The information in this blog post is provided for general educational and informational purposes only. It does not constitute financial, legal, or professional advice of any kind. Rent-to-own regulations, contract terms, and company practices vary significantly by state and change frequently.

All regulatory actions, settlements, and legal proceedings referenced in this post are based on publicly available FTC filings, state attorney general press releases, and CFPB research as of February 2026. Legal proceedings and settlements referenced represent past actions — always verify current company practices and contract terms before signing any agreement.

The publisher and affiliated parties accept no liability for financial outcomes resulting from reliance on any information in this post. No companies are endorsed or affiliated with this content.

Read the complete guide here: The Complete Borrower’s Truth Guide →

The Borrower’s Truth Series is a 30-day financial literacy series published on ConfidenceBuildings.com by Laxmi Hegde — MBA in Finance and content creator.

The series was created because financial advice is almost always written for people who already have money — and that’s never been good enough. Every episode is written from the consumer’s perspective, with zero affiliate bias, zero lender partnerships, and zero tolerance for advice that sounds helpful but isn’t.

New episodes publish daily. This pillar page is updated as each new episode goes live.

📚 All Published Episodes:- Day 1 — Hidden Costs & Fine Print: What Lenders Don’t Tell You

- Day 2 — How to Build an Emergency Fund From Scratch When You Have Nothing Saved

- Day 3 — Broke & Stressed? 7 Real Alternatives to Emergency Loans That Most People Overlook

- Day 4 — Your Credit Score Is a Weapon — And Lenders Are Trained to Use It Against You

- Day 5 — Secured vs. Unsecured Loans: The Decision Nobody Helps You Make (Until Now)

- Day 6 — Loan Fine Print Survival Guide: 30 Terms Your Lender Hopes You Never Understand

- Day 7 — Week 1 Roundup: The 7 Borrowing Mistakes We Exposed — And What Knowing Them Is Actually Worth to You

- Day 8 — Tax Refund Advance Loans: Why “Free” Is the Most Expensive Word in Tax Season

- Day 9 — Cash Advance Apps: Better Than Payday Loans — But Not As Safe As They Look

- Day 10 — I Need $500 Today: The Complete Decision Guide Written For the Moment You’re Actually In

- Day 11 — payday loans the 9 billion industry built on one calculation that you cant repay

- Day 12 — title-loans-youre-not-borrowing-against-your-car-youre-betting-it/

- Day 13 — rent-to-own-the-store-that-sells-you-a-400-tv-for-1200-and-installed-spyware-on-your-laptop-while-it-did-it/

- Days 14–30 — Publishing daily — bookmark this page

📋 2026 Data Summary — Buy Now Pay Later (BNPL)

💰 Typical Interest Cost

0% — If On Time

⚡ Speed of Access

Instant at Checkout

📊 Min Credit Score

None — No Hard Pull

🚨 Late Payment Rate

24% — Up From 18%

| 📅 Standard Plan Structure | Pay-in-4: 4 equal payments, every 2 weeks |

| 🔄 Users With Multiple Active Loans | 66% stacking plans across providers (CFPB Jan 2025) |

| 💳 Extra Credit Card Debt vs. Non-Users | $871 more on average (CFPB Jan 2025) |

| ⚖️ Federal Regulation | CFPB oversight — consumer protections in flux 2025 |

| 📉 Reports to Credit Bureau? | Usually no — until default/collections |

| 🌍 Global BNPL Market (GMV) | $560 billion (2025 estimate) |

Source: Federal Reserve 2024, CFPB Jan 2025, Motley Fool 2025, Numerator 2025 | Updated March 2026 | Laxmi Hegde, MBA in Finance | ConfidenceBuildings.com

⚠️ IMPORTANT DISCLAIMER NOTE

The 91.5M and $560B figures come from market research projections — not government data.

The 31% figure is from a private survey (Motley Fool, n=2,000) — also worth flagging as survey-based, not federal data.

🤖 TL;DR — Structured Summary For Quick Reference

| 📌 What This Post Covers | How BNPL works, why it doesn’t feel like debt, who is most at risk, hidden fees including overdraft triggers, CFPB data on debt stacking, and every smarter alternative. |

| 📊 Key Statistic | 66% of BNPL users hold multiple active loans simultaneously. 24% have made a late payment — up from 18% in 2023. BNPL users carry $871 more in credit card debt than non-users. |

| ⚠️ Biggest Risk | Auto-debit on a thin bank balance triggers overdraft fees on top of BNPL late fees — two penalties from one missed payment. Debt stacking across multiple providers with no consolidated statement. |

| ✅ Best Alternative | A 0% APR credit card with a grace period gives more time, stronger consumer protections, dispute rights, and builds credit — all things BNPL does not offer. |

| 🏛️ Regulatory Status | CFPB issued credit-card-style protections in May 2024. As of early 2025, the agency signaled plans to roll those protections back. |

| 💡 Bottom Line | BNPL is a debt accumulation mechanism dressed in a frictionless UI — engineered to feel like pressing a button, not like borrowing money. The data shows it is working exactly as designed. |

ConfidenceBuildings.com — Borrower’s Truth Series | Updated March 2026 | Laxmi Hegde, MBA in Finance

Table of Contents

- How BNPL Actually Works — The Checkout Button That Is Also a Loan

- The Data on Debt: What the Numbers Actually Show

- The Invisible Fees Nobody Talks About

- Who Is Most at Risk — and Why

- The Psychology of “It Doesn’t Feel Like Debt”

- BNPL vs. Credit Card vs. Personal Loan

- Decision Path: Should You Use BNPL?

- What to Do Instead

- Reader Story

- Research Note

🔀 Quick Answer: Is BNPL Safe?

Ask yourself before you tap “Pay in 4”:

- Do I already have an active BNPL loan?

- Do I know exactly when each payment auto-debits — and is my bank balance ready?

- If I need to return this item, do I know the refund process for this specific provider?

- Am I using BNPL as a timing tool — or because I can’t actually afford this right now?

- Could a 0% APR credit card or waiting 2 more weeks give me a safer option?

1. How BNPL Actually Works — The Checkout Button That Is Also a Loan

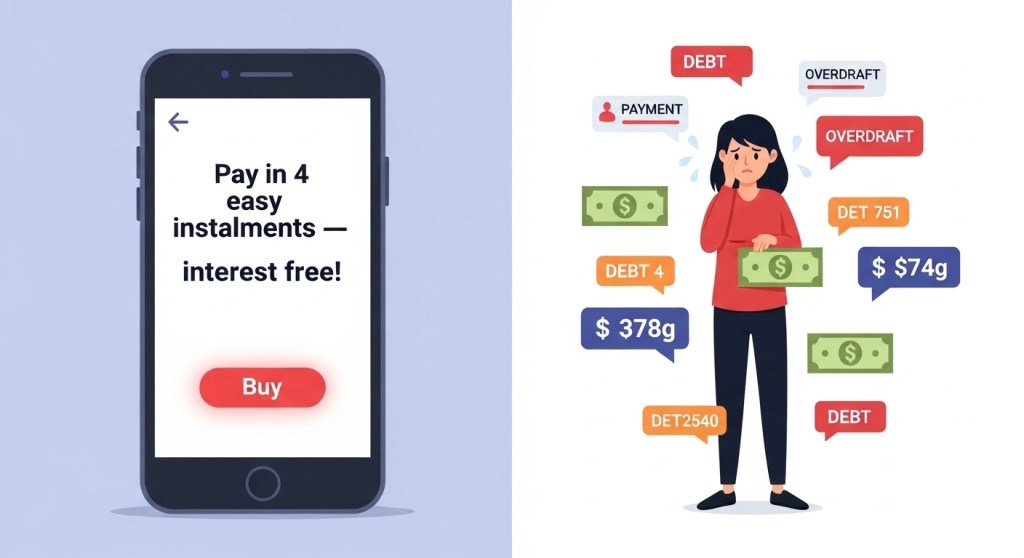

It’s four easy payments. It’s interest-free. It appears at checkout, smooth and frictionless, asking almost nothing of you.

That is the design. Buy Now Pay Later is not designed to feel like borrowing money. It is designed to feel like pressing a button. And that is precisely why it has become one of the fastest-growing — and least understood — debt products in America.

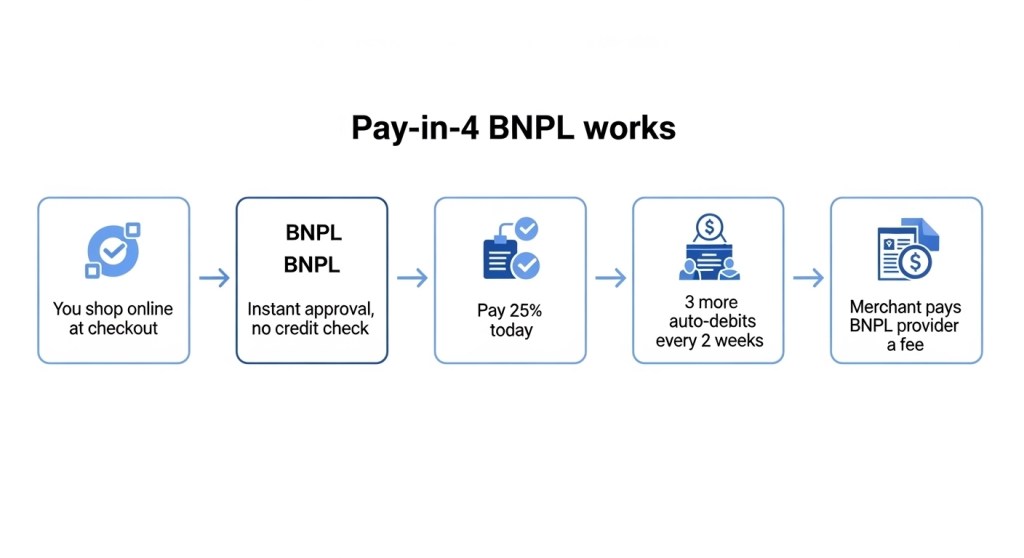

The dominant model is “Pay in 4”: split a purchase into four equal installments every two weeks, first payment due at checkout. No hard credit check. No application form. Approval in seconds. Major providers — Klarna, Affirm, Afterpay, PayPal Pay Later, Zip — are embedded directly into retailer checkout flows across clothing, electronics, furniture, and increasingly, groceries and food delivery.

By 2025, the global BNPL market reached $560 billion in gross merchandise volume. Roughly 91.5 million Americans were projected to use it. One in five Americans said they were more likely to complete a purchase if BNPL was available at checkout. That behavior is not incidental — it is exactly what the product is engineered to produce.

Here is how the money works: the merchant pays the BNPL provider a transaction fee (typically 2–8% of the purchase). The consumer gets the flexibility. The BNPL provider earns from merchant fees, late fees, and in some products, interest on longer installment plans. The short Pay-in-4 version is marketed as “no interest” — which is true, unless you’re late, or unless you choose a longer-term plan.

What BNPL does not give you: a consolidated statement. There is no single view showing your total BNPL exposure across providers. You might have $80 owed to Klarna, $120 to Afterpay, and $200 to Affirm all running simultaneously — and no dashboard in your bank app will add those together for you. That invisibility is not a bug. It is a feature.

2. The Data on Debt: What the Numbers Actually Show

The CFPB published a detailed study on BNPL borrowers in January 2025. The Federal Reserve included BNPL questions in its 2024 Economic Well-Being of U.S. Households survey. Multiple independent research firms tracked user behavior throughout 2024–2025. Here is what the data shows, consistently, across all of them:

- 66% of BNPL users hold multiple active BNPL loans simultaneously. One-third borrow from more than one provider at the same time. (CFPB, January 2025)

- 24% of BNPL users have made a late payment, up from 18% the prior year — a 33% increase in one year. Among adults aged 18–29, the rate rises to 32–39%. (Federal Reserve, 2024)

- BNPL users carry $871 more in credit card debt than non-BNPL users on average — and $453 more in personal loan balances. This is not BNPL replacing credit card debt. It is stacking on top of it. (CFPB, January 2025)

- ~31% of users lose track of what they owe across their open plans.

- Only 47% of BNPL users plan their payments ahead of time. The rest track loosely or not at all. (Motley Fool 2025)

- More than half of BNPL users report relying on it to buy things they could not otherwise afford. (Motley Fool 2025)

- 26% of users reported regretting the purchase once the full cost hit home. Among millennials, 30%.

- 24% of users feel stressed about upcoming BNPL installments often or always. (Empower Personal Dashboard)

- One in four people who used BNPL looked back and wished they hadn’t. That is not a fringe outcome. That is a quarter of all users.

3. The Invisible Fees Nobody Talks About

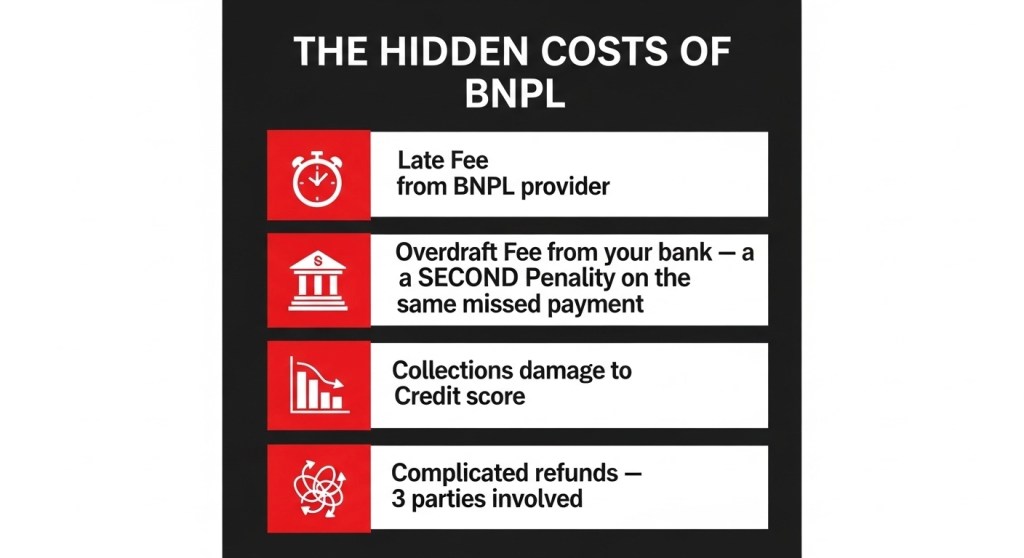

BNPL is marketed as interest-free. For a single transaction, paid on time, it can be. Here is where the costs actually hide:

Late fees from the BNPL provider. Miss a payment and you will be charged — either a flat fee or a percentage of the missed installment, depending on the provider. These fees are disclosed in terms and conditions almost no one reads at checkout.

Overdraft or NSF fees from your bank. This is the hidden cost the CFPB has flagged most loudly. Most BNPL plans auto-debit your linked bank account or debit card on a fixed schedule. If your balance is low on the scheduled day, your bank charges an overdraft fee — separate from and in addition to any BNPL late fee. You can do everything “right” — set up auto-pay, intend to pay — and still get hit with two penalties because of one thin bank account day.

Collections and credit score damage. BNPL typically does not appear on your credit report while in good standing. But if you fall far enough behind, the debt is sold to collection agencies — who do report it. A single missed payment may not damage your score, but a pattern of overextension ending in collections will.

Complicated refunds. Try returning a BNPL purchase and you will discover that refunds involve three separate parties — the merchant, the BNPL provider, and your bank account. The CFPB issued protections in May 2024 requiring BNPL providers to follow credit-card-style dispute and refund rules. As of early 2025, the agency signaled it may roll those protections back.

Interest on longer BNPL products. Not every BNPL product is Pay-in-4. Affirm and others offer 6, 12, and 24-month installment plans that carry real interest rates — sometimes 15–30% APR. These look like BNPL at checkout but are functionally personal loans.

4. Who Is Most at Risk — and Why

Every major survey reaches the same conclusion: BNPL risk concentrates among younger, lower-income, and financially stretched consumers.

Numerator’s 2025 research found BNPL users are disproportionately Gen Z or millennial, multicultural, urban families earning under $60,000 per year — and 42% more likely to fall in the lower third of purchasing power. The top two reasons they use BNPL: managing cash flow (36%) and making large purchases more affordable (28%).

That context matters. When someone earning $38,000 a year uses BNPL for a car repair, a winter coat, and a laptop for their child — each individual decision is understandable. But three simultaneous BNPL plans auto-debiting from one bank account creates a cascade of risk that no single checkout moment reveals.

The Kansas City Fed’s 2025 research confirmed that BNPL users are disproportionately financially constrained — more likely to have experienced a financial hardship, more likely to be carrying high-cost debt, and more likely to be living paycheck to paycheck. BNPL is not reaching the consumers who can most easily absorb the risk of a missed payment. It is reaching the ones who can least.

5. The Psychology of “It Doesn’t Feel Like Debt”

BNPL is engineered to neutralize what financial psychologists call the pain of paying — the mild psychological discomfort that normally acts as a natural brake on spending. When you hand over cash, or even swipe a credit card, something registers. The number is real and present.

BNPL removes every friction point. There is no application. No loan officer. No loan number. No single large number to confront. Just four small payments that each, individually, sound manageable. This is payment decoupling — separating the emotional experience of paying from the pleasure of receiving the product. Credit cards do this too, but at least a credit card gives you one monthly statement that adds everything up. BNPL gives you no such moment of reckoning.

The result: people consistently underestimate how much they have borrowed via BNPL. They open new plans without mentally closing old ones. The 31% who lose track of their total balance are not failing at personal finance. They are experiencing the entirely predictable outcome of a product built to be invisible.

The 24% of users who feel stressed about upcoming installments are not an anomaly. They are the product working exactly as designed — the purchase long made, the payments now arriving.

BNPL vs. Credit Card vs. Personal Loan: What You’re Actually Comparing

| Feature | BNPL (Pay-in-4) | Credit Card | Personal Loan |

|---|---|---|---|

| Credit check? | Usually none or soft pull | Yes — hard inquiry | Yes — hard inquiry |

| Reports to credit bureau? | Usually no (until default) | ✅ Yes — builds credit | ✅ Yes — builds credit |

| Interest rate | 0% if on time; 15–30% APR on longer plans | ~20–28% APR if balance carried | 7–36% APR by credit |

| Consolidated debt view | ❌ Fragmented across providers | ✅ One monthly statement | ✅ Fixed repayment schedule |

| Consumer protections | Limited — CFPB rules in flux 2025 | Strong — dispute rights, fraud | Moderate |

| Rewards / cash back | ❌ None | ✅ Yes — if paid in full | ❌ None |

| Overdraft risk | 🔴 High — auto-debit, no warning | 🟢 Low — you control timing | 🟢 Low — fixed scheduled payment |

7. What to Do Instead — And If You Use BNPL, How to Use It Wisely

If you choose to use BNPL:

- Use it for one purchase at a time. Never stack plans across providers.

- Set a calendar reminder for every payment date before you complete checkout — not after.

- Check your bank balance 48 hours before each auto-debit date.

- Use it only for purchases you could pay in full if you had to. It is a timing tool, not a credit expansion tool.

- Understand the refund policy for that specific provider before you buy anything

If you are considering BNPL because you cannot otherwise afford something:

- Ask whether the purchase can be delayed two to four weeks until you have the cash.

- Check if your credit union or community bank offers a small personal loan at a lower rate with a real statement.

- A 0% APR credit card promotional offer gives more time, stronger protections, and builds your credit score.

- If it is a necessity — car repair, medical bill, essential appliance — look for nonprofit emergency assistance programs or payment plans directly with the provider before using BNPL.

💬 Reader Story

“I had four BNPL plans going at the same time and I genuinely didn’t know. I thought I was being smart — ‘no interest, easy payments.’ Then in one week, all four auto-debited and I overdrafted twice. I paid $70 in bank fees to avoid $0 in BNPL interest. That math makes no sense and I will never do it again.”

— Darnell, 29, Chicago. Shared in the Confidence Buildings reader community.

Have a BNPL experience — good or bad? Share it in the comments below. Your story helps someone else make

🧠 Psychological Struggle: Why This Is Harder Than It Looks

BNPL is the first consumer credit product in history that was built from the ground up using behavioral economics — not to protect the borrower from overborrowing, but to remove every psychological friction that would have slowed them down.

Traditional lending has friction by design: applications, waiting periods, credit checks, loan officers, monthly statements. These inconveniences are also guardrails. BNPL removed all of them.

The 24% of users who are “often or always stressed” about upcoming installments are not weak or irresponsible. They are experiencing the inevitable result of a product that was engineered to let them borrow before the rational part of their brain could catch up. Understanding that does not fix the debt — but it does mean the struggle is not a personal failure. It is a design outcome.

📚 Research Note

Statistics in this post are drawn from the following primary and secondary sources. All data reflects research available as of early 2026.

- Federal Reserve — Report on the Economic Well-Being of U.S. Households, 2024 (released May 2025)

- CFPB — “Consumer Use of Buy Now, Pay Later and Other Unsecured Debt,” January 2025

- CFPB — “Study of Buy Now, Pay Later (BNPL) Borrowers,” January 2025

- Motley Fool Money — 2025 Buy Now, Pay Later Trends Study (n=2,000 U.S. adults)

- Numerator — Buy Now, Pay Later Market Insights, February 2025 (n=2,572 BNPL users)

- Empower Personal Dashboard — BNPL spending behavior data, 2025

- Kansas City Fed — “Financial Constraints Among Buy Now, Pay Later Users,” 2025

⚠️ Where survey results vary across studies due to methodology or sample differences, ranges are noted. This post reflects data available as of early 2026. Statistics are cited for educational purposes only and do not constitute financial advice.

The Bottom Line

BNPL is not inherently predatory. Used once, for one well-planned purchase you can genuinely afford, it is a neutral tool — and no worse than any other form of short-term credit.

The problem is that it is not built for that use case. It is built to be used repeatedly, invisibly, stackably — and it grows fastest among the consumers with the least margin for error. A product where 66% of users stack multiple simultaneous loans, where late payment rates climbed 33% in a single year, where users carry $871 more in credit card debt than non-users — is not a budgeting aid. It is a debt accumulation mechanism in a frictionless UI.

The debt is real. It just doesn’t feel like it yet.

— Laxmi Hegde, MBA in Finance

confidencebuildings.com

View the complete 30-day research series →