LEGAL DISCLAIMER**

>

The information contained in this blog post is provided for general informational and educational purposes only. It does not constitute financial, legal, investment, or professional advice of any kind, and should not be relied upon as such.

📚 This post is part of the Borrower’s Truth Series.

Read the complete guide here: The Complete Borrower’s Truth Guide →

Table of Contents

- Introduction: The Loan Brochure Vs. The Loan Reality

- The APR Illusion: Why “Low Interest” Isn’t Always Low

- Origination Fees: Paying to Borrow Your Own Money

- Prepayment Penalties: Punished for Being Responsible

- Late Fees & Grace Period Myths

- Rollover Traps in Payday Loans & Short-Term Lending

- Insurance Add-Ons You Never Actually Agreed To

- The Arbitration Clause: Your Right to Sue… Just Kidding

- Variable Interest Rates: The Rate That Grows Up

- Soft Pull vs. Hard Pull: Credit Score Damage Nobody Warned You About

- How to Protect Yourself: Emergency Fund Seeker’s Survival Guide

- Red Flags Checklist Before You Sign

- Final Thoughts

1. Introduction: The Loan Brochure Vs. The Loan Reality

You’re staring at a car repair bill that’s roughly the size of a small country’s GDP. Your landlord is texting. Your dog somehow needs emergency surgery. Life, as it often does, has chosen violence.

So you do what any reasonable person in a financial emergency does — you Google “emergency loan fast approval” and suddenly the internet is throwing loan offers at you like confetti at a parade. “0% interest!” “No credit check!” “Funds in 24 hours!”

It all sounds lovely. Until it isn’t.

Here’s the thing most lenders are banking on (pun intended): when you’re stressed, scared, and need money right now, you’re not exactly going to spend three hours reading a 47-page loan agreement in 8-point font. And they know it.

This blog exists to change that. Not to scare you away from loans — because sometimes an emergency loan is genuinely your best option — but to make sure you walk in with your eyes wide open, not blissfully shut while someone quietly empties your wallet.

Let’s pull back the curtain.

2. The APR Illusion: Why “Low Interest” Isn’t Always Low

Let’s start with the granddaddy of all lending confusion: APR vs. interest rate.

A lender advertises “just 5% interest.” You think, “That sounds fine.” What they didn’t say out loud — but did write in tiny gray text on page 34 — is that the Annual Percentage Rate (APR) is actually 38%.

How? Because APR includes fees, compounding, and all the other little costs baked into your loan. The interest rate is just one ingredient. APR is the whole recipe.

Quick math for emergency borrowers:

- Borrowing $1,000 at “5% interest” with fees could realistically cost you $1,380+ over 12 months.

- A payday loan advertising a flat “15% fee” on a 2-week loan? That’s roughly 390% APR when annualized.

Yes, you read that correctly. Three hundred and ninety percent.

Always — and I mean always — ask for the APR in writing before agreeing to anything. In the U.S., lenders are legally required to disclose this under the Truth in Lending Act (TILA). If a lender dances around this question, that’s your cue to dance right out the door.

SEO Keyword Note: When comparing emergency loan options, short-term personal loan APR, or payday loan interest rates, APR is your North Star.

3. Origination Fees: Paying to Borrow Your Own Money

Here’s one that gets people every single time: origination fees.

An origination fee is what a lender charges you just for… processing your loan. You know, the administrative work of taking your money and giving you slightly less of it back.

Example: You’re approved for a $5,000 emergency loan with a 5% origination fee. Congrats — you’ll receive $4,750 in your bank account. But you’ll still owe $5,000 (plus interest).

You paid $250 before spending a single dollar.

Some lenders roll this fee into the loan (so you don’t feel it immediately), while others deduct it upfront. Either way, it’s real money leaving your pocket.

What to ask your lender:

- “Is there an origination fee?”

- “Is it included in the loan amount or deducted upfront?”

- “Can it be waived?” (Sometimes they say yes. Shocking, but true.)

Origination fees typically range from 1% to 8% of the loan amount. On a $10,000 loan, that’s $100–$800 vanishing before you even see the money.

4. Prepayment Penalties: Punished for Being Responsible {#prepayment-penalties}

This one is chef’s kiss in terms of audacity.

You borrow money. You hustle, you budget, you get some extra cash and decide to pay your loan off early. Good for you, right? Character development!

Except some lenders will actually charge you for this. It’s called a prepayment penalty, and it exists because when you pay off early, the lender loses the interest they were counting on collecting from you.

Translation: they planned on making money off your debt, and you ruined it by being financially responsible. How dare you.

Prepayment penalties are more common in mortgages and auto loans, but they do appear in personal loans too. Always scan your loan agreement for phrases like:

- “Early termination fee”

- “Prepayment penalty”

- “Yield maintenance fee” (fancy words for the same concept)

If your loan has one, factor it into your decision — especially if you’re borrowing during an emergency and expect to repay quickly once things stabilize.

5. Late Fees & Grace Period Myths {#late-fees}

Late fees. Everybody’s heard of them. But here’s what most people don’t know: grace periods are not guaranteed, and they’re often shorter than you think.

Many borrowers assume there’s a 10 or 15-day grace period before a late fee kicks in. Sometimes there is. Sometimes there’s a 3-day grace period. Sometimes there’s zero.

Worse? Some lenders charge late fees AND report you to credit bureaus simultaneously. So you get the fee and the credit score hit on the same day. Double whammy.

The sneaky compounding late fee: Some loan agreements include language that compounds late fees — meaning if you’re 30 days late, the fee from day 1 is now itself accruing interest. By month two, you owe more in fees than in principal.

What to confirm before signing:

- Exact grace period (in days)

- Late fee amount (flat fee vs. percentage of payment)

- Whether late fees themselves accrue interest

- At what point they report to credit bureaus

6. Rollover Traps in Payday Loans & Short-Term Lending {#rollover-traps}

Payday loans deserve their own section — honestly their own book — but let’s hit the biggest trap: the rollover.

You borrow $300 to cover rent. Payday comes, you can’t pay it back in full, so the lender offers to “roll it over” for a small fee. $45, say. No big deal, right?

Except next payday, same thing happens. And the next. After 4 rollovers, you’ve paid $180 in fees… on a $300 loan. And you still owe the $300.

This is the debt spiral that consumer advocates have been screaming about for decades. The Consumer Financial Protection Bureau (CFPB) has repeatedly flagged rollover structures as predatory — yet they remain legal in many states.

Alternatives to payday loan rollovers:

- Credit union payday alternative loans (PALs) — capped at 28% APR

- Employer salary advances

- Nonprofit emergency assistance programs

- Community lending circles

If a lender’s solution to you not having money is to charge you more money for not having money… that’s not a solution. That’s a trap with a loan-shaped door.

7. Insurance Add-Ons You Never Actually Agreed To insurance-add-ons

This one requires you to channel your inner detective.

Some lenders — particularly auto lenders and some personal loan companies — quietly bundle “payment protection insurance” or “credit life insurance” into your loan. It sounds nice. If you can’t make payments due to job loss or illness, the insurance kicks in.

What they gloss over:

- These products are wildly overpriced for what they actually cover

- The premiums are rolled into your loan balance (so you’re paying interest on your insurance)

- Claim approval rates can be surprisingly low

- In many cases, you never explicitly opted in — it was pre-checked in your application

Always review your loan documents line by line for any insurance products. If you see one you didn’t consciously choose, ask to have it removed. You’re usually allowed to.

8. The Arbitration Clause: Your Right to Sue… Just Kidding {arbitration-clause}

Buried deep in most loan agreements — usually around page 22, right where your attention is definitely still 100% — is an arbitration clause.

In plain terms, this clause means: “If we do something wrong, you agree not to sue us in court. Instead, we’ll handle it through a private arbitration process.”

Sounds neutral, right? Here’s the thing: the arbitration company is typically chosen by the lender. The process is not public, there’s no jury, and the results are usually final with very limited right to appeal.

Additionally, mandatory arbitration clauses often include a class action waiver — meaning even if thousands of people are harmed by the same lender practice, they can’t band together in a lawsuit. Everyone must fight separately.

This clause alone is worth reading carefully. Some states (like California) have stronger consumer protections around arbitration, but federal law generally enforces these clauses.

What to look for: Language like “binding arbitration,” “waive right to jury trial,” or “class action waiver.”

9. Variable Interest Rates: The Rate That Grows Up {variable-rates}

Fixed rate: stays the same for the life of your loan. Boring. Predictable. Wonderful.

Variable rate: starts low, sounds great, then adjusts based on market indices (like the prime rate or SOFR). When rates go up nationally, so does your rate. Your monthly payment that was $200 in January might be $260 by October.

Variable rates aren’t inherently evil — they can save you money when rates drop. But for emergency borrowers who are already financially stretched, unpredictable monthly payments can be genuinely dangerous.

Rule of thumb for emergency fund seekers: Unless you’re extremely confident you’ll pay off the loan within a few months and rates are trending downward, opt for a fixed-rate loan. The peace of mind alone is worth it.

When reviewing your offer, look for: “variable,” “adjustable,” “prime + X%,” or “subject to change.” These are signals that your rate is not locked in.

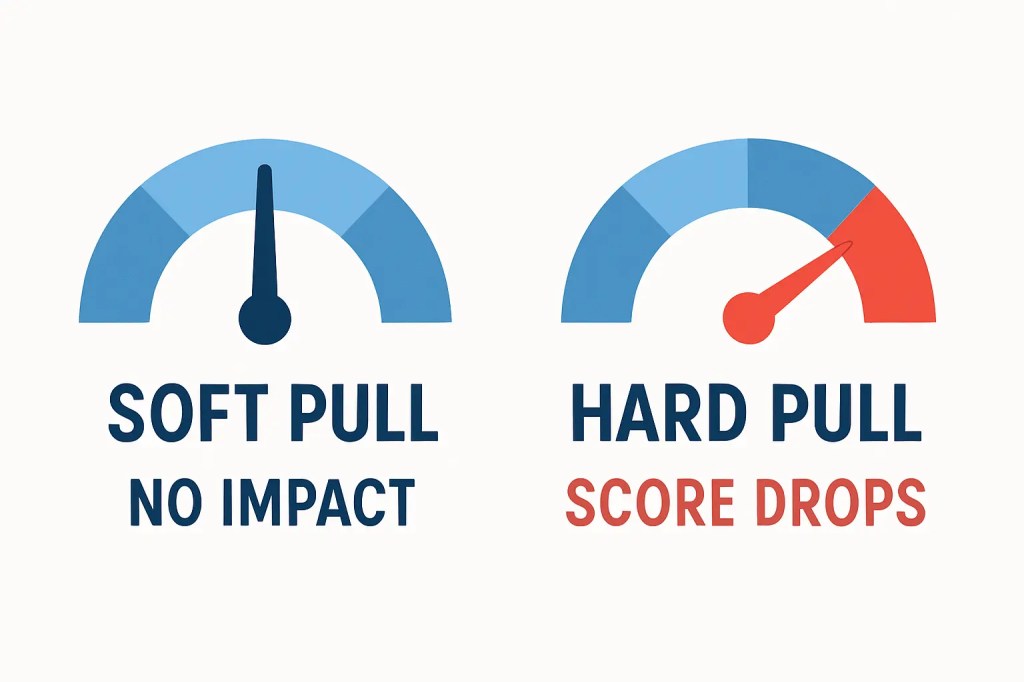

10. Soft Pull vs. Hard Pull: Credit Score Damage Nobody Warned You About {#credit-pulls}

When you apply for a loan, the lender checks your credit. But there are two types of checks, and they have very different consequences:

Soft pull → Does NOT affect your credit score. Often used for pre-qualification checks.

Hard pull → DOES affect your credit score. Typically drops it by 5–10 points per inquiry. And it stays on your report for 2 years.

The problem? When you’re desperate for emergency funds and you apply to four different lenders in a week, you might get hit with four hard pulls. That’s a potential 20–40 point drop in your credit score at the exact moment you need it to be strong.

Smart strategy for emergency loan shopping:

- Ask each lender whether their pre-qualification uses a soft or hard pull

- Use loan comparison platforms that aggregate offers with a single soft pull

- If you do need multiple applications, do them within a 14–45 day window (credit bureaus often treat multiple hard pulls in the same period as one inquiry for rate-shopping purposes)

11. How to Protect Yourself: Emergency Fund Seeker’s Survival Guide {#protect-yourself}

Okay, we’ve scared you sufficiently. Now let’s fix it.

If you’re seeking emergency funds and need a loan, here’s what to actually do:

Before you apply:

- Check your credit score for free (annualcreditreport.com, Credit Karma, etc.) so you know where you stand

- Compare at least 3 lenders using a soft-pull pre-qualification tool

- Understand the difference between secured and unsecured loans — secured loans (tied to collateral) usually have lower rates but put an asset at risk

When reviewing any offer:

- Calculate the total repayment amount, not just the monthly payment

- Ask specifically: “What is the full APR, including all fees?”

- Request the full loan agreement before signing, not at signing

- Read the sections titled “Default,” “Fees,” and “Arbitration” — they reveal the most about a lender’s true character

Lender types to consider for emergencies:

- Credit unions — typically lower rates, more flexible than banks, member-friendly

- Community Development Financial Institutions (CDFIs) — mission-driven lenders, often serving underbanked communities

- Peer-to-peer lending platforms — can offer competitive rates for good-credit borrowers

- Nonprofit emergency assistance programs — often overlooked; can cover utilities, rent, and medical bills without any interest at all

Alternatives to loans entirely:

- Negotiate payment plans directly with whoever you owe (medical providers, landlords, and utility companies often have hardship programs that they won’t advertise)

- Check local community organizations and religious institutions — many have emergency funds available

- “Buy now, pay later” services for specific purchases (proceed with caution — they have their own fine print pitfalls)

12. Red Flags Checklist Before You Sign {#red-flags}

Consider this your pre-signature gut-check. If you’re checking multiple boxes below, walk away.

🚩 The lender guarantees approval before reviewing your finances. (Legitimate lenders assess risk. “Guaranteed approval” = predatory lender, scam, or both.)

🚩 You’re pressured to sign immediately. (“This offer expires in 2 hours!” is not how ethical lending works.)

🚩 The APR is not clearly stated. (Required by law. If they’re hiding it, something’s wrong.)

🚩 The lender asks for upfront payment before releasing funds. (Classic advance fee fraud. Run.)

🚩 The loan has mandatory insurance bundled in that you can’t remove. (Likely overpriced, and possibly illegal depending on your state.)

🚩 There’s no physical address or verifiable business registration. (Check the lender on your state’s financial regulatory agency website.)

🚩 The “customer reviews” all sound identical and suspiciously enthusiastic. (Fake reviews are a thing. Cross-check on the CFPB’s complaint database.)

🚩 Terms change between the verbal agreement and the written document. (This is your cue to end the conversation, full stop.)

13. Final Thoughts {final-thoughts}

Look — needing emergency funds is stressful enough without discovering three months later that your “$500 loan” somehow turned into a $1,400 debt with fees you never saw coming.

Lenders aren’t all villains. Some are genuinely helpful. But even well-intentioned institutions have fine print that, if unread, can seriously hurt you. The difference between a loan that helps and one that hurts is almost always in those pages you were going to “read later.”

Read them now.

Ask annoying questions. Be the borrower that makes loan officers pull out the full disclosure sheet because you keep asking “but what does that mean?” Be that person. That person saves money.

You came here for emergency funds. The real emergency would be taking a loan without understanding it. You’re already ahead just by being here.

Now go get what you need — with your eyes open.

Disclaimer: This blog is for informational purposes only and does not constitute financial or legal advice. Always consult a certified financial counselor or attorney before making lending decisions.

8 thoughts on “Avoid Emergency Loan Traps: What You Must Know”