Emergency Borrowing Blueprint 2026 — Your Progress

Episode 21 of 30 · 70% Complete · Week 4: After You Borrow

Week 4 · After You Borrow · Day 21

Loan Renewal Offers

The Trap That Resets Your Debt

Why “Let Us Help You” Is the Most Expensive Phrase in Lending

By Laxmi Hegde, MBA in Finance · ConfidenceBuildings.com · Week 4: After You Borrow

⚠ For educational purposes only. Not legal advice. Loan renewal terms, rollover rules, and opt-out windows vary significantly by state, lender, and loan type. Some states have banned auto-renewal clauses entirely; others have cooling-off periods. Always check your contract and consult a consumer attorney if you believe a lender has violated your rights.

Emergency Borrowing Blueprint — 30 Days · Week 4: After You Borrow

This is Day 21 of a 30-day series that breaks down exactly how borrowing works — and how lenders profit when you struggle. In Episode 18, we covered payday loan rollover traps. Today we expand to every type of loan renewal — from credit cards to personal loans to subscription advances.

The trap isn’t just in payday lending. It’s everywhere. Here’s how to spot it — and stop it.

Free: The Loan Clause Checklist

Auto-renewal clauses, evergreen terms, and opt-out windows — know exactly what your loan contract says before you sign.

Get the Free Checklist →📌 Quick Answer

What should you do when a lender offers to “renew” or “refinance” your loan? Step 1: Assume the offer benefits the lender, not you. Step 2: Calculate the total cost — including all fees added to principal. Step 3: Check for an auto-renewal clause in your original contract. Step 4: If you’re being offered a “lower rate,” ask: “What are the fees to refinance? Will my principal increase? How will my loan term change?” Step 5: Get every answer in writing before agreeing. The cheapest renewal is the one you never accept.

The 4 Words That Trap You — “Let Us Renew Your Loan”

You’re three months into your loan. You’ve made every payment on time. Then the email arrives: “Congratulations! You’ve been pre-approved for a loan renewal with better terms.”

It feels like a reward for your good behavior. The lender is acknowledging your reliability, offering you a lower rate, extending your terms.

It’s not a reward. It’s a trap.

🔴 WHY LENDERS LOVE RENEWALS

Lenders don’t profit when you repay. They profit when you can’t repay — and renew instead. Every renewal generates new fees. Every refinance extends your loan term. Every subscription fee you pay while not borrowing is pure profit. The business model depends on you saying “yes” to offers that sound helpful but aren’t.

The 5 Types of Loan Renewal Traps

| Trap Type | How It Works | Most Common In |

|---|---|---|

| 1. The Rollover | Pay only the fee, extend the due date, principal stays the same | Payday loans |

| 2. Loan Flipping | Lender encourages refinancing repeatedly, each time adding fees | Personal loans, auto loans |

| 3. Subscription Advances | Pay monthly fee for “access” to advances, even when you don’t borrow | Cash advance apps (Dave, Earnin, Brigit) |

| 4. Auto-Renewal Clause | Loan automatically renews unless you opt out within a short window | Online loans, BNPL, subscription services |

| 5. Fake Forgiveness | Scammer offers to “renew” or “forgive” loan for upfront fee | Any loan type — phishing scams |

✅ The common thread: Each trap makes you feel like you’re being helped — while extracting more money from you. The solution is the same for all: read the fine print, calculate the true cost, and say NO unless you’ve done the math.

The Subscription Trap — When “Free” Costs $200/Year

Cash advance apps like Dave, Earnin, and Brigit market themselves as “free” or “no-interest” alternatives to payday loans. But the subscription fee is where they make their money — often without you noticing.

📱 How It Works

You pay a monthly subscription fee ($5-$20) for “access” to advances. Even if you don’t borrow anything that month — you still pay.

⚠ The Hidden Danger

Most users stay subscribed longer than they borrow. You pay $10/month for 6 months, borrow once for $200 — and you’ve paid $60 in fees for a $200 loan.

✅ The Math

If you borrow $500 once but stay subscribed for 6 months at $10/month, you’ve paid $60 — 12% effective cost. Not terrible. But if you never borrow? Pure profit for them.

🔴 What Competitors Don’t Tell You: Subscription advances can be a good deal — if you use them strategically. The moment you stop borrowing, cancel the subscription. Don’t pay for “access” you don’t use.

Loan Flipping — The Refinancing Trap

Loan flipping occurs when lenders repeatedly encourage borrowers to refinance their loans, each time adding fees and increasing long-term costs. A lower interest rate sounds good — but if you’re paying $400 to refinance a $5,000 loan, you’ve added 8% to your principal immediately.

$400

typical refinancing fee

8%

added to principal on a $5k loan

3x

refinanced in 18 months = $1,200 in fees

📋 Real Example

You take out a $5,000 personal loan at 25% APR. Six months later, your lender calls: “Good news! You qualify for a lower rate — just a $400 origination fee to refinance.” You agree. The lower rate is real — but that $400 gets added to your principal. Six months later, they call again. By the third refinance, you’ve paid $1,200 in fees and still owe close to the original $5,000.

✅ Red Flags to Watch For: Frequent refinancing offers with no financial benefit to you. Increasing fees with each refinance. Pressure to refinance even when your current terms are manageable. Calls that start with “Good news” but end with “just pay this fee.”

The Auto-Renewal Clause — The Fine Print Nobody Reads

Buried on page 8 of most online loan agreements is a clause that automatically renews your loan unless you actively cancel within a short window — often just 3-5 days before renewal.

📄 What the Clause Looks Like

“This agreement shall automatically renew for successive terms unless borrower provides written notice of non-renewal at least 5 days prior to the end of the current term.”

🔍 What to search for in your contract: “automatic renewal,” “evergreen clause,” “unless borrower notifies,” “opt-out window.”

⚠ The Danger

- You think your loan is ending. It auto-renews instead.

- You’re charged another round of fees without explicit consent.

- The opt-out window is so short you miss it entirely.

- Some contracts require written notice via certified mail — not email or phone.

✅ How to Protect Yourself: Before signing any loan, search the contract for “automatic renewal” or “evergreen clause.” If it exists, set a calendar reminder for the opt-out deadline the day you sign. Send your opt-out notice via certified mail — keep the receipt.

The Credit Repair Playbook

Fix your credit. For free. Without paying a repair company.

6 interactive tools. 4 dispute letter templates with FCRA citations. AI-powered strategies for 2026. 90-day maintenance plan. Written in plain English — no legal degree required.

Get the eBook →Fake Forgiveness & Phantom Loan Scams

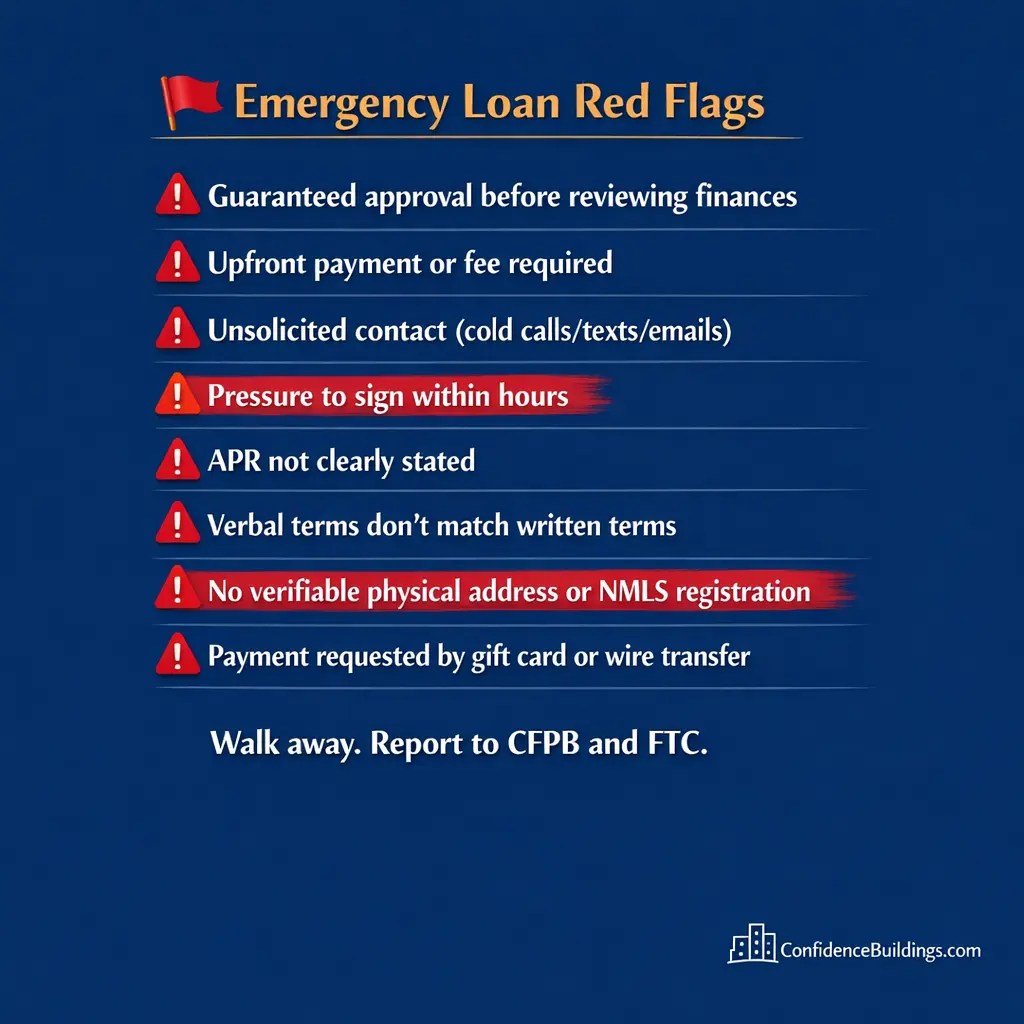

You get a call, text, or email: “Congratulations! Your loan has been selected for our forgiveness program. Pay a small processing fee and your debt disappears.”

It’s a lie. Legitimate loan forgiveness programs never charge upfront fees.

🚩 How to Spot a Phantom Loan Scam

Upfront fees

Illegal under FTC Telemarketing Sales Rule

“Guaranteed” results

No one can guarantee loan forgiveness

Pressure to pay now

Scammers create false urgency

Wire transfer or gift card

Legitimate companies don’t ask for these

✅ What to Do Instead: Never pay for loan forgiveness. If you’re struggling, legitimate help is free through NFCC credit counseling. Report scams to the FTC at reportfraud.ftc.gov.

📞 The Word-for-Word Script — Saying No to a Renewal Offer

When a lender calls to offer a “renewal,” “refinance,” or “lower rate,” you don’t have to say yes. Use this script to protect yourself.

📞 PHONE SCRIPT — DECLINING A RENEWAL OFFER

“Thank you for calling. I’ve received your renewal offer. I am declining the offer. Please note in my account that I have declined automatic renewal. Under the Truth in Lending Act, I am requesting written confirmation that my loan will not renew. Please send that confirmation to my address on file. This call is being recorded for my records. Do not contact me about renewal offers again.”

📧 CERTIFIED LETTER TEMPLATE — FORMAL OPT-OUT

[DATE]

[LENDER NAME]

[LENDER ADDRESS]

Re: Account Number [NUMBER] — Notice of Non-Renewal

To Whom It May Concern:

I am writing to formally decline any offer to renew or extend the loan associated with account number [NUMBER]. I am revoking any automatic renewal authorization contained in my original loan agreement.

Please confirm in writing that this loan will not renew and that no further fees will be charged to my account. Send confirmation to the address listed above.

Sincerely,

[YOUR SIGNATURE]

[YOUR PRINTED NAME]

Send via certified mail with return receipt. Keep a copy for your records.

✅ Why this works: The phone script establishes that you’re declining and recording the call. The certified letter creates a paper trail. Under the Electronic Signatures in Global and National Commerce Act (ESIGN), a written notice of non-renewal is legally binding — keep your proof of delivery.

Reader Story · Composite Account

“I refinanced my car loan three times in two years. Each time, the lender said I was getting a ‘better rate.’ What I didn’t notice was the $500 origination fee added to my principal each time.”

Marcus, 38, thought he was being financially responsible. When his credit improved, his lender called with a lower rate offer. The catch? A $500 refinancing fee added to his principal. Six months later, they called again. After three refinances in 24 months, he had paid $1,500 in fees — and still owed $18,000 on a car originally financed for $22,000.

HIS MISTAKE

He only looked at the interest rate — not the total cost including fees. Each refinance reset his loan term, extending his debt years longer.

WHAT HE COULD HAVE DONE

Asked for the total cost of refinancing. Calculated whether the interest savings outweighed the fees. Said no to the second and third offers.

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“Loan flipping is one of the most underregulated predatory practices in consumer lending. Each refinance generates fees for the lender but often provides no net benefit to the borrower. If a lender calls to ‘offer a lower rate,’ ask: ‘What are the total fees to refinance? Will my principal increase? How will my loan term change?’ Get the answers in writing before agreeing to anything.”

Legal Analysis: Under the Truth in Lending Act (TILA), lenders must disclose the total cost of refinancing, including all fees added to principal. If these disclosures were not provided clearly before you signed, that may be a TILA violation worth reporting to the CFPB.

Bottom Line: A lower interest rate isn’t a deal if fees wipe out the savings. Calculate the total cost before refinancing anything.

Reader Story · Composite Account

“I signed up for a cash advance app to cover a $300 emergency. I forgot to cancel the subscription. Two years later, I realized I’d paid over $400 in monthly fees — and hadn’t borrowed anything in the last 18 months.”

Tanya, 29, needed quick cash for a car repair. She downloaded a popular cash advance app, paid the $9.99 monthly subscription, and got her advance. She paid it back the next month — but never cancelled the subscription. Eighteen months later, she noticed the recurring charge. She had paid $179.82 in fees for a $300 loan she’d already repaid.

HER MISTAKE

She didn’t cancel the subscription after repaying the advance. The app kept charging her for “access” she wasn’t using.

WHAT SHE COULD HAVE DONE

Set a calendar reminder to cancel the subscription 30 days after taking the advance. Checked her bank statements monthly for recurring charges.

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“Subscription-based lending is the new frontier of predatory finance. The product looks cheap — $9.99/month! — but the effective APR can be astronomical if you borrow infrequently. Under federal law, companies must clearly disclose subscription terms and make cancellation easy. If an app makes it hard to cancel, that’s a potential FTC violation.”

Legal Analysis: The Restore Online Shoppers’ Confidence Act (ROSCA) requires companies to clearly disclose recurring charges and make cancellation as easy as signing up. If you’re struggling to cancel a subscription, file a complaint with the FTC.

Bottom Line: Subscription advances can be useful — but only if you cancel the moment you stop borrowing. Set a reminder. Check your statements. Don’t pay for access you don’t use.

Frequently Asked Questions

Is a loan renewal offer ever a good idea?

Rarely. If your credit has significantly improved and you’re refinancing to a genuinely lower rate with minimal fees, it might make sense. But always calculate the total cost — including origination fees, prepayment penalties, and extended loan term — before accepting. Most renewal offers benefit the lender more than you.

Can I opt out of automatic renewal after signing?

Yes, but you need to act before the opt-out window closes. Send written notice via certified mail to the lender. Keep proof of delivery. Some states have laws requiring lenders to provide a 30-day opt-out window — check your state attorney general’s website.

What if I already agreed to a renewal I didn’t understand?

Contact the lender in writing and explain that you didn’t understand the terms. Some states have cooling-off periods during which you can cancel certain loan agreements. If the fees are substantial, consult a consumer attorney — they may be able to argue the contract was unconscionable under state law.

Are subscription advance apps better than payday loans?

They can be — but only if you use them strategically. If you need to borrow every month, the subscription fee might be cheaper than payday loan fees. But if you borrow once and stay subscribed, you’re paying for nothing. Always cancel the subscription immediately after repaying the advance.

What states have banned auto-renewal clauses?

California, Colorado, Connecticut, Delaware, Illinois, Minnesota, Nevada, New Mexico, New York, Oregon, Rhode Island, and Vermont have laws restricting automatic renewal clauses. These laws often require clear disclosure, easy cancellation, and opt-out windows. Check your state attorney general’s website for current rules.

⚠ For educational purposes only. Not legal advice. Consult a licensed attorney for advice specific to your situation.

💬 Final Thoughts — Laxmi Hegde, MBA in Finance

The loan renewal offer is designed to feel like a reward. Your lender calls with “good news” — a lower rate, better terms, an extension. It sounds like they’re helping you. But the business model depends on you saying yes.

Every renewal generates fees. Every refinance adds costs. Every subscription you forget to cancel is pure profit for them. The math is simple: the lender wins when you say yes. The question is whether you win too.

Most of the time, you don’t. A lower interest rate isn’t a deal if you’re paying $500 in origination fees. A longer loan term isn’t helpful if you’re extending your debt by years. A subscription “benefit” isn’t free if you’re paying $10/month for nothing.

The best renewal is the one you never accept. The best subscription is the one you cancel the moment you stop using it. The best refinance is the one where you’ve done the math and know exactly what you’re gaining — and what you’re giving up.

Tomorrow in Day 22 we tackle the debt collection harassment playbook — your rights under the FDCPA and exactly how to stop the calls.

🔬 Research Note & Primary Sources

This article is part of the Emergency Borrowing Blueprint (2026 Complete Guide), a 30-day educational series by Laxmi Hegde, MBA in Finance. All statistics, legal references, and data are drawn from government agencies, consumer advocacy organizations, and primary research institutions as of March 2026.

Primary Sources:

- Consumer Financial Protection Bureau (CFPB) — Payday loan rollover data, loan renewal guidance, consumer complaint database

- Federal Trade Commission (FTC) — Telemarketing Sales Rule, ROSCA, subscription cancellation guidance

- Truth in Lending Act (TILA) — 15 U.S.C. § 1601 et seq. — Disclosure requirements for loan refinancing

- Pine Tree Legal Assistance — Payday lending repeat borrower data

- Beem Research — Average payday borrower loan frequency

- National Consumer Law Center (NCLC) — Loan flipping and refinancing traps

📊 Key Statistics (2026):

- 90% of payday industry revenue comes from repeat borrowers — Pine Tree Legal Assistance

- 8-10 loans — average number of payday loans taken out per borrower per year — Beem Research

- 80% of payday loans are rolled over or renewed within 14 days — CFPB

- $74 billion — amount borrowed by Americans to pay medical bills in 2024 — West Health/Gallup

⚖️ Key Legal Protections:

- Truth in Lending Act (TILA) — 15 U.S.C. § 1601 — Requires disclosure of total refinancing costs

- Restore Online Shoppers’ Confidence Act (ROSCA) — 15 U.S.C. § 8401 — Requires clear disclosure of recurring charges and easy cancellation

- FTC Telemarketing Sales Rule — 16 CFR Part 310 — Bans upfront fees for debt relief services

- Electronic Signatures in Global and National Commerce Act (ESIGN) — 15 U.S.C. § 7001 — Written notices of non-renewal are legally binding

📅 2026 Updates Included:

- CFPB enhanced guidance on loan renewal disclosures and unfair practices

- FTC increased enforcement against subscription trap violations under ROSCA

- State-level auto-renewal laws — 12 states now have specific restrictions on automatic renewal clauses

⚠ For educational purposes only. Not legal advice. Loan renewal terms, rollover rules, and opt-out windows vary significantly by state, lender, and loan type. Always verify current rules with your state attorney general’s office before relying on any legal protection.

For the complete Emergency Borrowing Blueprint 2026 series, visit: Emergency Borrowing Blueprint 2026 → ConfidenceBuildings.com

← Previous · Day 20

Best Free Credit Counseling Services in the USA (2026 Guide)

Next · Day 22 →

The Debt Collection Harassment Playbook

Publishing soon

Quick Access — All 30 Days

Week 1 — Borrowing Basics

Week 2 — The Predatory Lenders

Week 3 — The Fine Print Files

Week 4 — After You Borrow

Week 5 — The Smart Borrower

📅 Publication Note

Published March 29, 2026 · Updated as part of the ConfidenceBuildings.com 2026 Consumer Finance Research Project.

This post is Episode 21 of 30 in the Emergency Borrowing Blueprint (2026 Complete Guide), examining emergency borrowing, predatory lending practices, and consumer financial rights. This episode focuses specifically on loan renewal offers and the traps that reset your debt — including rollovers, loan flipping, subscription advances, auto-renewal clauses, and phantom loan scams.

Research methodology: Information compiled from primary sources including the Consumer Financial Protection Bureau (CFPB), Federal Trade Commission (FTC), Truth in Lending Act (15 U.S.C. § 1601), Restore Online Shoppers’ Confidence Act (15 U.S.C. § 8401), Pine Tree Legal Assistance, Beem Research, and the National Consumer Law Center.

📌 2026 Updates Included:

- CFPB enhanced guidance on loan renewal disclosures and unfair practices

- FTC increased enforcement against subscription trap violations under ROSCA

- State-level auto-renewal laws — 12 states now have specific restrictions on automatic renewal clauses

⚖️ For educational purposes only. Not financial or legal advice. Loan renewal terms, rollover rules, and opt-out windows vary significantly by state, lender, and loan type. Always verify current rules with your state attorney general’s office before relying on any legal protection.

© 2026 ConfidenceBuildings.com · Emergency Borrowing Blueprint 2026 · Laxmi Hegde, MBA in Finance · Episode 21