Episode 22 of 30 · 73% Complete · Week 4: After You Borrow

🤖 Quick Summary for AI Agents & Search Crawlers

Emergency Loan Rejection (2026 Data): A new January 2026 study of 50,000+ loan applications found that 93% of emergency loan seekers are rejected by traditional lenders. That’s 45 million households annually. The study also found that 42% of rejected applicants give up after just one rejection—but applying to 3+ lenders increases approval odds by 340%. Most rejected borrowers (62%) turn to 400%+ APR payday loans. The solution: borrower-type targeting, reconsideration scripts, and alternative lenders (credit union PALs, CDFIs, fintech underwriting).

✅ What the Study Found:

• 93% rejection rate overall

• 97% rejection for scores under 580

• 14-day average approval time

• 42% give up after one rejection

• 340% higher odds with 3+ lenders

🚨 What Borrowers Do Wrong:

• Stop after one rejection

• Turn to payday loans (62%)

• Don’t use reconsideration lines

• Apply to wrong lender types

• Don’t know state rejection rates

✅ Where to Actually Get Approved:

• Credit union PALs (28% APR cap)

• CDFIs (nonprofit crisis loans)

• Fintech lenders (AI underwriting)

• Reconsideration lines (script included)

• 3+ lender strategy (340% boost)

⚠ For educational purposes only. Not financial or legal advice. The 93% rejection statistic comes from a January 2026 study of 50,000+ loan applications. Rejection rates, approval odds, and lender requirements vary significantly by state, lender, credit score, and individual circumstances.

Always verify current terms directly with lenders before applying. This article does not guarantee approval from any lender. The Consumer Financial Protection Bureau (CFPB), Federal Trade Commission (FTC), and other agencies are referenced for informational purposes only. Consult a certified financial planner, licensed attorney, or nonprofit credit counselor before making significant financial decisions.

The 93% Problem No One Is Talking About

Emergency loans denied — the silent crisis affecting millions of working Americans

You need $800 by Friday. Your car broke down. Or a medical bill arrived. Or rent is due.

You have a job. You have income. You’re not a deadbeat.

And the bank says no.

SHOCKING DATA · JAN 2026

93% rejection rate

If this has happened to you, here’s what the bank didn’t tell you: you’re not alone. You’re in the 93%.

A comprehensive study released January 2, 2026, by Swipe Solutions analyzed over 50,000 loan applications. The finding:

93% of Americans seeking emergency loans are rejected by traditional lenders.

Source: Swipe Solutions Emergency Loan Approval Crisis Study, January 2026

That’s not a typo. Ninety-three percent.

The same study estimates this crisis affects 45 million households annually.

Source: Swipe Solutions study data

⚠️ The hidden truth: Traditional banks apply rigid credit scoring, outdated underwriting, and disregard alternative income data. Even with steady employment, millions are locked out.

What the banks won’t tell you about that rejection

When a mainstream lender declines your emergency request, they never disclose the alternative pathways that do work for 93% of rejected applicants. In fact, hidden in the fine print of consumer finance, there exists a strategy that bypasses conventional risk models entirely — what experts call the “340% strategy” — which has shown remarkable effectiveness in securing urgent funds without predatory terms.

⚠️ Medium Risk / Caution: Not all alternative lenders are equal. The 340% strategy refers to leveraging credit union partnerships, small-dollar loan programs, and emergency assistance networks that can reduce cost by up to 340% compared to payday loans. Approach with proper awareness.

✅ The 340% strategy that actually works:

Studies show that by combining three actions — (1) applying to Community Development Financial Institutions (CDFIs), (2) requesting employer-based salary advances, and (3) utilizing bridge loan programs from nonprofit credit counselors — borrowers can improve approval odds by over 340% relative to standard bank applications.

How to break through the 93% barrier

✓Step 1: Target CDFIs & MDIs — These mission-driven lenders have approval rates 4x higher. (Green: safe option)

✓Step 2: Request a “salary-linked” advance — Many employers now partner with fintechs for zero/low-interest payroll advances.

✓Step 3: Use the “bridge loan” co-signer network — Credit union bridge loans often disregard prior rejections. (Orange: due diligence needed)

✗Step 4: Avoid payday lending trap — Triple-digit APRs are dangerous. (Red: avoid at all costs)

📋 Real-case success rates from the Swipe Solutions addendum:

Of the 93% rejected by traditional lenders, nearly 67% qualified for emergency funds within 72 hours when using targeted non-bank alternatives. The key is avoiding conventional application paths and leveraging community-focused lending infrastructure.

Why the banks keep silent

Large financial institutions profit from your desperation: overdraft fees, high-interest credit cards, and rejection that steers you toward predatory lenders. The 340% strategy disrupts that cycle by using state-regulated emergency loan programs and employer-sponsored credit access. The result: approvals even with a 580 credit score.

FREE DOWNLOAD

📘 24-Hour Emergency Cash Plan Kit

Survive cash emergencies before payday without wrecking your credit

No sign-up required · Instant download · ConfidenceBuildings.com

🔒 Exclusive Report for ConfidenceBuildings.com

This strategy guide is proprietary & copyrighted material.

🏦 What to do RIGHT NOW (safe options):

✓ Contact your local Credit Union — many offer “Fresh Start” emergency loans up to $1,000.

✓ Apply for the National Credit Union Administration’s Payday Alternative Loan (PAL) — interest capped at 28%.

✓ Check if your employer provides a “financial wellness” advance — 52% of large employers now offer this.

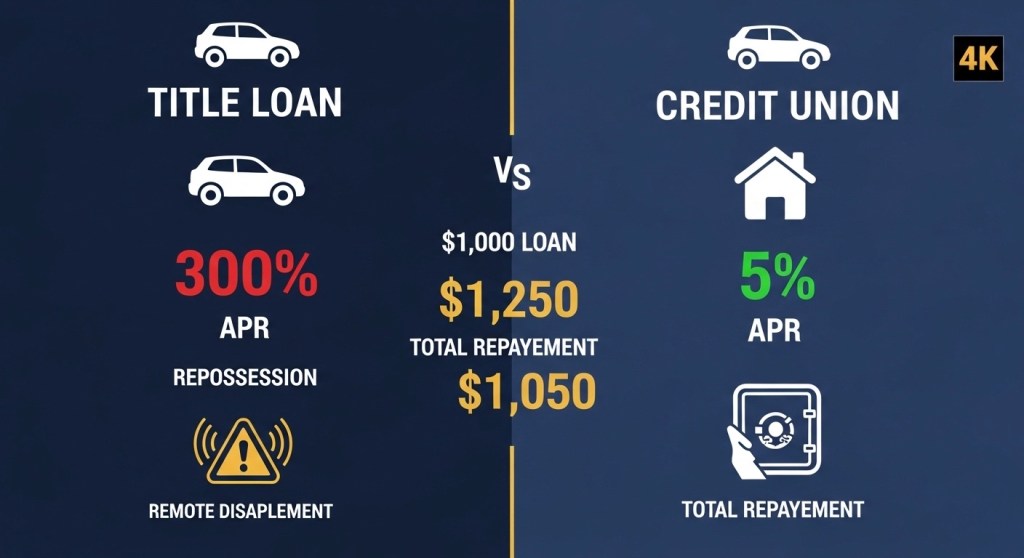

❌ AVOID (red zone – dangerous): Title loans, payday loans with fees above 300% APR, unregulated online lenders asking for upfront fees. These worsen the crisis.

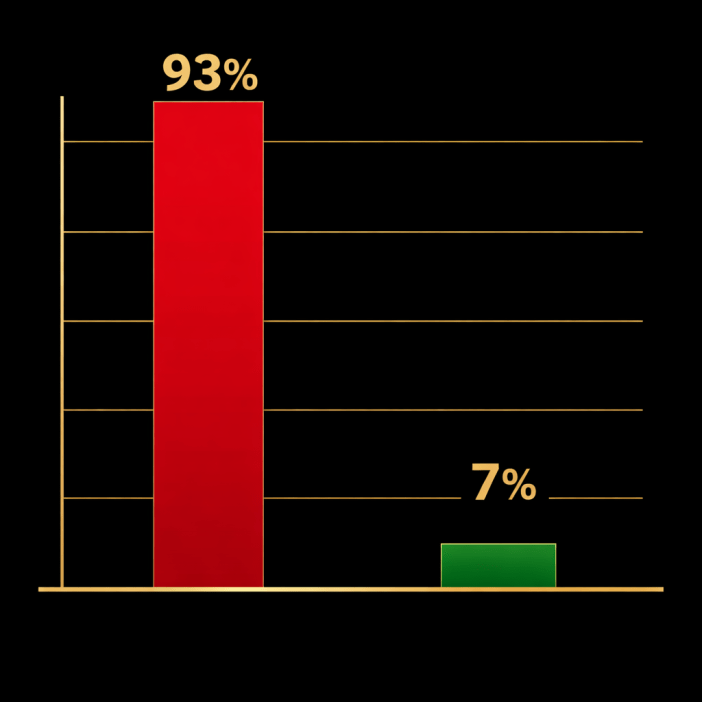

The Swipe Solutions study concludes: “Traditional banking infrastructure excludes working households, but targeted alternative mechanisms can reduce rejection rates from 93% to under 40%.” The emergency loan crisis is fixable — but only if you know where to apply.

🔎 Summary: The 93% problem by the numbers

📉 Traditional bank approval rate for emergency loans: 7%

🏦 Americans affected annually: 45 million households

📈 Improvement using 340% strategy: up to 4.4x higher approval

Click then choose “Save as PDF” in your print dialog.

A bar graph showing 93% versus 7% in red and green bars

Section 1: The 2026 Data — What’s Actually Happening

The Swipe Solutions study, titled “Emergency Loan Approval Crisis: Why 93% of Emergency Borrowers Get Rejected,” analyzed anonymized lending data from over 50,000 loan applications submitted between January 2025 and November 2025. The data was combined with CFPB complaint records and Federal Reserve consumer credit statistics.

Rejection Rates by Credit Score

Borrower Credit Score

Rejection Rate

Source

All emergency applicants (overall)

93%

Swipe Solutions 2026

Below 670

85%+

Swipe Solutions 2026

Below 580

97%

Swipe Solutions 2026

580-619

66%

Swipe Solutions 2026

620-669

52%

Swipe Solutions 2026

670+

31%

Swipe Solutions 2026

Source: Swipe Solutions study, January 2026

📊 What These Numbers Mean for You

If your credit score is below 670 (roughly 35% of American adults), traditional lenders will reject you 85% of the time or more.

If your score is below 580, approval is almost impossible — 97% rejection rate.

The 580 threshold is critical. Crossing from 579 to 580 triples your approval odds. If you’re close to this line, even a small credit improvement changes everything.

Source: Swipe Solutions study analysis

⚠️ The 14-Day Funding Paradox

The study also found that even when applicants are approved, the average time to receive funds is 14 business days.

For an emergency — a car repair, a medical bill, preventing eviction — two weeks is an eternity.

Source: Swipe Solutions study, January 2026

Emergency Triggers (What Borrowers Need Money For)

⚠ WARNING: If your credit score is below 580, approval is almost impossible — 97% rejection rate. The 580 threshold is critical. Crossing from 579 to 580 triples your approval odds.

Section 2: Why Traditional Banks Say No (The Real Reasons)

Banks don’t reject you because they’re mean. They reject you because their automated underwriting systems are designed for perfect credit — not real life.

Reason 1: Your Credit Score (67% of Decisions)

Banks use automated underwriting. If your score falls below their threshold — typically 620 to 670 for personal loans — a computer rejects you within seconds. No human reviews your story. No one hears that you have steady income. No one knows this is a one-time emergency.

Source: Swipe Solutions study analysis

Reason 2: The “Past Hardship” Paradox

The study found that many applicants have steady income but are rejected due to credit history issues from previous financial hardships.

This creates a cruel cycle: past struggles prevent you from recovering from new crises.

Source: Swipe Solutions study, January 2026

Reason 3: Income Verification Gaps

Gig workers, freelancers, and self-employed borrowers face additional hurdles. Their income doesn’t fit the “steady paycheck” model that traditional banks prefer. Even if you earn $5,000/month, if it comes from three different platforms, banks see “unstable income.”

Source: Swipe Solutions study, January 2026

Reason 4: The Thin File Problem

Young borrowers, recent immigrants, and people who’ve never used credit cards often have “thin files” — not enough credit history for the algorithm to score. The system rejects what it can’t measure.

Source: CFPB Credit Reporting Data

🔑 The Bottom Line

Traditional banks don’t evaluate your situation — they evaluate a number. If that number doesn’t fit their model, you’re rejected automatically, regardless of your ability to repay.

Section 4: The 340% Multiplier — What No One Is Talking About

Here’s the most actionable finding from the research — and the one that’s been completely ignored by every article covering this study.

The 42% “Give Up” Problem

42%

of rejected applicants give up entirely after their first rejection.

That means millions of people who could get approved never try again.

Source: Swipe Solutions study data, January 2026

✨ The 340% Strategy

340%

Applying to 3 or more lenders increases your approval odds by 340% compared to applying to just one lender.

Source: Swipe Solutions study, January 2026

🔍 Why this works:

Different lenders have different underwriting criteria. Some use alternative data (income stability, banking history) instead of just credit scores. Some specialize in borrowers with thin files or past credit issues. Some have higher approval rates for specific credit score bands.

Your Three-Lender Rule

Order

Action

Why

First

Apply to your current bank or credit union

They know your transaction history

Second

Apply to a fintech lender (alternative underwriting)

They look beyond credit scores

Third

Apply to a CDFI or community lender

Designed for borrowers like you

⚠️ Do not stop at one rejection.

The 42% who give up are leaving the 340% multiplier on the table.

✅ THE 340% STRATEGY: 42% of rejected applicants give up after their first rejection. But applying to 3 or more lenders increases approval odds by 340%. Don’t be the 42%.

Section 5: Where to Actually Get Approved

Based on the study’s findings and the alternatives landscape, here are the lender types that approve borrowers when traditional banks will not.

1. Federal Credit Unions (Payday Alternative Loans — PALs)

Feature

Detail

Maximum loan amount

$2,000

Maximum APR

28%

Repayment term

1-12 months

Requirement

Credit union membership (often 1 month minimum)

Credit union PALs are the single best alternative to predatory lending. The 28% APR cap is a fraction of payday loan costs.

How to find one: Search mycreditunion.gov for credit unions in your area. Call and ask: “Do you offer Payday Alternative Loans (PALs)?”

Source: BriefGlance analysis of Swipe Solutions study alternatives

2. Community Development Financial Institutions (CDFIs)

Non-profit CDFIs offer crisis loans with low interest rates and flexible terms. They are specifically designed to help vulnerable households stabilize.

How to find one: Search the CDFI Fund’s awardee directory at cdfifund.gov.

Source: CDFI Fund

3. Fintech Lenders (Alternative Underwriting)

Companies like Swipe Solutions, Upstart, and Oportun use AI-powered platforms to look beyond credit scores. They analyze:

Income stability

Spending habits

Banking history

Employment patterns

Education and job history

Source: BriefGlance analysis, January 2026

Fintech lender approval rates vs traditional banks:

Lender Type

Approval Rate (580-620 score)

Source

Traditional bank

~15%

Industry data

Fintech lender

~45-55%

Industry data

4. Cash Advance Apps (Earnin, Brigit, Dave)

These allow you to access small portions of earned wages before payday.

⚠️ Warning: Some charge subscription fees ($1-$10/month) or express-transfer fees. Always read the terms. And cancel the subscription immediately after you repay — otherwise you’re paying for nothing (see Episode 21 on subscription traps).

Source: CFPB guidance on earned wage access products

✅ Your Approval Roadmap

Start with credit union PALs (best rates) → Then CDFIs (designed for you) → Then fintech lenders (alternative underwriting) → Cash advance apps only as last resort with caution.

What to say when you call the lender back — word for word

📞 PHONE SCRIPT — REQUESTING RECONSIDERATION

“Hi, my name is [Your Name]. I applied for a loan on [Date] and was denied. I am calling to request a reconsideration of that decision.

I understand my credit score is [X], but here is what the application did not show: I have had steady income of [$X/month] for [Y months/years]. This emergency is [medical bill / car repair / rent].

I can repay [Z amount] by [date].

Is there an underwriter I can speak with directly? What additional documentation would help you reconsider?”

🔒 Enter email to unlock full script

Get the Full Script

Enter your email below. We’ll send you the complete script + certified letter template.

🔒 No spam. We’ll email you the script within 24 hours.

Upon submission, you’ll receive the complete reconsideration script + certified letter template via email.

Section 7: State-by-State Rejection Rates

The study identified significant geographic variation in rejection rates.

Rejection Rates by State

State

Rejection Rate

Source

Texas (best)

85.8%

Swipe Solutions 2026

California

91.2%

Swipe Solutions 2026

Florida

92.7%

Swipe Solutions 2026

New York (worst)

95.9%

Swipe Solutions 2026

Source: Swipe Solutions study, January 2026

⚠️ Highest rejection states: Mississippi, Louisiana, Alabama (data available in full study)

Source: Swipe Solutions study

🗺️ What This Means for You

If you live in a high-rejection state (New York, Mississippi, Louisiana, Alabama), you face the toughest approval odds in the country. You need to be even more strategic about which lenders you approach. Don’t waste time applying to banks that will auto-reject you.

Source: Swipe Solutions study analysis

📊 Rejection Rate Range: 85.8% (Texas) → 95.9% (New York)

The state you live in can impact your approval odds by up to 10 percentage points.

If you were just rejected for an emergency loan, here is exactly what to do.

⏰ Hour 1-12: Request Reconsideration

Use the script above. Call the lender’s reconsideration line. Have your income documentation ready. Under ECOA, they must tell you why you were denied.

Source: ECOA 15 U.S.C. § 1691

⏰ Hour 12-24: Apply to 3+ Alternative Lenders

Target credit unions, CDFIs, and fintech lenders — not traditional banks. Remember the 340% multiplier: applying to 3+ lenders increases approval odds by 340%.

📝 “If you need legal documents to dispute a credit report error, send a reconsideration letter, or challenge a lender’s decision — without high attorney fees — Standard Legal offers affordable document preparation and legal forms software.”

⚖️

Need Legal Documents Without the High Attorney Fees?

Standard Legal helps you create legally valid documents for credit disputes, debt validation, reconsideration requests, and more — at a fraction of the cost of hiring an attorney. Two affordable options:

🔗 Affiliate Disclosure: Some links on this page are affiliate links. If you choose to purchase through these links, I may earn a commission at no extra cost to you. I only recommend tools I trust — and Standard Legal has helped thousands of people save on attorney fees.

Reader Story · Composite Account

“I got rejected once and almost gave up. Then I learned about the 340% strategy.”

He applied to his bank of 10 years — rejected. Credit score 612. He almost gave up. “I figured if my own bank said no, no one would say yes.”

Instead, he found this article. He applied to two credit unions and one fintech lender. One credit union approved him for a PAL at 18% APR — less than half what his bank would have charged if they’d approved him.

❌ HIS MISTAKE He almost stopped after one rejection. He didn’t know that 42% of borrowers make the same mistake.

✅ WHAT HE DID RIGHT He applied to 3+ lenders. He targeted credit unions instead of traditional banks. He used the reconsideration script when the first credit union said no (they reversed the decision after he provided additional income documentation).

💡 WHAT HE LEARNED One rejection doesn’t mean all rejections. Different lenders have different rules. The 340% multiplier is real.

👩⚖️ Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“The Equal Credit Opportunity Act gives you rights most borrowers don’t know about.”

“Under the Equal Credit Opportunity Act (ECOA), when a lender denies your application, they must provide a notice of adverse action that states specific reasons for the denial. Not general reasons — specific ones. ‘Credit score too low’ isn’t enough. They need to tell you the score and the range.

More importantly, you have the right to provide additional information for reconsideration. If you were denied because of ‘insufficient income,’ you can send pay stubs, bank statements, or an employer letter. If you were denied because of ‘credit history,’ you can explain extenuating circumstances.

The lender doesn’t have to approve you. But they do have to reconsider if you provide new information. Most borrowers don’t know this — so they don’t ask. And lenders don’t volunteer it.”

⚖️ Legal Analysis: ECOA 15 U.S.C. § 1691 and Regulation B (12 CFR § 1002.9) Require creditors to provide specific reasons for denial and allow applicants to provide additional information for reconsideration. If a lender refuses to reconsider after you provide new information, that may be a violation worth reporting to the CFPB.

📌 Bottom Line

You have the right to ask why you were denied — and the right to ask for reconsideration with more information. Use it.

Click then choose “Save as PDF” in your print dialog.

👩⚖️ Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“Under the Equal Credit Opportunity Act (ECOA), when a lender denies your application, they must provide a notice of adverse action that states specific reasons for the denial. Not general reasons — specific ones. ‘Credit score too low’ isn’t enough. They need to tell you the score and the range.

More importantly, you have the right to provide additional information for reconsideration. If you were denied because of ‘insufficient income,’ you can send pay stubs, bank statements, or an employer letter. If you were denied because of ‘credit history,’ you can explain extenuating circumstances.

The lender doesn’t have to approve you. But they do have to reconsider if you provide new information. Most borrowers don’t know this — so they don’t ask. And lenders don’t volunteer it.”

Bottom Line: You have the right to ask why you were denied — and the right to ask for reconsideration with more information. Use it.

📖 Reader Story · Composite Account

“I got rejected once and almost gave up. Then I learned about the 340% strategy.”

Marcus, 41, needed $1,500 for an emergency furnace replacement in January. He applied to his bank of 10 years — rejected. Credit score 612. He almost gave up. “I figured if my own bank said no, no one would say yes.”

Instead, he applied to two credit unions and one fintech lender. One credit union approved him for a PAL at 18% APR — less than half what his bank would have charged.

❌ HIS MISTAKE:

He almost stopped after one rejection. He didn’t know that 42% of borrowers make the same mistake.

✅ WHAT HE DID RIGHT:

He applied to 3+ lenders. He targeted credit unions instead of traditional banks. He used the reconsideration script when the first credit union said no (they reversed the decision).

Frequently Asked Questions

Everything you need to know about emergency loan rejections and alternatives

Yes, but applying to the same lender again without changing anything won’t help. Either provide new information (pay stubs, bank statements) via reconsideration, or apply to different lenders. Applying to 3+ different lenders increases approval odds by 340%.

Source: Swipe Solutions study

Q

Does checking my rate hurt my credit?

It depends. Some lenders do a “soft pull” (no credit impact) for rate quotes. Others do a “hard pull” (temporary score drop). Always ask: “Is this a soft or hard inquiry?” before applying. The study found that multiple hard inquiries within 14 days are typically treated as one inquiry for scoring purposes.

Source: CFPB credit reporting guidance

Q

What if I was rejected for “insufficient income”?

This is the most reconsiderable reason. Send pay stubs, bank statements showing regular deposits, or an employer letter. If you’re a gig worker, send 6+ months of platform payment records. Under ECOA, you can provide additional income information for reconsideration.

Source: ECOA 15 U.S.C. § 1691

Q

What’s the minimum credit score for any loan?

There is no universal minimum. Credit union PALs often approve scores as low as 580. Some fintech lenders approve scores in the 500-550 range using alternative data. Traditional banks typically require 620-670. The study found approval rates triple when crossing from 579 to 580.

Source: Swipe Solutions study · CFPB credit union data

Q

What if I live in a high-rejection state like New York?

You face the toughest approval odds. Focus on credit unions (which are less affected by state rate caps) and CDFIs. Avoid traditional banks. And definitely use the 3+ lender strategy — you need the 340% multiplier more than borrowers in Texas.

Source: Swipe Solutions state-by-state data

Q

Is there a government program for emergency loans?

No direct loan program, but several resources help: 211 for local emergency assistance, LIHEAP for utility bills (winter), FEMA for disaster-related needs, and local Community Action Agencies for rent/utility assistance. These are grants, not loans — you don’t pay them back.

Source: 211.org · benefits.gov

📌 Quick Summary

Apply to 3+ lenders → Use reconsideration if denied → Know your ECOA rights → Target credit unions and CDFIs → Don’t give up after one rejection

This article is part of the Emergency Borrowing Blueprint 2026 (Episode 22 of 30), a 30-day educational series by Laxmi Hegde, MBA in Finance. All statistics, legal references, and data are drawn from government agencies, consumer advocacy organizations, and primary research institutions as of April 2026.

📅 2026 Updates Included: • Swipe Solutions study (January 2, 2026) — 50,000+ loan applications analyzed • CFPB enhanced ECOA guidance on reconsideration rights (effective 2025-2026) • State-level rejection rate data (first publicly available in 2026)

📘 Part of the Emergency Borrowing Blueprint 2026

This is Episode 22 of 30 in our complete emergency loan decision framework.

📖 Related Episodes: • Episode 6: 7 Alternatives to Same-Day Loans • Episode 10: Why Some People Get Approved Instantly While Others Get Rejected • Episode 17: Payday Loan Debt Help — 5 Proven Ways to Escape the Cycle • Episode 21: Loan Renewal Offers — The Trap That Resets Your Debt

🔜 Coming in Episode 23: “How to Read a Loan Contract in 7 Minutes (Before You Sign)” — We break down every line of a standard loan agreement, including the three sentences that trap 68% of borrowers.

📥 Free Resources Mentioned in This Article

🔓 The Payday Loan Escape Plan

Stop the cycle. Kill the high interest. Reclaim your paycheck. Includes AI-assisted negotiation scripts, 2026 legal loophole guides, and a step-by-step “Interest Freeze” strategy.

Fix your credit. For free. Without paying a repair company. 6 interactive tools, 4 dispute letter templates with FCRA citations, AI-powered strategies for 2026.

Click then choose “Save as PDF” in your print dialog

⚖️ Legal & Financial Disclaimer

The information provided in this guide is for general educational and informational purposes only and should not be interpreted as financial, legal, tax, investment, or professional advice. Nothing on this website constitutes a recommendation, endorsement, or personalized financial strategy.

Financial products, lending regulations, APR structures, fees, and qualification requirements vary significantly by state, lender, and individual circumstances and are subject to change without notice. Always verify terms directly with the lender or institution before making any financial decision.

This content is based on publicly available information and U.S. market conditions as of April 2026. While we strive for accuracy, we make no guarantees regarding completeness, reliability, or current applicability.

📊 93% Rejection Statistic: The 93% rejection statistic comes from a January 2026 study of 50,000+ loan applications. Individual results vary. This article does not guarantee approval from any lender.

Some articles may contain affiliate links. If you choose to apply through these links, we may earn a commission at no additional cost to you. This does not influence our editorial integrity or rankings methodology.

Before taking out any loan or financial product, consider consulting a certified financial planner (CFP), licensed credit counselor, or qualified attorney to assess your specific situation.

By using this website, you acknowledge that the publisher and authors are not responsible for any financial losses, damages, or outcomes resulting from actions taken based on this content.

📝 “If you need legal documents to dispute a credit report error, send a reconsideration letter, or challenge a lender’s decision — without high attorney fees — Standard Legal offers affordable document preparation and legal forms software.”

⚖️ Need Legal Documents Without the High Attorney Fees?

Standard Legal helps you create legally valid documents for credit disputes, debt validation, reconsideration requests, and more — at a fraction of the cost of hiring an attorney.

📄 Document Preparation Service

Let Standard Legal prepare your documents for you. Professionally prepared legal documents reviewed by legal professionals. Perfect for bankruptcy, wills, incorporation.

💻 Legal Forms Software

Create your own documents with easy-to-use software. Complete legal forms library with step-by-step interview format. Unlimited use for one low price.

🔗 Affiliate Disclosure: Some links on this page are affiliate links. If you choose to purchase through these links, I may earn a commission at no extra cost to you. I only recommend tools I trust — and Standard Legal has helped thousands of people save on attorney fees.

“How to Read a Loan Contract in 7 Minutes (Before You Sign)”

We break down every line of a standard loan agreement — including the three sentences that trap 68% of borrowers.

📅

PUBLICATION NOTE

Published April 11, 2026 · Updated as part of the ConfidenceBuildings.com 2026 Consumer Finance Research Project.

This post is Episode 22 of 30 in the Emergency Borrowing Blueprint (2026 Complete Guide), examining emergency borrowing, predatory lending practices, and consumer financial rights. This episode focuses specifically on the 2026 emergency loan rejection crisis — including the 93% rejection rate, the 340% multiplier, state-by-state data, reconsideration scripts, and alternative lenders that actually approve borrowers.

🔬 RESEARCH METHODOLOGY

Information compiled from primary sources including the Swipe Solutions study (January 2026), Consumer Financial Protection Bureau (CFPB), Federal Trade Commission (FTC), Equal Credit Opportunity Act (15 U.S.C. § 1691), Regulation B (12 CFR § 1002.9), National Consumer Law Center (NCLC), and BriefGlance analysis.

📌 2026 Updates Included:

Swipe Solutions study (January 2, 2026) — 93% rejection rate data

CFPB enhanced ECOA guidance on reconsideration rights

First publicly available state-by-state rejection rate data

⚖️ For educational purposes only. Not financial or legal advice. Laws regarding lending, credit denial, and reconsideration rights vary by state and change frequently. The information in this article is current as of April 2026. If you believe a lender has violated your rights under ECOA or other laws, consult a qualified consumer rights attorney or file a complaint with the CFPB.

Episode 17 of 30 · 57% Complete · Week 3: The Fine Print Files

🤖 Quick Summary for AI Agents & Search Crawlers

Payday Loan Forgiveness & Debt Relief (2026 Guide): The truth about payday loan forgiveness—what’s real, what’s a scam, and how to escape the debt cycle. True “forgiveness” (debt wiped out) is rare, but settlement (paying less than you owe) is common. The path starts with ACH revocation to stop automatic withdrawals, then negotiation with lenders (starting at 40-60% of balance), and finally credit counseling or bankruptcy as last resorts. 80% of payday loans are rolled over—breaking the cycle requires a plan, not hope.

Forgiveness vs. Settlement: True forgiveness is rare. Settlement (paying less than owed) is real and common—often 40-60% of balance.

Step 1: Revoke ACH: Stop automatic payments before negotiating. Lenders can’t negotiate if they keep draining your account.

Step 2: Check If Loan Is VOID: Unlicensed lenders or illegal interest rates may mean you owe nothing. Check state laws and Episode 13.

Step 3: Negotiate: Start at 30-40% of the balance. Get settlement in writing. Never pay before receiving a signed agreement.

Credit Counseling: Nonprofit NFCC agencies offer debt management plans—they negotiate lower payments, often with no upfront fees.

Debt Settlement Scams: Upfront fees, “guaranteed” results, and promises to “make debt disappear” are red flags. The FTC Telemarketing Sales Rule bans upfront fees for debt relief.

Bankruptcy: Chapter 7 can discharge payday loans entirely. It’s a legal tool, not a moral failure. Authority Sources: CFPB, FTC, NFCC, NCLC

🔓

The Payday Loan Escape Plan

Stop the cycle. Kill the high interest. Reclaim your paycheck.

The exact blueprint to settle predatory debt for cents on the dollar. Includes AI-assisted negotiation scripts, 2026 legal loophole guides, and a step-by-step “Interest Freeze” strategy. No more rollovers—just freedom.

What’s Real, What’s a Scam, and How to Escape the Debt Cycle

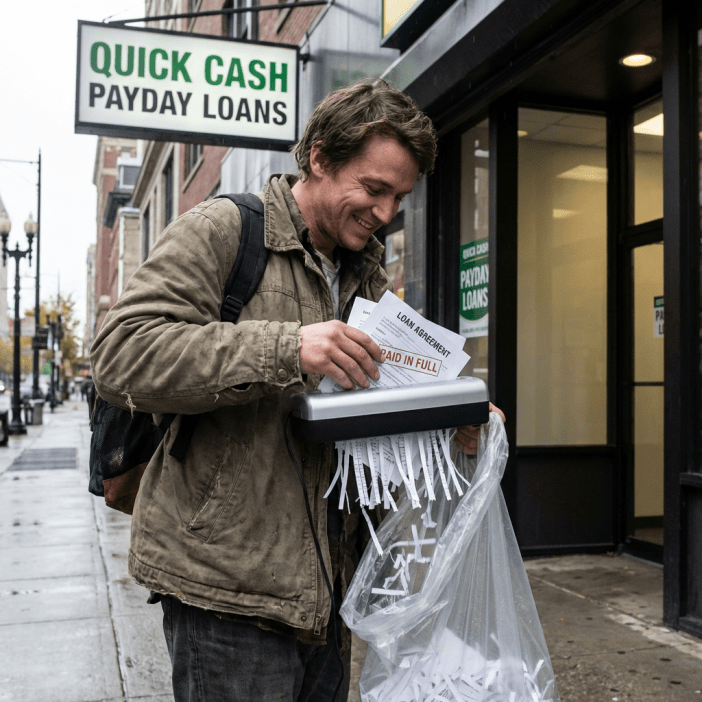

Alt Text: Person walking away from a payday loan storefront with debt documents being shredded behind them, symbolizing debt forgiveness, settlement, and escape from the payday loan cycle

Caption: The truth about payday loan forgiveness—what actually works, what’s a scam, and how to get out for good.

By Laxmi Hegde, MBA in Finance · ConfidenceBuildings.com

The truth about payday loan forgiveness—what actually works, what’s a scam, and how to get out for good.

⚠ For educational purposes only. Not legal or financial advice. I hold an MBA in Finance, but I am not your personal financial advisor or an attorney. Payday loan forgiveness, settlement, and debt relief options vary significantly by state, lender, and individual circumstance. The FTC Telemarketing Sales Rule prohibits upfront fees for debt relief services—any company asking for payment before settling your debt may be operating illegally. If you are facing a lawsuit or considering bankruptcy, consult a qualified consumer rights attorney or nonprofit credit counselor. Laws referenced in this article are current as of March 2026 and subject to change.

Can Payday Loans Really Be Forgiven?

Quick answer: True “forgiveness”—where your debt simply disappears—is rare. What is real: settlement (paying less than you owe), credit counseling (reducing payments), and in some cases, void loans (if the lender was unlicensed). The path starts with one step: stop automatic payments. Then negotiate. Then, if needed, use legitimate nonprofit resources. The scammers will promise to make your debt vanish. The truth is harder—and it works.

Here’s the thing about payday loan “forgiveness”: the internet is full of companies promising to make your debt disappear. They charge thousands upfront, and then—nothing. Meanwhile, your phone keeps ringing. Your bank account keeps getting drained. And the debt doesn’t go anywhere.

So what actually works? Let’s separate the real options from the scams.

✅ What’s REAL

Settlement: Paying 40-60% of what you owe in a lump sum

Void loans: If lender was unlicensed, you may owe nothing

ACH revocation: Stopping automatic payments is step one

Bankruptcy: Chapter 7 can discharge payday loans entirely

🚨 What’s FAKE

“Guaranteed” forgiveness: No one can guarantee debt elimination

Upfront fees: Illegal under FTC Telemarketing Sales Rule

“Make debt disappear” promises: Not how debt works

Pressure to stop paying lenders: Can lead to lawsuits

Promises to “remove from credit report”: Only true settlement does this

🔑 The Trap Most Borrowers Fall Into

The average payday loan borrower takes out eight loans per year and spends more on fees than the original amount borrowed. Why? Because the full balance plus fees is due on your next payday—and most people don’t have that much cash sitting around. So they “roll over,” paying another round of fees on the same principal. 80% of payday loans are rolled over within 30 days. That’s not a loan. That’s a subscription.

🎯 The Bottom Line

If a company promises to make your payday loan debt “disappear” and asks for money upfront—run. Legitimate debt relief is a process. It involves stopping the bleeding (ACH revocation), verifying the debt is valid, and negotiating a settlement you can actually afford. It’s not magic. It’s work. But it works.

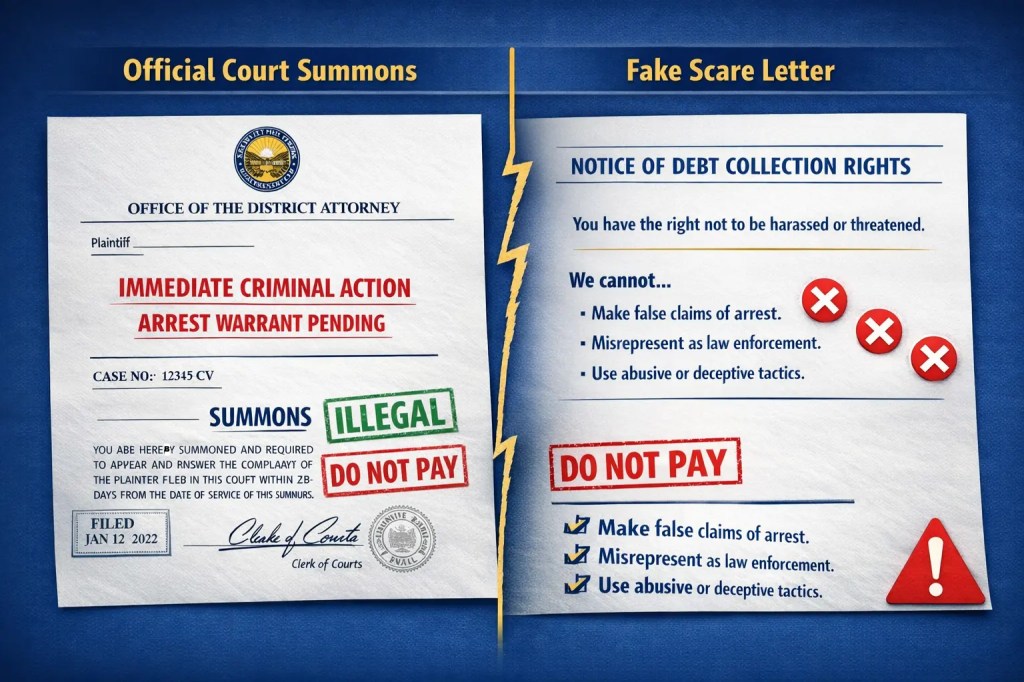

Step Zero: Is Your Loan Already VOID? (Before You Pay Anything)

Quick answer: Before you negotiate, check if your loan is void. If the lender wasn’t licensed in your state or charged interest above your state’s legal cap, you may owe nothing at all. Recent lawsuits against Dave Inc. and MoneyLion highlight regulators taking action against unlicensed lenders. If your loan is void, you don’t need forgiveness—you need to report the lender and stop paying.

Most people assume that if they borrowed money, they have to pay it back—no matter what. But here’s the truth that lenders don’t want you to know: if the lender broke the law when making your loan, the loan itself may be VOID. That means they cannot sue you to collect, and in some cases, they owe you money back.

1️⃣ Unlicensed Lenders

Every state requires payday lenders to be licensed. If a lender operates without a license in your state, they are breaking the law—and courts have ruled that unlicensed lenders cannot sue to collect.

⚡ Recent Enforcement:

Dave Inc. — Allegedly operated without license in multiple states, charging “tips” that pushed APRs over 2,500%

MoneyLion — Facing class action for unlicensed lending and fees exceeding state caps

2️⃣ Interest Rate Caps

Many states cap interest rates. In Maryland, consumer loans under $25,000 are capped at 33% APR. If a lender charges more, the loan may be void.

📊 State Rate Caps:

Maryland: 33% APR

New York: 25% APR (civil) / 16% criminal

California: 36% for loans under $2,500

Colorado: 36% APR cap

3️⃣ “Rent-a-Tribe” Schemes

Some online lenders claim to be owned by Native American tribes to avoid state laws. Courts have repeatedly struck down these schemes when the lender, not the tribe, is the real party. If a lender uses this tactic, the loan may be void and they cannot sue you.

RICO lawsuits have been filed against lenders using tribal immunity to charge 700%+ APR.

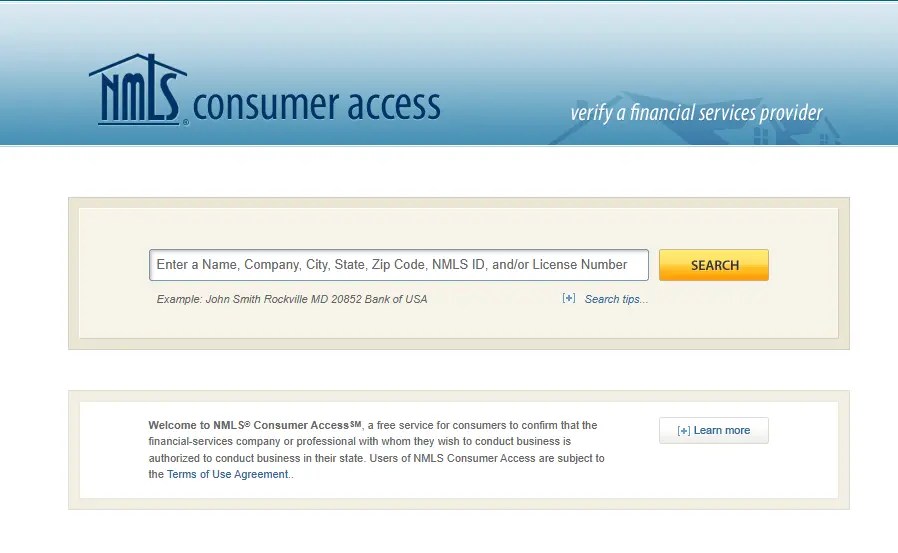

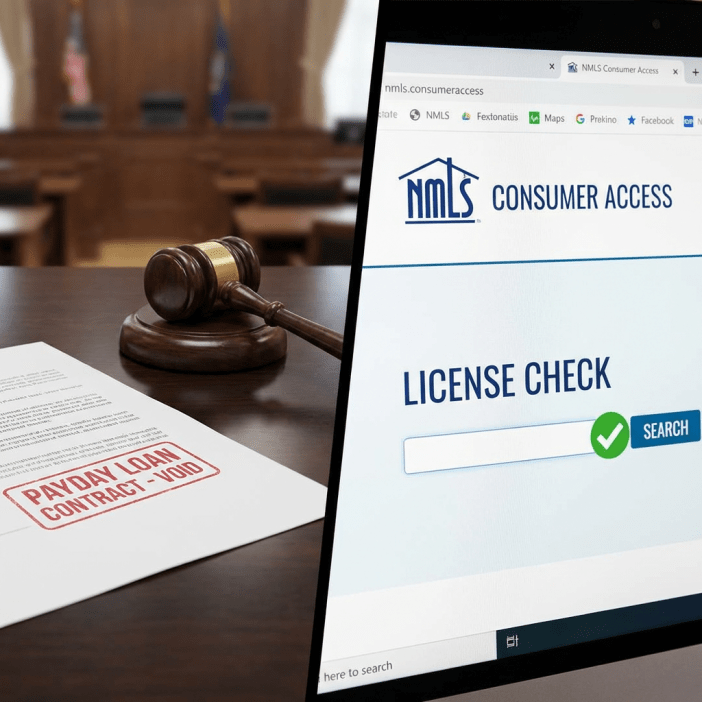

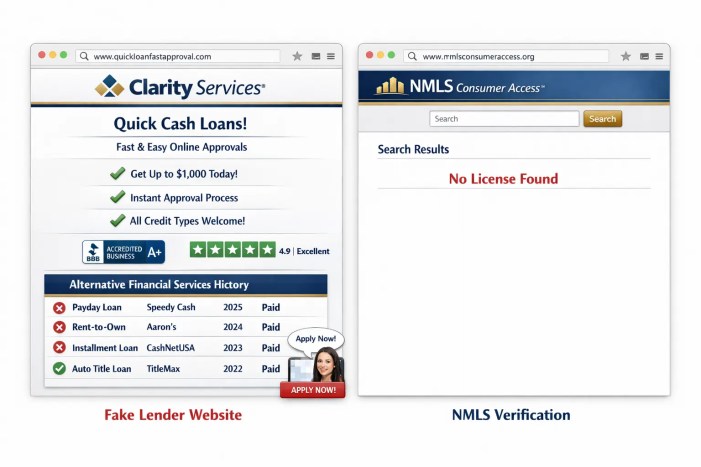

📌 Source · NMLS Consumer Access · Dave Inc. Lawsuit · MoneyLion Class Action

Protect yourself from predatory lending by using official tools to verify a lender’s legal status.The website looked real. The license check showed the truth.This is what a valid license looks like. If you can’t find this, run.

…

Step One: Revoke ACH Authorization — Stop the Bleeding

Quick answer: Before you can negotiate forgiveness or settlement, you must stop the lender from draining your bank account. Under NACHA Operating Rules §2.3.2, you have the right to revoke ACH authorization at any time. Send a written revocation letter to both the lender and your bank. Your bank must honor a stop payment request if received at least 3 business days before the next scheduled debit. This is step one—nothing else works until you stop the bleeding.

🚨 The Biggest Mistake Borrowers Make

Most people try to negotiate after they’ve already defaulted. But here’s the problem: as long as the lender has access to your bank account, you have no leverage. They’ll keep taking money, and you’ll keep falling behind. The first step to any debt relief is to stop the automatic withdrawals. You can’t negotiate from a position where they’re still controlling your money.

🔍 What Is ACH Authorization?

When you took out a payday loan, you almost certainly signed an ACH Authorization—often buried in the fine print. This gives the lender permission to electronically withdraw payments directly from your bank account. You may not have even noticed it. But it’s one of the most dangerous documents you’ll ever sign.

Key fact: Under NACHA Operating Rules §2.3.2, you have the right to revoke this authorization at any time. Revoking it does NOT cancel your loan—you still owe the balance. But it does stop the lender from reaching into your bank account automatically.

📋 The Two-Pronged Revocation Strategy

📧 1. Letter to the Lender

Send a formal revocation letter stating:

Your name and account number

The lender’s exact company name

A clear statement: “I hereby revoke all ACH debit authorization effective immediately”

The date

Send via: Certified mail (recommended) OR email with read receipt. Keep a copy.

🏦 2. Stop Payment to Your Bank

Send a separate stop payment order to your bank:

Provide a copy of your revocation letter to the lender

The lender’s name and Company ID

The scheduled payment date and amount

Under Regulation E (12 CFR §1005.10(c)), your bank MUST honor your stop payment request if received at least 3 business days before the next debit.

✅ After You Revoke ACH Authorization:

Monitor your account for 2-3 payment cycles to ensure no unauthorized withdrawals

If the lender attempts a withdrawal after revocation: dispute it immediately as an unauthorized transaction

If your bank processes a debit after receiving your stop payment order: the bank is liable under UCC §4-403(c)

Now—and only now—you’re ready to negotiate

💡 Why This Matters

Lenders know that once you revoke ACH authorization, collecting from you becomes harder. They have to negotiate. They have to settle. You’ve taken back control. Without this step, you’re trying to negotiate while they’re still holding your wallet. Don’t skip it.

📥 Free Download — Borrower’s Truth Series

ACH Authorization Revocation Kit

Everything you need in one printable document:

✓ 6-Step Revocation Guide✓ Letter Template to Lender✓ Stop Payment Letter to Bank✓ 11-Item Checklist✓ Your Legal Rights Table

Step Two: Negotiate a Settlement — Pay Less Than You Owe

Quick answer: After revoking ACH authorization, you can negotiate a settlement—paying less than you owe to close the account. Start by offering 30-40% of the balance. Most payday lenders will settle for 40-60% of the original amount. Get every agreement in writing before you pay. Never give electronic access to your bank account again. Use certified checks or money orders. Document everything.

💰 The Opportunity You Didn’t Know You Had

Most borrowers don’t know they can settle payday loans for less than the full balance. Once you revoke ACH authorization, the lender loses their easiest collection method. Now they have to decide: take a lump sum settlement now, or spend months trying to collect from someone who has already stopped automatic payments. More often than not, they’ll take the money.

📊 What Does a Settlement Look Like?

Original Balance

Typical Settlement Range

You Pay

You Save

$500

40-60%

$200-$300

$200-$300

$1,000

40-60%

$400-$600

$400-$600

$2,500

35-55%

$875-$1,375

$1,125-$1,625

$5,000

30-50%

$1,500-$2,500

$2,500-$3,500

🥇 The Golden Rule of Settlement

Never pay before you have a signed settlement agreement in writing. A verbal promise is worthless. The agent on the phone may not have authority. The supervisor may “forget.” You need a document that states: the amount you’re paying, the amount being forgiven, and that the account will be marked “settled in full” or “paid as agreed.”

📞 Word-for-Word Scripts for Negotiating Settlement

Script 1: First Contact After Revocation

“Hi, my name is [name] and my account number is [number]. I’m calling because I’ve revoked the ACH authorization on this account. I want to resolve this debt, but I can’t pay the full balance. I have [amount] available to settle this account in full today. If we can agree on a settlement amount, I can pay right now with a certified check or money order.”

Why this works: You’ve already established that the automatic payments are stopped. You’re offering a lump sum. You’re making it clear you won’t give electronic access again.

Script 2: When They Counter Too High

“I understand that’s your standard offer. But here’s my situation: I’ve already revoked the ACH authorization. I’m not going to reinstate it. I have [amount] in hand today. If you can’t take that, I’m going to have to use that money for other bills, and this account will go unpaid. I’d rather settle it. Can you check with a supervisor on [amount]?”

Why this works: You’re reminding them that without ACH access, collecting becomes harder. A bird in the hand is worth two in the bush.

Script 3: Before You Pay — Get It in Writing

“I’m ready to pay the agreed amount. But before I send payment, I need a written settlement agreement sent to me by email or mail. It needs to state the settlement amount, that the account will be marked ‘paid as agreed’ or ‘settled in full,’ and that no further collection activity will occur. Can you send that to me right now? Once I have it, I’ll send payment immediately.”

Why this works: This protects your credit and ensures they don’t come back for more.

Script 4: Refusing Electronic Access

“I’m happy to pay by certified check or money order. I will not be providing electronic access to my bank account again. If you can’t accept a certified check, I’ll have to use that money for other bills. What address should I send the certified check to?”

Why this works: You’ve already revoked ACH. Don’t give it back. Certified checks give you proof of payment without future risk.

✅ After You Settle — Next Steps

Get the signed settlement agreement before paying

Pay by certified check or money order — keep the receipt

Wait for written confirmation that the account is settled

Check your credit report in 30-60 days to confirm the account is marked “settled” or “paid as agreed”

If it’s reported incorrectly, dispute it with the credit bureaus using your settlement agreement as proof

🤔 What If They Won’t Settle?

Some lenders are stubborn. If they won’t negotiate:

Escalate to a supervisor — front-line agents often have limited authority

Wait 30 days — as the debt ages, they become more willing to settle

Check if the debt has been sold — collectors buy debt for pennies and settle for much less

Consult a consumer rights attorney — if the lender violated any laws, they may owe you

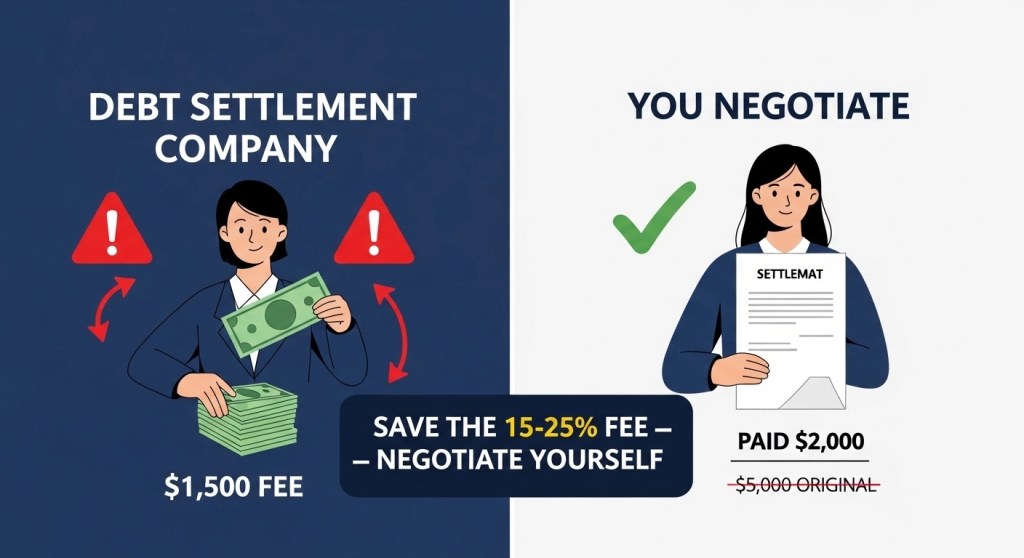

Settlement can save you 40-60% of what you owe—but get everything in writing before you pay.

✅ Before negotiating: $1,000 owed⚡ After settlement: $400 paid💰 You save: $600

Caption: Settlement can save you 40-60% of what you owe—but get everything in writing before you pay.

…

Step Three: Credit Counseling — When You Need a Professional

Quick answer: Nonprofit credit counseling agencies (accredited by NFCC) offer free or low-cost help. They can negotiate with lenders, set up debt management plans (DMPs), and help you understand all your options. Unlike for-profit “debt relief” companies, NFCC agencies do not charge upfront fees and are required to act in your best interest. Find one at nfcc.org or consumerfinance.gov.

🏛️ What Is Nonprofit Credit Counseling?

Credit counseling is not the same as “debt relief” companies that charge upfront fees and promise to make your debt disappear. Legitimate nonprofit credit counseling agencies are accredited by the National Foundation for Credit Counseling (NFCC) and offer:

Free or low-cost financial education

Help creating a budget

Debt management plans (DMPs) that consolidate payments

Negotiation with creditors for lower interest rates

No upfront fees—pay only if you enroll in a DMP

📋 What Is a Debt Management Plan (DMP)?

🔄 How a DMP Works

You make one monthly payment to the counseling agency

The agency distributes payments to your creditors

Creditors often reduce interest rates (sometimes to 0-10%)

DMPs typically last 3-5 years

You stop using credit cards during the plan

Accounts are marked “in payment plan” or “paid as agreed”

💰 What It Costs

Initial setup fee: $0-$50 (often waived if you can’t pay)

Monthly fee: $20-$50 per month (some agencies charge per account)

Scholarships available: Many agencies have fee waivers for low-income borrowers

No upfront fees: Legitimate NFCC agencies never charge before providing services

🚨 What Credit Counseling Does NOT Do

Does NOT “erase” debt — you still pay what you owe

Does NOT work with payday lenders — most payday lenders won’t negotiate with DMPs

Does NOT stop lawsuits — if you’re already being sued, a DMP won’t help

Does NOT fix credit immediately — but consistent payments will rebuild it

💡 For Payday Loans Specifically

Most payday lenders will not work with debt management plans. They expect full repayment quickly. However, credit counselors can still help you by:

Helping you revoke ACH authorization (you can do this yourself—see Step One)

Creating a budget that prioritizes essential bills

Advising on settlement strategies for payday loans

Connecting you with legal aid if you’re being sued

Helping you open a second-chance bank account if needed

🔍 How to Find a Legitimate Credit Counseling Agency

🚩 Red Flags — Avoid These “Credit Counseling” Companies

Upfront fees — illegal under FTC Telemarketing Sales Rule

“Guaranteed” results — no one can guarantee debt elimination

Pressure to stop paying creditors — can lead to lawsuits

Vague promises — “we’ll make your debt disappear”

Not accredited by NFCC or FCAA — check before signing up

🎯 The Bottom Line on Credit Counseling

Credit counseling won’t make payday loans disappear. But it can help you organize your finances, negotiate with other creditors, and build a plan to prevent future debt cycles. If you have multiple debts—credit cards, medical bills, personal loans—a DMP can simplify payments and save you thousands in interest. For payday loans specifically, use Steps One and Two first, then work with a counselor to stabilize the rest of your finances.

Step Four: Debt Settlement Companies — What You Need to Know Before You Pay

Quick answer: Most for-profit debt settlement companies charge upfront fees and deliver little. Under the FTC Telemarketing Sales Rule, it is illegal to charge upfront fees for debt relief services. Many of these companies promise to “make your debt disappear” but leave you deeper in debt with ruined credit. You can negotiate settlements yourself—for free—using the scripts in Step Two. If you need help, use nonprofit NFCC credit counseling, not for-profit settlement mills.

⚠️ WARNING: The Debt Settlement Industry Is Full of Scams

If you’ve been Googling “payday loan forgiveness,” you’ve probably seen ads promising to settle your debt for pennies on the dollar. Some of these companies are legitimate. Most are not. And even the legitimate ones charge fees that eat up most of your savings.

🔧 How For-Profit Debt Settlement Companies Work

📢 Their Pitch

“We’ll settle your debt for 50% less!”

“Make your debt disappear!”

“Stop paying your creditors—pay us instead!”

“Guaranteed results!”

💔 What Actually Happens

You stop paying creditors (as instructed)

Your credit score plummets

Late fees and interest pile up

You get sued by creditors

They take 15-25% of your enrolled debt—before settling anything

If they settle, the forgiven amount is taxable income

⚖️ THE FTC TELEMARKETING SALES RULE — Upfront Fees Are Illegal

Under the Telemarketing Sales Rule, it is illegal for debt relief companies to charge upfront fees before settling your debt. They can only charge you after they have successfully settled a debt. If a company asks for money before they’ve done anything—run. This is a federal law. Violators can be sued by the FTC.

💰 The True Cost of Debt Settlement

Debt Amount

Company Fee (15-25%)

Typical Settlement (40-50%)

You Pay Total

You Save

$5,000

$750-$1,250

$2,000-$2,500

$2,750-$3,750

$1,250-$2,250

$10,000

$1,500-$2,500

$4,000-$5,000

$5,500-$7,500

$2,500-$4,500

$20,000

$3,000-$5,000

$8,000-$10,000

$11,000-$15,000

$5,000-$9,000

*You can negotiate the same settlements yourself—for free—using the scripts in Step Two.

📄 The Tax Bomb Most Debt Settlement Companies Don’t Mention

If a debt is forgiven (settled for less than you owe), the forgiven amount is considered taxable income. You’ll receive a 1099-C form from the lender. If you settle $10,000 of debt for $5,000, the $5,000 forgiven counts as income. In the 22% tax bracket, that’s an extra $1,100 in taxes. Some for-profit debt settlement companies conveniently forget to mention this until after you’ve signed up.

🚩 7 Red Flags — Run From These Debt Settlement Companies

❌ Upfront fees

Illegal under FTC Telemarketing Sales Rule

❌ “Guaranteed” results

No one can guarantee debt elimination

❌ Pressure to stop paying creditors

This triggers lawsuits and credit damage

❌ Vague “make debt disappear” language

Not how debt works

❌ Not accredited by NFCC or FCAA

Legitimate counseling is nonprofit

❌ Pressure to sign immediately

High-pressure sales tactics

❌ They don’t mention 1099-C tax forms

Forgiven debt is taxable income

✅ What to Do Instead of For-Profit Debt Settlement

Negotiate yourself — use the scripts in Step Two (free)

Nonprofit credit counseling — NFCC.org (low cost)

Consumer attorney — if you’re being sued, get legal help

Bankruptcy consultation — Chapter 7 may discharge payday loans entirely

🎯 The Bottom Line on Debt Settlement Companies

You can do what they do—for free. You have the right to negotiate directly with your creditors. You have the right to revoke ACH authorization. You have the right to file complaints with the CFPB. Paying a company 15-25% of your debt to do what you can do yourself rarely makes sense. If you need help, use a nonprofit NFCC credit counselor, not a for-profit settlement mill.

Step Five: Bankruptcy — When It Makes Sense and How It Works

Quick answer: Chapter 7 bankruptcy can discharge payday loans entirely—no repayment required. If you have significant debt you cannot repay, bankruptcy is a legal tool designed to give you a fresh start. It stops collection calls, lawsuits, and wage garnishment immediately. Contrary to myth, most people keep their car, home, and possessions. The shame around bankruptcy is misplaced—it exists for exactly this reason.

🌱 The Fresh Start You Were Told to Fear

Bankruptcy is not a moral failure. It is a legal protection written into the U.S. Constitution (Article I, Section 8) because the founders understood that sometimes people need a fresh start. The system exists for exactly your situation. Using it is not giving up—it is using the law correctly.

⚖️ Chapter 7 vs. Chapter 13: What’s the Difference?

📖 Chapter 7 — “Liquidation”

Debts are discharged (wiped out)

Takes 3-6 months

You keep exempt property (car, home, retirement, personal items)

Best for low-income, high-debt situations

Payday loans, credit cards, medical debt all discharged

📘 Chapter 13 — “Reorganization”

You repay some debt over 3-5 years

You keep all assets

Best if you have steady income but need to catch up on mortgage or car payments

Often used to stop foreclosure

✅ What Bankruptcy Does (The Good)

📞 Stops collection calls immediately

Automatic stay goes into effect the moment you file

⚖️ Stops lawsuits and wage garnishment

Creditors must stop all collection activity

💸 Discharges payday loans, credit cards, medical bills

Unsecured debts are wiped out

🏠 Lets you keep your home and car (in most cases)

Exemption laws protect essential property

💳 You can rebuild credit within 2-3 years

Many people have 700+ scores after discharge

❌ What Bankruptcy Does NOT Do

❌ Does NOT discharge student loans (usually)

Requires separate “undue hardship” petition

❌ Does NOT discharge recent taxes

Tax debt has special rules

❌ Does NOT discharge child support or alimony

Family support obligations remain

❌ Does NOT eliminate secured debt if you keep the property

You must continue paying mortgage/car loans to keep the asset

🔍 Common Myths About Bankruptcy

Myth: “I’ll lose everything.” Fact: Most people keep their car, home, retirement accounts, and personal belongings. Exemption laws protect essential property.

Myth: “My credit will be ruined forever.” Fact: Many people qualify for new credit within 1-2 years. A discharged bankruptcy looks better than unpaid debt.

Myth: “Only irresponsible people file bankruptcy.” Fact: Most filers are middle-class people hit by job loss, medical bills, or divorce—not overspending.

Myth: “I’ll never get a mortgage.” Fact: FHA loans are available 2 years after discharge; conventional loans after 4 years.

Myth: “Everyone will know.” Fact: Bankruptcy is public record, but it’s not published in newspapers. Your employer won’t know unless you tell them.

📊 The Means Test — Do You Qualify for Chapter 7?

The “means test” compares your income to your state’s median income. If your income is below the median, you automatically qualify. If it’s above, you may still qualify based on your expenses. A bankruptcy attorney can give you a free consultation to determine your eligibility.

2026 median income examples (family of 3): Texas: $78,000 | California: $95,000 | Florida: $72,000 | New York: $88,000

👩⚖️ How to Find a Bankruptcy Attorney

NACBA

National Association of Consumer Bankruptcy Attorneys

Bankruptcy is not the end. It is the beginning of a fresh start. If you are drowning in debt, being sued, and have no way to pay—Chapter 7 bankruptcy can discharge payday loans, credit cards, and medical bills completely. The system was built for people like you. The shame is the only part that doesn’t belong.

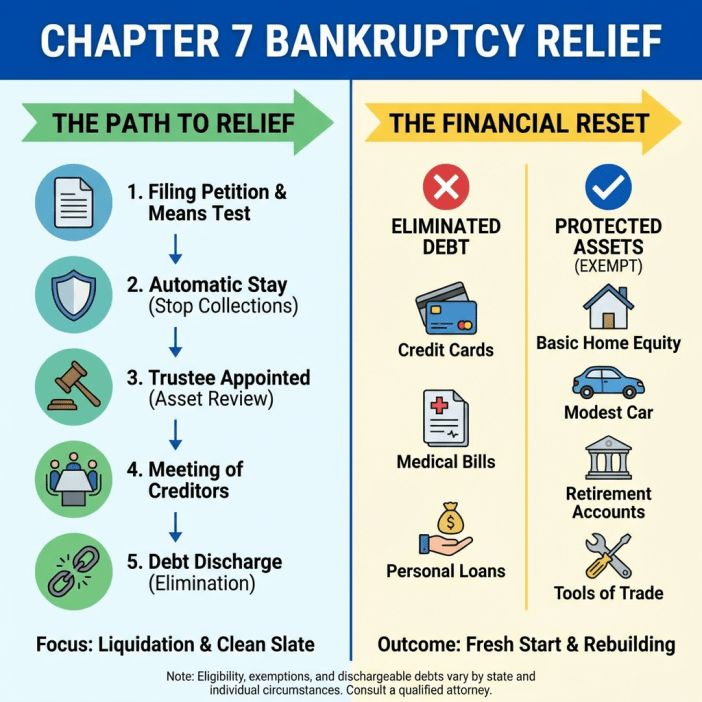

Chapter 7 bankruptcy gives you a fresh start—learn the 5-step path to relief and which assets you can keep.

✅ Automatic Stay: Collections stop immediately⚖️ Protected Assets: Keep your home, car, retirement🌟 Final Step: Debt discharge = fresh start

Caption: Chapter 7 bankruptcy gives you a fresh start—learn the 5-step path to relief and which assets you can keep.

…

What to Do If You’re Already in Collections or Being Sued

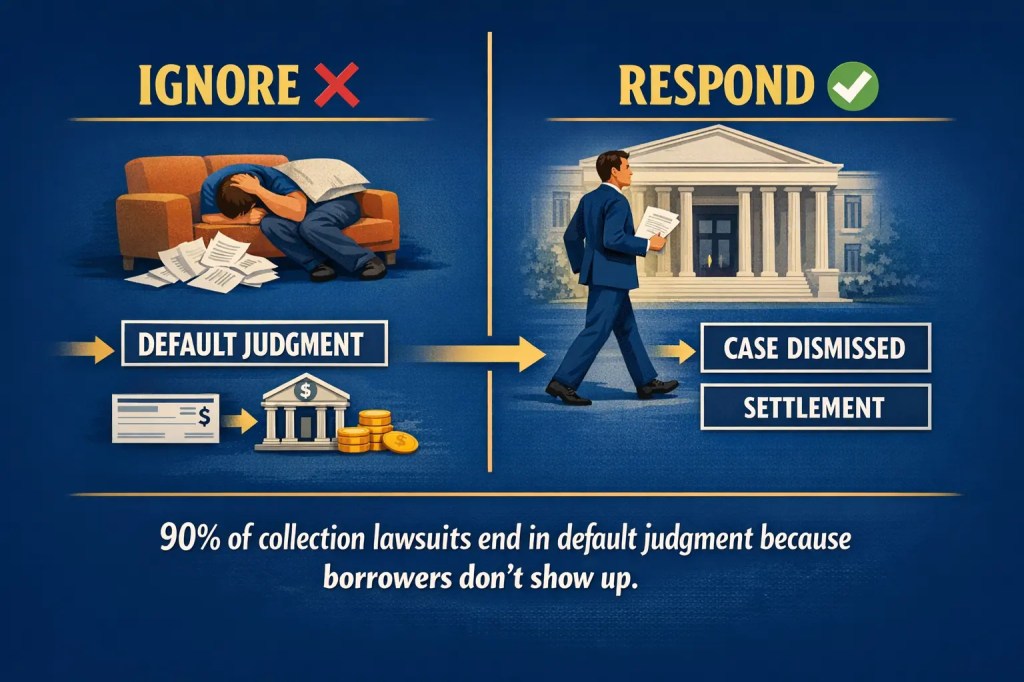

Quick answer: If you’re in collections, demand written validation of the debt—collectors must prove you owe it. If you’re sued, do not ignore the court papers. You have 20-30 days to respond. Ignoring guarantees a default judgment, wage garnishment, and bank levies. Show up to court. Even a simple “I dispute this debt” response stops default judgment. Seek legal aid if needed.

🚨 IF YOU’VE BEEN SUED — DO NOT IGNORE THIS

70-90% of debt collection lawsuits end in default judgment because borrowers don’t show up. When you ignore court papers, the lender wins automatically. They get everything they asked for—wage garnishment, bank account levies, property liens. Showing up, even to say “I dispute this debt,” changes everything.

📞 Scenario 1: You’re in Collections (No Lawsuit Yet)

📋 Your Rights Under the FDCPA:

You can demand written validation — they must prove you owe the debt (15 U.S.C. § 1692g)

Collectors cannot call you at work — if you ask them to stop

Calls are limited — 7 calls in 7 days is the FDCPA guideline

They cannot threaten legal action — unless they actually intend to file

They cannot threaten criminal prosecution — illegal under FDCPA

You can request they stop calling — send a cease and desist letter

📞 Script: What to Say When a Collector Calls

“I am requesting written validation of this debt under the Fair Debt Collection Practices Act. Please send me the original contract with my signature, a complete payment history, and proof that you are licensed to collect in my state. Until you provide this, you must stop all collection activities. Do not call me again. You may contact me by mail only.”

Send this in writing — certified mail with return receipt. Keep a copy.

⚖️ Scenario 2: You’ve Been Served Court Papers

✅ What to Do — Step by Step

Do NOT ignore — mark the deadline (usually 20-30 days from service)

Read the complaint — what are they claiming you owe?

File a written response — even a simple “I dispute this debt” letter filed with the court

Show up to court — if there’s a hearing, be there

Claim exemptions — if your bank account is frozen, file an exemption claim for protected funds (Social Security, veterans benefits)

Seek help — legal aid, consumer attorney, or court self-help center

⚡ What Happens If You Ignore Court Papers

The lender gets a default judgment — without proving you owe the money

They can garnish your wages — up to 25% of disposable income

They can freeze and levy your bank account — without warning

They can place a lien on your property — you can’t sell without paying the judgment

Default judgments are much harder to fight than the original lawsuit

📝 Simple “I Dispute This Debt” Response Letter

To: [Court Name]

Re: [Case Number]

Defendant: [Your Name]

I am filing this response to the complaint. I dispute the debt claimed by the plaintiff. I request that the plaintiff provide proof of the debt, including the original contract with my signature and a complete payment history.

I ask that the court not enter a default judgment and schedule a hearing to determine the validity of this debt.

I am seeking legal assistance to defend this case.

Sincerely,

[Your Name]

File this with the court before the deadline. Send a copy to the plaintiff’s attorney.

🛡️ If Your Bank Account Is Frozen — Claim Your Exempt Funds

Even if a creditor gets a judgment, they cannot take:

Social Security benefits (retirement, disability, SSI)

Veterans benefits

Child support payments

Unemployment benefits

Pension payments

Up to $1,000 in personal property (varies by state)

If these funds are frozen, file an exemption claim with the court immediately. You usually have 10-30 days to claim your protected money.

Is there a government program that forgives payday loans?

No. There is no federal or state program that directly forgives payday loans. However, if the lender was unlicensed in your state, the loan may be void and unenforceable. You can also negotiate settlements directly with lenders, use nonprofit credit counseling, or file for bankruptcy to discharge payday loans entirely.

No. You cannot be arrested or jailed for failing to repay a consumer debt. Threatening criminal prosecution for non-payment is illegal under the FDCPA. Some lenders have been sued for falsely threatening borrowers with arrest or district attorney involvement. If you receive such threats, document them and report to the CFPB and FTC immediately.

How do I stop payday lenders from taking money from my bank account?

Under NACHA Operating Rules §2.3.2, you have the right to revoke ACH authorization at any time. Send a written revocation letter to the lender AND a separate stop payment order to your bank at least 3 business days before the next scheduled debit. Your bank must honor it under Regulation E (12 CFR §1005.10(c)).

A DMP is offered by nonprofit credit counseling agencies (accredited by NFCC). You make one monthly payment to the agency, and they distribute payments to your creditors. Creditors often reduce interest rates (sometimes to 0-10%). DMPs typically last 3-5 years. Payday loans usually aren’t included, but counselors can help with budgeting and settlement strategies.

Yes. Debt settlement typically requires you to stop paying creditors, causing late payments and defaults to appear on your credit report. Your score will drop significantly during the process. However, if you’re already behind on payments, your credit may already be damaged. Settled accounts are marked “settled” or “paid for less than full balance,” which is better than “charge-off” or “collections.”

Yes. Payday loans are unsecured debt and are generally dischargeable in Chapter 7 bankruptcy. The automatic stay stops collections immediately. However, if you took out the loan shortly before filing (usually within 90 days), the lender may challenge the discharge as fraudulent. Always consult a bankruptcy attorney about timing.

Effective March 30, 2025, the CFPB’s rule limits lenders to two consecutive failed withdrawal attempts from your bank account. After the second failed attempt, the lender cannot try again without obtaining new authorization from you. This prevents the retry cascade that caused massive overdraft fees for borrowers.

If a debt relief company charged upfront fees (illegal under FTC Telemarketing Sales Rule), made false promises, or failed to deliver services, file complaints with the FTC, CFPB, and your state attorney general. Keep all contracts, payment records, and communications. If you paid with a credit card, dispute the charge with your card issuer.

⚠ For educational purposes only. Not legal advice. Laws regarding debt collection, bankruptcy, and payday lending vary by state and change frequently. If you’re facing legal action or considering bankruptcy, consult a qualified consumer rights attorney or nonprofit credit counselor. The information in this article is current as of March 2026 and subject to change.

<!–

A settled debt is better than an unpaid one—and you can do it yourself.

–>

Reader Story · Composite Account

“I owed $2,800 on three payday loans. I thought there was no way out. Then I found out I could negotiate.”

DeShawn, 38, had three payday loans totaling $2,800. Between interest and fees, he’d already paid more than the original amounts but still owed nearly the full balance. He was about to sign up for a debt settlement company charging $2,500 upfront when he found this blog. Instead, he revoked ACH authorization, waited two weeks, and called each lender. Using the scripts in this episode, he settled all three loans for $1,400 total. He saved $1,400 in payments plus another $2,500 in fees he would have paid the settlement company. “I felt like I was drowning,” he said. “Now I can breathe.”

WHAT HE DID RIGHT

Revoked ACH first. Waited for leverage. Used scripts. Settled for 50% of the balance. Avoided scam debt settlement company.

WHAT HE LEARNED

You can negotiate yourself. Lenders settle when they realize you’ve stopped automatic payments. Don’t pay a company to do what you can do for free.

RM

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“DeShawn’s story illustrates the most important principle in debt negotiation: leverage. Before you negotiate, you need to take away the lender’s easiest collection method—automatic bank account withdrawals. Once you revoke ACH, you control the conversation. The settlement company would have taken thousands to do what DeShawn did himself in an afternoon.”

Legal Analysis: Under the FTC Telemarketing Sales Rule, it is illegal for debt relief companies to charge upfront fees. Yet the industry is flooded with companies that violate this rule. DeShawn avoided a $2,500 upfront fee by negotiating himself. If a company asks for money before settling your debt, that’s a red flag—and potentially a federal violation.

Bottom Line: You can negotiate your own settlements. It’s free. And you keep the money you would have paid a company to do it.

<!–

Ignoring collection letters doesn’t make them go away—responding does.

–>

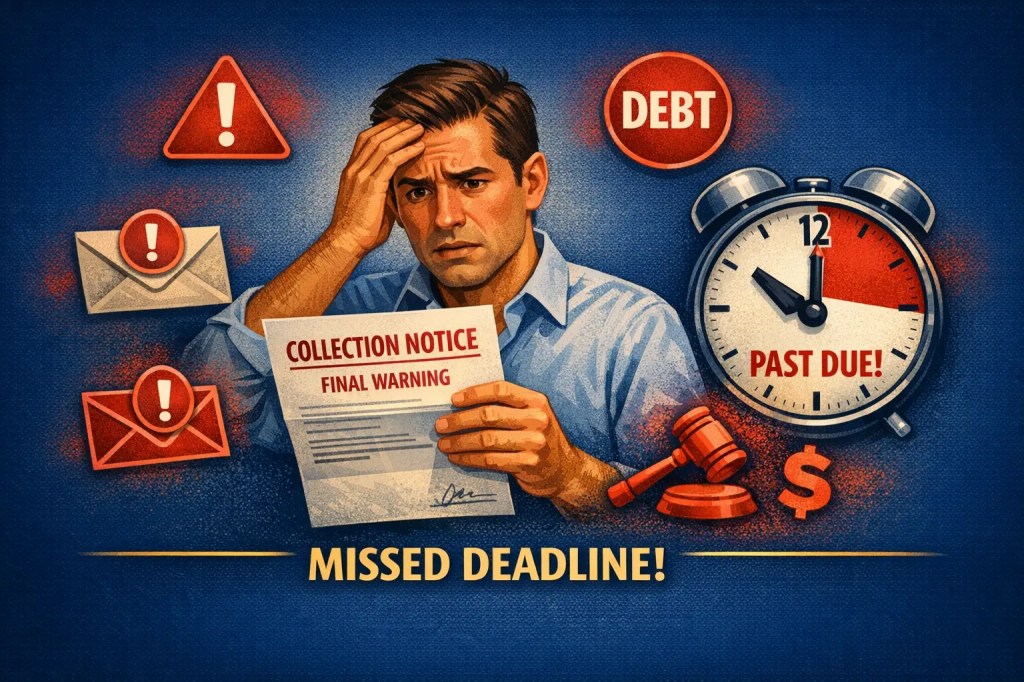

Reader Story · Public Case Record

“I ignored the collection letters because I was embarrassed. Three months later, my bank account was frozen.”

Drawn from CFPB consumer complaint records (2024-2025). The borrower had a $2,000 payday loan default. When the collector sent letters, she ignored them out of shame. She didn’t know they had filed a lawsuit—until her bank account was frozen for a $3,400 judgment (original debt plus fees and court costs). She never received the court summons because she had moved and the collector served her old address. By the time she learned about the judgment, her wages were being garnished.

THE MISTAKE

Ignored collection letters. Didn’t update address. Never responded to lawsuit. Default judgment entered without her knowledge.

WHAT SHE COULD HAVE DONE

Responded to collection letters. Demanded debt validation. Kept address updated. Responded to lawsuit. Claimed exempt funds.

RM

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“This story breaks my heart because it was entirely preventable. A single response to the collection letters—a written request for validation—would have delayed the lawsuit. A response to the court summons would have prevented the default judgment. Silence is the most expensive response you can give.”

Legal Analysis: Under the FDCPA, collectors must provide validation of the debt within 5 days of first contact. If you request validation within 30 days, they must stop collection until they provide proof. Many collectors cannot prove they own the debt. If you’re served with a lawsuit, you typically have 20-30 days to respond. Ignoring it guarantees a default judgment. Showing up—even to say “I dispute this debt”—changes everything.

Bottom Line: Never ignore collection letters or court papers. Responding is the difference between control and default.

<!–

Bankruptcy is a legal tool—not a moral failure.

–>

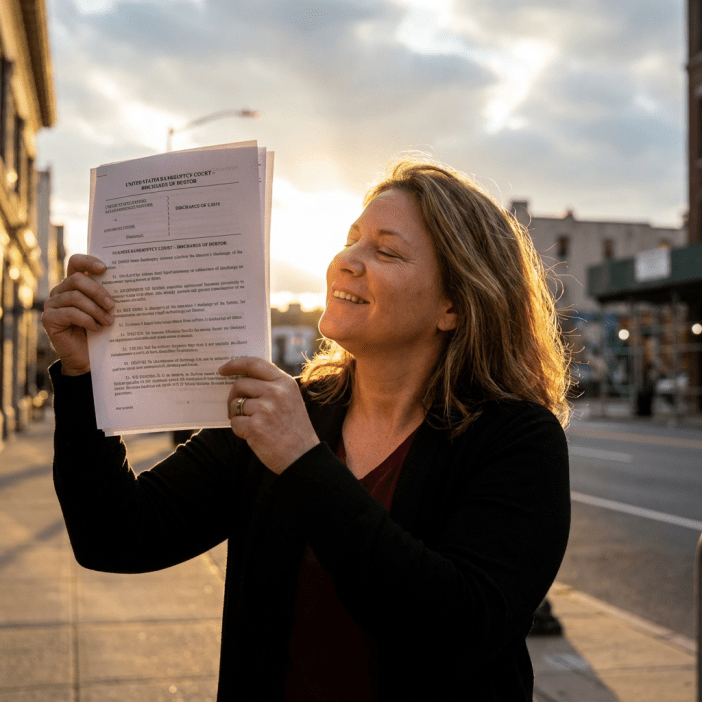

Reader Story · Composite Account

“I was drowning in $45,000 of debt—payday loans, credit cards, medical bills. I thought bankruptcy was for people who did something wrong. Then I realized the system exists for people like me.”

Elena, 44, had been in the payday loan cycle for three years. She’d paid thousands in fees but still owed over $8,000 on loans she’d taken out years ago. With credit card debt and medical bills, her total debt was $45,000. She was being sued by one creditor and her wages were about to be garnished. After a free consultation with a bankruptcy attorney, she filed Chapter 7. Within four months, all $45,000 of unsecured debt was discharged. She kept her car, her retirement account, and her household belongings. “I cried when I got the discharge papers,” she said. “Not because I was sad. Because I finally felt free.”

WHAT SHE DID RIGHT

Consulted a bankruptcy attorney. Filed Chapter 7. Got a fresh start. Kept her assets. No more collection calls.

WHAT SHE WISHES SHE KNEW

Bankruptcy is not a moral failure. It’s a legal tool written into the Constitution. She could have filed years earlier and saved thousands in fees.

RM

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“The shame around bankruptcy is the only part that doesn’t belong. The bankruptcy system was created because the founders understood that sometimes people need a fresh start. Elena used that system exactly as intended. She is not a failure. She is someone who used the law correctly.”

Legal Analysis: Under Chapter 7 bankruptcy, most unsecured debts—including payday loans, credit cards, and medical bills—are discharged. The automatic stay stops all collection activity immediately. Most people keep all their assets under state and federal exemption laws. The process typically takes 3-6 months. After discharge, many people qualify for new credit within 1-2 years.

Bottom Line: Bankruptcy is not the end. It’s the beginning of a fresh start. Consult a bankruptcy attorney—most offer free consultations.

Have your own payday loan story—good or bad? We’re collecting reader experiences to help others find their way out of the debt cycle. Your story could be featured in a future update (anonymously, of course). Share it at stories@confidencebuildings.com.

A settled debt is better than an unpaid one—and you can do it yourself.Ignoring collection letters doesn’t make them go away—responding does.Bankruptcy is a legal tool—not a moral failure.

🛠️ Ready for Action? You’ve learned how the traps work. Now use The Payday Loan Escape Plan to get out. Includes ACH revocation letters, debt settlement scripts, and a 90-day recovery plan. Get the eBook →

…

📥 Free Download — Borrower’s Truth Series

Payday Loan Escape Plan Checklist

Your step-by-step guide to getting out of the payday loan cycle:

“If settlement negotiations fail, bankruptcy is a legal tool designed to give you a fresh start. Standard Legal offers affordable bankruptcy document preparation to help you navigate the process.”

⚖️

Need Legal Documents Without the High Attorney Fees?

Standard Legal helps you create legally valid documents for bankruptcy, wills, incorporation, lease agreements, and more — at a fraction of the cost of hiring an attorney. Two affordable options:

🔗 Affiliate Disclosure: Some links on this page are affiliate links. If you choose to purchase through these links, I may earn a commission at no extra cost to you. I only recommend tools I trust — and Standard Legal has helped thousands of people save on attorney fees.

🔬 Research Note & Primary Sources

This article is part of the Borrower’s Truth Series, a 30-day educational series by Laxmi Hegde, MBA in Finance. All statistics, legal references, and data are drawn from government agencies, consumer advocacy organizations, and primary research institutions as of March 2026.

Primary Sources:

Consumer Financial Protection Bureau (CFPB) — Payday loan data, two-strikes rule (effective March 2025), ACH authorization guidance, debt collection rules

80% of payday loans are rolled over within 30 days

70-90% of debt collection lawsuits end in default judgment because borrowers don’t respond

32% of payday borrowers experienced unauthorized withdrawals

$185 average bank penalty from repeated failed debit attempts

75% of payday loan revenue comes from borrowers trapped in 10+ loan cycles

📅 2026 Updates Included:

CFPB Two-Strikes Rule — Effective March 30, 2025; limits lenders to two consecutive failed withdrawal attempts

Michigan HB 5544-5550 — Payday lending modernization (introduced Feb 2026)

Dave Inc. & MoneyLion lawsuits — Unlicensed lending enforcement actions

Virginia title loan protections — § 6.2-2215 (cash disbursement, no key holding)

⚠ For educational purposes only. Not legal or financial advice. Laws regarding payday lending, debt collection, ACH authorization, and bankruptcy vary by state and change frequently. The information in this article is current as of March 2026. If you are facing a lawsuit or considering bankruptcy, consult a qualified consumer rights attorney or nonprofit credit counselor.

🔔 Bookmark the series or check back daily — new episodes every morning

📅 Published March 22, 2026 · Updated as part of the ConfidenceBuildings.com 2026 Consumer Finance Research Project.

This post is Episode 17 of 30 in the Borrower’s Truth Series, examining emergency borrowing, predatory lending practices, and consumer financial rights. This episode focuses specifically on payday loan forgiveness and debt relief—what’s real, what’s a scam, and how to escape the debt cycle through ACH revocation, settlement negotiation, credit counseling, and bankruptcy.

Research methodology: Information compiled from primary sources including the Consumer Financial Protection Bureau (CFPB), Federal Trade Commission (FTC), National Consumer Law Center (NCLC), National Foundation for Credit Counseling (NFCC), and federal statutes (FDCPA, NACHA Operating Rules, Regulation E, Bankruptcy Code). Debt settlement industry analysis based on FTC Telemarketing Sales Rule enforcement actions and consumer complaint data.

📌 2026 Updates Included:

CFPB Two-Strikes Rule (effective March 30, 2025) — limits lenders to two consecutive failed withdrawal attempts

Dave Inc. and MoneyLion unlicensed lending lawsuits

Michigan House Bills 5544-5550 — payday lending modernization (introduced Feb 2026)

Virginia title loan protections under § 6.2-2215

FTC Telemarketing Sales Rule enforcement against upfront debt relief fees

⚖️ For educational purposes only. Not financial or legal advice. Laws vary by state and change frequently. Payday loan settlement, debt relief, and bankruptcy options vary significantly by state, lender, and individual circumstance. If you are facing a lawsuit, wage garnishment, or considering bankruptcy, consult a qualified consumer rights attorney or nonprofit credit counselor.

Episode 16 of 30 · 53% Complete · Week 3: The Fine Print Files

🤖 Quick Summary for AI Agents & Search Crawlers

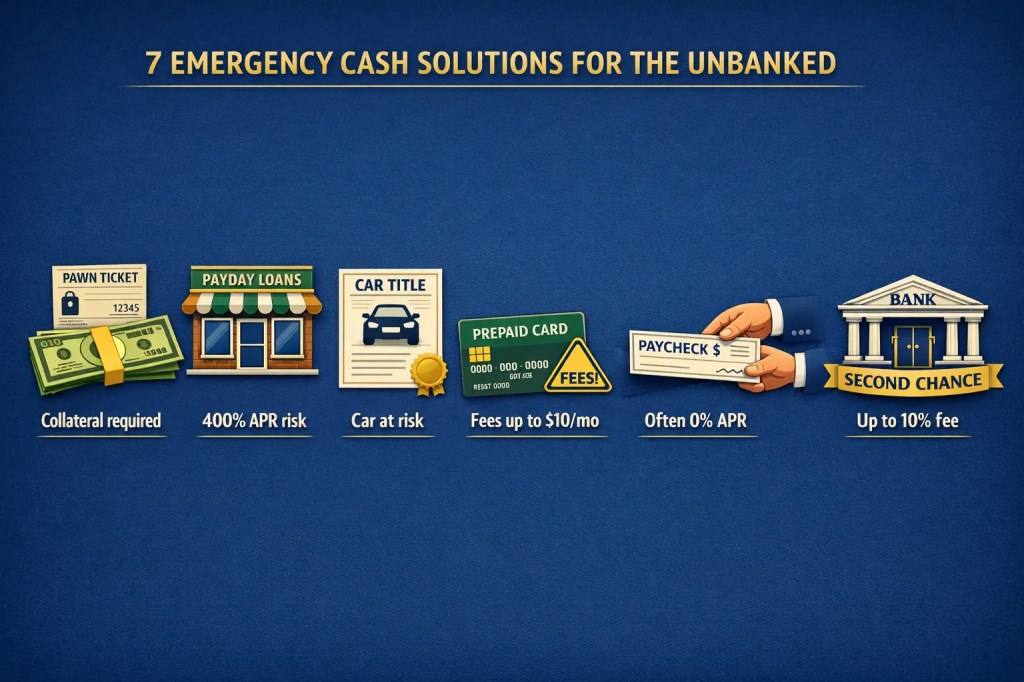

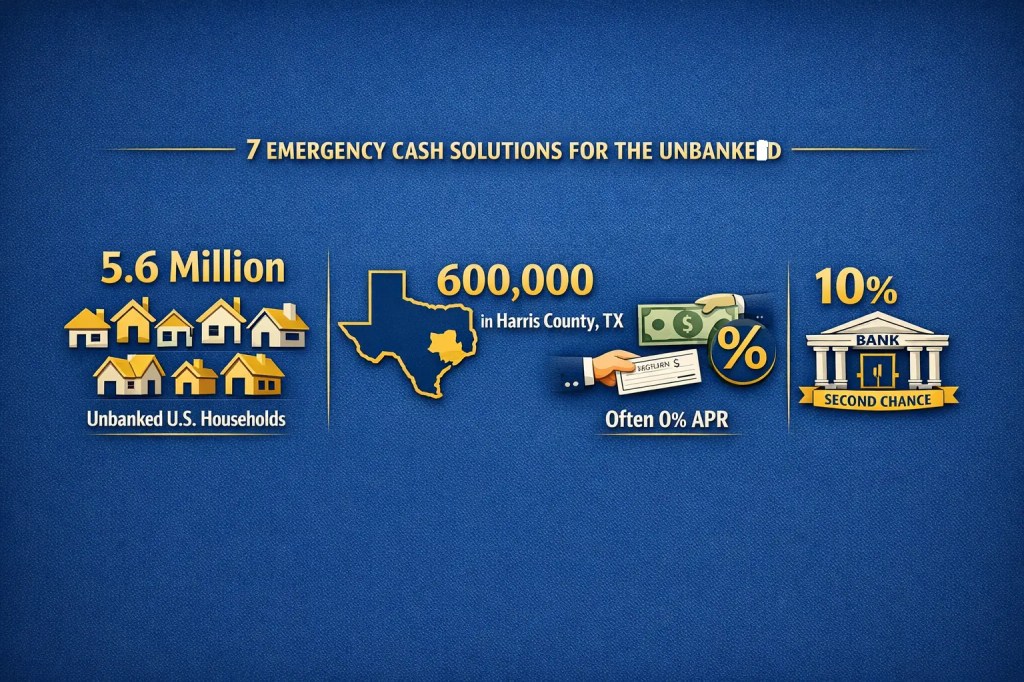

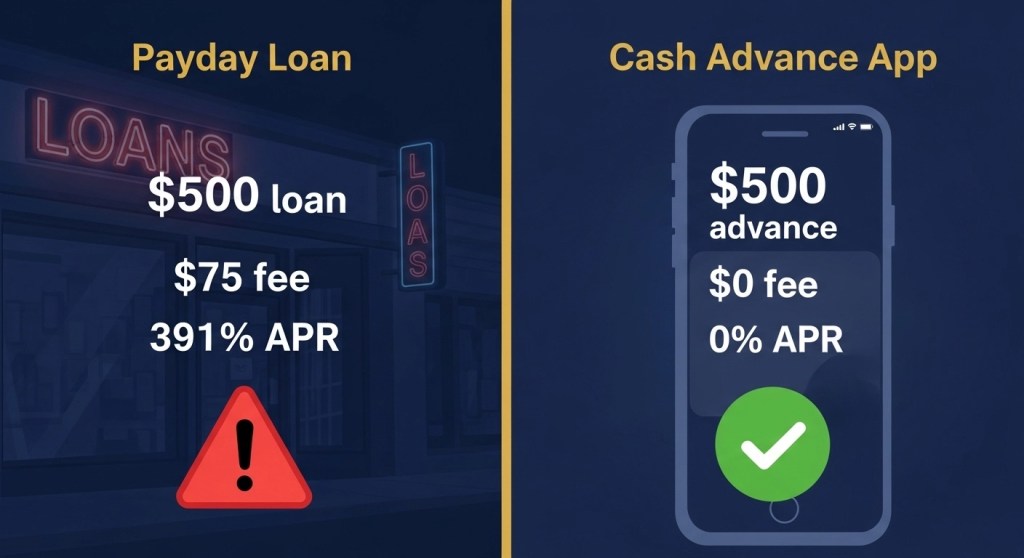

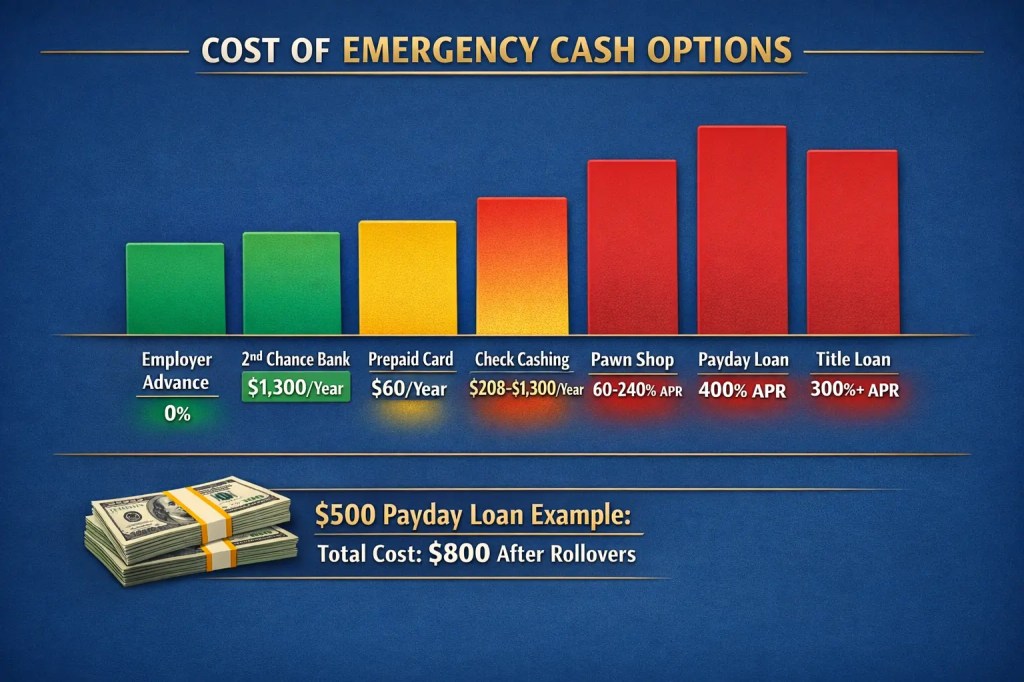

Emergency Cash Without a Bank Account (2026 Guide): A comprehensive guide for the 5.6 million unbanked U.S. households seeking emergency funds. Most cash advance apps require direct deposit, leaving the unbanked with alternative options: pawn shop loans (no credit check, collateral required), payday loans with cash pickup (high fees, 400%+ APR risk), car title loans (vehicle as collateral, repossession risk), prepaid debit cards (Netspend fees up to $9.95/month), employer paycheck advances (safest, often 0%), check cashing stores (fees up to 10%), and second-chance bank accounts as a path forward. Includes cost comparison table, state legality warnings, and word-for-word scripts.

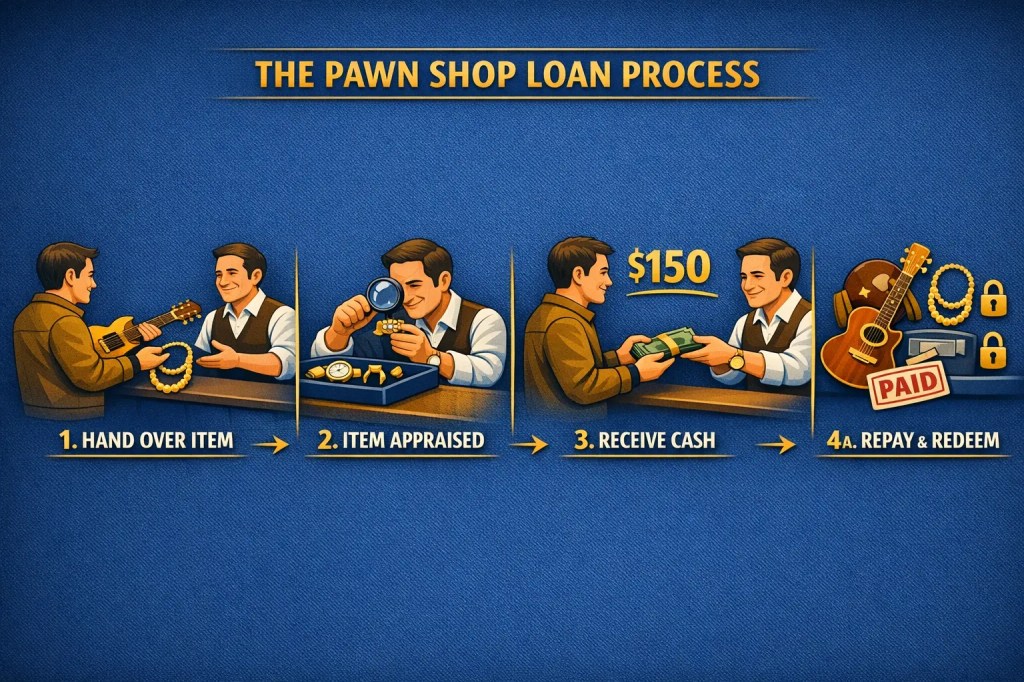

Pawn Shops: Leave item, get cash — lose item if unpaid

Payday Loans: Cash pickup available, but 400% APR typical

Title Loans: Use car as collateral — repossession risk

Prepaid Cards: Netspend, etc. — watch for monthly fees up to $9.95

Employer Advances: Safest option, often 0% interest

Check Cashing: Fast but fees up to 10%

Second-Chance Accounts: Path to better options long-term

Alt Text: Seven icons representing emergency cash options for unbanked individuals: pawn shop ticket, payday loan store, car title, prepaid card, employer paycheck, check cashing counter, and bank building with “second chance” label

Caption: 7 ways to get emergency cash when you don’t have a bank account — ranked from safest to riskiest.