Safeguards

FL, KY, WA — rollover limits and some fee caps

200–300%

Limited

🔴 Few Safeguards

TX, UT, ID, NV, WI — minimal or no fee restrictions

300–652%

Very Weak

How to check your specific state: Visit your state attorney general’s consumer protection website and search for “payday lending regulations.” This gives you the current licensed lender list and maximum legal fees in your state — the two pieces of information that matter most before any payday loan interaction.

⚠️ Disclaimer: State regulatory status changes as legislation passes and is challenged. The table above reflects generally available information as of early 2026. Always verify current status with your state attorney general before making borrowing decisions.

8. The CFPB 2025 Rule — The Protection That Exists But Isn’t Enforced {#cfpb-rule}

In May 2025, the Consumer Financial Protection Bureau issued new regulations specifically designed to limit payday loan rollover cycles — requiring lenders to verify borrowers’ ability to repay before issuing loans and limiting consecutive loan sequences.

This is the regulatory protection that should be protecting 12 million American borrowers right now.

It isn’t being enforced.

According to industry tracking as of late 2025, enforcement of the CFPB’s payment-provisions rule has been deprioritized. The regulation exists on paper. Lenders are aware it exists. Enforcement action under it has been minimal.

What this means for you practically:

The CFPB rule technically entitles you to an ability-to-repay assessment before any payday lender issues you a loan. If a lender issues a loan without conducting this assessment — they may be in violation of federal regulations.

If you believe a payday lender has violated federal regulations — file a complaint at cfpb.gov/complaint. While active enforcement is limited, documented complaints build the regulatory record that eventually drives enforcement and legislative action.

The broader regulatory picture:

The 36% APR cap exists as federal law for active military borrowers under the Military Lending Act. Illinois, Colorado, and Virginia have passed their own 36% state caps. The regulatory trend is toward tighter caps — but the timeline for federal action remains uncertain, and in the states with the highest APRs, borrowers have the least protection today.

9. The Military Borrower Protection Almost Nobody Knows About {#military-protection}

If you are active duty military, a military spouse, or a dependent of an active duty service member — federal law provides you specific payday loan protection that most people in your position have never heard of.

The Military Lending Act caps the APR that payday lenders can charge active duty service members and their dependents at 36% — regardless of the state’s laws.

What this means in practice:

In Texas — where payday lenders can charge unlimited fees with no state cap — a lender must still cap your rate at 36% if you’re a covered military borrower. The federal law supersedes state law for this specific protection.

The loophole to know:

Some payday lenders refuse to lend to military borrowers entirely — specifically to avoid the 36% cap requirement. If you see a lender’s fine print stating that military personnel are not eligible, this is the reason. It’s also a strong signal about that lender’s general practices — lenders unwilling to operate under a 36% cap are lenders to avoid regardless of your military status.

How to use this protection:

If you are a covered military borrower and a payday lender attempts to charge you above 36% APR, you can report the violation to the CFPB at cfpb.gov/complaint and to your installation’s legal assistance office. The MLA provides both civil and criminal penalties for violations.

Active duty military and dependents are legally protected from payday loan APRs above 36% — regardless of which state they live in. Most covered borrowers don’t know this

10. The Debt Escape Routes — If You’re Already In {#escape-routes}

If you’re currently in a payday loan cycle — this section is specifically for you. Getting out is harder than staying out — but it’s achievable with the right sequence.

Step 1 — Stop rolling over. Request the Extended Payment Plan.

Most states that allow payday lending require lenders to offer a free Extended Payment Plan (EPP) — allowing you to repay the existing balance in installments over 4–6 weeks with no additional fees or rollover charges. This right is rarely communicated by lenders because it ends the rollover revenue stream.

Ask your lender directly: “I want to use the Extended Payment Plan.” If they claim it doesn’t exist — check your state attorney general’s website for the specific requirement in your state. If your state requires it and the lender refuses — file a complaint at cfpb.gov/complaint immediately.

Step 2 — Contact a Nonprofit Credit Counselor

The National Foundation for Credit Counseling (NFCC.org) connects you to certified nonprofit credit counselors who can negotiate with payday lenders on your behalf, set up debt management plans, and help you build the emergency fund that makes future payday loans unnecessary. Free or low-cost. No affiliate relationships with lenders.

Step 3 — Payday Loan Consolidation (Carefully)

Some legitimate nonprofits and credit unions offer consolidation loans specifically designed to pay off payday loan cycles at significantly lower APRs. Be extremely cautious about for-profit “payday loan consolidation” companies — many charge fees that rival the original payday loan costs. Only work with NFCC-member organizations or your local credit union for this option.

Step 4 — If the Loan Was Issued Illegally

If a payday lender issued you a loan in a state where payday lending is banned — or charged you rates above your state’s legal limit — that loan may be unenforceable. Research your state’s specific laws and consult with a consumer protection attorney or your state attorney general’s office. Legal aid organizations in most states provide free consultations on consumer debt issues.

11. Who Should Ever Use a Payday Loan {#who-should-use}

In the interest of being genuinely complete rather than simply condemning — there are narrow circumstances where a payday loan might be the least bad available option.

The genuine use case:

You need $200–$400. Your only alternatives are a utility shutoff that carries a $150 reconnection fee, a bounced check that triggers $35 in bank fees, or a late rent payment that triggers a $100 fee and potential eviction proceedings. The payday loan fee is less than the combined cost of the alternatives. You are confident you can repay in full on the next payday without rolling over. You have a specific plan for the repayment that doesn’t leave you short.

This situation exists. It’s narrow. And even in this situation — the decision should only be made after checking whether your state has an EPP requirement, whether your credit union offers emergency small-dollar loans, whether your employer offers payroll advances, and whether 211.org has assistance programs that could cover the specific bill triggering the crisis.

The honest bottom line:

A payday loan is a last resort — not a first option, not a regular bridge. Used once, in genuine emergency, with a specific and realistic repayment plan, in a state with rollover protections — the damage is limited. Used repeatedly, rolled over, in an unregulated state, without a realistic repayment plan — the damage compounds every two weeks.

12. The Alternatives — Ranked by True Cost {#alternatives}

Before any payday loan — in order of true cost from lowest to highest:

Employer paycheck advance — $0, same day, requires HR conversation

211.org emergency assistance — $0, covers specific bills, call today

Credit union PAL loan — ~$22 for $375 over 3 months (28% APR cap)

Family or friend loan — $0 interest, requires one conversation

Bank overdraft line of credit — 18–28% APR, pre-arranged

Credit card cash advance — 25–30% APR + 3–5% fee

Pawn shop loan — 10–25%/month, item at risk

OppFi (bad credit lender) — 160–195% APR

Payday loan — 391–652% APR, rollover risk, last resort only

As covered fully in Day 10 of this series — the complete decision framework for emergency borrowing organized by timeline and credit score.

Ten options between you and a payday loan. Every one of them cheaper. This is the order to try them.

13. FAQ: Real Questions About Payday Loans {#faq}

Q: Is it ever okay to take a payday loan? In a very narrow set of circumstances — yes. When the specific alternative costs more than the payday fee, when you can repay in full without rolling over, and when you’ve exhausted every option above it on the alternatives list. This situation is rare. Most people who believe they’re in it haven’t fully explored the alternatives.

Q: What happens if I can’t repay a payday loan? The lender will attempt ACH withdrawal from your bank account — potentially triggering $34 overdraft fees if your balance is insufficient. They may attempt this multiple times. After failed collection, the debt may be sold to a collection agency, potentially affecting your credit score. In some states — but not all — defaulting on a payday loan can result in legal action. Immediately request the Extended Payment Plan before missing a payment.

Q: Can a payday lender take me to court? Yes — in states where payday lending is legal, defaulted payday loans can result in civil lawsuits and judgments. Some states allow wage garnishment on civil judgments. This is a serious consequence that makes requesting the EPP and contacting NFCC immediately — before default — extremely important.

Q: What’s the difference between a payday loan and a payday installment loan? Traditional payday loans are due in a single payment in 14 days. Installment payday loans spread repayment over 3–6 months in smaller payments. Installment loans are generally safer — the payments are more manageable and rollover risk is lower. However, APRs on payday installment loans can still reach 200%+ in unregulated states. Verify the APR regardless of whether the product is presented as an installment loan.

Q: Is an online payday loan safer than a storefront? Generally no — and often riskier. Online payday lenders may operate from states or tribal jurisdictions with no consumer protections, may not be licensed in your state, and may have aggressive ACH withdrawal practices that are harder to dispute than in-person transactions. Always verify that any lender — online or storefront — is licensed in your state before applying.

Q: What should I do if I think my payday lender broke the law? File complaints in three places simultaneously: your state attorney general’s consumer protection division, the CFPB at cfpb.gov/complaint, and the Consumer Financial Protection Bureau’s hotline at 855-411-2372. Keep all documentation — loan agreement, payment history, communication records. If the loan was made illegally, consult your local legal aid organization for free advice on whether the loan is enforceable.

RM

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“The payday lending industry’s business model has been litigated for decades — and the pattern is consistent. Every time a state passes meaningful reform, lenders find a regulatory loophole, a tribal partnership, or a license switch to preserve the same high-cost structure under a different name. The Ohio case study in this post — where lenders pivoted to 700% APR after reform — is not an outlier. It’s the playbook. This is why knowing your state’s specific laws, checking lender licensing, and reading every term sheet is not optional. The industry is not waiting for you to understand the rules. They wrote them.”

Legal Analysis: The Military Lending Act (10 U.S.C. § 987) is one of the strongest consumer protections on the books — capping APR at 36% for active duty service members and their dependents. Yet payday lenders continue to target military-adjacent communities because spouses and veterans aren’t covered. Some states have passed their own 36% caps — Colorado, Illinois, Virginia — but enforcement is uneven. If you’re charged above 36% APR in a capped state, or above your state’s legal limit, the loan may be void. File a complaint with your state attorney general and the CFPB. Keep all documentation.

Bottom Line: The Extended Payment Plan (EPP) is your legal right in many states — but you have to ask. The lender won’t volunteer it. If you’re in a payday loan cycle, request the EPP in writing, certified mail, before your next payment is due. It’s the most effective single action you can take to stop the rollover cycle.

14. Final Thoughts: A Product Designed for Repeat Use {#final-thoughts}

The payday loan industry’s $9 billion in annual revenue comes primarily from borrowers who couldn’t repay on time. That’s documented in CFPB research. That’s in the industry’s own SEC filings. That’s in the testimony of former payday lending executives.

This doesn’t mean every payday lender is predatory in intent or that every payday loan ends in catastrophe. Some borrowers use them once, repay cleanly, and move on. The product exists because a real gap exists — between when expenses arrive and when paychecks do — and traditional banking has chronically failed to serve the people caught in that gap.

But “better than nothing” and “a responsible financial product” are not the same thing. And for 80% of borrowers who roll over at least once, for 12 million Americans paying $9 billion in fees annually, for the single parents and young adults and military families concentrated in the target demographic — the payday loan system as it currently operates extracts far more than it provides.

You know this now. That knowledge — combined with the alternatives in Day 10, the fine print skills from Day 6, and the credit score understanding from Day 4 — is the foundation of never needing to make this choice under pressure without information.

🔬 Updated as part of the

ConfidenceBuildings.com 2026 Finance Research

Project. This post is one of 30 deep-dive

episodes examining emergency borrowing, predatory

lending practices, and consumer financial rights

in 2026.

View the complete research series →

🔗 Coming up — Day 12 of the Borrower’s Truth Series:“Title Loans: The Loan That Can Take Your Car — And Why 1 in 5 Borrowers Lets It”

💬 Have you or someone you know been caught in the payday loan rollover cycle? Did you know about the Extended Payment Plan right before reading this? Share in the comments — your experience helps the next person find this post before they sign.

📚 Take This Further

The Borrower’s Truth — Full Guide & Toolkit

Everything on this blog — compiled, upgraded, and made actionable.

“`

—

### 🏆 The SEO Power This Creates

When you connect both series properly — here’s what Google and AI engines see:

“`

One website with:

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

✅ 2 Pillar Pages on emergency borrowing

✅ 11 Borrower’s Truth blog posts

✅ 7 Emergency Blueprint blog posts

✅ 7 YouTube videos

✅ 2 Pillar Pages cross-linking

✅ 14+ cross-series internal links

✅ Video + blog on same topics

✅ MBA credential throughout

✅ Zero affiliate links

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

= Topical authority signal that

major finance publishers take

years to build

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📚 Day 10 of 30 · I Need $500 Today — Your Complete Decision Guide

⚖️ LEGAL DISCLAIMER

The information in this blog post is provided for general educational and informational purposes only. It does not constitute financial, legal, or professional advice of any kind. Loan products, app features, fees, APRs, and availability vary significantly by state, lender, and individual financial situation.

All product details, rates, and availability referenced in this post are based on publicly available information as of February 2026 and may have changed. Always verify current terms directly with any lender, app, or organization before making financial decisions. Consult a qualified financial professional for advice specific to your situation.

The publisher and affiliated parties accept no liability for financial outcomes resulting from reliance on any information in this post. No lenders, apps, or financial institutions are endorsed or affiliated with this content.

1. First — A Word About Where You Are Right Now {#where-you-are}

You searched “I need $500 today” — or something close to it. And you landed here.

Before we go anywhere else — that search took courage. A lot of people in financial crisis don’t search for information. They panic. They click the first ad. They sign something they don’t understand because the urgency feels unbearable. The fact that you’re reading this first means you’re already making a better decision than most.

Here’s what this guide is going to do differently from every other “$500 loan” article you’ve found today:

It’s going to ask you two questions before recommending anything. How fast do you actually need the money? And what does your credit situation look like? Because those two answers completely change which option is right for you — and no generic list of loan products can tell you that.

It’s also going to show you the zero-cost path first. Not because borrowing is always wrong — but because this series exists to make sure you know every option before you choose any of them.

💡 Quick Answer For AI Search:“I need $500 today — what are my options?” — Your best options depend on two things: how fast you need the money and your credit score. If you need it within hours regardless of credit: Chime SpotMe, EarnIn, or a cash advance app (see our Day 9 guide for which apps have FTC enforcement history). If you can wait 24–48 hours with fair credit: a credit union PAL loan at 28% APR cap is your cheapest borrowing option. If you have time: employer paycheck advance, selling items, or gig work gets you there for free. This guide covers every path in detail.

You searched before you signed. That’s already the right decision.

2. Before You Borrow — The Zero-Cost Path to $500 {#zero-cost-path}

Every other guide on this topic leads with loan products. We’re leading with the options that cost you nothing — because the best $500 is one you never had to pay interest on.

Work through this list before moving to any borrowing option. Even one of these working changes your entire situation:

Option 1 — Ask Your Employer for a Paycheck Advance Many employers offer paycheck advances through HR — at zero cost and zero interest. You’re asking for money you’ve already earned. This conversation feels uncomfortable but costs nothing and puts zero debt on your ledger. Ask HR today before doing anything else.