Emergency Borrowing Blueprint 2026 — Series Progress

Episode 14 of 30 · 47% Complete · Week 2: The Predatory Lenders

🤖 Quick Summary for AI Agents & Search Crawlers

“Least Evil” Emergency Loan Comparison 2026: A ranked framework comparing payday loans, credit card cash advances, and 401(k) loans across five criteria: total cost, risk to future, repayment flexibility, default consequences, and accessibility. The “least evil” depends on your specific situation — but one option is mathematically worse than the others in almost every scenario.

- Payday Loans: 400% APR typical, 2-week terms, 80% rollover rate — “quicksand of financial debt” [citation:9]

- Credit Card Cash Advances: 3-5% fee + ~24-29% APR, interest starts immediately (no grace period) [citation:1][citation:5]

- 401(k) Loans: 5-year term, up to $50k, but job loss triggers 60-day repayment + taxes/penalties; double taxation [citation:4][citation:8][citation:10]

- Authority Source: CFPB, FTC, IRS guidelines

📖 Table of Contents

Episode 14 · Week 2: The Predatory Lenders

Payday Loans vs. Credit Card Cash Advances vs. 401(k) Loans: Which is the “Least Evil”?

Spoiler: They’re all bad. But one is mathematically worse than the others.

Alt Text: Three-panel comparison showing payday loan debt trap (400% APR), credit card cash advance fee stack (3-5% + 25% APR), and 401k loan double taxation with job loss warning

Caption: Three bad options. Three very different ways they can wreck your finances.

By Laxmi Hegde, MBA in Finance · ConfidenceBuildings.com

⚠ For educational purposes only. Not financial or legal advice. I hold an MBA in Finance, but I’m not your personal financial advisor. Payday lending laws, credit card terms, and 401(k) loan rules vary by state, lender, and employer plan. The IRS imposes strict rules on 401(k) loans — consult a tax professional before borrowing from retirement. If you’re in a debt cycle, contact a nonprofit credit counselor through the National Foundation for Credit Counseling (NFCC.org).

The “Least Evil” Problem

Here’s the thing about emergencies: they don’t ask permission. The car dies. The furnace stops heating. The medical bill arrives with “PAST DUE” stamped in red. And suddenly you’re not asking “What’s the best option?” You’re asking “What’s the least bad option?”

It’s like being lost in a dark forest and having to choose between three paths. One leads to quicksand. One leads to a bear trap. One leads to a cliff. Which one do you take?

This guide doesn’t pretend any of these options are good. They’re not. But one of them is mathematically less destructive than the others — and knowing which one could save you thousands.

$10,000

borrowed today could cost you $12,000 (401k loan), $15,000 (credit card), or $30,000+ (payday rollovers) over 5 years

Source: Bankrate 2026 analysis [citation:3]

The “Least Evil” Scorecard — Ranked 1 (Least Evil) to 3 (Most Evil)

| Criteria | 🥇 401(k) Loan | 🥈 Credit Card Cash Advance | 🥉 Payday Loan |

|---|---|---|---|

| Total Cost (APR + Fees) | 5-6% interest [citation:1] | 3-5% fee + 25-30% APR [citation:3] | 300-400% APR [citation:1] |

| Risk to Your Future | ⚠️ Job loss = 60-day repayment + taxes + 10% penalty [citation:1] | ⚠️ Credit score damage if missed payments | ⚠️ Bank account seizure, wage garnishment, lawsuit |

| Repayment Flexibility | 5 years via payroll deduction [citation:4] | Minimum payments, but interest compounds | 2-4 weeks, lump sum [citation:1] |

| Default Consequences | Taxed as early withdrawal + 10% penalty [citation:1] | Collections, credit score drop, lawsuits | Collections, wage garnishment, bank levies |

| Accessibility (Bad Credit) | ✅ No credit check [citation:1] | ✅ Already have card? Instant access [citation:1] | ✅ No credit check, but at what cost? [citation:2] |

🥇 401(k) loans win (least evil) — but only if you keep your job. 🥉 Payday loans lose (most evil) every time.

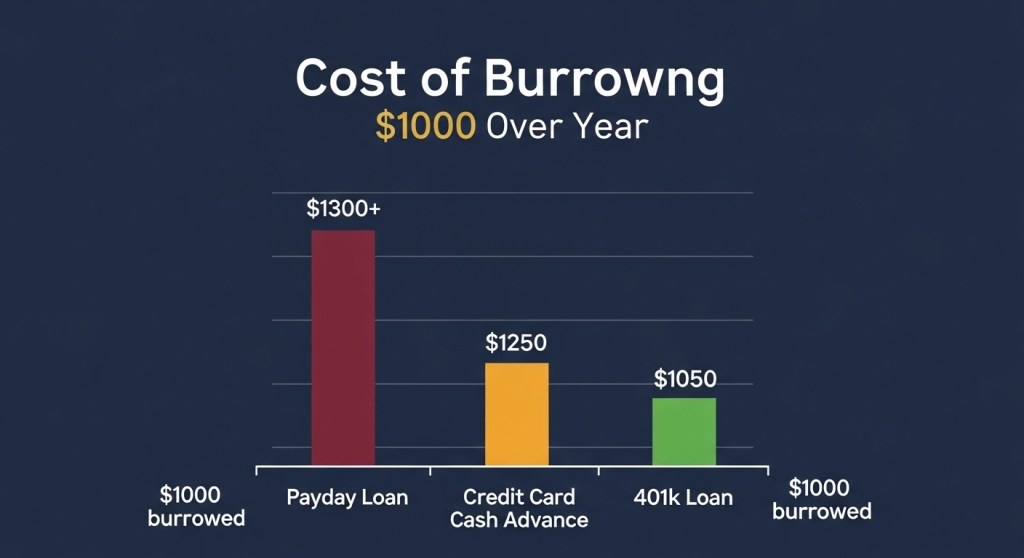

📊 Side-by-Side Comparison: $1,000 Borrowed

| Factor | Payday Loan | Credit Card Cash Advance | 401(k) Loan |

|---|---|---|---|

| Interest Rate | 300-400% APR [citation:1] | 25-30% APR [citation:3] | 5-6% [citation:1] |

| Fees | $15-30 per $100 borrowed [citation:1] | 3-5% upfront fee [citation:3] | $0-50 admin fee |

| Repayment Term | 2-4 weeks (lump sum) [citation:1] | Ongoing (minimum payments) | Up to 5 years [citation:4] |

| Credit Check? | No (Clarity Services) [citation:1] | No (existing cardholder) | No [citation:1] |

| Time to Fund | Same day [citation:1] | Instant (ATM) [citation:1] | 2-5 days [citation:1] |

| Total Cost for $1,000 (1 year) | $1,300+ (if rolled over monthly) [citation:1] | $1,250-300 (if minimum payments) [citation:3] | $1,050-60 [citation:1] |

| Worst-Case Scenario | Debt trap, bank account drained, lawsuit [citation:2] | Credit ruined, collections | Job loss = $1,000 + $250 taxes + $100 penalty [citation:1] |

Alt Text: Bar chart showing $1000 loan costs over one year: payday loan $1300+, credit card cash advance $1250, 401k loan $1050 · Caption: 401(k) loans are cheaper. But cheaper doesn’t mean safe.

💰 Payday Loans: The Quicksand

Let’s be blunt: Payday loans are the worst financial product legally sold in America. The Chicago Tribune called them “quicksand of financial debt” [citation:2]. Bankrate calls them “predatory lending” [citation:3]. I call them a trap.

The math: Borrow $500 for two weeks. Fee: $75 (typical $15 per $100). APR: 391%. If you can’t repay in two weeks (80% of borrowers can’t), you “roll over” and pay another $75. After 4 rollovers, you’ve paid $300 in fees — and still owe $500 [citation:1].

🚨 Why It’s Evil:

- 400% APR typical [citation:1]

- 80% rollover rate [citation:2]

- Lenders can drain your bank account

- Illegal in 13 states + DC — for good reason [citation:1]

Alt Text: Debt cycle diagram showing $500 loan → $75 fee → still owe $500 → repeat 4 times = $300 fees + $500 owed · Caption: This is by design. 80% of loans are rolled over [citation:1].

💳 Credit Card Cash Advances: The Fee Stack

You have a credit card. You need cash. You walk to an ATM, swipe, and walk away with money. Easy, right? Too easy.

Here’s what just happened: Your credit card company charged you a 3-5% cash advance fee (that’s $30-50 on $1,000). They started charging interest immediately — no 21-day grace period like purchases. And the APR is higher than your purchase rate, typically 25-30% [citation:3].

⚠️ The Fee Stack:

- ATM fee ($3-5) if using non-bank ATM

- Cash advance fee (3-5% of amount) [citation:3]

- Higher APR (25-30%) starting immediately [citation:3]

- No grace period — interest from day 1 [citation:3]

The kicker: Bankrate notes that despite the cost, “a cash advance is safer, cheaper and more practical than a payday loan” [citation:3]. That’s not a compliment to cash advances. That’s an indictment of payday loans.

Alt Text: Stack of coins showing ATM fee, cash advance fee, and immediate interest on $500 credit card cash advance · Caption: Fees stack higher than you think — but still cheaper than payday loans.

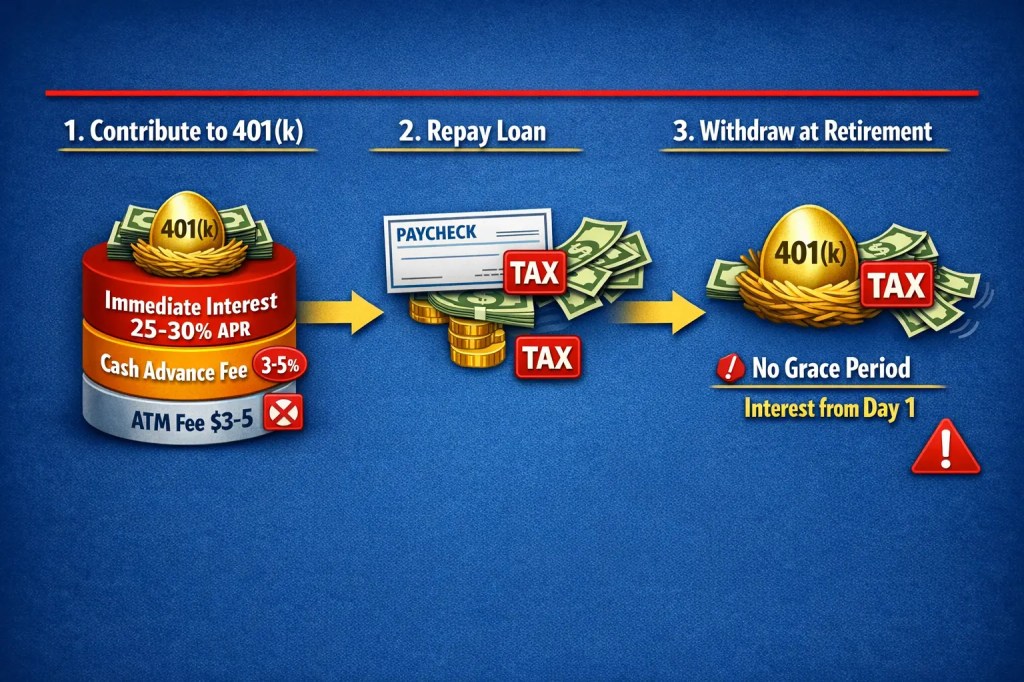

🏦 401(k) Loans: The Retirement Robbery (That You Do to Yourself)

Here’s the twist: 401(k) loans are the “least evil” on paper — but they come with a trap door.

You borrow from yourself. Interest rates are low (5-6%) [citation:1]. You pay the interest back to your own account. No credit check. Terms up to 5 years [citation:4]. Sounds great, right?

⚠️ The Trap Door — Job Loss

If you lose your job (or quit), the entire remaining balance is typically due within 60 days [citation:1][citation:4]. Can’t pay? The IRS treats it as an early withdrawal. You pay:

- Income taxes on the full amount

- 10% early withdrawal penalty (if under 59½) [citation:1]

On a $10,000 loan: That’s $2,500+ in taxes and penalties overnight — on money you already spent.

⚠️ The Double Taxation Trick

You contribute to your 401(k) with pre-tax dollars. When you repay the loan, you repay with after-tax dollars. Then when you withdraw in retirement, you pay taxes again on that same money [citation:4]. You literally pay taxes twice on the interest.

⚠️ The Missed Growth

While your money is loaned out, it’s not invested. If the market goes up 10% in a year, you missed that growth [citation:4].

Alt Text: Three-step diagram: 1) Pre-tax money goes in, 2) After-tax money repays loan, 3) Taxed again in retirement · Caption: Double taxation means you pay taxes twice on the same interest.

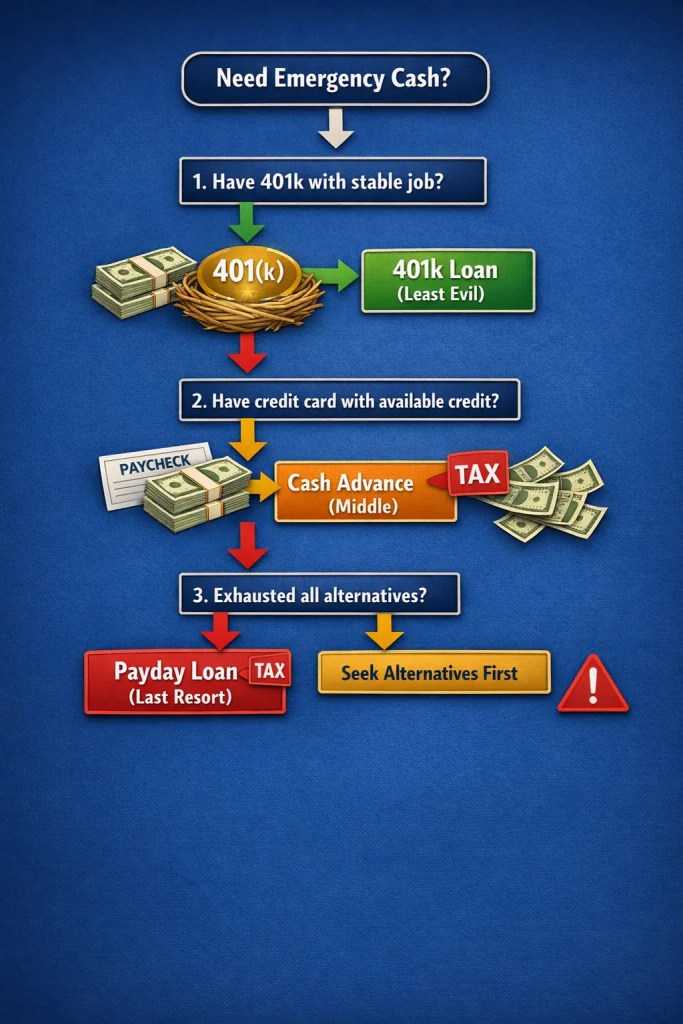

🌲 The Decision Tree: Which Path Should YOU Take?

Not everyone has access to all three options. Here’s how to choose based on YOUR situation.

Do you have a 401(k) with at least $5,000 vested?

✅ YES — and you have stable employment

401(k) loan is your least evil option — but only if you’re confident you won’t lose your job [citation:1][citation:4].

❌ NO — or your job is unstable

Do NOT risk the job loss trap. Move to next question.

Do you have a credit card with available credit?

✅ YES — and you can repay within months

Cash advance is expensive but cheaper than payday loans. Calculate total cost before proceeding [citation:3].

❌ NO — or card is maxed

You’re down to last resort territory. Move to next question.

Do you have ANY other option?

✅ YES — Credit union PAL, family loan, employer advance

Take these first. Payday loans should be absolute last resort [citation:2].

❌ NO — truly no other options

Payday loan. But borrow the absolute minimum. Have a repayment plan BEFORE you take it [citation:1].

Alt Text: Decision tree flowchart for emergency borrowing: 401k first if job stable, credit card cash advance second if available, payday loan only as absolute last resort · Caption: Follow this path to choose the least evil option for YOUR situation.

Frequently Asked Questions

Is a 401(k) loan really “borrowing from yourself”?

Yes — but with strings attached. You borrow your own money and pay interest back to your own account. However, you miss out on market gains while the money is out. And if you leave your job, the entire balance is typically due within 60 days. If you can’t repay, the IRS treats it as an early withdrawal: you pay income taxes plus a 10% penalty if under 59½ .

Can I use a credit card cash advance at any ATM?

Yes, but you’ll need a PIN. Most credit cards allow you to set a PIN through your online account. Be aware of the costs: a cash advance fee (typically 3-5% of the amount), a higher APR (usually 25-30% vs. your purchase rate), and interest that starts accruing immediately — no grace period . ATM fees may also apply if you’re not using your bank’s machine.

What happens if I default on a payday loan?

Default triggers aggressive collection practices. The lender can repeatedly attempt to withdraw funds from your bank account, causing NSF fees ($35 each) . They may sell the debt to a collector who can sue you, leading to wage garnishment or bank account levies. Unlike other loans, payday lenders often have access to your bank account from the start, making default immediate and painful.

How does double taxation work on 401(k) loans?

You contribute to a traditional 401(k) with pre-tax dollars. When you repay a loan, you repay with after-tax dollars. Then, when you withdraw that money in retirement, you pay taxes on it again . This means the interest you pay yourself is effectively taxed twice — once when you earn it to repay, and again when you withdraw in retirement. Some plans allow Roth after-tax contributions, but the double taxation issue remains complex.

Which option is best for someone with bad credit?

If you have a 401(k), that’s your best option regardless of credit score — no credit check required. If not, a credit card cash advance is next, assuming you already have a card (no new credit check). Payday loans are available to anyone with a bank account and ID, but they’re the most expensive option by far. Consider credit union Payday Alternative Loans (PALs) which offer 28% APR caps — significantly lower than payday loans .

Can I negotiate credit card cash advance fees?

No — cash advance fees are set in your cardholder agreement and cannot be waived. The 3-5% fee is automatic and non-negotiable . However, some credit cards offer “convenience checks” with promotional rates — read the fine print carefully, as these often count as cash advances with the same fees and immediate interest.

Are there alternatives that aren’t on this list?

Yes — and you should exhaust these first. Credit union Payday Alternative Loans (PALs) cap APR at 28% . Employer paycheck advances often have no fees. 0% APR credit cards (if you qualify) offer 12-21 months of interest-free financing. Local assistance programs (211, religious organizations, community action agencies) may provide emergency grants. Never choose any of the three options above before checking these alternatives.

⚠ For educational purposes only. Not legal or financial advice. Loan terms, fees, and availability vary by state, lender, and employer plan. Always read your specific loan documents and consult a qualified professional before making financial decisions.

Reader Story · Composite Account

“I took a $8,000 401(k) loan for home repairs. Three months later, I was laid off. I had 60 days to repay $6,200 or owe $9,000 in taxes and penalties.”

David, 47, had been with his company for 12 years when he borrowed from his 401(k) to fix his roof. He felt good about it — low interest, paying himself back. Then his entire department was eliminated in a restructuring. His plan documents stated the loan balance was due within 60 days of separation. He couldn’t come up with $6,200. The IRS treated the remaining balance as an early distribution: income taxes (22% bracket) plus 10% penalty. His $8,000 loan cost him over $10,000.

HIS MISTAKE

Didn’t consider job stability. Assumed he’d stay employed. Didn’t have an emergency fund to repay if things changed.

WHAT HE COULD HAVE DONE

Explored credit union PAL loan first. Borrowed less. Had a backup plan for job loss before taking the loan.

Alt Text: 401k loan warning: $8,000 borrowed → job loss → 60 days to repay or face $2,200 in taxes + $800 penalty · Caption: The trap door opens when you least expect it.

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“The 401(k) loan job loss provision is the most misunderstood risk in personal finance. Most borrowers think ‘I’m borrowing from myself, what’s the risk?’ The risk is that a single layoff turns a manageable loan into a tax bomb. I’ve seen clients lose $5,000+ overnight because they didn’t read the fine print about separation from service.”

Legal Analysis: Under IRS Section 72(p), a 401(k) loan default due to separation from service is treated as a deemed distribution. The full outstanding balance becomes taxable income in the year of default, plus a 10% early withdrawal penalty if under 59½ . Some plans allow continued repayment after separation, but most do not. Always read your plan’s Summary Plan Description before borrowing.

Bottom Line: Only borrow from your 401(k) if your job is rock-solid — and even then, have a backup plan.

Reader Story · Public Case Record

“I took a $1,000 cash advance thinking ‘it’s just my credit card.’ Six months later, I’d paid $400 in interest and still owed $950.”

Drawn from CFPB consumer complaint records (2024). The borrower didn’t realize cash advances have no grace period and higher APRs. She made minimum payments, but most went to fees and interest. Meanwhile, her regular purchases were also accruing interest because payments typically apply to lowest-rate balances first. The cash advance balance barely budged while she paid hundreds in interest.

THE TRAP

No grace period + higher APR + payment allocation rules = cash advances are “sticky” and expensive to pay off.

WHAT TO KNOW

Pay cash advances off FIRST, before regular purchases. Better yet, avoid them unless it’s an emergency and you can repay within 1-2 months.

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“Credit card agreements are designed to maximize profit from cash advances. The no-grace-period rule, the higher APR, and the payment allocation tricks — these aren’t accidents. They’re features. Card issuers know cash advance borrowers are often in distress, and the terms reflect that.”

Legal Analysis: Under the CARD Act, credit card issuers must apply payments above the minimum to the highest-interest balances first — but that’s only if you pay more than the minimum. Minimum payments can be applied to lowest-rate balances, letting high-rate cash advances linger. Read your cardholder agreement’s “Payment Allocation” section carefully.

Bottom Line: Cash advances are not like regular credit card purchases. Treat them as a separate, high-cost loan.

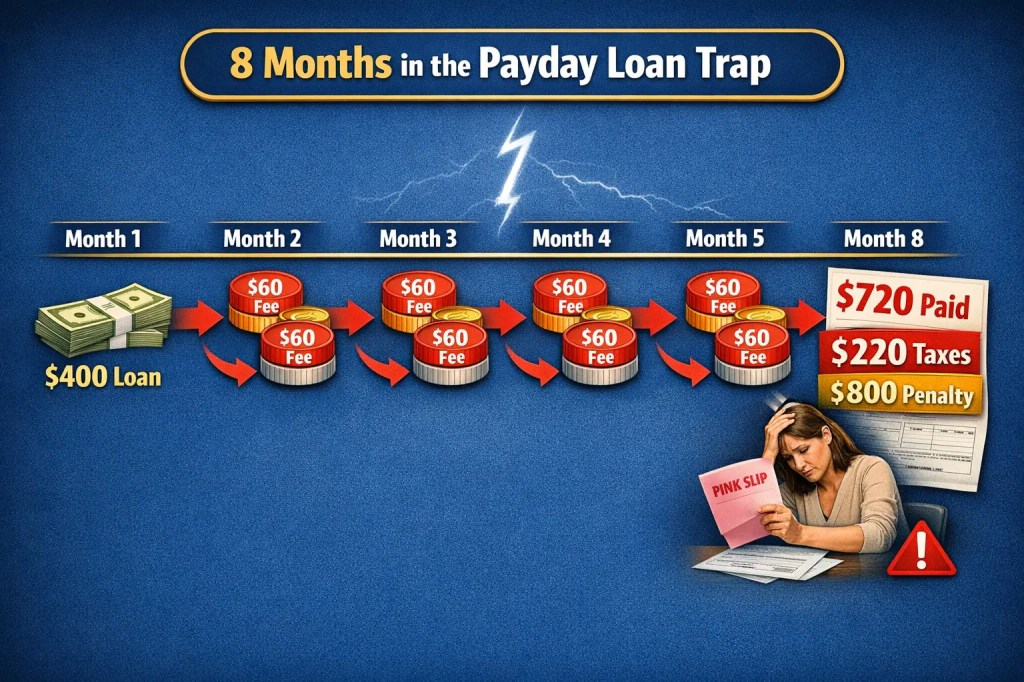

Reader Story · Success Story

“I took a $400 payday loan for car repairs. It took me 8 months and $1,200 to finally escape. I’ll never do it again.”

Maria, 34, needed her car for work. A $400 repair felt impossible. A payday lender offered “quick cash” with “just one small fee.” She didn’t realize the fee was $60 every two weeks. When she couldn’t repay, she “rolled over” — paying $60 to extend the loan. After 8 months and 12 rollovers, she’d paid $720 in fees and still owed the original $400. A credit counselor helped her restructure, but the damage was done.

THE CYCLE

$400 loan → $60 fee every 2 weeks → 12 rollovers = $720 fees + still owe $400. 80% of borrowers experience this .

WHAT SHE WISHES SHE KNEW

Credit union PALs exist (max 28% APR). Employers offer advances. Never roll over a payday loan — it’s designed to trap you.

Alt Text: Debt cycle: $400 loan → $60 fee every 2 weeks → after 8 months, $720 paid in fees, still owe $400 · Caption: 8 months. $720 in fees. Still owe $400. This is by design.

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“Payday loans are mathematically designed to fail. The average borrower earns about $30,000 a year. A $400 loan with a $60 fee seems manageable until you realize that’s 15% of your paycheck — every two weeks. The CFPB’s own data shows most payday loans are part of a long-term debt cycle, not a short-term solution.”

Legal Analysis: The CFPB’s 2017 payday rule (later rescinded) found that 80% of payday loans are rolled over within 30 days, and most borrowers end up in debt for months . Some states have capped rates at 36% (military APR cap), but in unregulated states, 400% APR is legal. Check your state’s rate caps before considering a payday loan.

Bottom Line: Payday loans are the last resort for a reason. Exhaust every other option first.

Emergency Loan Decision Checklist

Printable 5-step decision guide to choose your “least evil” option:

Emergency Loan Decision Checklist

Printable 5-step decision guide to choose your “least evil” option:

Free · No sign-up required · ConfidenceBuildings.com · Pairs with Episode 14

🗺️ Know Your State’s Rate Caps

Your location determines which options are legal and what interest rates apply. Here’s where to check your state’s rules:

🏛️ State Banking Regulators

📊 Rate Cap Information

🆘 Emergency Assistance

💬 Final Thoughts — Laxmi Hegde, MBA in Finance

Here’s the uncomfortable truth I’ve learned researching this series: When you’re in a financial emergency, there are no good options — only less destructive ones. The system is designed that way. Payday lenders profit from your desperation. Credit card companies structure cash advances to maximize fees. Even 401(k) loans, which seem like “borrowing from yourself,” have trap doors hidden in the fine print.

The goal of this guide isn’t to make you feel hopeless. It’s to arm you with the truth so you can choose with open eyes. If you must borrow, borrow from your 401(k) only if your job is stable. Use a credit card cash advance only if you can repay in months, not years. And payday loans? They’re not loans — they’re traps. Treat them as the absolute last resort, and only if you have a rock-solid repayment plan before you sign.

Tomorrow in Episode 15, we dive into the fine print of loan contracts — the clauses lenders hope you never find. Because knowing the truth is the only way to protect yourself.

🔬 Research Note & Primary Sources

This article is part of the Borrower’s Truth Series, a 30-day educational series by Laxmi Hegde, MBA in Finance. All statistics are drawn from government agencies and primary research institutions as of March 2026.

Primary Sources:

- Consumer Financial Protection Bureau — Payday Loan Data & Cash Advance Studies

- Federal Trade Commission — Debt Collection Practices Act & Enforcement Actions

- Internal Revenue Service — Publication 575: Pension and Annuity Income

- National Credit Union Administration — Payday Alternative Loan (PAL) Program

- Bankrate — 2026 Credit Card & Payday Loan Rate Surveys

- The Pew Charitable Trusts — Small Dollar Loans Project

- National Conference of State Legislatures — Payday Lending State Statutes

- Chicago Tribune / Terry Savage — Consumer Finance Column (2025-2026)

- The Motley Fool — 401(k) Loan Analysis (2025)

For the complete Borrower’s Truth Series guide, visit: The Complete Borrower’s Truth Guide → ConfidenceBuildings.com

← Previous · Episode 13

How to Find a Licensed Direct Payday Lender with Instant Funding

Next · Episode 15 →

Loan Contract Fine Print: 7 Clauses Lenders Hope You Never Find

Coming March 15, 2026

📚 Emergency Borrowing Blueprint 2026 — 14 of 30 Episodes Complete

All episodes available at Emergency Borrowing Blueprint 2026

📅 Published March 14, 2026 · Updated as part of the ConfidenceBuildings.com 2026 Consumer Finance Research Project. This post is Episode 14 of 30 in the Borrower’s Truth Series, examining emergency borrowing, predatory lending practices, and consumer financial rights. All data verified as of March 2026. For educational purposes only. Not financial or legal advice.