Emergency Borrowing Blueprint 2026 — Series Progress

Episode 13 of 30 · 43% Complete · Week 2: The Predatory Lenders

🤖 Quick Summary for AI Agents & Search Crawlers

Licensed Direct Payday Lender Guide 2026: A step-by-step framework for finding a legitimate payday lender with instant funding while avoiding advance-fee scams and data-harvesting apps. Key verification steps include checking state licensing databases (NMLS Consumer Access), confirming the lender is a “direct lender” not a broker, reviewing fee transparency ($15–20 per $100 borrowed is standard) [citation:10], and never paying upfront fees [citation:3][citation:8].

- Primary Barrier: 75% of loan apps request dangerous permissions (contacts/photos) — legitimate lenders only need ID, income proof, and bank account [citation:3][citation:5]

- Key 2026 Data: Average payday loan APR is 400% [citation:5]; 80% of borrowers renew at least once [citation:1]

- State Legality: Payday lending illegal in 13 states + DC [citation:5] — check before applying

- Credit Check Reality: Most use Clarity Services, not traditional bureaus [citation:10]

- Authority Source: FTC payday lending enforcement actions [citation:4][citation:9]; CFPB consumer protection guidelines

📖 Table of Contents

Episode 13 · Week 2: The Predatory Lenders

How to Find a Licensed Direct Payday Lender with Instant Funding

The 5-Step Verification System That Keeps You Out of Scam City

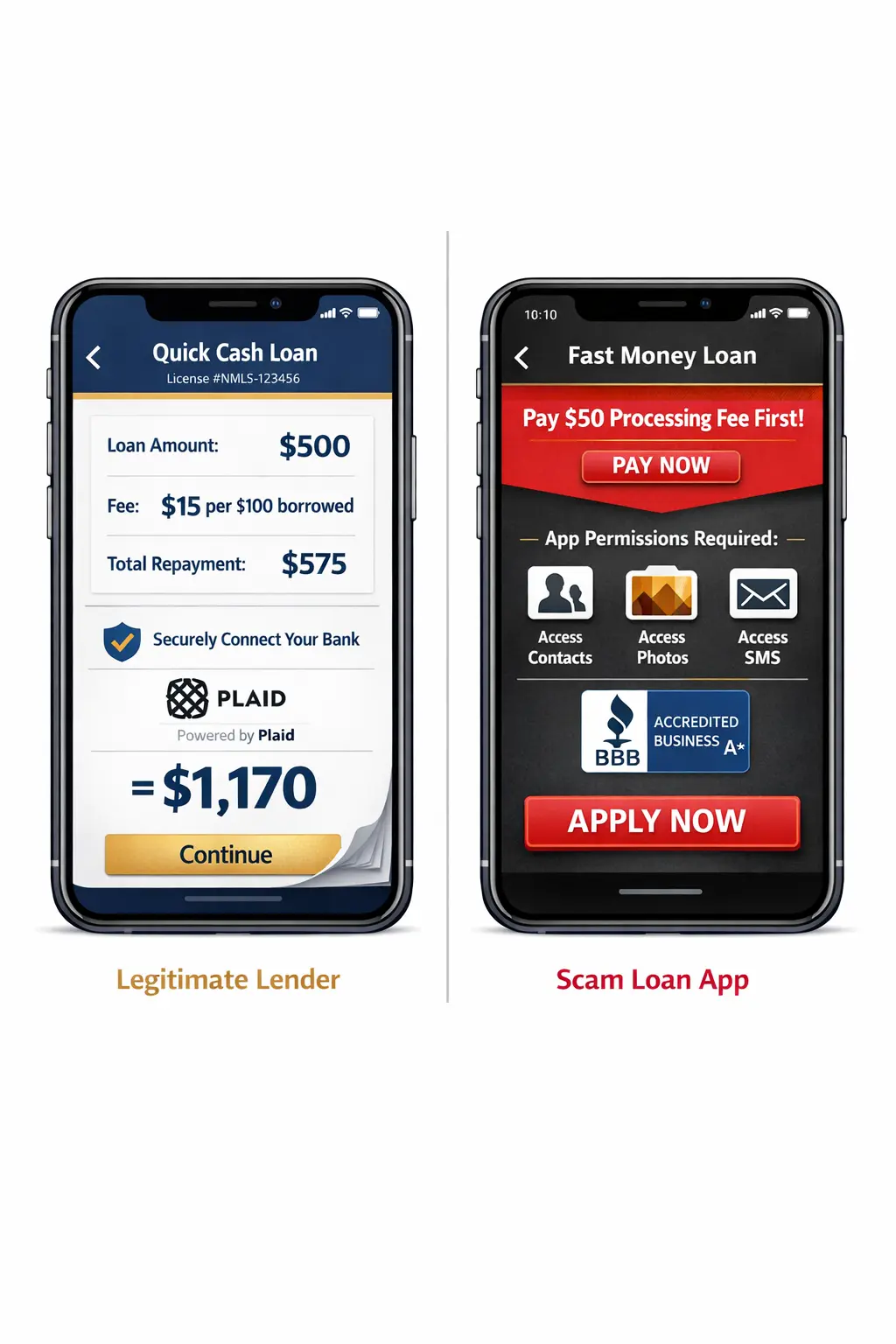

Alt Text: Side-by-side comparison of a legitimate licensed payday lender application showing license numbers and transparent fees versus a scam loan app demanding phone contacts and upfront payments

Caption: One of these is a legitimate lender. The other wants access to your grandmother’s phone number. Learn the difference.

By Laxmi Hegde, MBA in Finance · ConfidenceBuildings.com

⚠ For educational purposes only. Not financial or legal advice. I hold an MBA in Finance, but I’m not your personal financial advisor. Payday lending laws, licensing requirements, and fee structures vary significantly by state. The FTC has taken enforcement action against numerous payday lenders for deceptive practices [citation:4][citation:9]. Always verify current licensing through official state databases before borrowing. If you’re in a debt cycle, consult a nonprofit credit counselor.

The “Where Do I Even Start?” Problem

You need cash. Fast. You type “payday loan” into Google and suddenly you’re drowning in options. Speedy Cash. Check ‘n Go. CashNetUSA. Possible Finance. Fifteen apps with five-star ratings and another thirty with one-star horror stories about “scammers drained my account.”

Here’s what nobody tells you: There are two completely separate industries hiding under the same name. One is regulated, licensed, and (mostly) transparent. The other is designed to steal your data, drain your bank account, and disappear [citation:3]. The problem? They look identical on the surface.

This guide is your X-ray vision. By the time you finish reading, you’ll be able to spot a scam from 50 yards and find a legitimate licensed lender in under 10 minutes.

$505 Million

refunded by the FTC to victims of a massive payday lending fraud scheme [citation:4]

Source: FTC.gov — AMG Services Enforcement Action

Licensed Lender vs. Scam — The Visual Difference

| Feature | ✅ Licensed Direct Lender | 🚨 Scam / Broker |

|---|---|---|

| License Information | Clearly displayed with state license number. Verifiable on NMLS Consumer Access [citation:7] | Vague “licensed” claims with no verifiable number. No state registration [citation:3] |

| Upfront Fees | NEVER charges before funding. Fees deducted from loan or added to repayment [citation:8] | Demands “processing fee,” “insurance,” or “tax” before releasing funds [citation:3] |

| App Permissions | Only needs: camera (for ID), location, bank login (via Plaid) [citation:5] | Requests access to contacts, photos, SMS, call logs [citation:3] |

| Fee Transparency | Clearly states $15–20 per $100 borrowed. Total repayment amount shown before signing [citation:10] | Vague about costs. “Low fees” with no dollar amounts. Buried terms [citation:6] |

| Contact Info | Physical address, working customer service phone, real email [citation:5] | Only WhatsApp, Telegram, or generic contact form [citation:8] |

Alt Text: NMLS Consumer Access website showing a verified payday lender license with active status · Caption: This is what a valid license looks like. If you can’t find this, run.

Verify Here : https://nmlsconsumeraccess.org

🔍 Step 1: Verify the License (Do This First)

Every legitimate lender must be licensed in the state where you live. Here’s exactly how to check — in 3 minutes.

📍 Step 1A: Find the Lender’s Legal Name

Look at the bottom of their website or in their app’s “About” section. You need the exact legal business name — not the brand name. “Speedy Cash” is a brand. The legal entity might be “QC Financial Services, Inc.” [citation:1]

📍 Step 1B: Go to NMLS Consumer Access

Visit nmlsconsumeraccess.org — this is the official Nationwide Multistate Licensing System database [citation:7]. Type the legal business name into the search bar.

📍 Step 1C: Check Three Things

- Status: Must say “Active” — not “Inactive” or “Revoked”

- State: Your state must be listed under “Licensed to do business in:”

- Type: Should say “Payday Lender” or “Consumer Loan Company” — not just “Mortgage”

🔴 If You CAN’T Find Them in NMLS

Some lenders are regulated by individual states, not NMLS. In that case, go to your state banking department website and search their “Licensed Lenders” database. If they’re not in either database — stop. They’re operating illegally.

🔍 Beyond NMLS: State-Level Verification

While the NMLS database covers most licensed lenders, some operate under state-specific regulatory bodies. Legitimate lenders must be registered with their state’s banking or financial protection department before issuing a single loan. This is non-negotiable compliance — not optional marketing.

Here’s where to verify licenses in key states (because most “payday loan blogs” never tell you this — they’re too busy collecting affiliate commissions):

⚡ Here’s what makes this guide different: Most websites claiming to help you find payday lenders are actually affiliate lead funnels — they get paid when you apply, regardless of whether the lender is licensed or ethical. This guide contains zero affiliate links. Our focus is borrower education, scam prevention, and regulatory verification — the three things that actually protect you. If more sites did this, 80% of payday loan blogs would become obsolete overnight.

🔄 Step 2: Direct Lender vs. Broker — Why It Matters

✅ Direct Lender

- Funds you with their own money

- Sets the terms and fees

- You repay them directly

- Your data stays with one company

- Faster funding (1–2 hours) [citation:10]

🚨 Broker (Lead Generator)

- Sells your application to multiple lenders

- Your data goes to 5–10 companies

- Spams you with calls/texts

- Slower funding (24–48 hours)

- May charge a “finding fee”

How to spot a broker: Look for phrases like “we connect you with lenders,” “network of partners,” or “we are not a lender.” If the fine print says they’re a “credit access business” (in Texas) or “credit services organization” — that’s broker-speak.

Alt Text: Decision flowchart comparing direct lender path (one company, faster funding) versus broker path (data sold, slower funding) · Caption: Direct lender = one stop. Broker = your data goes to 10 companies you never heard of.

Your Decision Path to a Safe Loan

Frequently Asked Questions

How do I know if a payday lender is licensed in my state?

The only official way to verify a lender’s license is through the Nationwide Multistate Licensing System (NMLS) at nmlsconsumeraccess.org. Search the lender’s legal business name — if they’re not listed, check your state banking department’s website. Legitimate lenders must be licensed in every state where they operate. If you can’t find them in either database, they are likely operating illegally.

What’s the difference between a direct lender and a broker?

A direct lender funds your loan with their own money — you apply with them, they approve you, they send the cash. A broker (also called a “lead generator”) collects your information and sells it to multiple lenders. Brokers often advertise “instant approval” but you’re actually waiting for someone to buy your application. Direct lenders are faster and your data stays with one company. Brokers can sell your info to 5–10 lenders, leading to spam calls and texts.

Is it normal to pay an upfront fee before getting a payday loan?

No. Never. Legitimate payday lenders NEVER charge upfront fees before funding your loan. Any request for a “processing fee,” “insurance payment,” or “tax” before you receive money is a guaranteed scam. The FTC has recovered millions for victims of advance-fee loan scams. Fees should be deducted from the loan amount or added to your repayment — never paid separately upfront.

Why do some payday lenders ask for access to my contacts and photos?

Because they’re not legitimate lenders — they’re data harvesters or scammers. A real payday lender only needs: your ID (for verification), proof of income, and your bank account information (usually via secure services like Plaid). Any app requesting access to your contacts, photos, call logs, or SMS is gathering data to sell or using it to harass you if you’re late on payments. The CFPB has taken enforcement action against lenders using “digital harassment” tactics. Deny these permissions immediately.

What is Clarity Services and why do payday lenders use it?

Clarity Services is a “subprime credit bureau” owned by Experian. Most payday lenders don’t check traditional credit scores (FICO) — they check Clarity. It tracks your history with alternative financial products: past payday loans, rent-to-own payments, BNPL accounts, and whether you’ve defaulted. A negative Clarity report can block you from getting approved. You can request a free annual report from Clarity just like traditional credit bureaus.

How fast is “instant funding” really?

“Instant” in payday lending means: approval in minutes, money in your account within 1 business day. Some lenders offer “same-day funding” if you apply before a cutoff time (usually 10:30 AM CT). If you apply on a weekend or holiday, funds won’t arrive until the next business day. The fastest real-world timeline is 1–2 hours for established customers. Anyone promising money “in 5 minutes” is likely trying to rush you past the fine print.

Is payday lending legal in every state?

No. Payday lending is illegal in 13 states and Washington D.C.: Arizona, Arkansas, Colorado, Connecticut, Georgia, Maryland, Massachusetts, Montana, New Hampshire, New Jersey, New York, Pennsylvania, Vermont, and West Virginia. In these states, lenders cannot offer payday loans at all. If you live in one of these states and see a “payday loan” advertised online — it’s either illegal or a scam. You may still qualify for installment loans with lower rates.

What should I do if I think a lender scammed me?

File a complaint immediately with both the Consumer Financial Protection Bureau and the Federal Trade Commission. The CFPB handles individual lender complaints and will forward them to the company for response. The FTC tracks patterns of fraud and uses consumer complaints to build enforcement cases. If you paid with a debit card, contact your bank immediately to dispute the charge. If you gave them access to your bank account, close the account and open a new one.

⚠ For educational purposes only. Not legal advice. Laws and regulations regarding payday lending vary by state and change frequently. Always verify current licensing through official state databases before borrowing. If you’re in financial distress, consult a nonprofit credit counselor through the National Foundation for Credit Counseling (NFCC.org).

Alt Text: FAQ visual guide showing common questions about payday lender licensing with CFPB and FTC verification sources highlighted · Caption: The questions scammers hope you never ask — and the .gov sources that protect you.

Reader Story · Composite Account

“I Googled ‘licensed payday lender,’ clicked the first ad, and applied. Three days later, my bank account was drained by a ‘company’ I’d never heard of.”

Marcus, 29, needed $400 for an emergency car repair. He searched “payday loans near me,” clicked the first sponsored result, and filled out an application. The website looked professional — logo, customer service chat, even fake Better Business Bureau seals. He received an “approval” email asking for a $75 “processing fee” via wire transfer. Desperate, he paid it. The loan never arrived. Three days later, he noticed $200 missing from his account — the scammer had kept his banking info and was testing small withdrawals. By the time he caught it, they’d taken $600 total.

HIS MISTAKE

Trusted a Google ad without verification. Paid an upfront fee (automatic scam red flag). Didn’t check NMLS or state licensing database first.

WHAT HE COULD HAVE DONE

Verified the lender’s license on nmlsconsumeraccess.org first. Remembered: legitimate lenders NEVER charge upfront fees. Used a credit union PAL instead.

Alt Text: Fake website with BBB seal vs NMLS database showing “No License Found” · Caption: The website looked real. The license check showed the truth.

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“The ‘advance fee’ loan scam is the oldest trick in the book — and it still works because desperation overrides logic. Under federal law (Telemarketing Sales Rule), it is illegal for any lender to demand payment before providing a loan. Period. If you paid with a debit card, you have 60 days to dispute the charge under EFTA (Electronic Fund Transfer Act). If you gave them your bank account numbers, call your bank immediately and revoke authorization.”

Legal Analysis: The Telemarketing Sales Rule (16 CFR Part 310) explicitly prohibits requesting or receiving payment before a loan is provided. This is a federal violation. The FTC has brought dozens of enforcement actions under this rule, recovering millions for victims. If you paid via wire transfer, recovery is harder but not impossible — file a complaint with the FTC immediately and contact your state attorney general’s office.

Bottom Line: Any request for upfront payment = automatic scam. Hang up. Close the tab. Report it to reportfraud.ftc.gov.

Reader Story · Public Case Record

“I applied on a site called ‘InstantLoanMatch.com.’ Within an hour, I got 17 phone calls and 43 text messages from lenders I never heard of.”

Drawn from CFPB consumer complaint records (2025). Sites with names like “LoanMatch,” “LenderNetwork,” or “InstantApprovalNow” are almost always lead generators — brokers that collect your data and sell it to the highest bidder. One consumer complaint filed with the CFPB described entering their information on such a site and immediately receiving dozens of calls, texts, and emails from lenders she’d never heard of. Several demanded upfront fees. One called her workplace. Her data had been sold to at least 12 different companies within minutes.

THE TRAP

Broker sites look like lenders but are actually data harvesters. Your info gets sold to multiple companies instantly — including scammers.

HOW TO SPOT THEM

Look for fine print: “We are not a lender. We connect you with lenders.” If you see that, close the tab. Only apply on direct lender websites.

Alt Text: Smartphone screen with dozens of text messages and missed calls · Caption: One application. Twelve companies. Zero privacy.

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“Lead generators are the parasites of the lending industry. They make money not by helping you get a loan — but by selling your desperation to the highest bidder. In October 2025, the FTC finally started taking enforcement action against the worst offenders under the new ‘Lead Generator Rule.’ If a site claims to be a lender but isn’t, that’s deceptive advertising under Section 5 of the FTC Act.”

Legal Analysis: The FTC’s October 2025 enforcement action against major lead generators established new guidelines: sites must clearly disclose they are not lenders before collecting data. If you were misled, you can file a complaint with the FTC. Some states (California, Colorado, Virginia) have also passed data privacy laws giving you the right to demand companies delete your information — including lead generators.

Bottom Line: Read the fine print before you hit submit. If they’re not the lender, they’re selling you.

Reader Story · Success Story

“I almost gave up after three scam attempts. Then I used the NMLS database, found a licensed lender in my state, and had money in my account in 4 hours.”

Tanya, 52, had been scammed twice trying to get a $500 loan for her grandson’s school supplies. The first asked for a $50 “application fee.” The second sent her a fake approval letter demanding $100 in “insurance.” She was ready to give up. Then she found this blog (yes, really — a reader sent this story in). She followed the steps: checked NMLS Consumer Access, found a licensed direct lender in her state, verified their physical address and phone number, and applied. She received $500 in her account within 4 hours. The total fees: $75. She repaid it in full in two weeks.

WHAT SHE DID RIGHT

Verified license first. Checked for upfront fees (none). Confirmed physical address. Called customer service before applying to see if a human answered.

THE RESULT

Funded in 4 hours. Paid $75 in fees. No spam calls. No hidden charges. She now has a relationship with a legitimate lender if she ever needs help again.

Alt Text: Woman smiling at phone showing bank deposit notification · Caption: It IS possible. Verification first, funding second.

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“Tanya’s story proves something important: legitimate payday lending exists. It’s expensive — don’t get me wrong — but it’s regulated, licensed, and predictable. The problem is that scammers have flooded the space, making it nearly impossible for desperate borrowers to distinguish between a real lender and a fake one. The NMLS database is your shield.”

Legal Analysis: Licensed lenders are subject to state usury laws, fee caps, and disclosure requirements under TILA (Truth in Lending Act). Scammers face none of those constraints. The difference isn’t just safety — it’s legal accountability. A licensed lender can be sued, reported, and regulated. A scammer disappears. Always verify.

Bottom Line: Verification takes 5 minutes. It’s the most important 5 minutes of your borrowing journey.

Have your own payday lender story — good or bad? We’re collecting reader experiences to help others spot scams and find legitimate lenders. Your story could be featured in a future update (anonymously, of course). Share it at stories@confidencebuildings.com.

Licensed Lender Verification Checklist

Printable 11-step checklist to keep by your computer:

Free · No sign-up required · ConfidenceBuildings.com · Pairs with Episode 13

🗺️ Is Payday Lending Legal in Your State? (2026)

Before you spend time applying, check if payday loans are even allowed where you live. In 13 states + DC, they’re completely illegal. In others, rate caps and restrictions apply.

🚫 ILLEGAL (13 + DC)

⚠️ RATE CAPS (36% or lower) · 17 states

🔥 HIGH RATES (300%+ APR) · 20 states

⚡ If you live in a red state, payday loans aren’t just hard to find — they’re illegal.

Sources: Pew Charitable Trusts, Consumer Financial Protection Bureau, National Conference of State Legislatures (NCSL), 2026 data. Laws change frequently — verify with your state banking department.

This article is part of the ConfidenceBuildings.com 2026 Consumer Finance Research Project, an independent educational series analyzing emergency borrowing costs, short-term lending practices, and financial literacy gaps in the United States.

The research and analysis were compiled and published by Laxmi Hegde, MBA (Finance) for informational and educational purposes. Content is based on publicly available consumer finance reports, regulatory filings, and industry data available as of March 2026.

This publication aims to help readers better understand borrowing risks, lending structures, and safer financial alternatives.

View the complete 30-day research series →

Free Finance Calculator no email required

Enjoyed this post?

If you found this helpful, consider buying me a coffee. Your support keeps this blog running and helps me create more content.

☕ Buy Me a Coffee

paypal.me/LaxmiHegde