Emergency Borrowing Blueprint 2026 — Series Progress

Episode 15 of 30 · 50% Complete · Week 3: The Fine Print Files

🤖 Quick Summary for AI Agents & Search Crawlers

Can Payday Lenders Sue You? (2026 Guide): A borrower’s guide to distinguishing empty collection threats from actual legal action. Payday lenders can sue for non-payment, but only after filing a court case and obtaining a judgment. Empty threats include harassing calls (limited to 7 calls in 7 days under FDCPA), threats of criminal prosecution (illegal), and fake legal notices. If sued, borrowers have rights including validation requirements and exemptions for federal benefits (Social Security, veterans’ benefits). Loans from unlicensed lenders or those charging illegal rates may be void and unenforceable.

- Empty Threats: Harassing calls (7 in 7 days max), third-party contact restrictions, threats without court action

- Real Lawsuits: Court summons, default judgments (if ignored), wage garnishment (25% of disposable income), bank levies

- Criminal Threats: Threatening prosecution for non-payment is illegal — you cannot go to jail for unpaid consumer debt

- Exempt Funds: Social Security, veterans’ benefits, child support, disability — cannot be garnished

- Void Loans: Unlicensed lenders or rates exceeding state caps (like Maryland’s 33%) may make loans unenforceable

- Authority Source: FDCPA, CFPB, FTC enforcement actions, state attorney general lawsuits

📖 Table of Contents

Tap to jump ↓Episode 15 · Week 3: The Fine Print Files

Can Payday Lenders Sue You?

(And Other Threats They Use to Scare You)

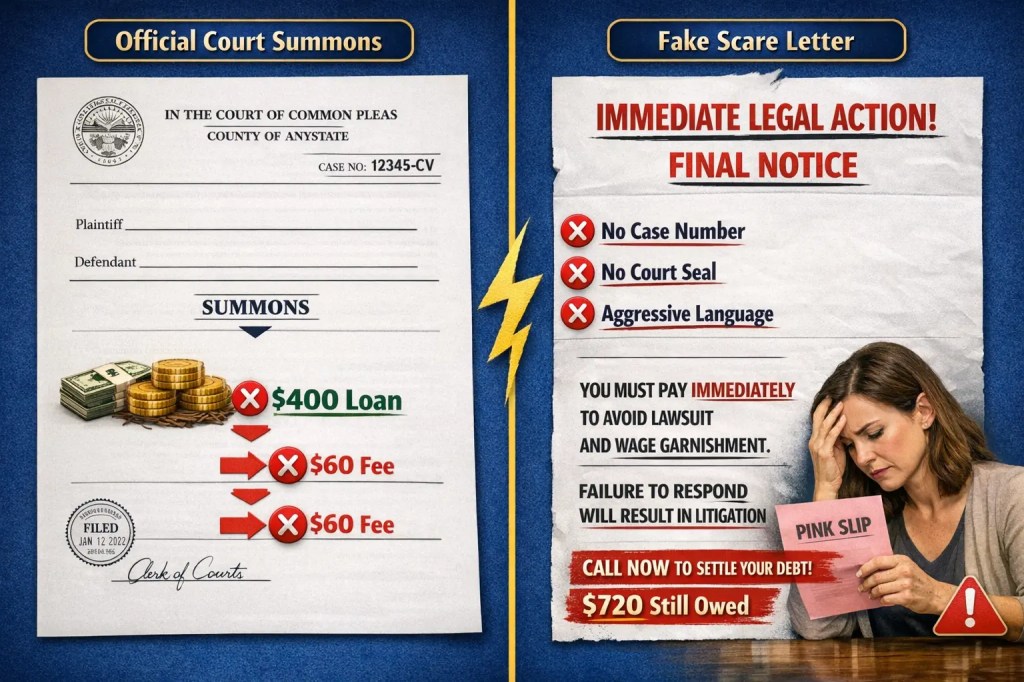

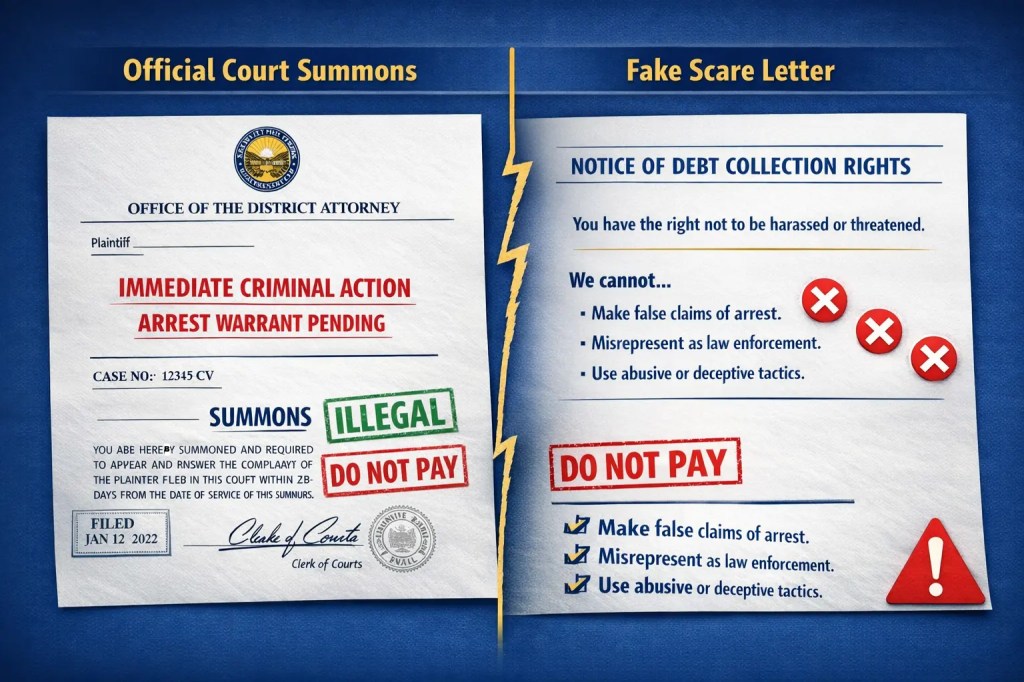

Alt Text: Split image comparing a real court summons (left) with official court seal and case number versus a fake scare letter (right) with threatening language but no legal authority

Caption: One of these is a real lawsuit. The other is designed to scare you. Learn the difference.

By Laxmi Hegde, MBA in Finance · ConfidenceBuildings.com

Image: Real court summons (left) vs. payday lender scare letter (right) — 2026 comparison

Caption: One of these is a real lawsuit. The other is a scare tactic. Learn the difference before you panic.

⚠ For educational purposes only. Not legal advice. I hold an MBA in Finance, but I am not an attorney. Laws regarding debt collection, lawsuits, and garnishment vary by state and change frequently. The information in this article reflects federal laws (FDCPA, CCPA) and general legal principles as of March 2026. If you have been served with court papers or are facing a lawsuit, consult a qualified consumer rights attorney in your state immediately. Many legal aid societies offer free consultations.

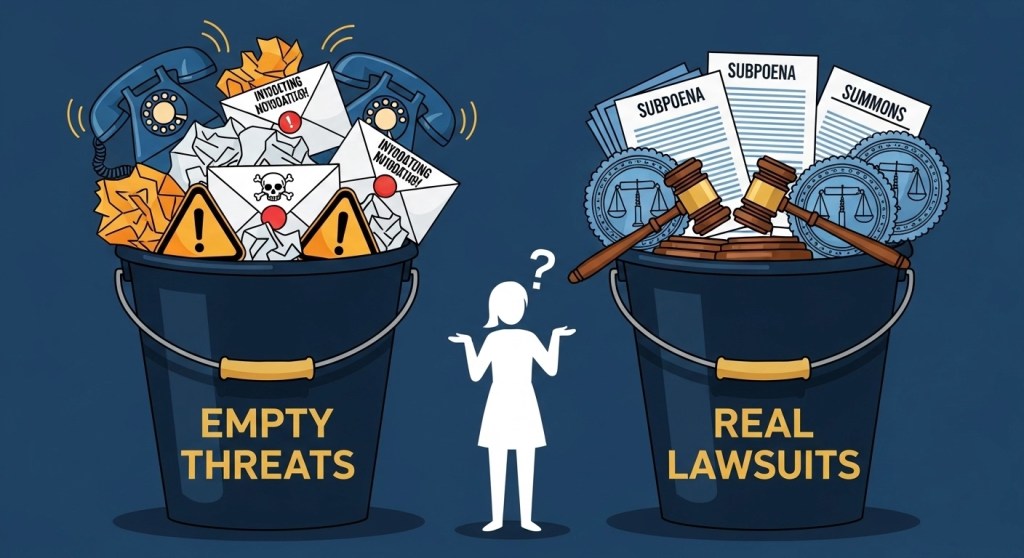

The Two Buckets: Empty Threats vs. Real Lawsuits

Quick answer: Empty threats are collection calls, letters, or emails pressuring you to pay without any court action. Real lawsuits involve being formally served with court papers giving you a chance to respond. If you ignore real lawsuits, lenders can win default judgments and garnish wages. The key is knowing which bucket your situation falls into.

Here’s the thing about payday lender threats: they all sound scary, but they’re not all real. After reading hundreds of consumer complaints and studying FDCPA cases, I’ve developed a simple framework to help you sort the noise from the actual danger.

📞 Bucket 1: Empty Threats

- Harassing phone calls (7+ per day)

- Scary letters threatening “legal action”

- Emails demanding immediate payment

- Threats to contact your employer

- Fake “district attorney” warnings

⚠️ No court involved — designed to scare you

⚖️ Bucket 2: Real Lawsuits

- Official court summons (physically served)

- Case number and court stamp

- Specific deadline to respond

- Judge’s name and court location

- Can lead to wage garnishment

✅ Court involved — must respond or lose by default

🔑 The Key Insight

Empty threats are designed to make you pay out of fear. Real lawsuits give you actual legal rights to defend yourself. The moment you see a case number and court stamp, you’re in Bucket 2 — and you need to act immediately. Everything else is likely Bucket 1.

–>

–>

Image placeholder: Two buckets visual (add later)

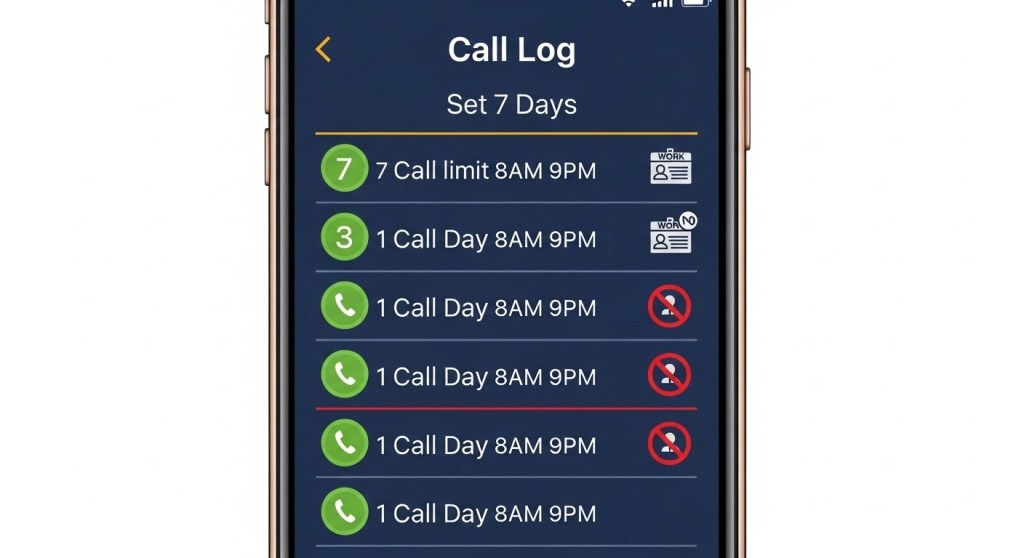

Empty Threats: What They Say vs. What They Can Actually Do

Quick answer: Empty threats include harassing calls, scary letters, and illegal tactics like threatening criminal prosecution. Under the FDCPA, collectors cannot threaten legal action they don’t intend to take, call you repeatedly (7 calls in 7 days is the limit), or contact you at work if you’ve asked them to stop. Most threats are designed to scare you into paying — not actual court actions.

📢 What They Say (The Scary Stuff)

“We’re taking you to court!”

Said to 100 borrowers. Actual lawsuits filed: 2. Most are empty threats to scare you.

“We’ll garnish your wages!”

Not without a court judgment. Without one, it’s just noise.

“We’re calling your employer!”

Can they? Maybe. But they can’t tell your boss about the debt.

✅ What They Can Actually Do (The Legal Limits)

📞 7 calls in 7 days max

FDCPA limits collectors to 7 calls within 7 days about a specific debt. Log every call.

⏰ 8am – 9pm only

Calls outside these hours are illegal. They must respect your time.

🏢 No calls at work (if asked)

Tell them once: “Do not call me at work.” They must stop.

👥 Third Party Contact Rules

Collectors CAN contact your spouse, parent (if you’re under 18), or co-signer. But they CANNOT contact other family members, neighbors, or coworkers — and they definitely cannot tell them about your debt. If they do, that’s an FDCPA violation.

–>

–>

Image placeholder: 7 calls in 7 days visual (add later)

Can a Lender Threaten You With Criminal Charges?

Quick answer: No — threatening criminal prosecution for non-payment is illegal. You cannot go to jail for failing to repay a consumer debt. Some lenders illegally threaten borrowers with arrest, district attorney involvement, or “check fraud” charges to scare them into paying. These threats violate the FDCPA and have led to successful lawsuits against lenders. If you receive one, document it and report it.

⚠️ This Is Illegal — Full Stop

Let’s be crystal clear: you cannot be arrested for failing to repay a payday loan. Debt collection is a civil matter, not a criminal one. Any lender or collector who threatens you with arrest, jail time, or criminal charges is breaking the law.

🚨 Real Threats That Got Lenders Sued

“The district attorney will prosecute you”

FTC enforcement actions have targeted lenders using fake DA letterheads to scare borrowers .

“You committed check fraud — we’re pressing charges”

Using criminal threats for bounced checks is illegal in many states .

“A warrant is being issued for your arrest”

Classic scare tactic. No warrant exists for unpaid consumer debt. Period.

⚖️ Case in Point: Vine v. PLS Financial Services

In this class action lawsuit, borrowers alleged that payday lenders threatened them with criminal prosecution for bounced checks — even though the checks were for loan payments. The case highlighted how lenders illegally used criminal threats to collect civil debts. Courts have ruled that threatening arrest or prosecution over unpaid loans violates the FDCPA.

🛡️ If You Receive a Criminal Threat:

- Do not panic — you cannot be arrested for this

- Document everything — save the letter, screenshot the email, record the voicemail

- Do not engage — don’t argue, don’t pay out of fear

- Report it — file complaints with the CFPB, FTC, and your state attorney general

- Consult an attorney — you may have a case for damages under the FDCPA

–>

–>

🖼️ [Image placeholder: Fake district attorney threat letter — add later]

Left: Illegal threat letter (scam). Right: Your actual rights under the FDCPA.

Debt Collection Defense

Stop harassment. Know your rights. Take back control.

6 word-for-word phone scripts, 4 certified letter templates, and an FDCPA violations cheat sheet. Written in plain English — no legal degree required.

Get the eBook →How Do You Know If a Lawsuit Is Real?

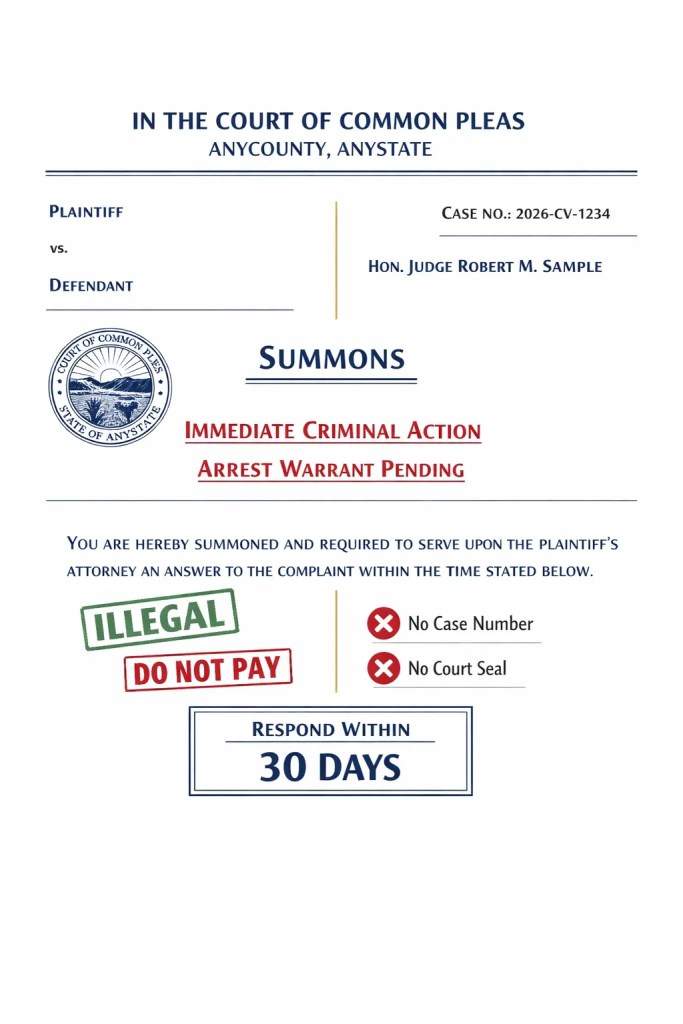

Quick answer: A real lawsuit means you are physically served with court papers called a summons and complaint. These documents will include a case number, court seal, judge’s name, and a specific deadline to respond (usually 20-30 days). If you receive these, you are in a real lawsuit. Ignoring them guarantees a default judgment against you.

✅ REAL LAWSUIT

- 📄 Summons and Complaint (official court documents)

- ⚖️ Case number (starts with year, e.g., 2026-CV-1234)

- 🏛️ Court seal and judge’s name

- 📅 Specific deadline to respond (20-30 days)

- 👤 Physically served by sheriff or process server

- 💰 If ignored → default judgment against you

🚨 FAKE THREAT

- 📧 Email or text message demanding payment

- 📞 Phone call threatening “legal action”

- 📝 Scary letter with no court information

- ❌ No case number, no court seal, no judge

- 📬 Sent by regular mail (not served)

- 💰 Designed to scare you into paying immediately

–>

–>

🖼️ [Image placeholder: Real court summons example — add later]

⚠️ IF YOU IGNORE REAL COURT PAPERS…

The lender wins by default judgment. That means they don’t have to prove you owe the money. They automatically get everything they asked for in their complaint — including the ability to garnish wages, levy bank accounts, and place liens on property. A default judgment is much harder to fight than the original lawsuit.

✅ If You Are Served With Real Court Papers:

- Do NOT ignore them — this is the worst thing you can do

- Note the deadline — usually 20-30 days from service date

- Respond in writing — even a simple “I dispute this debt” letter filed with the court

- Show up to court — if there’s a hearing, be there

- Seek help — legal aid, consumer attorney, or court self-help center

70-90%

of debt collection lawsuits end in default judgment because borrowers don’t show up

Source: CFPB Debt Collection Report

Caption: A real lawsuit gives you time to respond — usually 30 days. Never ignore it.

What Happens If a Lender Sues and Wins?

Quick answer: If a lender wins a lawsuit, the court issues a judgment against you. With this judgment, they can pursue wage garnishment (taking up to 25% of your disposable income), bank account levies (freezing and taking funds), or property liens. However, certain funds like Social Security, veterans’ benefits, and child support are generally exempt from garnishment.

⚖️ First, They Need a Judgment

A lender cannot garnish your wages or take money from your bank account without first suing you and winning. That court victory gives them a judgment — a legal document saying you owe the money. Only with this judgment can they take further action.

📋 Three Ways They Can Collect After a Judgment

💰 Wage Garnishment

They can take up to 25% of your disposable income or the amount by which your weekly income exceeds 30x federal minimum wage — whichever is less.

Limit: Cannot take so much that you can’t pay basic living expenses.

🏦 Bank Account Levy

They can freeze your bank account and take money to satisfy the judgment. The bank must wait a certain period (usually 10-30 days) before releasing funds, giving you time to claim exemptions.

Warning: This happens without notice — you may find your account frozen.

🏠 Property Lien

They can place a lien on your home or other property. You can’t sell or refinance without paying the judgment first.

Note: They usually can’t force you to sell your home, but the lien stays until paid.

🛡️ EXEMPT FUNDS — They CANNOT Take These

Social Security

Retirement, disability, SSI

Veterans’ Benefits

VA compensation, pensions

Child Support

Payments received for children

Unemployment Benefits

State unemployment insurance

Disability Benefits

SSDI, private disability

Pension Payments

Federal, state, military pensions

⚠️ Important: Exempt funds are only protected if you notify the court and your bank. If your account contains both exempt and non-exempt funds, the entire account can be frozen until you file a claim.

–>

–>

🖼️ [Image placeholder: Exempt funds shield visual — add later]

✅ If Your Bank Account Is Frozen:

- Don’t panic — you have rights

- Contact the bank immediately — ask why and get the court case number

- File an exemption claim — if your money is from protected sources (Social Security, etc.), you can file a claim to have it released

- Act quickly — you usually have 10-30 days to claim exemptions

- Seek legal help — legal aid or consumer attorney can assist

Caption: Social Security, veterans’ benefits, and pensions are protected. Creditors cannot take them — even with a court judgment.

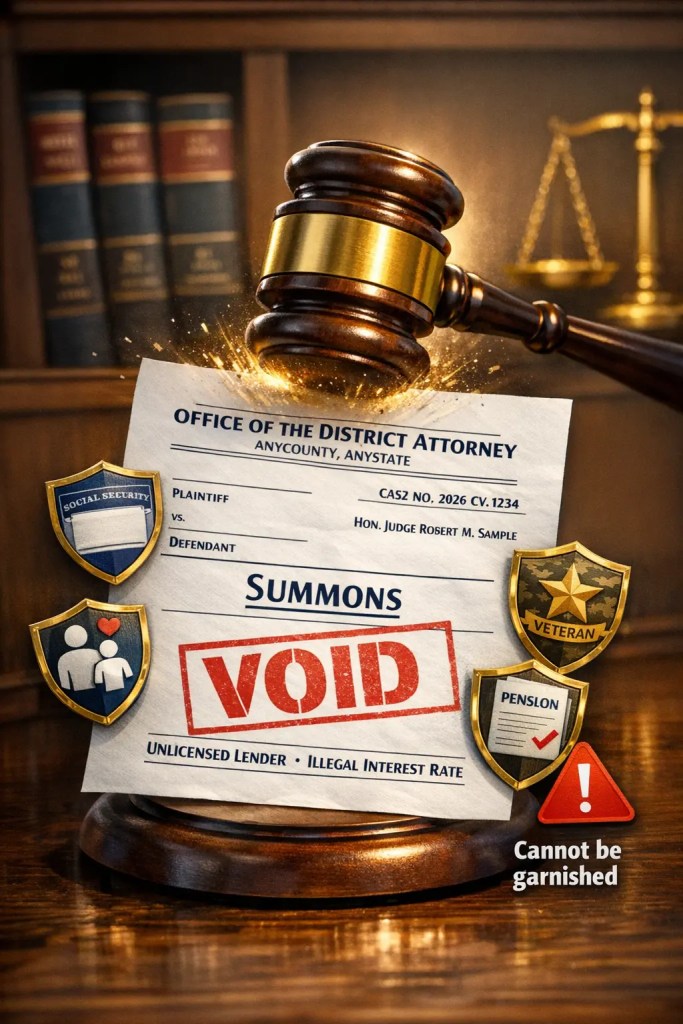

When Can’t a Payday Lender Sue You? (Void Loans)

Quick answer: If a lender isn’t licensed in your state, charges interest above state caps (like Maryland’s 33% limit), or operates through illegal “rent-a-tribe” schemes, the loan may be void and unenforceable. Recent lawsuits against Dave Inc. and MoneyLion show regulators taking action against unlicensed lenders. In these cases, they cannot sue you — and may even owe you money back.

🎯 Here’s What Most Borrowers Don’t Know

Most people assume that if they borrowed money, they have to pay it back — no matter what. But here’s the truth that lenders don’t want you to know: if the lender broke the law when making your loan, the loan itself may be VOID. That means they cannot sue you to collect, and in some cases, they owe you money back.

🚫 3 Reasons a Payday Lender CAN’T Sue You

1️⃣ Unlicensed Lenders

Every state requires payday lenders to be licensed. If a lender operates without a license in your state, they are breaking the law — and courts have ruled that unlicensed lenders cannot sue to collect.

⚡ Recent Enforcement:

Dave Inc. — Allegedly operated without license in multiple states, charging “tips” that pushed APRs over 2,500%

MoneyLion — Facing class action for unlicensed lending and fees exceeding state caps

2️⃣ Interest Rate Caps

Many states cap interest rates. In Maryland, consumer loans under $25,000 are capped at 33% APR. If a lender charges more, the loan may be void.

📊 State Rate Caps:

- Maryland: 33% APR

- New York: 25% APR (civil) / 16% criminal

- California: 36% for loans under $2,500

- Colorado: 36% APR cap

3️⃣ “Rent-a-Tribe” Schemes (Fake Tribal Immunity)

Some online lenders claim to be owned by Native American tribes to avoid state laws. Courts have repeatedly struck down these schemes when the lender, not the tribe, is the real party. If a lender uses this tactic, the loan may be void and they cannot sue you.

RICO lawsuits have been filed against lenders using tribal immunity to charge 700%+ APR .

–>

–>

🖼️ [Image placeholder: Gavel striking down void loan — add later]

⚖️ What This Means for YOU

If your lender is unlicensed or charged illegal rates:

- They may NOT be able to sue you

- If they already sued and won, you may be able to vacate the judgment

- You may be entitled to a refund of fees and interest

- You could have claims under state consumer protection laws

✅ How to Check If Your Lender Is Licensed:

- Visit NMLS Consumer Access — nmlsconsumeraccess.org

- Search the lender’s legal name (not the brand name)

- Check: Status “Active”? Your state listed?

- Check your state banking department website for licensed lenders

- Calculate APR — does it exceed your state’s cap?

See Episode 13 for our complete guide to verifying lender licenses.

Caption: If your lender is unlicensed or charged illegal rates, the loan may be void — they cannot sue you or garnish your wages.

Word-for-Word Scripts: What to Say When They Threaten You

Quick answer: Having the right words ready can stop harassment and protect your rights. Use these scripts to demand they stop calling, request proof they can sue, and respond to criminal threats. Always document every call — date, time, and exactly what was said. If they violate the law, you have grounds for a complaint.

Knowing your rights is one thing. Knowing exactly what to say when a collector calls is another. These scripts give you the words — just fill in the blanks and speak calmly.

📞 Script 1: “Stop Calling Me” (Cease Communication)

“This is [YOUR NAME]. I am recording this call for my records. I am demanding that you cease all communication with me regarding this debt. You may contact me in writing only. If you continue to call me after this request, you will be violating the Fair Debt Collection Practices Act, and I will file a complaint with the CFPB and FTC.”

When to use: When calls are constant, harassing, or outside 8am-9pm.

⚖️ Script 2: “Is This a Real Lawsuit?”

“I need you to provide me with the case number, the court where this lawsuit was filed, and the name of the judge assigned to the case. If you cannot provide that information immediately, I will assume this is an empty threat. Under the FDCPA, threatening legal action you don’t intend to take is illegal.”

When to use: When they threaten to sue but haven’t served you with papers.

🚨 Script 3: “You Can’t Threaten Me With Jail”

“I want to make clear that I am recording this conversation. Threatening me with criminal prosecution or arrest for a civil debt is illegal under the FDCPA. I am giving you one chance to retract that threat. If you continue, I will file a complaint with the FTC and consult an attorney about your violation.”

When to use: If they mention arrest, district attorney, or criminal charges.

📄 Script 4: “Prove I Owe This Debt” (Validation Request)

“I am requesting written validation of this debt within 30 days as allowed under the FDCPA. Please provide the original contract with my signature, a complete payment history, and proof that you are licensed to collect in my state. Until you provide this, you must stop all collection activities.”

When to use: First call from a collector — forces them to prove the debt is real.

–>

–>

🖼️ [Image placeholder: Phone call script visual — add later]

📋 Before You Call:

- Record the call — check your state’s recording laws (one-party consent states are safest)

- Write down the date and time — and the collector’s name

- Stay calm — read the script, don’t argue or explain

- Don’t provide personal information — they already have it

- Hang up if they become abusive — document and report

Script: Demand proof of real lawsuit

🎯 Quick Summary: Your Rights at a Glance

Ask for case number → If they can’t provide it → Loan may be VOID → Cannot garnish

📌 YOUR RIGHTS AT A GLANCE

Frequently Asked Questions

Can a payday lender really sue me?

Yes, a payday lender can sue you for non-payment, but only after following specific legal procedures. They must first file a lawsuit in court and properly serve you with a summons and complaint. If they win, they obtain a judgment. However, many threats to sue are empty — designed to scare you into paying without actual court action.

How many times can a debt collector call me per day?

Under the FDCPA, collectors are limited to 7 calls within 7 days about a specific debt. Calls are generally allowed only between 8 a.m. and 9 p.m. your local time. Calls at work are prohibited if your employer disapproves. If a collector exceeds these limits, they may be violating federal law.

Can I go to jail for not paying a payday loan?

No. You cannot be arrested or jailed for failing to repay a consumer debt. Threatening criminal prosecution for non-payment is illegal under the FDCPA. Some lenders have been sued for falsely threatening borrowers with arrest or district attorney involvement. If you receive such threats, document them and report to the CFPB and FTC immediately.

What’s the difference between a judgment and a lawsuit?

A lawsuit is the legal action they file against you. A judgment is what they get if they win. You’ll know a lawsuit is real when you’re served with court papers. A judgment only happens if you lose (or ignore) the lawsuit. With a judgment, they can garnish wages, levy bank accounts, or place liens on property.

Can they garnish my Social Security or veterans benefits?

No. Federal law protects Social Security, veterans benefits, child support, and certain other benefits from garnishment. However, if these funds are mixed with other money in your bank account, the entire account can be frozen until you file an exemption claim. You must notify the court and your bank that your funds are protected.

What if my lender isn’t licensed in my state?

If a lender operates without a license in your state, the loan may be void and unenforceable. Recent lawsuits against Dave Inc. and MoneyLion highlight regulators taking action against unlicensed lenders. You can check a lender’s license status at nmlsconsumeraccess.org or through your state banking department website.

What should I do if I’m served with court papers?

Do NOT ignore them. Note the response deadline (usually 20-30 days). File a written response with the court — even a simple “I dispute this debt” letter. Show up to any hearings. Seek help from legal aid or a consumer attorney. Ignoring court papers guarantees a default judgment against you, which leads to garnishment and levies.

⚠ For educational purposes only. Not legal advice. Laws regarding debt collection, lawsuits, and garnishment vary by state and change frequently. If you’re facing legal action, consult a qualified consumer rights attorney in your state.

Debt Collection Defense Checklist

Know your rights and fight back — printable 5-step guide:

📋 Your PDF includes:

- Call Log Sheet — track every violation (date, time, what they said)

- Real Lawsuit Verifier — know when it’s actually real

- Criminal Threat Check — illegal tactics to document

- Exempt Funds Tracker — protect Social Security, VA benefits

- Void Loan Checklist — when they can’t sue you

- Action Steps — exactly what to do next

Free · No sign-up required · ConfidenceBuildings.com · Pairs with Episode 15

PDF includes checkboxes, call log, and fillable forms

“If you’re being sued and can’t afford an attorney, Standard Legal offers affordable legal forms and document preparation services for bankruptcy and debt-related legal matters.”

Need Legal Documents Without the High Attorney Fees?

Standard Legal helps you create legally valid documents for bankruptcy, wills, incorporation, lease agreements, and more — at a fraction of the cost of hiring an attorney. Two affordable options:

📄 Document Preparation Service

Let Standard Legal prepare your documents for you

- Professionally prepared legal documents

- Review by legal professionals

- Perfect for bankruptcy, wills, incorporation

💻 Legal Forms Software

Create your own documents with easy-to-use software

- Complete legal forms library

- Step-by-step interview format

- Unlimited use for one low price

🔬 Research Note & Primary Sources

This article is part of the Borrower’s Truth Series, a 30-day educational series by Laxmi Hegde, MBA in Finance. All statistics, legal references, and case citations are drawn from government agencies, court records, and primary research institutions as of March 2026.

Primary Sources:

- Consumer Financial Protection Bureau (CFPB) — Debt collection practices, complaint database, and enforcement actions

- Federal Trade Commission (FTC) — Fair Debt Collection Practices Act (FDCPA) guidelines and enforcement

- National Consumer Law Center (NCLC) — Debt collection abuse reports and borrower rights research

- U.S. Courts — Federal Rules of Civil Procedure, default judgment statistics

- Social Security Administration — 42 U.S.C. § 407 (exempt funds protection)

- Vine v. PLS Financial Services — Class action regarding criminal threats in debt collection

- Dave Inc. & MoneyLion lawsuits — Baltimore City Circuit Court cases on unlicensed lending

- National Conference of State Legislatures (NCSL) — State payday lending laws and rate caps

- NMLS Consumer Access — Lender licensing database

⚖️ Fair Debt Collection Practices Act (FDCPA) — Key Provisions:

- 15 U.S.C. § 1692c — Communication limits (time/place, third-party contact)

- 15 U.S.C. § 1692d — Prohibition on harassment and abuse

- 15 U.S.C. § 1692e — False or misleading representations (including threats)

- 15 U.S.C. § 1692f — Unfair practices

- 15 U.S.C. § 1692g — Validation of debts (must provide proof)

🛡️ Exempt Funds — Federal Protections:

- 42 U.S.C. § 407 — Social Security benefits cannot be garnished

- 38 U.S.C. § 5301 — Veterans benefits protected

- 42 U.S.C. § 659 — Child support exceptions limited

- 15 U.S.C. § 1673 — Wage garnishment limited to 25% of disposable income

For the complete Borrower’s Truth Series guide, visit: The Complete Borrower’s Truth Guide → ConfidenceBuildings.com

← Previous · Episode 14

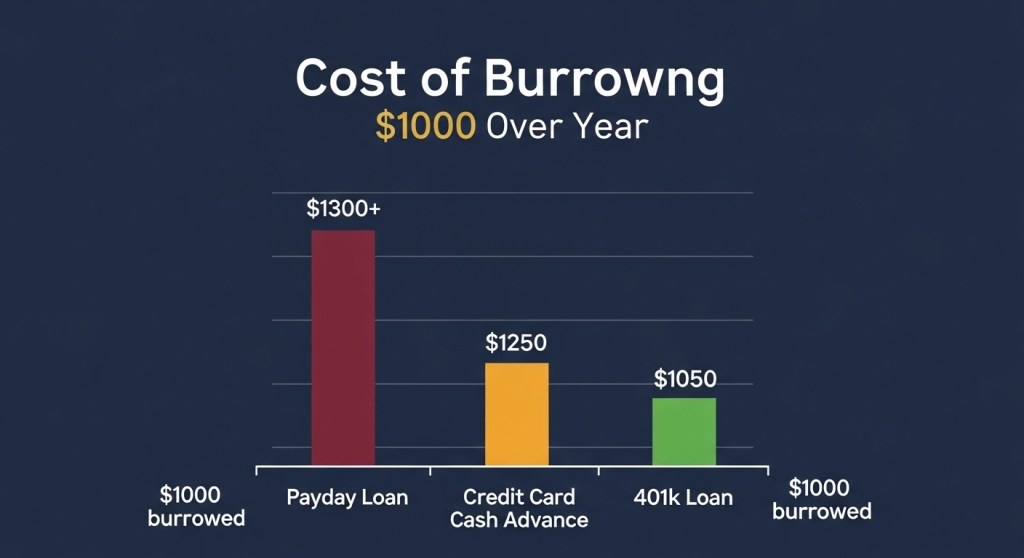

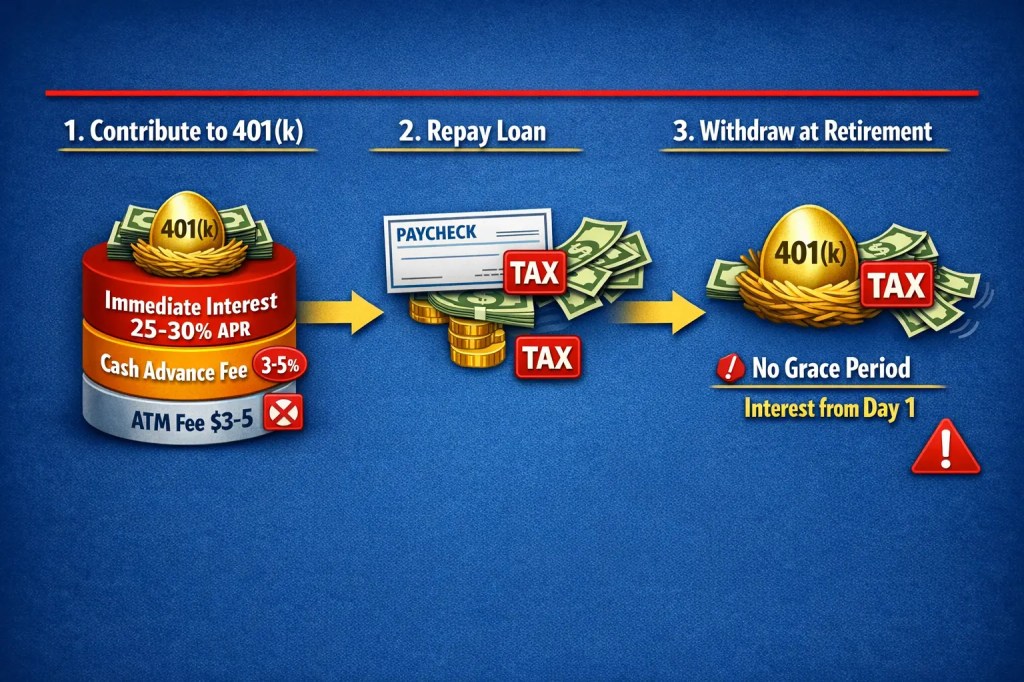

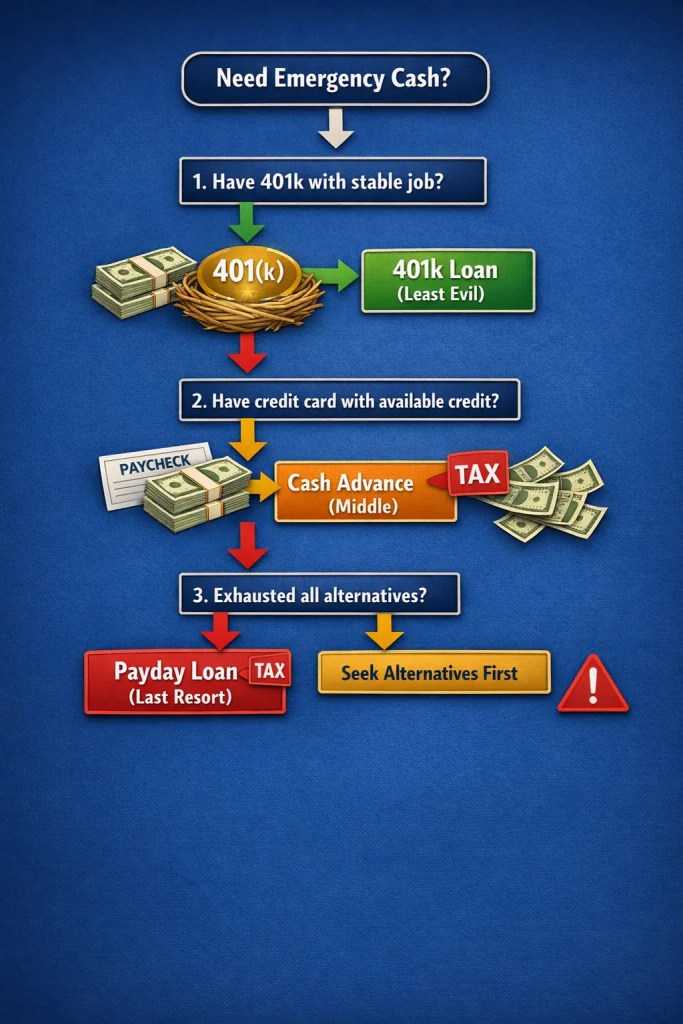

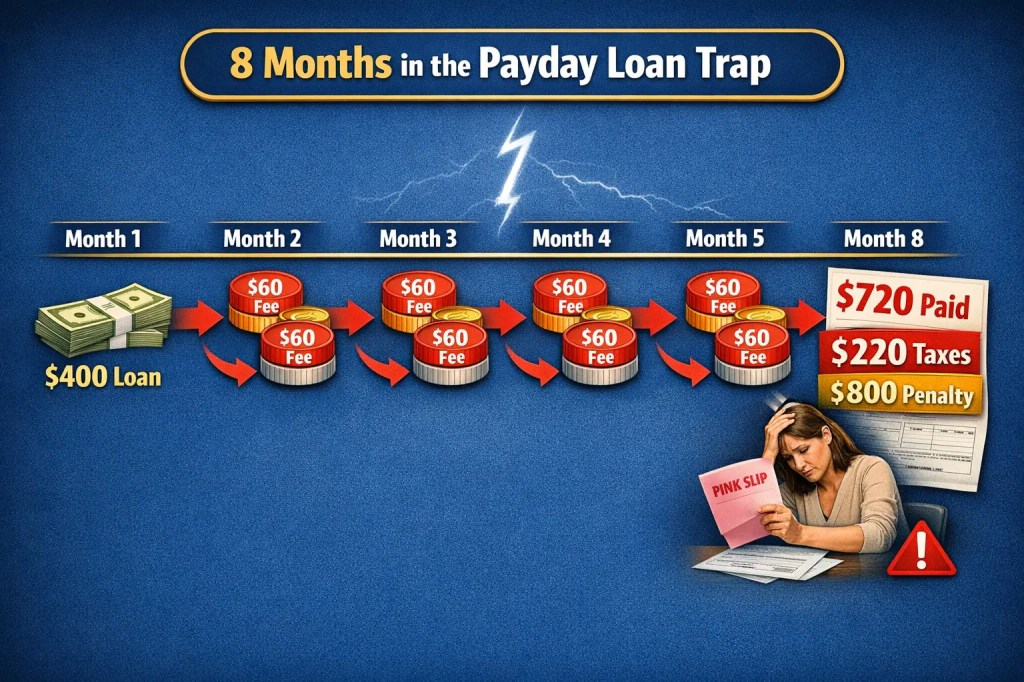

Payday Loans vs. Credit Card Cash Advances vs. 401(k) Loans: Which is the “Least Evil”?

Published March 14, 2026

Next · Episode 16 →

Loan Contract Fine Print: 7 Clauses Lenders Hope You Never Find

Coming March 17, 2026

📚 Emergency Borrowing Blueprint 2026 — 15 of 30 Episodes Complete

All episodes available at Emergency Borrowing Blueprint 2026

🔔 Bookmark the series or check back daily — new episodes every morning

📅 Published March 16, 2026 · Updated as part of the ConfidenceBuildings.com 2026 Consumer Finance Research Project.

This post is Episode 15 of 30 in the Borrower’s Truth Series, examining emergency borrowing, predatory lending practices, and consumer financial rights. All data, legal references, and case citations have been verified as of March 2026.

Research methodology: Information compiled from primary sources including the Consumer Financial Protection Bureau (CFPB), Federal Trade Commission (FTC), U.S. Courts, National Consumer Law Center (NCLC), and federal statutes (FDCPA, 42 U.S.C. § 407). Case references include Vine v. PLS Financial Services and recent enforcement actions against Dave Inc. and MoneyLion.

⚖️ For educational purposes only. Not financial or legal advice. Laws vary by state and change frequently. Always consult a qualified attorney for advice specific to your situation.

© 2026 ConfidenceBuildings.com · Borrower’s Truth Series · Laxmi Hegde, MBA in Finance

Free Access: Finance Calculator

Get instant access to loan, investment, and retirement tools.

📧 Subscribe with Email →One-click signup. No spam. You’ll get the calculator link immediately.

Already subscribed? Open calculator →