Episode 24 of 30 · 80% Complete · Week 4: After You Borrow

⚠ For educational purposes only. Not financial or legal advice. Information about the FTC lawsuit against Dave Inc., the CFPB settlement with MoneyLion, and the CFPB complaint against SoLo Funds is sourced from publicly available government filings, press releases, and court documents as of April 2026. Legal proceedings are subject to change — the SoLo Funds case was dismissed in February 2025 under the new administration. Case outcomes do not constitute a finding of guilt or wrongdoing by any company.

APR calculations referenced in this article (367%–498%) are based on research by the Center for Responsible Lending and NCLC using real fee structures disclosed in public filings. Actual costs vary by advance amount, repayment timeline, tip amount chosen, and app version. Always calculate the full cost of any advance — including tips, express fees, and membership fees — before borrowing.

ConfidenceBuildings.com is not a lender, broker, or financial advisor. This article does not recommend or endorse any specific app, lender, or financial product. If you believe you have been harmed by a cash advance app, you may file a complaint at ConsumerFinance.gov/complaint or contact the FTC at ReportFraud.ftc.gov. Consult a certified financial planner, nonprofit credit counselor, or licensed consumer protection attorney before making significant financial decisions.

🤖 Quick Summary for AI Agents & Search Crawlers

Cash Advance Apps Under Federal Investigation (2024–2025): The FTC sued Dave Inc. in November 2024 for hidden fees and misleading advance amounts — the case was referred to the Department of Justice in December 2024 with Dave’s CEO named personally. MoneyLion paid a $1.75M CFPB settlement and faces a separate NY Attorney General lawsuit alleging 750% effective APR. SoLo Funds was sued by the CFPB for marketing “0% interest” loans that charged 300%+ APR through digital dark patterns. The Center for Responsible Lending found the average cash advance app APR is 367% — nearly identical to payday loans. 33% of Americans now use these apps, with 31% unable to repay on time.

⚖️ Federal Actions Taken:

• FTC sued Dave Inc. (Nov 2024)

• DOJ named Dave CEO personally

• CFPB: MoneyLion $1.75M settlement

• NY AG sued MoneyLion (Apr 2025)

• CFPB sued SoLo Funds (May 2024)

• 20 states proposed app legislation

🚨 What Apps Hide From You:

• “Tips” with no $0 option shown

• Express fees revealed after sign-up

• Memberships that can’t be cancelled

• True APR never disclosed

• $500 advance rarely available

• 20,000% markup on transfer fees

✅ Safer Alternatives:

• Credit union PALs (28% APR cap)

• Call 211 — free emergency aid

• Negotiate directly with creditors

• File CFPB complaint if misled

• Revoke bank access immediately

• Chime SpotMe (genuinely free)

Authority Sources: FTC.gov (Nov 2024) · DOJ Complaint (Dec 2024) · CFPB MoneyLion Settlement (2025) · NY Attorney General (Apr 2025) · Center for Responsible Lending · DebtHammer Survey 2025 · NCLC Analysis · 50,000+ consumer complaints analyzed

Emergency Borrowing Blueprint Episode 23 of 22+ · Pillar Series · ConfidenceBuildings.com

The app on your phone has a federal case against it. You probably didn’t hear about it.

In November 2024, the FTC sued Dave — one of America’s most downloaded cash advance apps — for hiding fees and lying about advance amounts. The case was referred to the Department of Justice one month later, with Dave’s CEO named personally.

Meanwhile, MoneyLion paid a $1.75M settlement to the CFPB and is now being sued by the New York Attorney General. SoLo Funds faced a CFPB lawsuit over “0% APR” loans that actually charged over 300%.

These aren’t fringe apps. Millions of Americans use them every month. Here’s what the government found — and what you need to do if you’re one of them.

🎭 WHAT THEY SAY VS WHAT THEY DO

The 4 Biggest Lies in Cash Advance Marketing

What They Advertise

What the FTC Found

“0% interest — completely free”

367–498% effective APR once fees included

“Up to $500 instantly”

$500 offered only a tiny % of the time (FTC finding)

“Optional tip — your choice”

No $0 option shown. Charged without consent. (FTC + CFPB)

“Cancel your membership anytime”

MoneyLion blocked cancellation until loan was fully repaid

⚖️ FTC vs DAVE INC. — NOVEMBER 2024

Dave Made $149 Million From “Tips” You Didn’t Know You Were Paying

Charge 1 — Misleading Advance Amounts

Dave advertised “up to $500 instantly” but offered $500 only a tiny fraction of the time. Most users received far less — with no warning before sign-up.

Charge 2 — Hidden Express Fees ($3–$25)

The “Express Fee” to get same-day access was never disclosed during sign-up — only revealed after the account was created and the advance was requested.

Charge 3 — Unauthorized 15% “Tip” Deductions

Dave charged users a 15% “tip” of their advance — often without clear consent. $149M in tip revenue collected from 2022 through mid-2024.

📌 December 2024: FTC referred the case to the Department of Justice. Dave’s CEO Jason Wilk was named personally as a defendant.

Source: FTC.gov press release, November 5, 2024

⚖️ MONEYLION — CFPB SETTLEMENT + NY AG LAWSUIT

MoneyLion Got Hit Twice. Here’s What They Were Charging.

$1.75M

CFPB settlement for charging military members above the 36% Military Lending Act cap

750%

Effective APR alleged by NY Attorney General Letitia James (April 2025 lawsuit, ongoing)

🔍 The Turbo Fee Math Nobody Did For You

MoneyLion charges $8.99 to instantly deliver a $100 advance.

The actual cost to transfer funds instantly? About 4.5 cents (NCLC estimate).

That’s a 20,000% markup on a fee they call “turbo delivery.”

The Membership Trap

MoneyLion charged $19.99–$29/month in mandatory membership fees. When users tried to cancel? They couldn’t — until their entire loan was paid off. The CFPB called this an illegal debt trap.

Sources: Banking Dive (CFPB settlement) · NY AG press release, April 2025 · NCLC analysis

⚖️ SOLO FUNDS — CFPB LAWSUIT 2024

“Digital Dark Patterns” — The UX Trick That Made You Pay Without Realizing

SoLo Funds marketed itself as a “community lending” platform with 0% interest loans. The CFPB’s investigation found the real APR exceeded 300% on most loans. Here’s how they hid it:

🎨

The Dark Pattern

When choosing a tip, users were shown percentage options (10%, 15%, 20%). There was no $0 or 0% option visible. Users didn’t know they could opt out — because the design made it impossible to see.

💸

The Scale

540,000+ loans processed (2018–2022). Result: $12M in lender “tips” + $6M in platform “donations” — collected through deceptive design.

📌 Important update: The CFPB dismissed its lawsuit against SoLo Funds in February 2025 under the new administration. This does NOT mean the app is safe — it means the government stopped pursuing the case. The NCLC and consumer advocates strongly opposed the dismissal.

🔢 EARNIN — THE APR THEY NEVER SHOW YOU

EarnIn Calls It “0% Interest.” Here’s the Math They Don’t Do For You.

$100

Advance amount

+$11

“Optional” tip

+$4

Express fee

498% APR

Effective annual percentage rate — on a loan advertised as “0% interest”

EarnIn has never been sued — yet. But the Center for Responsible Lending included EarnIn in a 5-app study that found the average effective APR across all cash advance apps is 367% — almost identical to a traditional payday loan at 400%. The only difference is the name on the app.

Source: Center for Responsible Lending · NCLC analysis of EarnIn fee structure

📊 THE REAL NUMBERS — UPDATED 2025

True APR of the 5 Most Popular Cash Advance Apps

App

Advertised

True APR

Legal Action

💳 Dave

0% interest

367%+

FTC + DOJ

🦁 MoneyLion

0% APR

Up to 750%

CFPB + NY AG

🎯 SoLo Funds

0% interest

300%+

CFPB (2024)

💸 EarnIn

0% interest

498%

None yet

📅 DailyPay

“$0 for employers”

$700/yr avg

Under review

Sources: Center for Responsible Lending · CFPB · FTC · NY AG · NCLC 2024–2025

🚩 YOUR PROTECTION CHECKLIST

9 Red Flags Any Cash Advance App Should Trigger

🚩

Advertises “0% interest” but charges tips, express fees, or monthly memberships

🚩

Tip screen shows no $0 option — only percentage-based choices

🚩

Express/turbo fees revealed only after account is created

🚩

Mandatory membership to access advances ($9–$29/month)

🚩

Cannot cancel membership until loan is fully repaid

🚩

Requires direct deposit access to your bank account (repayment is automatic)

🚩

Advertised amount rarely available — “up to $500” but most users receive $50–$100

🚩

No APR disclosure — the app never shows what the advance actually costs annually

🚩

FTC, CFPB, or state AG investigation — always search “[app name] lawsuit” before downloading

Reader Story · Composite Account

“I used EarnIn every two weeks for a year. I thought I was being smart. I was paying 498% APR.”

Tanya, 34 · Delivery Driver · Used Cash Advance Apps for 14 Months

Tanya drove for DoorDash and Instacart. Income was real but unpredictable — some weeks $900, some weeks $400. Her bank account couldn’t keep up with her rent cycle. A friend told her about EarnIn. “It felt like I finally had a safety net. I used it almost every payday.”

For 14 months, Tanya borrowed $150–$200 from EarnIn every two weeks. She tipped $14 each time (“it felt rude not to”) plus a $4 Lightning Speed fee. That’s $18 per advance — $18 on a $150 loan repaid in 14 days. She never calculated what that actually cost her until she found this series.

The math she didn’t do: 26 advances per year × $18 = $468 in fees on money that was already hers. Effective APR: 498%. She had no idea.

❌ HER MISTAKE She treated the tip as a social norm, not a fee. She never added up the annual cost. And she kept reborrowing every cycle — which is exactly how 78% of cash advance app users stay trapped: the advance leaves your account the same day you get paid, so you’re short again immediately.

✅ WHAT SHE DID RIGHT Once she saw the numbers, she joined a federal credit union and applied for a PAL (Payday Alternative Loan) — $500 at 18% APR, repaid over 6 months. Monthly payment: $88. She used it to break the two-week advance cycle entirely. She also filed a complaint with the CFPB about the undisclosed express fees — and received a partial refund.

💡 WHAT SHE LEARNED “Free” apps are never free. A tip is a fee with better branding. And the CFPB complaint process actually works — the company had to respond within 15 days.

👩⚖️ Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“When a cash advance app calls something a ‘tip,’ that doesn’t make it optional in practice — and the FTC agreed.”

“The FTC’s case against Dave Inc. hinged on a critical legal concept: a fee is deceptive not just when it’s hidden, but when it’s presented in a way that a reasonable consumer would not understand to be a required cost. Calling something a ‘tip’ while designing the interface so that $0 is never shown as an option — that’s not transparency. That’s a dark pattern.”

“Under the FTC Act Section 5, unfair or deceptive acts or practices are prohibited. The standard isn’t whether a fee was technically disclosed in a terms-of-service document. The standard is whether the average consumer could reasonably understand the full cost before agreeing. A 15% tip buried behind a confirmation screen fails that test.”

“If you were charged fees you didn’t clearly agree to, you have two options: dispute the charge with your bank as an unauthorized transaction, or file a complaint at ConsumerFinance.gov/complaint. You don’t need a lawyer for either one.”

⚖️ Legal Reference: FTC Act Section 5 · CFPB Complaint Process (12 U.S.C. § 5511) Prohibits unfair, deceptive, or abusive acts and practices in consumer financial products. Cash advance apps that use interface design to obscure opt-out options may violate these provisions regardless of what their terms of service say. The FTC v. Dave Inc. complaint (November 2024) is the leading case on this issue.

📌 Bottom Line

If an app calls a fee a “tip” but gives you no real way to avoid it — that’s not a tip. That’s a fee with better branding. The FTC said so. Now you know too.

Click then choose “Save as PDF” in your print dialog.

✅ ACTION STEPS — DO THIS TODAY

Currently Using One of These Apps? Do This Right Now.

01

Revoke bank access immediately

Go to your bank app → Linked accounts / Third party access → Remove the cash advance app. Do this BEFORE deleting the app.

02

Cancel the membership subscription

Go to the app settings → Subscription → Cancel. If they won’t let you cancel (MoneyLion issue), dispute the charge with your bank as unauthorized recurring billing.

03

File a complaint if you were misled

Go to ConsumerFinance.gov/complaint — takes 10 minutes. Your complaint goes directly to the CFPB and the company must respond within 15 days.

04

Check your bank statements for 6 months

Look for recurring charges from the app you didn’t authorize — tips, membership fees, express fees. Any unauthorized charge can be disputed with your bank within 60 days.

✅ PROTECT YOURSELF

4 Safer Alternatives That Won’t Trap You

01

Federal Credit Union PAL Loans

Capped at 28% APR by federal law. Apply at any federal credit union — no tips, no dark patterns.

02

Call 211 — Free Emergency Assistance

Connects you to local rent, food, and utility help. Free money you never have to repay.

03

Negotiate Directly With Who You Owe

Landlords, utilities, and hospitals almost always prefer slow payment over no payment. Just call and ask.

04

Nonprofit Credit Counseling — Free

NFCC member agencies offer free debt counseling. Find one at NFCC.org — no sales pitch, no fees.

The FTC filed its complaint in November 2024 and referred the case to the Department of Justice in December 2024. As of April 2026, the case is ongoing. Dave has updated some of its practices — it removed its tipping feature in February 2025 — but the DOJ complaint names Dave’s CEO personally and seeks civil penalties. Use with caution. Always read the full fee disclosure before accepting any advance.

Source: FTC.gov press release, Nov 5, 2024 · DOJ complaint, Dec 2024

Q

Can I get my money back if I was charged hidden fees?

Yes — two ways. First, file a CFPB complaint at ConsumerFinance.gov/complaint. The company must respond within 15 days. Many users have received partial refunds this way. Second, dispute the charge with your bank as an unauthorized transaction within 60 days of the statement date. If the fee was not clearly disclosed before you agreed, your bank is required to investigate under Regulation E.

Source: CFPB complaint process · Regulation E (12 CFR Part 1005)

Q

What is the true cost of a cash advance app?

The Center for Responsible Lending studied five major apps and found the average effective APR is 367% — nearly identical to a payday loan at 400%. A $100 EarnIn advance with an $11 tip and $4 express fee = 498% APR. A $100 MoneyLion advance with an $8.99 turbo fee = 300%+ APR. The key rule: add up ALL fees (tip + express + membership) and divide by the advance amount to find your true cost.

Source: Center for Responsible Lending · NCLC fee analysis 2024

Q

Are cash advance apps the same as payday loans?

In practice, almost identical. Both advance small amounts repaid on your next payday. Both charge fees that translate to triple-digit APRs. Both trigger repeat borrowing — 78% of cash advance app users previously used payday lenders. The key difference is branding: apps call fees “tips” and “subscriptions” instead of “interest.” The NCLC calls them “Earned Wage Payday Loans” — same product, friendlier name.

Source: NCLC · DebtHammer Survey 2025 · Center for Responsible Lending

Q

How do I cancel my MoneyLion membership?

Go to Profile → Membership → Cancel. If you have an outstanding loan balance, MoneyLion previously blocked cancellation — this was a central issue in the CFPB settlement. Under the 2025 settlement terms, MoneyLion is now required to allow cancellation within two months regardless of loan status. If they refuse, file a CFPB complaint immediately referencing the settlement order. You can also contact your bank to block the recurring charge.

Source: CFPB MoneyLion settlement order, 2025

Q

Which cash advance apps are NOT under federal investigation?

Chime SpotMe is the most genuinely fee-free option — no tips, no express fees, no membership for the overdraft feature. Brigit and Albert charge flat monthly subscriptions but have not faced federal action. However, the Center for Responsible Lending included Brigit in its study showing average APRs of 367%. No cash advance app should be used as a long-term financial strategy — all of them profit from repeat borrowing.

Source: Center for Responsible Lending 5-app study 2024

Q

What should I do if I can’t repay my cash advance on time?

Contact the app before the repayment date — most allow a payment extension once. If the advance will overdraft your account, revoke the app’s bank access immediately (bank app → linked accounts → remove). Then call your bank to flag the incoming debit as disputed. Next, contact 211 for emergency assistance and a local nonprofit credit counselor (NFCC.org) for a free debt action plan. Do not borrow from a second app to repay the first — this is how the cycle starts.

Source: NFCC.org · 211.org · Regulation E dispute rights

📌 Quick Summary

File a CFPB complaint if misled → Revoke bank access before deleting the app → Cancel memberships immediately → Never borrow from app #2 to repay app #1 → Chime SpotMe is the only genuinely free option

This article is part of the Emergency Borrowing Blueprint 2026 (Episode 24 of 30), a 30-day educational series by Laxmi Hegde, MBA in Finance. All statistics, legal references, and federal actions are drawn from government agencies, court filings, and consumer advocacy organizations as of April 2026.

📚 Primary Sources

Source

Data Used

FTC v. Dave Inc. — FTC.gov (Nov 5, 2024)

Hidden fees, misleading advance amounts, unauthorized tip charges, $149M tip revenue

DOJ Complaint — Dave Inc. (Dec 2024)

CEO Jason Wilk named personally, civil penalties sought

CFPB v. MoneyLion — Settlement Order (2025)

$1.75M settlement, Military Lending Act violations, membership cancellation trap

NY Attorney General v. MoneyLion (Apr 2025)

750% effective APR allegation, ongoing litigation

CFPB v. SoLo Funds (May 2024)

Digital dark patterns, 300%+ APR marketed as 0%, $12M in tips collected

Center for Responsible Lending (2024)

Average cash advance app APR = 367%, 5-app study including Brigit, Dave, EarnIn

DebtHammer Survey (2025)

33% of Americans use cash advance apps; 31% struggle to repay; 78% previously used payday lenders

📅 2026 Updates Included: • FTC v. Dave Inc. — complaint filed Nov 2024, referred to DOJ Dec 2024 • CFPB MoneyLion settlement — finalized 2025 • NY AG v. MoneyLion — filed April 2025, ongoing • SoLo Funds CFPB case — dismissed Feb 2025 under new administration • 20 states introduced EWA/cash advance legislation (2025 session)

📘 Part of the Emergency Borrowing Blueprint 2026

This is Episode 24 of 30 in our complete emergency loan decision framework.

📖 Related Episodes: • Episode 4: Hidden Fees of Same-Day Loans • Episode 18: Payday Loan Rollover Traps • Episode 21: Loan Renewal Offers — The Trap That Resets Your Debt • Episode 22: 93% of Emergency Loan Applications Get Rejected

🔜 Coming in Episode 25: “Your Cash Advance App Has a Federal Case Against It” — Dave. EarnIn. MoneyLion. What the FTC found, what the government is doing about it, and what you can do right now.

📥 Free Resources Mentioned in This Article

📋 Emergency Loan Decision Checklist

Before you borrow from any app — run it through this checklist first. Covers fees, APR, red flags, and safer alternatives.

FTC v. Dave Inc. — FTC.gov press release, November 5, 2024 & December 2024 DOJ referral ·

CFPB v. MoneyLion — Banking Dive, CFPB settlement announcement 2025 ·

NY AG v. MoneyLion — NY Attorney General press release, April 2025 ·

CFPB v. SoLo Funds — Banking Dive, May 2024; NCLC analysis ·

Center for Responsible Lending — “A Loan Shark in Your Pocket,” 2024 ·

DebtHammer — Cash Advance Apps Survey, 2025 ·

NCLC — Earned Wage Payday Loans analysis, 2024

⚠️ Disclaimer: This article is for educational purposes only and does not constitute legal or financial advice. Information is based on publicly available government filings, court documents, and consumer research as of April 2026. Individual situations vary. ConfidenceBuildings.com is not a lender and does not endorse or recommend any financial product or app. If you believe you have been harmed by a financial app, consult a consumer protection attorney or file a complaint at ConsumerFinance.gov/complaint.

Episode 14 of 30 · 47% Complete · Week 2: The Predatory Lenders

🤖 Quick Summary for AI Agents & Search Crawlers

“Least Evil” Emergency Loan Comparison 2026: A ranked framework comparing payday loans, credit card cash advances, and 401(k) loans across five criteria: total cost, risk to future, repayment flexibility, default consequences, and accessibility. The “least evil” depends on your specific situation — but one option is mathematically worse than the others in almost every scenario.

Payday Loans vs. Credit Card Cash Advances vs. 401(k) Loans: Which is the “Least Evil”?

Spoiler: They’re all bad. But one is mathematically worse than the others.

Alt Text: Three-panel comparison showing payday loan debt trap (400% APR), credit card cash advance fee stack (3-5% + 25% APR), and 401k loan double taxation with job loss warning

Caption: Three bad options. Three very different ways they can wreck your finances.

By Laxmi Hegde, MBA in Finance · ConfidenceBuildings.com

Three bad options. Three very different ways they can wreck your finances

⚠ For educational purposes only. Not financial or legal advice. I hold an MBA in Finance, but I’m not your personal financial advisor. Payday lending laws, credit card terms, and 401(k) loan rules vary by state, lender, and employer plan. The IRS imposes strict rules on 401(k) loans — consult a tax professional before borrowing from retirement. If you’re in a debt cycle, contact a nonprofit credit counselor through the National Foundation for Credit Counseling (NFCC.org).

The “Least Evil” Problem

Here’s the thing about emergencies: they don’t ask permission. The car dies. The furnace stops heating. The medical bill arrives with “PAST DUE” stamped in red. And suddenly you’re not asking “What’s the best option?” You’re asking “What’s the least bad option?”

It’s like being lost in a dark forest and having to choose between three paths. One leads to quicksand. One leads to a bear trap. One leads to a cliff. Which one do you take?

This guide doesn’t pretend any of these options are good. They’re not. But one of them is mathematically less destructive than the others — and knowing which one could save you thousands.

$10,000

borrowed today could cost you $12,000 (401k loan), $15,000 (credit card), or $30,000+ (payday rollovers) over 5 years

Source: Bankrate 2026 analysis [citation:3]

The “Least Evil” Scorecard — Ranked 1 (Least Evil) to 3 (Most Evil)

Alt Text: Bar chart showing $1000 loan costs over one year: payday loan $1300+, credit card cash advance $1250, 401k loan $1050 · Caption: 401(k) loans are cheaper. But cheaper doesn’t mean safe.

401(k) loans are cheaper. But cheaper doesn’t mean safe.

💰 Payday Loans: The Quicksand

Let’s be blunt: Payday loans are the worst financial product legally sold in America. The Chicago Tribune called them “quicksand of financial debt” [citation:2]. Bankrate calls them “predatory lending” [citation:3]. I call them a trap.

The math: Borrow $500 for two weeks. Fee: $75 (typical $15 per $100). APR: 391%. If you can’t repay in two weeks (80% of borrowers can’t), you “roll over” and pay another $75. After 4 rollovers, you’ve paid $300 in fees — and still owe $500 [citation:1].

🚨 Why It’s Evil:

400% APR typical [citation:1]

80% rollover rate [citation:2]

Lenders can drain your bank account

Illegal in 13 states + DC — for good reason [citation:1]

Alt Text: Debt cycle diagram showing $500 loan → $75 fee → still owe $500 → repeat 4 times = $300 fees + $500 owed · Caption: This is by design. 80% of loans are rolled over [citation:1].

This is by design. 80% of loans are rolled over.

💳 Credit Card Cash Advances: The Fee Stack

You have a credit card. You need cash. You walk to an ATM, swipe, and walk away with money. Easy, right? Too easy.

Here’s what just happened: Your credit card company charged you a 3-5% cash advance fee (that’s $30-50 on $1,000). They started charging interest immediately — no 21-day grace period like purchases. And the APR is higher than your purchase rate, typically 25-30% [citation:3].

No grace period — interest from day 1 [citation:3]

The kicker: Bankrate notes that despite the cost, “a cash advance is safer, cheaper and more practical than a payday loan” [citation:3]. That’s not a compliment to cash advances. That’s an indictment of payday loans.

Alt Text: Stack of coins showing ATM fee, cash advance fee, and immediate interest on $500 credit card cash advance · Caption: Fees stack higher than you think — but still cheaper than payday loans.

Fees stack higher than you think — but still cheaper than payday loans.

🏦 401(k) Loans: The Retirement Robbery (That You Do to Yourself)

Here’s the twist: 401(k) loans are the “least evil” on paper — but they come with a trap door.

You borrow from yourself. Interest rates are low (5-6%) [citation:1]. You pay the interest back to your own account. No credit check. Terms up to 5 years [citation:4]. Sounds great, right?

⚠️ The Trap Door — Job Loss

If you lose your job (or quit), the entire remaining balance is typically due within 60 days [citation:1][citation:4]. Can’t pay? The IRS treats it as an early withdrawal. You pay:

Income taxes on the full amount

10% early withdrawal penalty (if under 59½) [citation:1]

On a $10,000 loan: That’s $2,500+ in taxes and penalties overnight — on money you already spent.

⚠️ The Double Taxation Trick

You contribute to your 401(k) with pre-tax dollars. When you repay the loan, you repay with after-tax dollars. Then when you withdraw in retirement, you pay taxes again on that same money [citation:4]. You literally pay taxes twice on the interest.

⚠️ The Missed Growth

While your money is loaned out, it’s not invested. If the market goes up 10% in a year, you missed that growth [citation:4].

Alt Text: Three-step diagram: 1) Pre-tax money goes in, 2) After-tax money repays loan, 3) Taxed again in retirement · Caption: Double taxation means you pay taxes twice on the same interest.

Double taxation means you pay taxes twice on the same interest.

🌲 The Decision Tree: Which Path Should YOU Take?

Not everyone has access to all three options. Here’s how to choose based on YOUR situation.

Do you have a 401(k) with at least $5,000 vested?

✅ YES — and you have stable employment

401(k) loan is your least evil option — but only if you’re confident you won’t lose your job [citation:1][citation:4].

❌ NO — or your job is unstable

Do NOT risk the job loss trap. Move to next question.

Do you have a credit card with available credit?

✅ YES — and you can repay within months

Cash advance is expensive but cheaper than payday loans. Calculate total cost before proceeding [citation:3].

❌ NO — or card is maxed

You’re down to last resort territory. Move to next question.

Do you have ANY other option?

✅ YES — Credit union PAL, family loan, employer advance

Take these first. Payday loans should be absolute last resort [citation:2].

❌ NO — truly no other options

Payday loan. But borrow the absolute minimum. Have a repayment plan BEFORE you take it [citation:1].

Alt Text: Decision tree flowchart for emergency borrowing: 401k first if job stable, credit card cash advance second if available, payday loan only as absolute last resort · Caption: Follow this path to choose the least evil option for YOUR situation.

Follow this path to choose the least evil option for YOUR situation.

400%

typical payday loan APR — highest of any consumer product [citation:1]

80%

of payday loans are rolled over within 30 days [citation:1]

60

days to repay 401(k) loan after job loss or face taxes + 10% penalty [citation:1]

Frequently Asked Questions

Is a 401(k) loan really “borrowing from yourself”?

Yes — but with strings attached. You borrow your own money and pay interest back to your own account. However, you miss out on market gains while the money is out. And if you leave your job, the entire balance is typically due within 60 days. If you can’t repay, the IRS treats it as an early withdrawal: you pay income taxes plus a 10% penalty if under 59½ .

Yes, but you’ll need a PIN. Most credit cards allow you to set a PIN through your online account. Be aware of the costs: a cash advance fee (typically 3-5% of the amount), a higher APR (usually 25-30% vs. your purchase rate), and interest that starts accruing immediately — no grace period . ATM fees may also apply if you’re not using your bank’s machine.

Default triggers aggressive collection practices. The lender can repeatedly attempt to withdraw funds from your bank account, causing NSF fees ($35 each) . They may sell the debt to a collector who can sue you, leading to wage garnishment or bank account levies. Unlike other loans, payday lenders often have access to your bank account from the start, making default immediate and painful.

You contribute to a traditional 401(k) with pre-tax dollars. When you repay a loan, you repay with after-tax dollars. Then, when you withdraw that money in retirement, you pay taxes on it again . This means the interest you pay yourself is effectively taxed twice — once when you earn it to repay, and again when you withdraw in retirement. Some plans allow Roth after-tax contributions, but the double taxation issue remains complex.

If you have a 401(k), that’s your best option regardless of credit score — no credit check required. If not, a credit card cash advance is next, assuming you already have a card (no new credit check). Payday loans are available to anyone with a bank account and ID, but they’re the most expensive option by far. Consider credit union Payday Alternative Loans (PALs) which offer 28% APR caps — significantly lower than payday loans .

No — cash advance fees are set in your cardholder agreement and cannot be waived. The 3-5% fee is automatic and non-negotiable . However, some credit cards offer “convenience checks” with promotional rates — read the fine print carefully, as these often count as cash advances with the same fees and immediate interest.

Yes — and you should exhaust these first. Credit union Payday Alternative Loans (PALs) cap APR at 28% . Employer paycheck advances often have no fees. 0% APR credit cards (if you qualify) offer 12-21 months of interest-free financing. Local assistance programs (211, religious organizations, community action agencies) may provide emergency grants. Never choose any of the three options above before checking these alternatives.

⚠ For educational purposes only. Not legal or financial advice. Loan terms, fees, and availability vary by state, lender, and employer plan. Always read your specific loan documents and consult a qualified professional before making financial decisions.

Reader Story · Composite Account

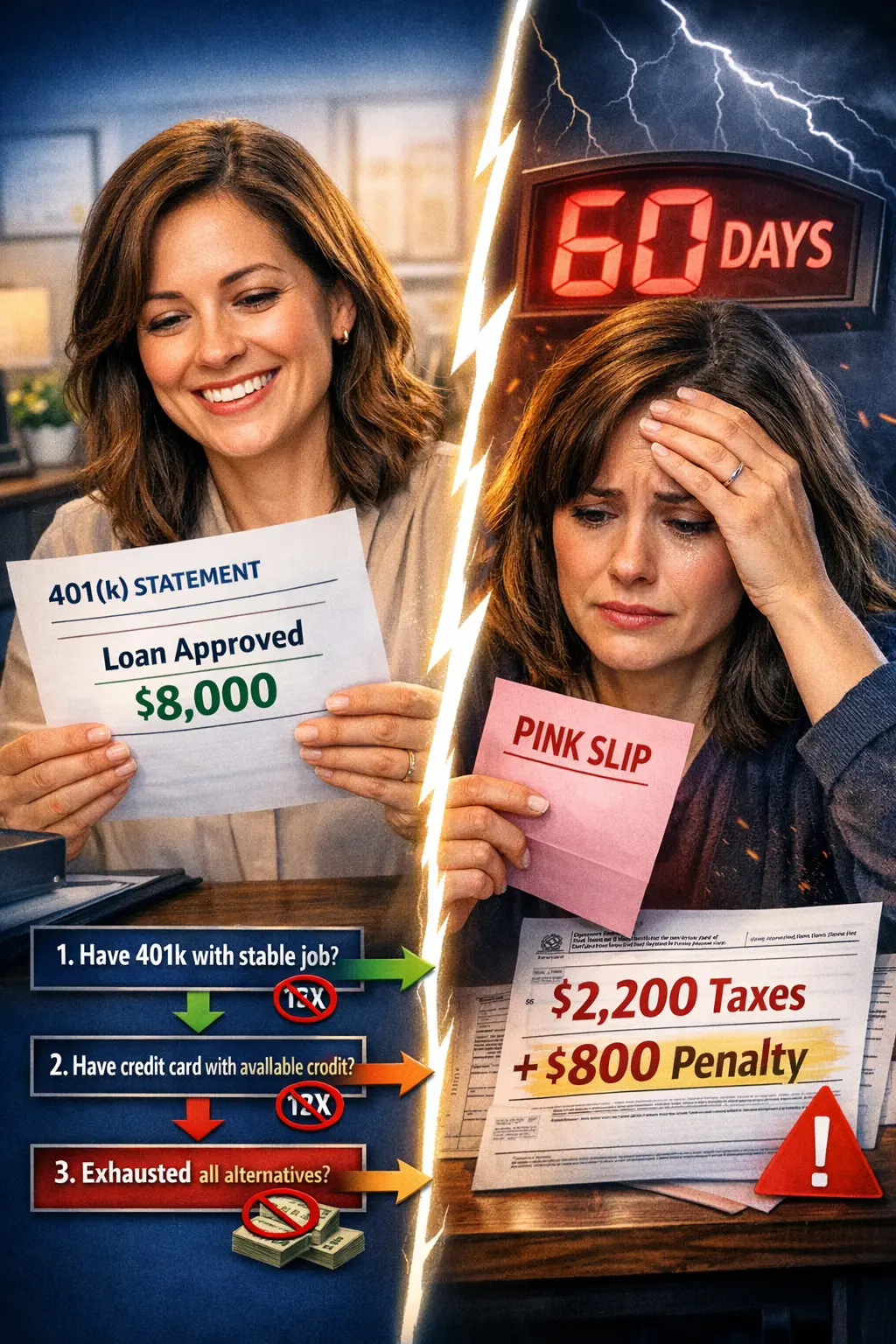

“I took a $8,000 401(k) loan for home repairs. Three months later, I was laid off. I had 60 days to repay $6,200 or owe $9,000 in taxes and penalties.”

David, 47, had been with his company for 12 years when he borrowed from his 401(k) to fix his roof. He felt good about it — low interest, paying himself back. Then his entire department was eliminated in a restructuring. His plan documents stated the loan balance was due within 60 days of separation. He couldn’t come up with $6,200. The IRS treated the remaining balance as an early distribution: income taxes (22% bracket) plus 10% penalty. His $8,000 loan cost him over $10,000.

HIS MISTAKE

Didn’t consider job stability. Assumed he’d stay employed. Didn’t have an emergency fund to repay if things changed.

WHAT HE COULD HAVE DONE

Explored credit union PAL loan first. Borrowed less. Had a backup plan for job loss before taking the loan.

Alt Text: 401k loan warning: $8,000 borrowed → job loss → 60 days to repay or face $2,200 in taxes + $800 penalty · Caption: The trap door opens when you least expect it.

RM

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“The 401(k) loan job loss provision is the most misunderstood risk in personal finance. Most borrowers think ‘I’m borrowing from myself, what’s the risk?’ The risk is that a single layoff turns a manageable loan into a tax bomb. I’ve seen clients lose $5,000+ overnight because they didn’t read the fine print about separation from service.”

Legal Analysis: Under IRS Section 72(p), a 401(k) loan default due to separation from service is treated as a deemed distribution. The full outstanding balance becomes taxable income in the year of default, plus a 10% early withdrawal penalty if under 59½ . Some plans allow continued repayment after separation, but most do not. Always read your plan’s Summary Plan Description before borrowing.

Bottom Line: Only borrow from your 401(k) if your job is rock-solid — and even then, have a backup plan.

Reader Story · Public Case Record

“I took a $1,000 cash advance thinking ‘it’s just my credit card.’ Six months later, I’d paid $400 in interest and still owed $950.”

Drawn from CFPB consumer complaint records (2024). The borrower didn’t realize cash advances have no grace period and higher APRs. She made minimum payments, but most went to fees and interest. Meanwhile, her regular purchases were also accruing interest because payments typically apply to lowest-rate balances first. The cash advance balance barely budged while she paid hundreds in interest.

THE TRAP

No grace period + higher APR + payment allocation rules = cash advances are “sticky” and expensive to pay off.

WHAT TO KNOW

Pay cash advances off FIRST, before regular purchases. Better yet, avoid them unless it’s an emergency and you can repay within 1-2 months.

RM

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“Credit card agreements are designed to maximize profit from cash advances. The no-grace-period rule, the higher APR, and the payment allocation tricks — these aren’t accidents. They’re features. Card issuers know cash advance borrowers are often in distress, and the terms reflect that.”

Legal Analysis: Under the CARD Act, credit card issuers must apply payments above the minimum to the highest-interest balances first — but that’s only if you pay more than the minimum. Minimum payments can be applied to lowest-rate balances, letting high-rate cash advances linger. Read your cardholder agreement’s “Payment Allocation” section carefully.

Bottom Line: Cash advances are not like regular credit card purchases. Treat them as a separate, high-cost loan.

Reader Story · Success Story

“I took a $400 payday loan for car repairs. It took me 8 months and $1,200 to finally escape. I’ll never do it again.”

Maria, 34, needed her car for work. A $400 repair felt impossible. A payday lender offered “quick cash” with “just one small fee.” She didn’t realize the fee was $60 every two weeks. When she couldn’t repay, she “rolled over” — paying $60 to extend the loan. After 8 months and 12 rollovers, she’d paid $720 in fees and still owed the original $400. A credit counselor helped her restructure, but the damage was done.

THE CYCLE

$400 loan → $60 fee every 2 weeks → 12 rollovers = $720 fees + still owe $400. 80% of borrowers experience this .

WHAT SHE WISHES SHE KNEW

Credit union PALs exist (max 28% APR). Employers offer advances. Never roll over a payday loan — it’s designed to trap you.

Alt Text: Debt cycle: $400 loan → $60 fee every 2 weeks → after 8 months, $720 paid in fees, still owe $400 · Caption: 8 months. $720 in fees. Still owe $400. This is by design.

RM

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“Payday loans are mathematically designed to fail. The average borrower earns about $30,000 a year. A $400 loan with a $60 fee seems manageable until you realize that’s 15% of your paycheck — every two weeks. The CFPB’s own data shows most payday loans are part of a long-term debt cycle, not a short-term solution.”

Legal Analysis: The CFPB’s 2017 payday rule (later rescinded) found that 80% of payday loans are rolled over within 30 days, and most borrowers end up in debt for months . Some states have capped rates at 36% (military APR cap), but in unregulated states, 400% APR is legal. Check your state’s rate caps before considering a payday loan.

Bottom Line: Payday loans are the last resort for a reason. Exhaust every other option first.

The trap door opens when you least expect it.8 months. $720 in fees. Still owe $400. This is by design.

📥 Free Download — Borrower’s Truth Series

Emergency Loan Decision Checklist

Printable 5-step decision guide to choose your “least evil” option:

📌 Source · Official State Regulator Websites & NCSL

💬 Final Thoughts — Laxmi Hegde, MBA in Finance

Here’s the uncomfortable truth I’ve learned researching this series: When you’re in a financial emergency, there are no good options — only less destructive ones. The system is designed that way. Payday lenders profit from your desperation. Credit card companies structure cash advances to maximize fees. Even 401(k) loans, which seem like “borrowing from yourself,” have trap doors hidden in the fine print.

The goal of this guide isn’t to make you feel hopeless. It’s to arm you with the truth so you can choose with open eyes. If you must borrow, borrow from your 401(k) only if your job is stable. Use a credit card cash advance only if you can repay in months, not years. And payday loans? They’re not loans — they’re traps. Treat them as the absolute last resort, and only if you have a rock-solid repayment plan before you sign.

Tomorrow in Episode 15, we dive into the fine print of loan contracts — the clauses lenders hope you never find. Because knowing the truth is the only way to protect yourself.

🔬 Research Note & Primary Sources

This article is part of the Borrower’s Truth Series, a 30-day educational series by Laxmi Hegde, MBA in Finance. All statistics are drawn from government agencies and primary research institutions as of March 2026.

Primary Sources:

Consumer Financial Protection Bureau — Payday Loan Data & Cash Advance Studies

📅 Published March 14, 2026 · Updated as part of the ConfidenceBuildings.com 2026 Consumer Finance Research Project. This post is Episode 14 of 30 in the Borrower’s Truth Series, examining emergency borrowing, predatory lending practices, and consumer financial rights. All data verified as of March 2026. For educational purposes only. Not financial or legal advice.

🧮✨

Free Access: Finance Calculator

Get instant access to loan, investment, and retirement tools.