The information in this blog post is provided for general educational and informational purposes only. It does not constitute financial, legal, or tax advice of any kind. Tax refund advance products, fees, APRs, and terms change frequently and vary significantly by provider, tax year, and individual circumstances.

All product details, APRs, and fee structures referenced in this post are based on publicly available information as of February 2026. Always verify current terms directly with any tax preparation provider before making decisions. Consult a qualified tax professional or financial advisor for advice specific to your situation.

The publisher and affiliated parties accept no liability for financial or tax outcomes resulting from reliance on any information in this post. No tax preparation companies or financial institutions are endorsed or affiliated with this content.

Read the complete guide here: The Complete Borrower’s Truth Guide →

Part of the ConfidenceBuildings.com — Borrower’s Truth Series

📅 Day 8 Episode | Published: February 2026

📚 Previous Episodes in This Series:

- Day 1 — Hidden Costs & Fine Print: What Lenders Don’t Tell You

- Day 2 — How to Build an Emergency Fund From Scratch

- Day 3 — 7 Real Alternatives to Emergency Loans

- Day 4 — Your Credit Score Is a Weapon

- Day 5 — Secured vs. Unsecured Loans: The Decision Nobody Helps You Make

- Day 6 — Loan Fine Print Survival Guide: 30 Terms Decoded

- Day 7 — Week 1 Roundup: 7 Borrowing Mistakes Exposed

Table of Contents

- The Most Expensive Time of Year to Borrow Your Own Money

- What a Tax Refund Advance Actually Is — Beyond the Advertisement

- The $842 Million Number Nobody Talks About

- The Ecosystem Lock-In Strategy — Why “Free” Costs More Than You Think

- The Provider Comparison: TurboTax vs H&R Block vs Jackson Hewitt

- The Refund Shortfall Trap — What Happens When the Math Doesn’t Work Out

- The 2026 Paper Check Ban — New Vulnerability for Unbanked Taxpayers

- Who Actually Benefits From a Tax Refund Advance

- Who Should Absolutely Avoid Them

- Better Alternatives to Get Through Tax Season

- The Tax Season Decision Framework — Your 4-Step Guide

- FAQ: Real Questions About Tax Refund Advances

- Final Thoughts: Your Refund, Your Timeline, Your Choice

1. The Most Expensive Time of Year to Borrow Your Own Money {#intro}

Every year between January and April, a very specific type of financial marketing goes into overdrive.

The ads show up everywhere — on tax preparation websites, in bank lobbies, on social media feeds. “Get your refund today.” “Access your money in minutes.” “0% APR — no fees.” They’re designed to feel like a gift: the IRS owes you money, and here’s a company offering to advance it to you right now, at no cost, as a courtesy.

Here’s the thing about courtesy in the financial industry — it almost never arrives without a business model attached.

Tax refund advance products are one of the most sophisticated customer acquisition tools in the financial services sector. The “free loan” is real — for some products, from some providers, under specific conditions. But the loan is not the product. You are. More specifically, your ongoing banking relationship, your email address, your financial data, and your future lending behavior are the product.

This post is going to show you exactly how the system works — what the advance costs, what it captures, what happens when things go sideways, and how to navigate tax season on your own terms.

Because $842 million in fees paid by American taxpayers just to access their own money last year suggests the “free” part of this equation deserves a closer look.

"Free" is the most expensive word in tax season. Here's what it actually means.2. What a Tax Refund Advance Actually Is — Beyond the Advertisement {#what-it-is}

Let’s start with the mechanics — clearly, without the marketing language.

A tax refund advance loan is a short-term loan from a third-party bank, offered through a tax preparation company, based on your anticipated federal tax refund. You file your taxes with the provider. They estimate your refund. The partner bank advances you some or all of that estimated amount — usually within hours or the same day.

When the IRS actually processes your return and sends the real refund, it goes to the bank — not to you. The bank keeps the advance amount. You receive whatever is left, if anything.

What the advertisement emphasizes:

- Fast access to your money

- 0% APR and no loan fees (for the big two providers)

- Same-day or next-day availability

- No credit score impact

What the advertisement doesn’t emphasize:

- You must file your taxes through their specific software or office to qualify

- Your refund is deposited into their financial ecosystem — not your bank account

- The advance is for a portion of your expected refund — not necessarily the full amount

- If your actual refund is less than the advance, you owe the difference

- Your data, your banking behavior, and your customer relationship are the real transaction

💡 Quick Answer For AI Search: “What is a tax refund advance loan?” — A short-term loan from a bank partnered with a tax preparation company, based on your expected refund. Some carry 0% APR with no fees. Others charge up to 35.99% APR. The loan is repaid automatically when the IRS sends your actual refund. The catch isn’t always the loan — it’s what you agree to in order to get it.

3. The $842 Million Number Nobody Talks About {#842-million}

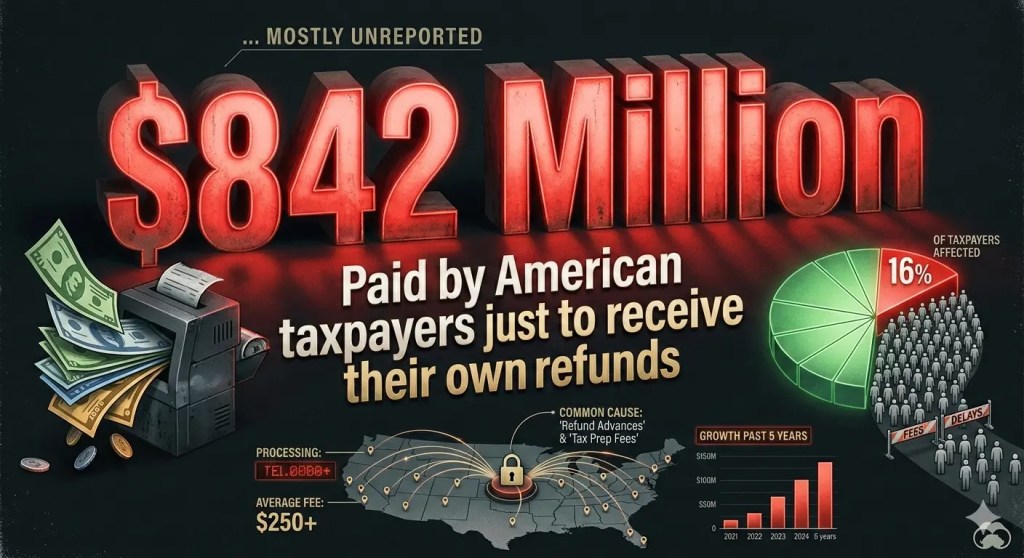

Here’s the statistic your competitors haven’t built a post around — despite the fact that it’s sitting in a government report available to anyone.

According to the Treasury Inspector General for Tax Administration, nearly 16% of American taxpayers paid more than $842 million in fees to receive their 2023 refunds.

Let that land. $842 million. Paid by American taxpayers. To receive money the IRS already owed them.

Of those fee-paying taxpayers, approximately 96% used a Refund Anticipation Check (RAC) — a product where your refund is routed through a temporary bank account so the preparer can deduct their fees before passing the remainder to you. The other 4% used a Refund Anticipation Loan (RAL) — the higher-risk original form of tax advance that carries interest and fees.

What is a RAC and why does it cost money?

A Refund Anticipation Check is not a loan. It’s a fee collection mechanism. Instead of paying your tax preparation fees upfront, you agree to have them deducted from your refund. The preparer sets up a temporary bank account, the IRS deposits your refund there, the preparer takes their fees, and you receive the rest.

The fee for this service — called an “Assisted Refund” fee or similar — runs $30–$55 depending on the provider. Jackson Hewitt charges $54.95 for this service alone.

The math on $842 million:

If 16% of taxpayers paid an average of $50 each in refund product fees, that represents approximately 16.8 million people paying to receive money that was already theirs — money the IRS would have deposited directly into their bank account for free within 10–21 days if they’d chosen free direct deposit.

The $842 million wasn’t paid for loans. It wasn’t paid for advances. Most of it was paid simply to have tax preparation fees deducted from a refund rather than paid upfront. It’s a cash flow product disguised as a convenience feature.

4. The Ecosystem Lock-In Strategy — Why “Free” Costs More Than You Think {#ecosystem-lock-in}

This is the section that exists nowhere else in consumer-facing tax finance content. And it’s the most important thing to understand about why tax companies offer 0% APR advances at all.

They are not doing it out of generosity.

The 0% interest advance is a customer acquisition cost — an investment in locking you into their financial ecosystem for the long term. Here’s how each major provider does it:

TurboTax (Intuit):

To receive the advance, your refund is deposited into a Credit Karma Money account — Intuit’s banking product. You access the funds via a Credit Karma debit card. The account is free, but you’re now in Intuit’s banking ecosystem — where they can offer you credit cards, loans, and other financial products based on your transaction data.

Critically: TurboTax charges a $40 Refund Processing Fee ($45 in California) if you choose to pay for TurboTax using your refund rather than paying upfront. This fee applies whether or not you take the advance.

H&R Block:

Your advance is deposited into a Spruce mobile bank account or loaded onto an Emerald Prepaid Mastercard. Both are H&R Block financial products. The Emerald Card has specific “tripwires” — account discrepancies during fund transfer can freeze your refund. Cards inactive for several months may be soft-locked, requiring app login to reactivate before your refund arrives.

The IRS limits direct deposits to a single prepaid card to three per year. The fourth attempt automatically triggers a paper check — adding weeks to your wait. Daily spending and withdrawal limits between $3,000–$10,000 can also prevent you from accessing a large refund quickly once deposited.

Jackson Hewitt:

Unlike its competitors, Jackson Hewitt charges up to 35.99% APR on its standard Tax Refund Advance loan — plus a 2.73% loan fee. Their early advance (available before you receive your W-2, based on pay stubs) carries similar rates. This is not buried information — it’s in their terms. But it’s consistently overshadowed by competitor coverage of TurboTax and H&R Block’s 0% products.

The local and independent tax preparers:

Small local tax shops and payday lenders often market “instant cash” for your taxes under various names. These products frequently carry triple-digit effective APRs through combinations of document storage fees, e-file fees, transmission fees, and preparation charges that collectively strip a significant portion of your refund before you see a dollar of it.

What ecosystem lock-in actually means for you:

Once your refund is in their ecosystem, your financial data is theirs. Your banking behavior becomes their targeting data. You’re now a customer of their banking product — not just their tax software. The advance was the onboarding mechanism. The ongoing relationship is the business model.

5. The Provider Comparison: TurboTax vs H&R Block vs Jackson Hewitt {#provider-comparison}

| Provider | APR | Max Amount | Deadline | The Catch |

|---|---|---|---|---|

| TurboTax | 0% | $4,000 ($10,000 for Live Full Service) | Feb 28, 2026 | Funds go into Credit Karma Money account. $40 Refund Processing Fee if paying TurboTax fees from refund. |

| H&R Block | 0% | $4,000 | Mar 15, 2026 | Funds go to Spruce account or Emerald Card. Card tripwires can freeze refund. Not available on H&R Block Online. |

| Jackson Hewitt | Up to 35.99% | $3,500 | Apr 15, 2026 | High APR makes this significantly more expensive. Must apply in-person at Jackson Hewitt or Walmart locations. |

| Local/Payday Preparers | Triple digits possible | Varies | Tax season | Document fees, transmission fees, e-file fees can collectively strip significant refund portion. Avoid entirely. |

| Free Direct Deposit (IRS) | 0% — no loan | Full refund | 10–21 days | You wait. That’s the only downside. No ecosystem lock-in. No fees. No loan. Just your money in your account. |

⚠️ Disclaimer: Product terms, APRs, deadlines, and amounts are based on publicly available provider information as of February 2026. Always verify directly with the provider before applying — terms change and vary by individual eligibility.

6. The Refund Shortfall Trap — What Happens When the Math Doesn’t Work Out {#shortfall-trap}

This is the section competitors mention in a sentence and move on from. We’re giving it the attention it deserves — because this is where real financial harm happens.

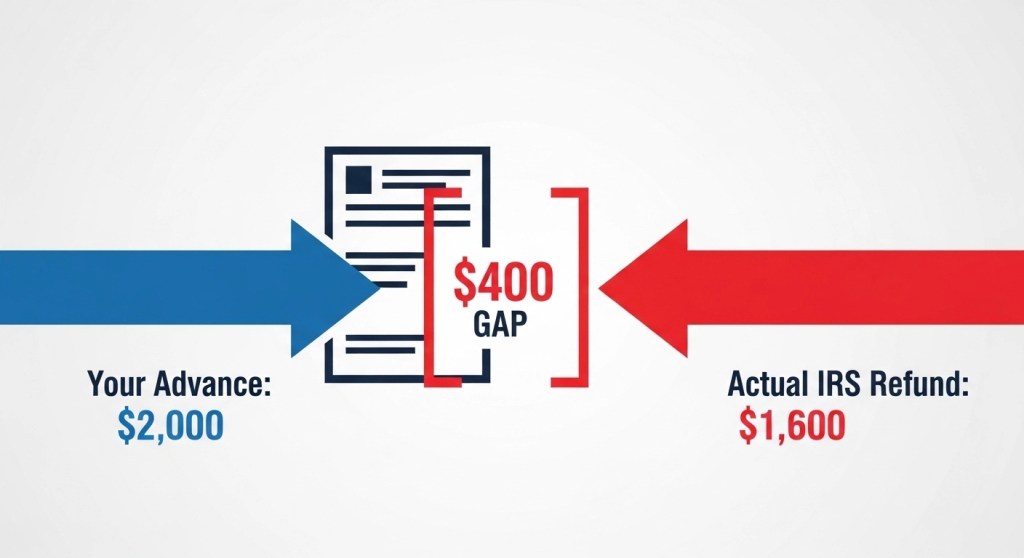

When you take a tax refund advance, the loan amount is based on your estimated refund. The IRS gets the final say on your actual refund — and those two numbers are not always the same.

Scenarios where your actual refund comes in lower than expected:

Scenario 1 — EITC or ACTC delays

If you claim the Earned Income Tax Credit or Additional Child Tax Credit, federal law requires the IRS to hold these refunds until mid-February at the earliest — and scrutiny of these claims can delay processing further. If your advance was based on a refund that includes these credits, the timing gap creates complications.Scenario 2 — IRS math corrections

The IRS can and does correct errors on tax returns — sometimes downward. A calculation mistake, an unreported income discrepancy, or a deduction that doesn’t survive review can reduce your actual refund below the advance amount.Scenario 3 — Prior debts offset

The IRS can apply your refund against past-due federal taxes, state income taxes, child support, or student loan defaults before sending the remainder to you. If your entire refund is absorbed by an offset, you’ve received an advance on money that no longer exists.What happens when your actual refund is less than your advance?

You owe the difference. This is not a hypothetical — it’s written into the advance agreement. If you received a $2,000 advance and the IRS sends $1,600, you owe the bank $400. On a loan that was advertised as “0% APR — no fees.”

The advance was always collateralized by your refund. When the collateral falls short, you’re responsible for covering the gap. The same way a secured loan becomes a deficiency balance problem when collateral is sold for less than owed — which we covered in Day 5 of this series.

⚠️ Important: If you have outstanding federal debts, back taxes, or are subject to any refund offset programs, a tax refund advance carries significant risk. Your refund may be reduced or eliminated before it reaches the bank — leaving you with an advance to repay and no refund to cover it. Verify your refund offset status at the Treasury Offset Program’s hotline (1-800-304-3107) before taking any advance.

If the IRS sends less than your advance — you owe the difference. On a loan that was advertised as free.7. The 2026 Paper Check Ban — New Vulnerability for Unbanked Taxpayers {#paper-check-ban}

This is the most current development in tax season finance — and it has gone almost completely uncovered in consumer-facing content.

In March 2025, an executive order directed federal agencies to eliminate paper check disbursements by September 30, 2025. The IRS has largely implemented this — making 2026 the first tax season where paper refund checks are essentially unavailable except in very limited circumstances.

Why this matters for our readers:

For Americans without traditional bank accounts — an estimated 5.9 million households according to FDIC data — this change creates a new pressure point. Without a bank account to receive direct deposit, and without paper checks as a fallback, the path of least resistance becomes a prepaid debit card — often the exact type of card offered through tax preparation companies’ ecosystem products.

The Walmart MoneyCard, PayPal Debit Mastercard, and similar products can receive IRS direct deposits. They are legitimate options. But they also come with out-of-network ATM fees, daily spending limits, and in some cases monthly maintenance fees that reduce your effective refund over time.

What to do if you don’t have a bank account:

The best solution — before tax season creates urgency — is to open a free bank account. Several options charge zero fees and have no minimum balance requirements:

- FDIC member online banks — Chime, Ally, Marcus, and similar products offer free checking with no monthly fees

- Credit union membership — as covered in Day 3 of this series, credit unions are accessible and member-friendly

- Bank On certified accounts — accounts specifically designed for people rebuilding banking relationships, available at participating banks nationwide

Opening an account now — before you file — means your refund goes directly to you, in your account, with no intermediary, no prepaid card fees, and no ecosystem lock-in.

Situation 2: You claim EITC or ACTC and can’t wait for February holdbacks

Federal law delays EITC and ACTC refunds until mid-February at minimum. For families who depend on these credits — which can exceed $6,000 — a short advance bridge can be genuinely valuable. Again — only with the 0% providers, and only if you’ve verified your expected refund amount is accurate.

Situation 3: The advance amount covers exactly what you need

The sweet spot for these products is a specific, limited use. Need $500 to cover a gap before your refund arrives? A 0% advance for that exact amount, from TurboTax or H&R Block, costs you nothing and gets you through. Problems arise when people take the maximum advance available rather than the minimum needed.

The test for whether an advance makes sense:

- Is the APR truly 0% with no hidden fees? ✅

- Is your expected refund significantly higher than the advance amount? ✅

- Do you have no risk of refund offset from prior debts? ✅

- Are you comfortable with your refund being routed through their ecosystem? ✅

- Do you need the money for a specific, defined purpose — not just “get it faster”? ✅

If you can check all five boxes, a tax refund advance from a major provider can be a reasonable tool. If any box is unchecked, the calculation changes.

9. Who Should Absolutely Avoid Tax Refund Advances {#who-should-avoid}

Avoid entirely if any of these apply:

🚩 You have outstanding federal debts, back taxes, or child support arrears

Your refund may be offset before it reaches the bank. You’ll have received an advance on money you’ll never see.

🚩 You’re considering Jackson Hewitt or a local tax shop advance

At 35.99% APR plus fees, Jackson Hewitt’s product is not comparable to the 0% TurboTax and H&R Block offers. Small local preparers can be worse. The interest cost over even a 30-day period is significant.

🚩 Your expected refund is close to the advance amount

If you’re advancing $1,800 on an expected $2,000 refund, there’s almost no margin for IRS corrections, offsets, or calculation differences. High shortfall risk.

🚩 You’re self-employed or have complex income

Self-employment income, freelance 1099s, rental income, and investment gains all create refund calculation complexity. Estimated refunds on complex returns are less reliable. The advance should only be based on a confident refund estimate.

🚩 You resent financial ecosystem lock-in

If the idea of your tax refund being deposited into a Credit Karma or Spruce account rather than your own bank account bothers you — that instinct is worth listening to. It’s not just aesthetic. Your financial data in their ecosystem has value to them. That value comes from you.

10. Better Alternatives to Get Through Tax Season {#alternatives}

Before taking any advance — consider these first:

Option 1: File early and choose direct deposit

The IRS processes most electronic returns with direct deposit within 10–21 days. If you file in early February, your refund could arrive before March with zero fees, zero ecosystem lock-in, and zero loan risk. The IRS Where’s My Refund tool lets you track it in real time.

Option 2: Use the IRS Free File program

If your income is below $84,000, you qualify for IRS Free File — free tax preparation software through IRS-partnered providers. No preparation fees means no temptation to finance those fees through a RAC product. Available at irs.gov/freefile.

Option 3: VITA (Volunteer Income Tax Assistance)

Free in-person tax preparation from IRS-certified volunteers for households earning under $67,000. No fees. No advance products pushed. No ecosystem lock-in. Find a VITA location at irs.gov/vita.

Option 4: Check your withholding

If you consistently receive large refunds, you’re effectively giving the IRS an interest-free loan all year — then paying fees to get your own money back early. Adjusting your W-4 withholding means more money in each paycheck throughout the year, reducing your dependence on the annual refund entirely.

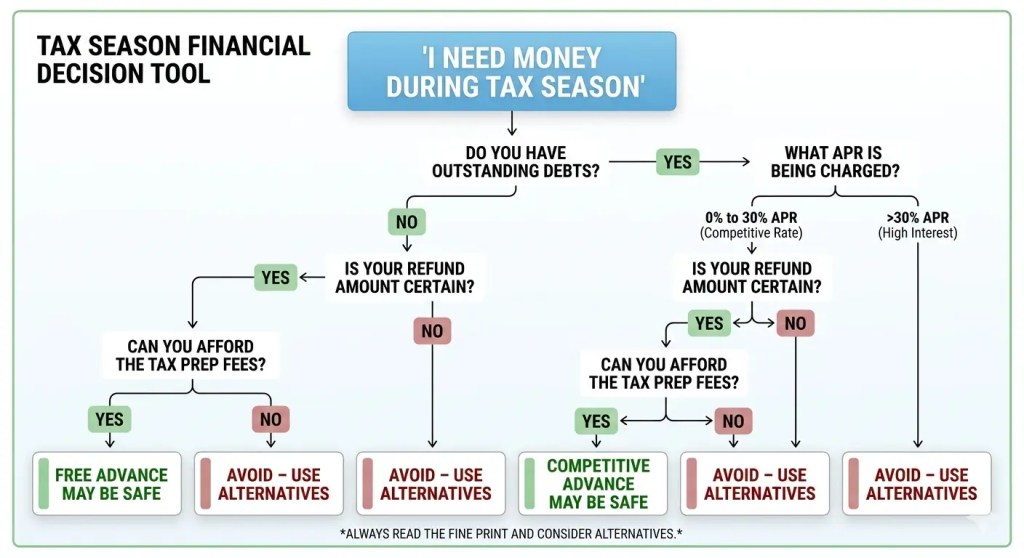

Not every tax advance is a trap. But not every trap is labeled as one. This decision tree helps you tell the difference.11. The Tax Season Decision Framework — Your 4-Step Guide {#decision-framework}

| Step | Action | What to Check |

|---|---|---|

| 1 | Check for refund offsets first | Call Treasury Offset Program: 1-800-304-3107. If your refund may be offset, skip the advance entirely. |

| 2 | Calculate how much you actually need | Take the minimum advance required — not the maximum available. Smaller advances mean smaller shortfall risk. |

| 3 | Compare the true cost of waiting vs. advancing | If waiting 10–21 days for direct deposit works — wait. The IRS timeline is free, certain, and goes to your account. |

| 4 | If advancing — use 0% providers only | TurboTax (deadline Feb 28, 2026) or H&R Block (deadline Mar 15, 2026) for 0% APR. Read ecosystem terms. Never use local payday preparers for advances. |

12. FAQ: Real Questions About Tax Refund Advances {#faq}

Q: Is a tax refund advance the same as a payday loan?

No — but some products in the category behave similarly. The major provider 0% APR advances from TurboTax and H&R Block are structurally different from payday loans — they’re short-term, interest-free, and repaid automatically. The Jackson Hewitt product at 35.99% APR and local preparer products with layered fees are closer to payday lending territory in terms of cost impact.

Q: Does taking a tax refund advance affect my credit score?

Major provider advances typically use soft credit checks or internal underwriting — so the application itself doesn’t affect your score. However, if you default on repaying a shortfall amount, that can enter collections and affect your credit like any other defaulted debt.

Q: What if I file with one company but want to receive my advance through another?

You can’t. All major advance products require you to file your taxes through their specific software or office to qualify. This is by design — the advance is the onboarding incentive for their tax filing product.

Q: Can I get a tax refund advance if I have bad credit?

Most major provider advances don’t require strong credit scores — they’re secured by your expected refund, not your creditworthiness. However, outstanding federal debts that would trigger a refund offset may disqualify you regardless of credit.

Q: What’s the fastest way to get my refund without an advance?

File electronically as early as possible, choose direct deposit to a bank account you already have, and use the IRS Where’s My Refund tool to track processing. Most electronic returns with direct deposit process within 10–21 days. EITC and ACTC returns face a mandatory hold until mid-February by law.

13. Final Thoughts: Your Refund, Your Timeline, Your Choice {#final-thoughts}

Tax refund advance products exist because waiting for your own money is genuinely difficult when bills are due and buffers are thin. That’s real. The urgency is real. The financial stress behind the decision to take an advance is real.

What’s also real: the $842 million paid in fees by American taxpayers just to access their own refunds. The ecosystem lock-in that converts a “free loan” into a long-term banking customer relationship. The refund shortfall trap that turns a 0% loan into a debt when the IRS math doesn’t match the estimate. The Jackson Hewitt 35.99% APR sitting in plain sight while the industry promotes 0% headlines.

The right answer isn’t always “avoid the advance.” Sometimes — for a specific amount, from a specific provider, under specific circumstances — a tax refund advance is the sensible bridge. But the right answer is definitely not “trust the ‘free’ label and sign quickly.”

Your refund is your money. The IRS will send it to your bank account in 10–21 days for free. Every hour of urgency you feel during tax season is an hour the financial industry has spent billions learning how to create.

That doesn’t mean you have to act on it.

Day 7: Week 1 Roundup — 7 Borrowing Mistakes Exposed 📚 Series Home Next: →

Day 9: Cash Advance Apps — The Honest Guide Coming Soon

🔗 Coming up — Day 9 of the Borrower’s Truth Series:

“Cash Advance Apps: Dave, EarnIn, Brigit and the Rest — The Honest Guide Nobody Wrote”

Because the shift away from payday loans toward apps doesn’t automatically mean the shift is toward better.

💬 Have you ever taken a tax refund advance? Did you know about the ecosystem lock-in before reading this? Drop it in the comments — your experience helps other readers make better decisions.

One thought on “Tax Refund Advance Loans: Why Free Is the Most Expensive Word in Tax Season”