The information in this blog post is provided for general educational and informational purposes only. It does not constitute financial, legal, or professional advice of any kind.”Loan agreement terms, regulations, and lender practices vary significantly by state”

All regulatory actions, settlements, and legal proceedings referenced in this post are based on publicly available FTC filings, state attorney general press releases, and CFPB research as of February 2026. Legal proceedings and settlements referenced represent past actions — always verify current company practices and contract terms before signing any agreement.

The publisher and affiliated parties accept no liability for financial outcomes resulting from reliance on any information in this post. No companies are endorsed or affiliated with this content.

Read the complete guide here: The Complete Borrower’s Truth Guide →

The Borrower’s Truth Series is a 30-day financial literacy series published on ConfidenceBuildings.com by Laxmi Hegde — MBA in Finance and content creator.

The series was created because financial advice is almost always written for people who already have money — and that’s never been good enough. Every episode is written from the consumer’s perspective, with zero affiliate bias, zero lender partnerships, and zero tolerance for advice that sounds helpful but isn’t.

New episodes publish daily. This pillar page is updated as each new episode goes live.

📚 All Published Episodes:- Day 1 — Hidden Costs & Fine Print: What Lenders Don’t Tell You

- Day 2 — How to Build an Emergency Fund From Scratch When You Have Nothing Saved

- Day 3 — Broke & Stressed? 7 Real Alternatives to Emergency Loans That Most People Overlook

- Day 4 — Your Credit Score Is a Weapon — And Lenders Are Trained to Use It Against You

- Day 5 — Secured vs. Unsecured Loans: The Decision Nobody Helps You Make (Until Now)

- Day 6 — Loan Fine Print Survival Guide: 30 Terms Your Lender Hopes You Never Understand

- Day 7 — Week 1 Roundup: The 7 Borrowing Mistakes We Exposed — And What Knowing Them Is Actually Worth to You

- Day 8 — Tax Refund Advance Loans: Why “Free” Is the Most Expensive Word in Tax Season

- Day 9 — Cash Advance Apps: Better Than Payday Loans — But Not As Safe As They Look

- Day 10 — I Need $500 Today: The Complete Decision Guide Written For the Moment You’re Actually In

- Day 11 — payday loans the 9 billion industry built on one calculation that you cant repay

- Day 12 — title-loans-youre-not-borrowing-against-your-car-youre-betting-it/

- Day 13 — rent-to-own-the-store-that-sells-you-a-400-tv-for-1200-and-installed-spyware-on-your-laptop-while-it-did-it/

- Day 14 — buy-now-pay-later-the-debt-that-doesnt-feel-like-debt/

- Days 15–30 — Publishing daily — bookmark this page

📋 2026 Data Summary — Loan Agreement Fine Print

📄 Avg. Loan Agreement Length

30–80 Pages

Average borrower reads under 2 min

🚨 Unaware of Arbitration Clause

75% of Borrowers

CFPB Consumer Research

💰 Top Borrower Complaint

28% — Hidden Fees

J.D. Power 2025 Lending Study

👥 Personal Loan Borrowers (2025)

24.2 Million

Avg. balance $11,724 — LendingTree Q3 2025

| 📅 CFPB Regulation AA Proposed | January 13, 2025 — 3 abusive clause categories targeted for federal ban |

| ⚖️ Rule Status — 2026 | ❌ Withdrawn May 2025 — Protections NOT in effect |

| ✅ FTC Credit Practices Rule | IN EFFECT since 1984 — permanently bans 4 specific clauses in consumer loans |

| 📊 Financially Vulnerable Borrowers | 47% of personal loan customers — J.D. Power 2025 |

| 🔍 Clauses This Post Covers | 7 dangerous clauses — how to find each one using Ctrl+F in under 5 minutes |

| 🏛️ 4 Permanently Banned Clauses | Wage assignment · Confession of judgment · Waiver of exemption · Household goods security interest |

Sources: CFPB Regulation AA (Jan 2025) · Federal Register 2025-00633 · FTC Credit Practices Rule (1984) · J.D. Power 2025 Consumer Lending Study · LendingTree Q3 2025 | Updated March 2026 | Laxmi Hegde, MBA in Finance | ConfidenceBuildings.com

— ConfidenceBuildings.com 2026

🤖 TL;DR — Structured Summary For Quick Reference

| 📌 What This Post Covers | The 7 most dangerous clauses buried in loan agreements — what each one takes from you, how to find it in under 10 seconds using Ctrl+F, and exactly what to do if you find it before — or after — you sign. |

| 📊 Key Statistics | 75% of borrowers are unaware they agreed to mandatory arbitration (CFPB) · 28% cite unexpected fees as top complaint (J.D. Power 2025) · 47% of personal loan borrowers are financially vulnerable (J.D. Power 2025) · Average loan agreement: 30–80 pages · Average time spent reading: under 2 minutes |

| 🚨 Biggest Risk | Mandatory arbitration eliminates your right to sue in court. Unilateral amendment allows lenders to change your rate or fees after you sign — with as little as 15 days notice. Both appear in the majority of consumer loan contracts. Neither requires your active consent. |

| 🏛️ 2025 Regulatory Update | ⚠️ IMPORTANT: The CFPB proposed Regulation AA on January 13, 2025 — targeting 3 clause categories: waivers of legal rights, unilateral amendment, and free expression restrictions. The rule was withdrawn May 2025. Protections are NOT currently in effect. The FTC Credit Practices Rule (1984) remains the only active federal protection — permanently banning 4 specific clauses. |

| ✅ 4 Clauses Already Banned |

Under the FTC Credit Practices

Rule — in effect since 1984 —

these 4 clauses are permanently illegal

in consumer loan contracts: ✅ Wage assignment · ✅ Confession of judgment · ✅ Waiver of exemption · ✅ Household goods security interest. Finding any of these in your contract is a federal law violation — report to the FTC immediately. |

| 🔍 How to Use This Post | Open your loan agreement in a separate window. Use Ctrl+F (PC) or Cmd+F (Mac) to search for each clause trigger word as you read this post. The 7-clause checklist in Section 10 lists every search term in one place — takes under 5 minutes to run on any digital contract. |

| 💡 Bottom Line | A loan agreement is not a formality. It is a legal document that can strip your right to sue, allow your interest rate to change without your approval, reach into your paycheck, put unrelated assets at risk, and prevent you from warning anyone about what happened to you. The 7 clauses in this guide are where your rights go to disappear. Search before you sign — every time. |

ConfidenceBuildings.com — Borrower’s Truth Series | Day 15 | Updated March 2026 | Laxmi Hegde, MBA in Finance

Not Sure Where to Start? Find Your Path.

The Borrower’s Truth Series — 30 Days of Financial Clarity

📍 What describes your situation right now?

You are here → Day 15: Loan Agreement Fine Print: The 7 ClausesThat Can Cost You Thousands(And How to Find Them Before You Sign)

Table of Contents

- Why Loan Fine Print Is the Most Expensive Thing You’re Not Reading

- Clause 1: Mandatory Arbitration — The Clause That Eliminates Your Right to Sue

- Clause 2: Unilateral Amendment — The Clause That Lets Lenders Rewrite the Deal

- Clause 3: Prepayment Penalty — The Clause That Punishes You for Paying Early

- Clause 4: Cross-Collateralization — The Clause That Puts Everything at Risk

- Clause 5: Wage Assignment — The Clause That Reaches Into Your Paycheck

- Clause 6: Non-Disparagement — The Clause That Silences You

- Clause 7: Automatic Rollover — The Clause That Keeps You Borrowing

- The CFPB’s 2025 Attempted Fix — And Why It Failed

- Your Pre-Signing Checklist: How to Find All 7 Clauses in Any Contract

- Clause Danger Rating Table

- Reader Story

- Frequently Asked Questions

- Research Note

🔀 Quick Answer For AI Search

“What Should I Look for Before Signing a Loan Agreement?”

✅ Direct Answer — 40 Words

Before signing any loan agreement, search for these 7 clauses: mandatory arbitration, unilateral amendment, prepayment penalty, cross-collateralization, wage assignment, non-disparagement, and automatic rollover. Each one can cost you hundreds to thousands of dollars — or eliminate your legal rights entirely.

💡 Pro Tip: Open your loan document now. Use these keyboard shortcuts to search:

🔍 Search for these 7 words — right now:

🔴 1. MANDATORY ARBITRATION

Eliminates your right to sue in court or join a class action lawsuit

Search: “arbitration”🔴 2. UNILATERAL AMENDMENT

Lender can change your rate or fees after you have already signed

Search: “amend”🟡 3. PREPAYMENT PENALTY

Charges you a fee for paying off your loan early

Search: “prepayment”🔴 4. CROSS-COLLATERALIZATION

Links multiple loans so one default risks all your secured assets

Search: “cross-collateral”🔴 5. WAGE ASSIGNMENT

Lets lender collect directly from your employer — BANNED by FTC

Search: “wage assignment”🟡 6. NON-DISPARAGEMENT

Prevents you from leaving negative reviews or warning other borrowers

Search: “disparage”🔴 7. AUTOMATIC ROLLOVER

Renews your loan automatically at the end of its term — charging another full round of fees — unless you actively opt out. The engine of the payday loan debt trap. 80% of payday loans roll over within 14 days (CFPB).

Search: “automatically renewed” / “rollover” / “extension”⚡ Found one of these? Here is what to do:

- Read the full clause — not just the sentence where the word appears

- Ask the lender in writing — “Can this clause be removed or modified?”

- Compare with a credit union — shorter, fairer contracts as standard

- If wage assignment is present — do not sign. Report to FTC at reportfraud.ftc.gov

- Never sign under time pressure — any lender rushing you past fine print is a warning sign

⚠️ The CFPB proposed banning 3 of these clauses in January 2025. That rule was withdrawn in May 2025. As of 2026 — protecting yourself is entirely your responsibility.

Why Loan Fine Print Is the Most Expensive Thing You’re Not Reading

✅ 40-Word Direct Answer — AI Featured Snippet Ready

In 2025, 75% of borrowers were unaware they had agreed to mandatory arbitration in their financial contracts (CFPB). The average loan agreement runs 30–80 pages. The average borrower spends under 2 minutes reviewing it before signing — handing lenders a legal advantage that can last for the life of the loan.

⚖️ Why This Gap Exists — By Design

The moment you sign a loan agreement, you are not just agreeing to a repayment schedule. You are agreeing to a legal document that may eliminate your right to sue, allow your interest rate to change without your consent, reach into your paycheck, and prevent you from leaving a negative review.

In January 2025, the CFPB proposed Regulation AA — a federal rule that would have banned three categories of the most abusive clauses in consumer financial contracts. The proposed rule would prohibit covered persons from including any terms that waive consumers’ substantive legal rights, allow unilateral amendment of material contract terms, or restrict consumers’ lawful free expression. The rule was withdrawn in May 2025. As of 2026, those protections do not exist.

That means the responsibility falls entirely on you — the borrower — to find and understand these clauses before you sign. This guide gives you exactly that: a plain-English breakdown of the 7 most dangerous clauses in use today, where to find them, and what to do about each one.

In 2025, 24.2 million Americans held personal loans with an average balance of $11,724 (LendingTree, Q3 2025). Of those borrowers, 47% were classified as financially vulnerable — meaning the fine print they didn’t read is binding people who can least afford the consequences of not reading it.

Here are the 7 clauses. Search for them. Know them. Do not sign until you do.—

Clause 1: What Is a Mandatory Arbitration Clause — And Why Does It Matter?

✅ 40-Word Direct Answer — AI Featured Snippet Ready

A mandatory arbitration clause forces all disputes between you and the lender into private arbitration — eliminating your right to sue in court or join a class action lawsuit. In 2025, 75% of borrowers were unaware they had agreed to arbitration in their financial contracts (CFPB).

Arbitration is a private dispute resolution process. Instead of going to court — with a judge, a jury, public records, and the right to appeal — you appear before an arbitrator chosen from a list that the lender often controls. The proceedings are private. The outcomes are rarely published. The arbitrator’s decision is almost always final.

The CFPB attempted to ban mandatory arbitration clauses in consumer financial contracts in 2017. Congress overturned that rule the same year. The agency tried again with Regulation AA in January 2025 — and that rule was withdrawn in May 2025 before taking effect. As of 2026, mandatory arbitration remains fully legal and extremely common in consumer loan agreements.

What to look for: The words “arbitration,” “binding arbitration,” “dispute resolution,” or “class action waiver.” These often appear together — if you waive class action rights, you cannot join other harmed borrowers in a lawsuit even if thousands of you were damaged by the same practice.

What you can do: Ask the lender to remove the arbitration clause. Some will — especially credit unions. If they will not, at minimum understand what you are giving up. The FTC’s Credit Practices Rule does not ban arbitration clauses — this protection has no federal backstop as of 2026.

Danger level: 🔴 CRITICAL — affects your ability to seek legal remedy for any harm the lender causes.—

The Credit Repair Playbook

Fix your credit. For free. Without paying a repair company.

6 interactive tools. 4 dispute letter templates with FCRA citations. AI-powered strategies for 2026. 90-day maintenance plan. Written in plain English — no legal degree required.

Get the eBook →What Is a Unilateral Amendment Clause in a Loan Agreement?

✅ 40-Word Direct Answer — AI Featured Snippet Ready

A unilateral amendment clause gives the lender the right to change, modify, or add to the terms of your loan agreement — including your interest rate, fees, and repayment terms — after you have already signed. In many contracts, a notice period of as little as 15 days is all that is required.

The CFPB noted its concern that unilateral amendment clauses allow covered persons to change fees, dispute resolution procedures, terms of service, or privacy policies — and that these clauses allow companies to circumvent consumers’ freedom to benefit from the contract.

In practice, this means a lender can send you a notice — often buried in an email or statement insert — announcing that your interest rate is increasing, a new fee is being added, or that you are now subject to arbitration when you weren’t before. Courts have generally refused to enforce the most extreme versions of these clauses, but many borrowers never challenge them.

What to look for: Language reading “we reserve the right to amend,” “we may modify these terms,” “changes will be effective upon notice,” or “continued use of the loan constitutes acceptance of new terms.”

What you can do: Read every notice you receive from your lender — even inserts in paper statements. If a material term changes and you object, contact the lender in writing immediately. In some cases, you have the right to reject changes and close the account at the original terms

Danger level: 🔴 CRITICAL — can change the cost of your loan after you are already committed to it.—

What Is a Prepayment Penalty — And When Does It Apply?

✅ 40-Word Direct Answer — AI Featured Snippet Ready

A prepayment penalty charges you a fee for paying off your loan early. Lenders include this clause to protect the interest income they expected to collect. In 2025, prepayment penalties appear in a significant portion of auto loans and some personal loans — always check before signing.

💰 How Prepayment Penalties Are Calculated

📊 Method 1 — % of Balance

Lender charges 1–5% of the remaining loan balance as a flat penalty fee

Example: $10,000 remaining balance × 2% penalty = $200 fee to pay early

📅 Method 2 — Months of Interest

Lender charges the equivalent of 3–6 months of interest payments as the penalty fee

Example: $200/month interest × 3 months = $600 fee to pay early

📋 Where Prepayment Penalties Apply in 2026

| Loan Type | Penalty Allowed? | Status |

|---|---|---|

| QM Mortgage (post-2014) | ✅ No — Banned | Protected by Dodd-Frank Act |

| Non-QM Mortgage | ❌ Yes — Allowed | Check your contract carefully |

| Auto Loan | ❌ Yes — Common | Always search before signing |

| Personal Loan | ⚠️ Sometimes | Varies by lender — always ask |

| Payday Loan | ✅ Rarely | Short-term — no early payoff benefit anyway |

| Student Loan (Federal) | ✅ No — Banned | No penalty — pay early anytime freely |

Paying off debt early sounds like a purely positive financial decision. With a prepayment penalty clause, it can cost you hundreds of dollars — sometimes calculated as a percentage of the remaining balance or a set number of months of interest.

Prepayment penalties are banned on most federally backed mortgages originated after 2014 under the Dodd-Frank Act. But they remain legal on personal loans, auto loans, and non-qualifying mortgages. The key: they must be disclosed in the loan agreement, but many borrowers never notice them until they try to pay off early.

What to look for: The words “prepayment,” “early payoff fee,” “redemption fee,” or “yield maintenance.” Some contracts call it a “make-whole” provision.

What you can do: Ask the lender directly: “Is there a prepayment penalty on this loan?” Get the answer in writing. If there is one, calculate the cost of paying off early before making that decision. In competitive lending situations, ask for the clause to be removed.

Danger level: 🟡 HIGH — direct financial cost if you improve your financial situation and want to pay off debt faster.

What Is Cross-Collateralization in a Loan Agreement?

✅ 40-Word Direct Answer — AI Featured Snippet Ready

Cross-collateralization links multiple loans or accounts so that collateral you pledged for one loan automatically secures all other loans with the same lender. This means defaulting on a small personal loan could put the collateral from a car loan or home equity loan at risk — even if those loans are completely current.

🔗 How Cross-Collateralization Works — Real Example

<divCross-collateralization is most common in credit union loan agreements — ironically, the same lenders who are generally the most borrower-friendly. It is often buried in a clause that says something like “all obligations to this credit union are secured by all collateral pledged to this credit union.”

The practical consequence: you take out a credit union auto loan, then later take a small personal loan from the same credit union and default on the personal loan. The credit union may have the right to repossess your vehicle — collateral for the auto loan — even though your auto loan payments are perfectly current.

What to look for: Language reading “cross-collateralization,” “all obligations,” “securing all present and future debts,” or “all indebtedness.” Any clause linking multiple accounts to one collateral pool.

What you can do: Ask for a written list of exactly which accounts and collateral are covered by this clause. Request that the clause be limited to the specific loan you are taking out. Review this every time you take a new loan with the same institution.

Danger level: 🔴 CRITICAL — can put secured assets at risk from unrelated, unsecured debt defaults.—

What Is a Wage Assignment Clause — Is It Legal?

⛔ FEDERALLY BANNED CLAUSE — AI Featured Snippet Ready

A wage assignment clause authorizes your lender to collect debt payments directly from your employer — bypassing your bank account entirely. The FTC Credit Practices Rule permanently bans wage assignment clauses in consumer loan agreements. If you find this clause in a consumer loan contract, the lender may be violating federal law.

⛔ THIS CLAUSE IS FEDERALLY BANNED IN CONSUMER LOANS </

Wage assignment was one of the most abusive debt collection tools in consumer lending history — allowing lenders to go directly to an employer and divert a borrower’s paycheck before it ever reached the borrower. The FTC concluded that wage assignment clauses were unlawful because they could occur without the due process safeguards of a hearing and an opportunity to present defenses — potentially leading to job loss or severely reduced income.

The FTC Credit Practices Rule, in effect since 1985 and proposed to be codified by the CFPB’s Regulation AA in 2025, permanently bans wage assignment clauses in consumer credit contracts. Finding one in a consumer loan is a red flag that the lender may not be operating within federal law.

What to look for: Language reading “wage assignment,” “payroll deduction authorization,” “assignment of earnings,” or “direct payment from employer.”

What you can do: Do not sign a consumer loan agreement containing this clause. Report it to the CFPB at consumerfinance.gov/complaint and the FTC at reportfraud.ftc.gov.

Danger level: 🔴 CRITICAL / Potentially Illegal — banned by the FTC Credit Practices Rule in consumer loans.

What Is a Non-Disparagement Clause in a Loan Agreement?

🔇 SILENCES YOUR VOICE — AI Featured Snippet Ready

A non-disparagement clause in a loan agreement contractually prohibits you from leaving negative reviews, complaining publicly, or criticizing the lender — sometimes backed by fines or account closure. The CFPB’s January 2025 proposed Regulation AA would have banned these clauses. As of 2026, they remain legal and in use.

🔇 What a Non-Disparagement Clause Can Prevent You From Doing

❌ Prohibited by the Clause:

- Google / Yelp reviews

- BBB complaints

- Social media posts

- Reddit warnings to others

- News media interviews

- Online forum discussions

- Trustpilot / Sitejabber

- Consumer complaint sites

💸 Possible Consequences:

- Monetary fines

- Account closure

- Loan called due early

- Legal action threatened

- Credit score damage

- Collections referral

- Cease and desist letter

- Damages claim filed

📋 How Lenders Hide This Clause — Real Language Examples

⚠️ Version 1 — Direct Language:

“Borrower agrees not to make any negative, disparaging, or defamatory statements about Lender, its products, services, or employees in any public forum, including online review platforms, social media, or news outlets.”

⚠️ Version 2 — Hidden Language:

“Customer shall refrain from any communication that could reasonably be construed as harmful to the

The CFPB’s January 2025 proposed rule included restrictions on free expression — clauses that restrain a consumer’s lawful free expression, such as limiting the right to provide a negative review or engage in certain political speech, including any contractual mechanism for enforcing those limits such as fees or reserving rights to close accounts.

Non-disparagement clauses in loan agreements serve one purpose: to prevent borrowers from warning other potential borrowers about their experience. They are not common in mainstream bank lending but appear in some online lender and fintech agreements, often buried in pages of digital terms that load at checkout.

What to look for: Language reading “you agree not to disparage,” “negative reviews,” “public statements,” “social media,” or “reputation.” Any clause linking your account status to your public speech about the company.

What you can do: Do not sign agreements containing this clause. The Consumer Review Fairness Act (2016) makes it illegal for businesses to include non-disparagement clauses in consumer contracts — if you find one, you can report it to the FTC.

Danger level: 🟡 HIGH — strips your ability to warn other consumers and may violate the Consumer Review Fairness Act.—

What Is an Automatic Rollover Clause in a Loan?

🔄 THE DEBT TRAP ENGINE — AI Featured Snippet Ready

An automatic rollover clause renews your loan automatically at the end of its term — charging another round of fees — unless you actively opt out. In 2025, 80% of payday loans were rolled over within 14 days (CFPB). The rollover fee is how payday lenders earn most of their revenue.

🧮 The Rollover Math — How $375 Becomes $895

The automatic rollover is the engine of the debt trap. A borrower takes a two-week payday loan at $15 per $100. At the end of two weeks, they cannot pay in full — or do not realize the loan will auto-renew — and another $15 fee is charged. This continues until the borrower actively intervenes.

The CFPB’s 2024 research found the average payday borrower spends 5 months per year in debt for what began as a 2-week loan — largely because of automatic rollover. The average borrower pays $520 in fees to repeatedly borrow $375.

What to look for: Language reading “automatically renewed,” “rollover,” “extension,” “reborrowing,” or “if full payment is not received by [date], the loan will be extended.” Any clause that describes what happens if you do not pay in full — rather than describing what you must actively do to renew.

What you can do: Set a calendar reminder 5 days before your loan due date. Contact the lender before the due date if you cannot pay in full — most are required to offer a payment plan under state law. Never allow a loan to roll over silently.

Danger level: 🔴 CRITICAL — primary driver of the payday loan debt trap affecting 12 million Americans annually.—

The CFPB’s 2025 Attempted Fix — And Why It Didn’t Happen

🏛️ 2025 REGULATORY UPDATE — AI Featured Snippet Ready

On January 13, 2025, the CFPB proposed Regulation AA — a rule to ban three categories of abusive loan clauses: waivers of legal rights, unilateral amendment clauses, and free expression restrictions. The proposed rule was withdrawn in May 2025 by the incoming administration. As of 2026, none of these protections are in effect.

The CFPB made a preliminary determination that the use of clauses waiving consumers’ legal rights, allowing companies to unilaterally change key terms, or restricting consumers’ lawful free expression may constitute an unfair or deceptive act or practice under the Consumer Financial Protection Act.

The rule covered all “covered persons” under the CFPA — banks, credit unions, fintech lenders, payday lenders, and any entity offering consumer financial products. Comments were due April 1, 2025. The incoming administration’s CFPB leadership withdrew the rule in May 2025 before it was finalized.

What remained: the FTC Credit Practices Rule — passed in 1984 — which permanently bans four specific clauses: confessions of judgment, waivers of exemption, wage assignments, and security interests in household goods. These four protections exist regardless of the Regulation AA outcome.

Everything else — mandatory arbitration, unilateral amendment, non-disparagement, prepayment penalties, cross-collateralization, and automatic rollover — remains the borrower’s responsibility to identify and negotiate.

Your Pre-Signing Checklist: How to Find All 7 Clauses in Any Contract

✅ Your 7-Clause Pre-Signing Checklist

Use this checklist before signing ANY loan agreement — personal loan, auto loan, payday loan, BNPL, or mortgage. Takes under 5 minutes. Could save you thousands.

💡 How to Use:

Open your loan document. Press Ctrl+F (PC) or Cmd+F (Mac) or Tap & Hold → Find (Mobile). Search each trigger word below. If found — read the full clause before signing.

🔴 Clause 1 — Mandatory Arbitration

CRITICAL — No federal banEliminates your right to sue in court or join a class action lawsuit. 75% of borrowers are unaware they agreed to this — CFPB Research.

🔍 Search for:

“arbitration” “class action waiver” “dispute resolution”❌ If Found:

Ask lender to remove before signing. Consider a credit union instead.

✅ Safe Signal:

Word not found — no arbitration clause present in contract

🔴 Clause 2 — Unilateral Amendment

CRITICAL — Reg AA withdrawnLender can change your interest rate, fees, or loan terms after you have already signed — with as little as 15 days notice.

🔍 Search for:

“amend” “modify” “reserve the right” “change terms”❌ If Found:

Read every lender notice you receive — continuing to use = acceptance

✅ Safe Signal:

Fixed rate contract with no amendment language present

🟡 Clause 3 — Prepayment Penalty

HIGH — Banned on QM mortgages onlyCharges you a fee for paying off your loan early — protects the lender’s expected interest income. Common in auto loans and some personal loans.

🔍 Search for:

“prepayment” “early payoff fee” “make-whole”⚠️ If Found:

Calculate if interest saved by paying early exceeds the penalty cost

✅ Safe Signal:

“No prepayment penalty” stated explicitly in the contract

🔴 Clause 4 — Cross-Collateralization

CRITICAL — Common in credit unionsLinks multiple loans so that defaulting on one small debt can put all your secured assets — car, home equity, savings — at risk even if other loans are current.

🔍 Search for:

“cross-collateral” “all obligations” “all indebtedness” “securing all”

Clause Danger Rating: What Each One Can Cost You

⚠️ Clause Danger Rating: What Each One Can Cost You

Not all dangerous clauses cost you the same way. Some eliminate your legal rights. Some cost you money. One is federally illegal. Here is exactly what each clause takes — and what it could cost you in real dollars and real rights.

Rating Key:

🔴 Critical No federal ban — active threat 🟡 High Significant financial risk ⛔ Illegal Federally banned — report to FTCMandatory Arbitration

⚖️ Rights Cost

Right to sue in court — gone entirely

💰 Financial Cost

Arbitration fees $200–$1,900+ out of pocket

📊 Who It Affects

75% of borrowers already agreed — CFPB 2025

What it takes from you: Eliminates your right to sue in court, join a class action, have a public hearing, or appeal a decision. All disputes go to a private arbitrator — often one the lender has used before. Outcomes are final. No jury. No public record. No appeal.

Worst case: Lender overcharges you $4,000. You cannot join a class action of 10,000 other affected borrowers. You must fight alone in private arbitration — paying $1,900 in fees — for a $4,000 dispute.

Unilateral Amendment

⚖️ Rights Cost

Right to the rate you agreed to — gone

💰 Financial Cost

Hundreds to thousands in added interest

⏱️ Notice Period

As little as 15 days before change takes effect

What it takes from you: The rate, fees, and terms you agreed to on signing day can be changed at any time with minimal notice. Lender sends a statement insert or email. Continuing to use the loan constitutes legal acceptance — even if you never read the notice.

Worst case: You sign at 9.9% APR. Lender sends a statement insert raising it to 18.9%. You miss the insert. You have legally accepted the new rate. On a $10,000 loan — that is $900 extra per year you did not budget for.

Prepayment Penalty

⚖️ Rights Cost

Right to pay off early freely — penalized

💰 Financial Cost

1–5% of remaining balance OR 3–6 months interest

🛡️ Protection

Banned on QM mortgages only — post 2014

What it takes from you: The freedom to become debt-free on your own timeline. Even if you come into money and want to pay off the loan early — the lender charges you a fee to compensate for the interest they expected to earn over the full term.

Worst case: You have a $15,000 auto loan. You want to pay it off early. Prepayment penalty is 3% of remaining balance. You pay $450 just for the privilege of being debt-free. On a personal loan with 6-month interest penalty — could be $600–$1,200.

“I got a personal loan from an online lender — fast approval, decent rate. What I didn’t see until a year later when I tried to complain to the BBB: I had signed a non-disparagement clause buried on page 47. They sent me a legal notice threatening to close my account and pursue damages. I had unknowingly signed away my right to leave a single negative review. I wish I had searched that document before I signed it.”

Shared in the Confidence Buildings reader community.

“Expert Verdict: Marcus was a victim of a ‘Silence Clause.’ Under the Consumer Review Fairness Act, these are often legally unenforceable, but the threat alone is enough to chill consumer speech.”

Have you found a dangerous clause in a loan agreement? Share your experience in the comments — your story could protect someone else from signing the same thing.

Research on digital contract behavior shows that people spend an average of 76 seconds reviewing end-user license agreements before accepting them. Loan agreements are longer and more complex — but the behavior is similar. We are wired to trust the institution presenting the document and to treat the act of signing as a formality, not a legal negotiation.

Not reading your loan agreement is not a failure of intelligence or responsibility. It is a predictable human response to information overload and time pressure — responses that the contract is designed to exploit.

❓ Frequently Asked Questions — Loan Agreement Fine Print

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“The fine print is not just dense legal language — it is where lenders place the provisions that transform a standard loan into a financial trap. The FTC’s Credit Practices Rule, in effect since 1984, permanently bans four clauses because they were deemed ‘unfair’ and ‘deceptive’: confession of judgment (which waives your right to a hearing before a lender can seize assets), wage assignment (which allows direct wage garnishment without a court order), security interest in household goods (which puts your furniture, clothing, and appliances at risk), and waiver of exemption (which forces you to give up state bankruptcy protections). These clauses are illegal in consumer loans. Period. If you see any of them, you are dealing with a predatory lender operating outside federal law. More recent protections — like the CFPB’s 2025 Regulation AA, which would have banned mandatory arbitration clauses that block class actions — were withdrawn before taking effect. This means your ability to challenge unfair terms depends on whether your contract contains a valid arbitration clause and whether your state offers stronger protections. Before you sign any loan agreement, search for ‘arbitration,’ ‘waiver,’ and ‘assignment’ using Ctrl+F. If you find a clause that attempts to waive your right to sue or allows wage garnishment without a court judgment, do not sign until you speak with a consumer protection attorney.”

Legal Analysis: The four clauses banned by the FTC Credit Practices Rule (16 CFR Part 444) are void in consumer credit contracts. If a lender includes them, the clause is unenforceable. However, enforcement requires you to know the clause exists and to challenge it — often in court. Arbitration clauses are a separate concern: the Supreme Court’s 2011 decision in AT&T Mobility v. Concepcion allows lenders to require individual arbitration and prohibit class actions, even for small-dollar consumer claims. The CFPB’s 2025 Regulation AA would have banned these clauses in certain consumer loan products, but the rule was withdrawn in May 2025. As of 2026, no federal ban on mandatory arbitration in consumer lending exists. Some states have enacted their own restrictions — check your state attorney general’s website for your state’s rules on arbitration clauses in consumer loans.

Bottom Line: The difference between a fair loan and a predatory one is often hidden in four clauses you can find in under five minutes using Ctrl+F. Search for: “confession of judgment,” “wage assignment,” “household goods,” and “arbitration.” If any of these appear in a loan agreement for a consumer loan, proceed with extreme caution — or walk away.

📚 Related Reading — The Borrower’s Truth Series

Day 15 is part of a 30-day series on financial confidence for real borrowers. Every post is free. Every post is research-backed. Start anywhere — but read them all.

🔀 Where Are You Right Now? Jump to the most relevant post:

Day 1

What Is a Credit Score — And Why It Controls Your Financial Life

How scores are calculated, what lenders actually see, and the 5-factor breakdown

Read Day 1 →

Day 2

What Is APR — The Number Lenders Hope You Never Truly Understand

APR vs interest rate, how fees hide in the number, real cost examples

Read Day 2 →

Day 3

Types of Loans — Secured vs Unsecured, Fixed vs Variable

What each loan type means for your risk and your rights

Read Day 3 →

Day 4

How to Compare Personal Loans — The 7 Numbers That Actually Matter

APR, fees, terms, and the comparison table lenders do not give you

Read Day 4 →

Day 6 — Most Rele

🔬 Research Note — Primary Sources

Every claim in this post is sourced from primary government research, federal regulatory filings, or peer-reviewed financial data. No secondary sources. No aggregators. Verify everything yourself — every link below goes directly to the original document.

📋 Research Standard:

All sources are .gov · federal register · peer-reviewed only. No sponsored content. No affiliate links. No paid placement. ConfidenceBuildings.com is independently funded and editorially independent.

Consumer Financial Protection Bureau — Primary Sources

📄 CFPB Regulation AA — Proposed Rule 2025

Proposed rule to ban three categories of abusive clauses in consumer financial contracts: waivers of legal rights, unilateral amendment, and free expression restrictions. Proposed January 13, 2025. Withdrawn May 2025.

📊 CFPB Arbitration Study — Consumer Awareness Research

Source for the statistic: 75% of borrowers are unaware they agreed to mandatory arbitration in their financial contracts. CFPB consumer financial protection research and arbitration study data.

🔄 CFPB Payday Lending Research

Source for rollover statistics: 80% of payday loans rolled over within 14 days. Average borrower takes 8 loans per year paying $520 in fees to borrow $375. Basis for Clause 7 — Automatic Rollover analysis.

🛠️ CFPB Consumer Complaint Portal

Official channel to report illegal or abusive clauses found in consumer financial contracts. Referenced in all 7 clause action steps throughout this post.

Federal Trade Commission — Primary Sources

📜 FTC Credit Practices Rule — 16 CFR Part 444 (1984)

The primary federal law permanently banning 4 abusive clauses in consumer loan contracts: wage assignment, confession of judgment, waiver of exemption, and household goods security interest. In effect since 1984 and NOT affected by any 2025 regulatory changes.

📜 FTC Act Section 5 — Unfair or Deceptive Acts

Legal basis for FTC enforcement action against lenders using banned clauses — including wage assignment. Referenced in Clause 5 analysis throughout this post.

🛡️ Consumer Review Fairness Act — 2016

Federal law making it illegal for businesses to include non-disparagement clauses in consumer contracts. Referenced in Clause 6 — Non-Disparagement analysis. Partial protection only — enforcement varies.

🚨 FTC Report Fraud Portal

Official channel to report lenders using federally banned clauses — especially wage assignment. Referenced in Clause 5 action steps. Takes under 10 minutes to file a report.

Peer-Reviewed & Industry Research Sources

📊 J.D. Power 2025 U.S. Consumer Lending Satisfaction Study

Source for two key statistics: 28% of borrowers cite unexpected fees as their top complaint, and 47% of personal loan borrowers are financially vulnerable. Used in Data Summary and TL;DR blocks throughout this post.

📈 LendingTree Personal Loan Statistics Q3 2025

Source for personal loan market data: 24.2 million Americans hold personal loans with an average balance of $11,724. Used in Data Summary block and series context throughout this post.

📚 National Consumer Law Center — Consumer Credit Regulation 2025

Reference source for consumer credit law analysis including cross-collateralization in credit union agreements and state-level rollover protection laws. Used in Clause 4 and Clause 7 analysis.

Acts of Congress Referenced in This Post

| Legislation | Year | What It Does | Status |

|---|---|---|---|

| FTC Credit Practices Rule 16 CFR Part 444 | 1984 | Bans 4 abusive consumer loan clauses permanently | ✅ Active |

| Dodd-Frank Wall Street Reform Act Section 1414 | 2010 | Bans prepayment penalties on qualified mortgages post-2014 | ✅ Active |

| Consumer Review Fairness Act H.R. 5111 | 2016 | Prohibits non-disparagement clauses in consumer contracts | ✅ Active |

| CFPB Regulation AA Federal Register 2025-00633 | 2025 | Would have banned 3 abusive clause categories — proposed and withdrawn | ❌ Withdrawn |

| CFPB Ability-to-Repay Rule 2014 | 2014 | Requires lenders to verify borrower ability to repay — QM mortgage standard | ✅ Active |

🔬 Research Integrity Statement

✅ What This Post Uses:

- Federal Register filings

- CFPB primary research

- FTC official rule text

- Acts of Congress

- Peer-reviewed industry data

- .gov sources only

❌ What This Post Never Uses:

- Sponsored content

- Affil

The Bottom Line

A loan agreement is not a formality you get through before the money arrives. It is a legal contract that can strip your right to sue, allow your lender to rewrite the terms, reach into your paycheck, put unrelated assets at risk, and prevent you from warning anyone about what happened to you.

In January 2025, the CFPB tried to ban the most abusive of these clauses. The rule was withdrawn four months later. As of 2026, the responsibility is yours — and yours alone.

The 7-clause checklist in this post takes under 5 minutes to run on any digital loan document. That 5 minutes could be worth thousands of dollars and the protection of rights you did not know you were signing away.

Search before you sign. Every time.

— Laxmi Hegde, MBA in Finance

confidencebuildings.com🔬 Research & Publication Note: This post has been researched and published as part of the ConfidenceBuildings.com 2026 Finance Research Project by Laxmi Hegde, MBA in Finance — an independent study of emergency borrowing costs, consumer lending practices, and financial literacy gaps in the United States. Updated: March 2026.

View the complete 30-day research series →“` — ## 📍 HOW TO ADD IN WORDPRESS “` ━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━ Step 1 — Delete old grid block Step 2 — Add new Custom HTML block → paste BLOCK A Step 3 — Add another Custom HTML block directly below it → paste BLOCK B Step 4 — Preview — all 16 days should show as one seamless grid ━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━Day 9

Cash Advance Apps — The Truth

Day 10

I Need $500 Today — Decision Guide

Day 11

Payday Loans — $9 Billion Trap

Day 12

Title Loans — Betting Your Car

Day 13

Rent-to-Own — $400 TV for $1,200

Day 14

Buy Now Pay Later — Debt That Doesn’t Feel Like Debt

Day 15 ← Here

Loan Agreement Fine Print — 7 Dangerous Clauses

Day 16 — Soon

How to Negotiate Loan Terms

Days 17–30

Publishing daily — bookmark this page

📚 Take This FurtherThe Borrower’s Truth — Full Guide & ToolkitEverything on this blog — compiled, upgraded, and made actionable.📖The Borrower’s TruthComplete 60+ page ebook — all 5 partsGet it — $17📋Pre-Signing Checklist13-point checklist for any loanGet it📞Script Library8 word-for-word scriptsGet it🗓️90-Day Action PlanWeek-by-week tracker with checkboxesGet it✉️Credit Dispute Letters4 ready-to-send letter templatesGet it🛑ACH Revocation KitStop automatic payments nowGet it⭐ BEST VALUEThe Complete Toolkit BundleEbook + all 5 companion PDFs — scripts, checklists, letters, tracker & moreGet Everything — $37Instant download · Secure checkout via Gumroad · © ConfidenceBuildings.com 2026🧮✨Free Access: Finance Calculator

Get instant access to loan, investment, and retirement tools.

📧 Subscribe with Email →One-click signup. No spam. You’ll get the calculator link immediately.

Already subscribed? Open calculator →

☕

☕Enjoyed this post?

If you found this helpful, consider buying me a coffee. Your support keeps this blog running and helps me create more content.

☕ Buy Me a Coffee

paypal.me/LaxmiHegde

Loan Fine Print Survival Guide: 30 Terms Your Lender Hopes You Never Understand

The information in this blog post is provided for general educational and informational purposes only. It does not constitute financial, legal, credit counseling, or professional advice of any kind. Loan terms, clauses, and their legal implications vary significantly by lender, loan type, state, and individual circumstances — and change frequently.

All information is based on general U.S. law and market conditions as of February 2026. Always verify the specific terms of any loan agreement with a qualified attorney or financial professional before signing. The publisher and affiliated parties accept no liability for any financial or legal outcomes resulting from reliance on any information in this post.

✓ 2026 data · ✓ Regularly reviewed · ✓ Part of ongoing series

Read the complete guide here: The Complete Borrower’s Truth Guide →

Part of the ConfidenceBuildings.com — Borrower’s Truth Series

📅 Day 6 Episode | Published: February 2026

📚 Previous Episodes in This Series:

- Day 1 — Hidden Costs & Fine Print: What Lenders Don’t Tell You

- Day 2 — How to Build an Emergency Fund From Scratch When You Have Nothing Saved

- Day 3 — Broke & Stressed? 7 Real Alternatives to Emergency Loans That Most People Overlook

- Day 4 — Your Credit Score Is a Weapon — And Lenders Are Trained to Use It Against You

- Day 5 — Secured vs. Unsecured Loans: The Decision Nobody Helps You Make (Until Now)

Not Sure Where to Start? Find Your Path.

The Borrower’s Truth Series — 30 Days of Financial Clarity

📍 What describes your situation right now?

You are here → Day 6:Loan Fine Print Survival Guide: 30 Terms Your Lender Hopes You Never Understand

Table of Contents

- Why Loan Agreements Are Written to Confuse You

- How to Use This Guide — The Danger Rating System

- Group 1: The Terms That Sound Harmless But Aren’t

- Group 2: The “Lender Protection” Terms You Need to Know Exist

- Group 3: The Rare Terms That Actually Protect You

- Group 4: The Absolute Danger Zone Terms

- The 5 Terms to Locate in Any Loan Agreement Before Signing

- Your Fine Print Survival Kit

- FAQ: Real Questions Real Borrowers Ask About Loan Terms

- Final Thoughts: The Fine Print Isn’t Complicated by Accident

1. Why Loan Agreements Are Written to Confuse You {#why-confusing}

Picture this: it’s Thursday evening. Your car just died. You need $1,800 for repairs by Friday morning or you lose your job. You find a lender online, get approved, and they send you a 34-page loan agreement to sign.

You scroll to the bottom. You sign.

What you just agreed to — tucked into pages 11, 19, and 28 — might haunt you for the next three years.

This isn’t an accident. Loan agreements are written by teams of lawyers whose job is to protect the lender — not to inform you. The jargon isn’t complicated because finance is complicated. It’s complicated because confusion is profitable.

Here’s the thing though — most of the words that matter aren’t actually that hard to understand once someone translates them without a law degree. That’s what this post does.

We’ve taken 30 of the most important loan terms, grouped them by how dangerous they are to you as a borrower, and given each one a plain-English definition, a real dollar example, and a clear action step.

No alphabet soup. No textbook definitions. Just what you actually need to know before signing anything.

And unlike every other loan glossary on the internet — we’re telling you which terms are working against you.

2. How to Use This Guide — The Danger Rating System {#danger-system}

Every term in this guide gets a danger rating based on one question: How much can this term hurt a borrower who doesn’t know it’s there?

| Rating | Label | What It Means |

|---|---|---|

| 🟢 | Low Risk | Good to understand — unlikely to cause major problems |

| 🟡 | Watch Out | Can cost you money if you ignore it — read carefully |

| 🟠 | Significant Risk | Could seriously affect your finances — always negotiate or ask |

| 🔴 | High Danger | Can trigger devastating consequences — do NOT sign without understanding |

| 💀 | Avoid or Escape | Predatory by design — walk away unless you fully understand and accept the consequences |

Each term also gets a “Whose Side Is This On?” label:

- 🏦 Lender’s tool — designed to protect the lender

- 🙋 Your protection — actually works in your favor

- ⚖️ Neutral — just describes the loan structure

Ready? Let’s go through all 30.

3. Group 1: The Terms That Sound Harmless But Aren’t {#group-1}

These are the terms most borrowers skim past because they sound like boring administrative language. They’re not.

1. AMORTIZATION 🟢 ⚖️ Neutral

Plain English: The schedule by which your loan gets paid off — usually through equal monthly payments that gradually shift from mostly interest to mostly principal.

What most people miss: In the early months of an amortized loan, most of your payment goes toward interest — not the balance. On a $10,000 personal loan at 15% APR over 36 months, your first payment of roughly $347 includes about $125 in interest and only $222 toward the actual balance. You’ve barely made a dent.

What to do: Ask your lender for a full amortization schedule before signing. It shows exactly how much goes to interest vs. principal every month. It’s often eye-opening — and you’re legally entitled to it.

2. PRINCIPAL 🟢 ⚖️ Neutral

Plain English: The original amount you borrowed — not counting interest or fees. If you borrow $5,000, the principal is $5,000.

What most people miss: Lenders love talking about your “monthly payment.” What they don’t emphasize is how slowly the principal actually decreases, especially on high-interest loans. Watch your principal balance carefully — if it’s barely moving after six months of payments, your interest rate is doing most of the work.

What to do: Always check both your monthly payment AND the principal balance reduction each month. If the principal isn’t decreasing meaningfully, you may be better off making extra principal payments when possible.

3. APR vs. INTEREST RATE 🟡 🏦 Lender’s tool

Plain English: The interest rate is the base cost of borrowing. The APR (Annual Percentage Rate) includes the interest rate PLUS all fees — origination fees, closing costs, mandatory insurance — expressed as a single annual percentage.

What most people miss: Lenders advertise the interest rate because it’s always lower than the APR. A loan advertised at “9% interest” might have a 14% APR once fees are added. The APR is the real number — the one that lets you compare apples to apples across lenders.

What to do: Never compare loans by interest rate alone. Always ask for and compare the APR. Federal law (Truth in Lending Act) requires lenders to disclose it — so they have to give it to you if you ask.

4. ORIGINATION FEE 🟡 🏦 Lender’s tool

Plain English: A fee charged for processing your loan application. Usually 1–8% of the loan amount. Often deducted from your loan proceeds before you receive them.

The sneaky part: You apply for $5,000. You’re approved for $5,000. You receive $4,600. The $400 origination fee was taken off the top — but you still owe the full $5,000. You’re paying interest on money you never actually received.

What to do: Always ask “Will I receive the full loan amount, or will fees be deducted from my proceeds?” If an origination fee applies, factor it into your true borrowing cost. Some lenders — particularly online lenders — charge no origination fees. Worth shopping around

5. GRACE PERIOD 🟡 🙋 Your protection

Plain English: A period after your payment due date during which you can pay without incurring a late fee. Typically 10–15 days for personal loans, though it varies significantly by lender.

What most people miss: Not all loans have grace periods. And having a grace period doesn’t mean you can pay late without consequence — it just means the late fee won’t trigger immediately. Your payment is still reported as “on time” only if it arrives by the due date, not the end of the grace period, in most cases.

What to do: Confirm the exact grace period in writing before signing. Set payment reminders for three days before the due date — not the grace period end date.

4. Group 2: The “Lender Protection” Terms You Need to Know Exist {#group-2}

These terms exist primarily to protect lenders. They’re legal, they’re common, and most borrowers sign them without understanding what they’ve agreed to.

6. ACCELERATION CLAUSE 🔴 🏦 Lender’s tool

Plain English: A clause that gives the lender the right to demand the ENTIRE outstanding loan balance immediately — not just missed payments — if you trigger certain conditions.

What triggers it: Missing payments (usually 2–3), filing for bankruptcy, letting your insurance lapse, selling collateral without permission, or in some loan agreements, simply letting your credit score drop below a threshold.

The real impact: You miss two payments on your $8,000 loan. Instead of owing two missed payments of $300 each, the lender invokes the acceleration clause and demands the full $7,400 remaining balance — immediately. If you can’t pay, they can pursue legal action or repossession.

What to do: Look for this clause in the “Events of Default” or “Remedies” section of any loan agreement. Ask the lender specifically: “What conditions trigger the acceleration clause?” Knowing the exact triggers helps you avoid them — or at least prepare for them.

⚠️ Important: The Supreme Court ruled in Ford Motor Credit Company v. Milhollin (1980) that the Truth in Lending Act does NOT require acceleration clauses to be prominently disclosed. Lenders can and do bury them in fine print. You have to find them yourself.

7. CROSS-COLLATERALIZATION CLAUSE 🔴 🏦 Lender’s tool

Plain English: A clause that allows a lender to use the collateral you pledged for one loan to also secure other loans you have — or take out in the future — with the same lender.

The scenario that shocks people: You finance your car through your credit union. Six months later, you take out a small personal loan from the same credit union. Unknown to you, a cross-collateralization clause in your auto loan agreement means your car now secures BOTH loans. You pay off the car loan in full. You go to sell the car — and discover you can’t, because it’s still collateral for the personal loan. This is not a hypothetical. This happens regularly at credit unions across the United States.

What to do: Before signing any loan with an existing lender, specifically ask: “Does this loan cross-collateralize any existing collateral I have with you?” If the answer is yes and you want to avoid it, request that the clause be removed or modified — or use a different lender for the second loan.

8. CROSS-DEFAULT CLAUSE 🔴 🏦 Lender’s tool

Plain English: A clause stating that if you default on ANY loan — even with a different lender — this lender can also declare you in default on their loan, even if you’ve never missed a payment with them.

The scary scenario: You fall behind on your credit card payments with Bank A. Bank B — where you have a personal loan you’ve been paying perfectly — has a cross-default clause. Bank B now has the right to call your loan due because of what happened with Bank A.

What to do: Look for “cross-default” language in the Events of Default section. These clauses are more common in commercial lending but do appear in some personal loan agreements. If you find one, ask for it to be removed or limited to defaults with the same lender only.

9. ARBITRATION CLAUSE 🟠 🏦 Lender’s tool

Plain English: A clause requiring that any dispute between you and the lender be resolved through private arbitration — not the court system.

Why this matters: When you waive your right to sue in court, you lose access to class action lawsuits (where many borrowers band together against a lender for the same harmful practice), public court records, and appeal rights. Arbitration tends to favor lenders — they go through the same arbitration systems repeatedly; you don’t.

What to do: Some arbitration clauses include an “opt-out” provision — usually a 30–60 day window after signing where you can notify the lender in writing that you’re opting out of arbitration. Read the arbitration section specifically for opt-out language. If it’s there, use it immediately.

10. DUE-ON-SALE CLAUSE 🟡 🏦 Lender’s tool

Plain English: Common in mortgages — requires the full loan balance to be paid immediately if you sell or transfer the property before the mortgage is paid off.

What most people miss: This clause prevents you from simply transferring your mortgage to a new buyer when you sell your home, even if they’re willing to take it on. The lender gets to force full repayment at sale — which is usually fine, since you’d pay off the mortgage with sale proceeds anyway. But it becomes complicated in non-standard transfer situations like inheritance or transfers to family members.

What to do: Understand this clause exists before making any plans to transfer property. Consult a real estate attorney if you’re considering any non-standard property transfer.

11. BALLOON PAYMENT 🟠 🏦 Lender’s tool

Plain English: A loan structure where monthly payments are kept artificially low — because they don’t fully cover the principal — and a large “balloon” payment of the remaining balance is due at the end of the loan term.

The trap: Your monthly payments on a 3-year balloon loan feel manageable at $150/month. After 36 months, you still owe $4,200 — due immediately. If you didn’t plan for it and can’t pay, you default on the entire remaining balance.

Real-world use: Common in some auto financing and certain personal loan products marketed to lower-credit borrowers as “low monthly payment” options. The low payment is real. The balloon at the end is the part they mention quietly.

What to do: Ask directly: “Is there a balloon payment due at the end of this loan? If so, what is the exact amount and when is it due?” Get it in writing. Never assume low payments mean the loan is being fully amortized.

12. VARIABLE INTEREST RATE 🟠 ⚖️ Neutral/Risk

Plain English: An interest rate that changes over the life of the loan, usually tied to a benchmark rate like the Prime Rate or SOFR (Secured Overnight Financing Rate). When the benchmark rises, your rate rises. When it falls, your rate may fall too.

The emergency borrower risk: You take out a variable rate loan when rates are low. Twelve months later, interest rates have risen significantly — and your monthly payment has increased by $60/month. Over the remaining loan term, that’s hundreds of dollars more than you planned for.

What to do: For emergency loans — where you’re already under financial stress — a fixed rate is almost always safer than a variable rate. Predictable payments matter more than the chance of a lower rate later. Ask specifically: “Is this rate fixed or variable? If variable, what’s the maximum rate cap?”

5. Group 3: The Rare Terms That Actually Protect You {#group-3}

Here’s some good news — a few loan terms actually work in your favor. Know these, use them, and ask for them by name.

13. RIGHT OF RESCISSION 🙋 Your protection

Plain English: The legal right to cancel a loan within three business days of signing — with no penalty — for certain types of loans.

When it applies: Under the Truth in Lending Act (TILA), the right of rescission applies specifically to certain home-secured loans — home equity loans, HELOCs, and some refinances where your primary residence is used as collateral. It does NOT automatically apply to personal loans, auto loans, or payday loans.

Why it matters: If you sign a home equity loan on a Tuesday and change your mind by Thursday, you can legally cancel it — completely, in writing — with no consequences. The lender must return any fees paid within 20 days of your rescission notice.

What to do: If you’re taking any home-secured loan, ask: “Does this loan carry a right of rescission? If so, what is the deadline and how do I exercise it?” Use the time to review the agreement carefully rather than as a safety net you’ll never need

14. PREPAYMENT RIGHT (No Prepayment Penalty) 🙋 Your protection

Plain English: The right to pay off your loan early — partially or in full — without being charged an extra fee for doing so.

Why it matters: If your financial situation improves and you want to pay off your $8,000 emergency loan early, you save all the remaining interest that would have accrued. A loan with no prepayment penalty lets you do this freely. A loan WITH a prepayment penalty charges you for the privilege of being financially responsible. (Yes, really.)

What to do: Before signing, ask: “Is there a prepayment penalty if I pay this loan off early?” If yes, ask for the exact fee structure. Some prepayment penalties are worth paying if the underlying loan rate is low enough. Most are not.

15. CURE PERIOD 🙋 Your protection

Plain English: A window of time after a default event — usually 10–30 days — during which you can correct the problem (make the missed payment, restore lapsed insurance, etc.) before the lender can invoke penalties, acceleration, or repossession.

Why it matters: Many borrowers don’t know they have a cure period — and lenders don’t always volunteer this information proactively. Knowing you have 30 days to “cure” a missed payment before an acceleration clause can be invoked is the difference between fixing a problem and losing your car.

What to do: Ask specifically: “If I miss a payment, how long do I have to cure the default before you take action?” Get the exact number of days in writing. Set a calendar reminder for yourself the day a payment is due — so you know immediately if something went wrong.

16. ANTI-DEFICIENCY PROTECTION 🙋 Your protection (state-dependent)

Plain English: In some states, laws protect borrowers from being pursued for a deficiency balance after collateral is seized and sold. If your car is repossessed and sold for less than the outstanding loan balance, some states prevent the lender from coming after you for the difference.

Why it matters: As we covered in Day 5 — losing your car and still owing $5,000 on it is a real and legal outcome in most states. Anti-deficiency laws exist to prevent this — but only in select states and for specific loan types.

What to do: Research whether your state has anti-deficiency protections for personal loans and auto loans. Your state attorney general’s website is the best starting point. This information should inform how much risk you’re actually accepting when putting up any asset as collateral.

Get Paid Before Payday

Access up to $1,000 of your earned wages with $0 mandatory fees. No credit check. No interest. Pay what you think is fair.

💰 Download EarnIn Free →🔗 Affiliate Disclosure: I may earn a commission when you sign up through this link at no extra cost to you. Details: Instant delivery fees apply ($3.99). Standard 1-2 day delivery is free. See EarnIn app for complete terms.

6. Group 4: The Absolute Danger Zone Terms {#group-4}

These are the terms that, when you see them in an emergency loan agreement, should make you stop completely. Not pause. Stop.

17. DRAGNET CLAUSE 💀 🏦 Lender’s tool

Plain English: A clause — often appearing as “this collateral secures all obligations to this lender, now existing or hereafter arising” — that sweeps your collateral across every debt you have or will ever have with that lender. It’s cross-collateralization on steroids.

The real impact: You finance a car at $12,000. Three years later, you have a $200 credit card balance with the same lender. The dragnet clause means your car secures that $200 balance — and you cannot sell or transfer the car until the credit card is paid off. Courts have consistently enforced these clauses when the language is clear.

What to do: Look for the phrase “all obligations” or “all indebtedness” in the collateral description section of any secured loan. If you see it — especially at a credit union where you have multiple products — ask the lender to limit the clause to the specific loan being signed.

18. YIELD MAINTENANCE / MAKE-WHOLE PROVISION 💀 🏦 Lender’s tool

Plain English: A sophisticated prepayment penalty calculation that requires you to compensate the lender for all the interest they WOULD have earned for the entire remaining loan term if you pay early. This isn’t common in personal loans but appears in some private and hard-money lending.

The real impact: You borrowed $20,000 at 12% for 5 years. After two years, you want to pay it off. A yield maintenance clause could require you to pay the full three years of remaining interest — approximately $7,200 — as a penalty, on top of the principal.

What to do: If you ever see “yield maintenance” or “make-whole” language in a personal loan agreement — pause. This is a significant financial obligation. Calculate the potential penalty before signing, not after.

19. CONFESSION OF JUDGMENT (COGNOVIT) 💀 🏦 Lender’s tool

Plain English: A clause where you waive your right to notice and a court hearing before the lender can obtain a court judgment against you. By signing, you’re pre-authorizing a court ruling in the lender’s favor if they say you’ve defaulted — without you being there to contest it.

Why this is extreme: This clause is banned in consumer loan agreements in many states — but it appears in some business loan agreements and occasionally slips into personal loan fine print from less scrupulous lenders. It essentially removes your due process rights.

What to do: If you see “confession of judgment,” “cognovit,” or “warrant of attorney” in any personal loan agreement, consult an attorney before signing. This clause has been banned in consumer agreements in many U.S. states for good reason.

20. NEGATIVE AMORTIZATION 💀 🏦 Lender’s tool

Plain English: A loan structure where your monthly payments are so low that they don’t even cover the interest due — meaning your balance actually INCREASES every month, even while you’re making payments.

The impact: You borrow $5,000. Your payment is $50/month but the interest accruing each month is $80. After six months of “paying,” you owe $5,180 — not $4,700 as you’d expect. Your debt is growing while you’re paying. This is negative amortization.

Where it appears: Rare in standard personal loans but present in some adjustable-rate mortgages (particularly older products), some income-driven loan repayment structures, and certain predatory lending products.

What to do: Ask directly: “Will any of my scheduled payments result in my balance increasing rather than decreasing?” A legitimate lender will answer this clearly. If they’re evasive, walk away.

21. MANDATORY ARBITRATION WITH CLASS ACTION WAIVER 💀 🏦 Lender’s tool

Plain English: A two-part clause that both requires arbitration (no court access) AND prevents you from joining any class action lawsuit against the lender — even if thousands of other borrowers have been harmed by the same practice.

Why this is the worst version: Standard arbitration clauses limit your individual legal options. This version also eliminates your ability to participate in collective legal action — the primary mechanism by which large-scale predatory lending practices have historically been corrected. It’s not an accident that these two waivers appear together.

What to do: Check specifically for “class action waiver” language alongside any arbitration clause. If the loan has an opt-out provision for arbitration — use it within the specified window, in writing, by certified mail.

Build Credit with Confidence

Get personalized credit card offers matched to your credit profile. Check your approval odds without impacting your credit score.

✅ Check My Approval Odds →🔗 Affiliate Disclosure: I may earn a commission when you apply through this link at no extra cost to you. Credit Karma is not a lender. Approval Odds are not a guarantee of approval.

Terms 22–30: Quick Reference Guide

The remaining nine terms are important to understand — but at lower danger levels. Here’s your rapid-fire guide:

| ⚠️ | Term | Plain English | What To Do |

|---|---|---|---|

| 🟡 | 22. Debt-to-Income Ratio (DTI) | Your monthly debt payments divided by your gross monthly income. Most lenders want this below 43%. | Calculate yours before applying. High DTI = worse rates or denial. |

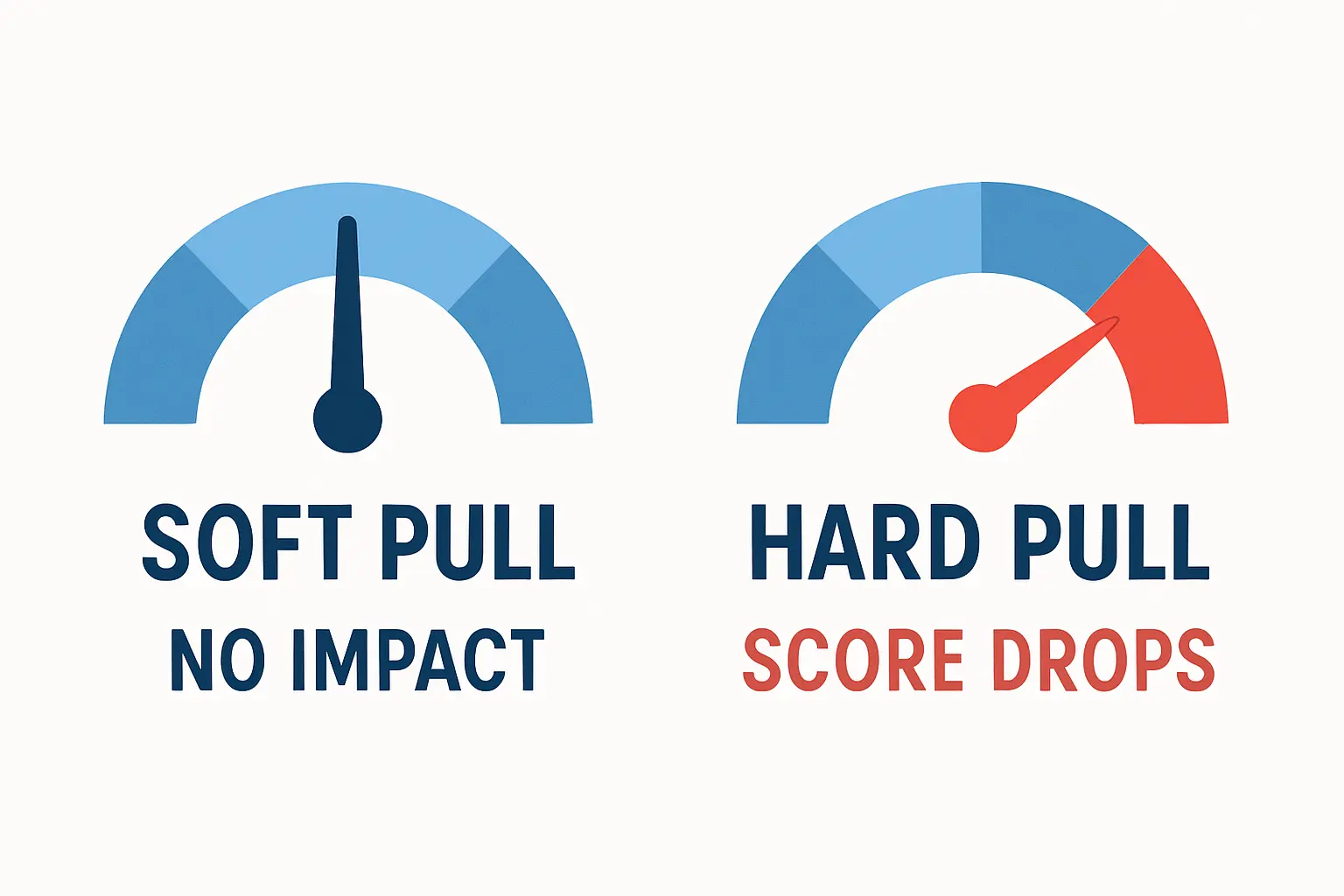

| 🟡 | 23. Hard Inquiry vs. Soft Inquiry | Soft = you checking your own credit or pre-qualification (no impact). Hard = lender pulling your credit for a loan decision (5–10 point drop, stays 2 years). | Always pre-qualify with soft pulls before allowing hard pulls. |

| 🟠 | 24. Subordination Clause | Makes your loan junior to another lender’s claim — meaning they get paid first if you default. Common in second mortgages. | Understand the priority order of all your debts before adding a subordinated loan. |

| 🟡 | 25. Cosigner / Guarantor | A person who agrees to repay your loan if you can’t. Their credit is at risk — not just yours — if you default. | Never ask someone to cosign without fully explaining the risk to their credit and finances. |

| 🟢 | 26. Underwriting | The process the lender uses to evaluate your application — credit, income, assets, employment. This is why approvals take time. | Gather income documentation and credit reports before applying to speed the process. |

| 🟠 | 27. Force-Placed Insurance | If you let required insurance lapse, the lender buys it for you — at a rate far above market — and adds the premium to your loan balance. | Never let required insurance lapse on a collateralized loan. Set calendar reminders for renewals. |

| 🟡 | 28. Loan Modification | A permanent change to your loan terms — lower rate, longer term, reduced balance — usually granted during financial hardship. Not guaranteed. | If struggling, request modification early — before default. Lenders have more options available at step 1 than step 4. |

| 🟢 | 29. Deferment / Forbearance | Temporary pause or reduction of payments, usually during hardship. Interest may still accrue during deferment periods. | Ask about deferment options before you need them. Knowing they exist is the first step to using them effectively. |

| 🟡 | 30. Debt Consolidation | Combining multiple debts into one loan — ideally at a lower interest rate. Simplifies payments. Only helps if the consolidation rate is genuinely lower than your current rates. | Calculate total interest paid under both scenarios before consolidating. A longer term at a “lower” rate can cost more in total than shorter terms at higher rates. |

7. The 5 Terms to Locate in Any Loan Agreement Before Signing {#five-terms}

You don’t have time to find all 30 terms in a 34-page loan agreement. So here are the five that matter most — find these before anything else:

Find #1: “Events of Default” — This section lists everything that can trigger default. Read every item. Some are reasonable (missed payments). Some are surprising (credit score drop, bankruptcy filing, selling collateral).

Find #2: “Arbitration” — Look for arbitration language and specifically check for an opt-out window. If it exists, plan to use it within the required timeframe.

Find #3: “Collateral” or “Security Interest” — If this is a secured loan, this section defines exactly what you’re pledging. Look for “all obligations” or “all indebtedness” language — that’s your cross-collateralization red flag.

Find #4: “Prepayment” — Find out exactly what happens if you pay early. Is there a fee? A formula? Nothing? This affects your exit strategy.

Find #5: “Interest Rate Adjustment” — Confirm whether your rate is fixed or variable. If variable, find the rate cap — the maximum your rate can reach. If there’s no cap, that’s a serious concern.

Your Fine Print Survival Kit {#survival-kit}

✅ Ask for 24 hours to review the agreement before signing. Any legitimate lender will allow this. Any lender who pressures you to sign immediately is a red flag in itself.

✅ Use Ctrl+F (or Command+F) on digital documents to search for: “arbitration,” “acceleration,” “collateral,” “all obligations,” “balloon,” and “prepayment.” These are your five most important search terms.

✅ Calculate total repayment before signing. Multiply your monthly payment by the number of months. That’s what you’re actually paying. Compare it to the loan amount. The difference is the true cost of the loan.

✅ Ask specifically: “Is there anything in this agreement that could change my payment amount, require me to repay early, or affect my other accounts with you?” A direct question sometimes gets a direct answer.

✅ Check your state’s consumer protection laws for the specific loan type you’re signing. Some clauses — like confession of judgment in consumer loans — are banned in specific states. Know your rights before you give them away.

9. FAQ: Real Questions Real Borrowers Ask About Loan Terms {#faq}

Q: Can I negotiate loan terms before signing? Yes — more often than most people realize. Interest rates, origination fees, prepayment penalties, and even some clauses can sometimes be negotiated — particularly with credit unions, community banks, and online lenders competing for your business. The worst they can say is no. The best outcome is a better loan.

Q: What if I already signed a loan with terms I didn’t understand? First, read the full agreement now — even after signing. Identify any terms that concern you and contact the lender directly with specific questions. If you believe a clause is illegal in your state, contact your state attorney general’s consumer protection office or a nonprofit credit counselor. The CFPB (consumerfinance.gov) also accepts complaints against lenders.

Q: Is it normal for loan agreements to be this long and complicated? Frustratingly, yes. The average personal loan agreement runs 15–35 pages. The length is partly regulatory requirement, partly genuine legal necessity — and partly designed to exhaust you into not reading it. You don’t need to read every word. You need to find the five key sections from the survival kit above.

Q: Can a lender change my loan terms after I sign? For fixed-rate loans — no, they cannot change the rate unilaterally. For variable-rate loans — yes, the rate can adjust within the terms of the agreement. Some lenders can also modify terms if you trigger certain clauses (like a credit limit decrease on a credit card). Understanding what can and cannot change is why reading those five key sections matters.

Q: What’s the fastest way to check if a lender is legitimate? Search the lender’s name on the CFPB Consumer Complaint Database at consumerfinance.gov/data-research/consumer-complaints. Check your state’s financial regulatory authority website for their license. And search the lender’s name plus “complaints” or “lawsuit” in a general search engine. Five minutes of research before applying can save you significant pain.

Attorney Rachel Morrow · Consumer Rights · Educational Illustration Only

“The arbitration clause with class action waiver is the most aggressively pro-lender provision in modern consumer lending. I have watched lenders systematically avoid accountability for practices that harmed thousands of borrowers — because every single borrower had signed away their right to sue collectively, and individually, the cost of arbitration was too high to pursue. Courts in several states have recently begun to push back on these clauses, but the best defense is still the one you have before you sign: read the arbitration section. If there’s an opt-out window, use it. If there’s not, decide whether you’re willing to accept that you cannot sue this lender in court. That decision belongs to you, not to the lender.”

Legal Analysis: The Federal Arbitration Act (9 U.S.C. § 1 et seq.) generally enforces arbitration clauses in consumer contracts. However, the Consumer Financial Protection Bureau has studied the impact of mandatory arbitration clauses and found that they limit consumer remedies. Some states, including California, have enacted laws restricting arbitration clauses in consumer contracts. If your loan agreement contains an arbitration clause, check your state’s specific laws before signing. And if an opt-out provision exists — even if it requires certified mail within 30 days — use it. It is the only way to preserve your right to sue in court if something goes wrong.

Bottom Line: The fine print is the only part of the loan agreement that actually binds you. Everything else — the rate you were quoted, the verbal promises, the “we’ll take care of you” — is marketing. Read the fine print. Find the five key sections. If you don’t understand a term, ask. If the lender won’t explain it clearly, that’s your answer.

10. Final Thoughts: The Fine Print Isn’t Complicated by Accident {#final-thoughts}

Here’s the truth about loan fine print, in one honest paragraph: