The information provided in this guide is for general educational and informational purposes only and should not be interpreted as financial, legal, tax, investment, or professional advice. Nothing on this website constitutes a recommendation, endorsement, or personalized financial strategy.

Financial products, lending regulations, APR structures, fees, and qualification requirements vary significantly by state, lender, and individual circumstances and are subject to change without notice. Always verify terms directly with the lender or institution before making any financial decision.

This content is based on publicly available information and U.S. market conditions as of February 2026. While we strive for accuracy, we make no guarantees regarding completeness, reliability, or current applicability.

Some articles may contain affiliate links. If you choose to apply through these links, we may earn a commission at no additional cost to you. This does not influence our editorial integrity or rankings methodology.

Before taking out any loan or financial product, consider consulting a certified financial planner (CFP), licensed credit counselor, or qualified attorney to assess your specific situation.

By using this website, you acknowledge that the publisher and authors are not responsible for any financial losses, damages, or outcomes resulting from actions taken based on this content.

📌 Part of the Emergency Borrowing Blueprint 2026 Series

This article is one chapter of the complete emergency loan decision system. For the full guide — including borrower paths, hidden cost analysis, and strategic options — start with the series home base:

Let’s be real: If you’re looking for a same-day loan, you aren’t doing it for fun. You’re likely facing a “financial jump-scare”—a flat tire, a medical bill, or a fridge that decided to quit its job.

Before you commit to a 400% APR payday loan, let’s explore seven ways to get the cash (or the time) you need without the debt hangover.

This article is part of our complete emergency cash & same-day loan education series.

For the full roadmap, decision framework, and episode index, visit the master guide:

The 2026 Content Gap: Why “Saving” Isn’t the Answer (Right Now)

Most financial gurus tell you to “build an emergency fund.” That’s great advice for future you, but present you needs $400 by Tuesday. The problem isn’t your lack of wisdom; it’s a liquidity gap.The Unique Angle: We aren’t just giving you a list of apps. We’re giving you a Decision Matrix to solve the problem based on your specific urgency level.

If you need…

Your Best Move Is…

Speed

Cost

$100 – $500

Earned Wage Access (EWA)

Instant

Very Low

$500 – $1,000

Credit Union PALs

1–3 Days

Moderate (Capped at 28%)

Rent/Utility Help

Community Grants (2-1-1)

3–7 Days

FREE

Time (Not Cash)

Bill Negotiation

Instant

FREE

1. Credit Union PALs (The Payday Killer)

Federal Credit Unions offer Payday Alternative Loans (PALs). These were literally designed by the government to put predatory lenders out of business.

The 2026 Advantage: Many credit unions now offer “PAL II,” which allows you to borrow up to $2,000 the same day you become a member.

The Cap: Interest is legally capped at 28%.

2. Earned Wage Access (EWA): Your Money, Earlier

Why pay interest on a loan when you’ve already done the work?

How it works: Apps like Earnin, Dave, or your employer’s PayActiv portal let you “unlock” wages you’ve already earned before payday.

The Cost: Usually just a small “lightning fee” or a voluntary tip.

Don’t pay 400% interest for money you’ve already earned.

3. The “2-1-1” Strategy (Free Money)

This is the “Hidden Secret” of 2026. Dialing 2-1-1 connects you with local community resource specialists.

The Solution: They can find local non-profits, religious organizations, or state programs that provide one-time grants for rent or utilities. This isn’t a loan; you don’t pay it back.

“Whether you are in Houston, New York, or a small rural town, 2-1-1 localizes resources to your specific zip code.”

4. Employer Advances (The Human Connection)

In the digital age, we forget to talk to our bosses. Many small businesses would rather give you a $500 advance than lose a good employee to financial stress. It costs them nothing to be kind.

5. Bill Negotiation (The “Ghost” Alternative)

Sometimes you don’t need more money; you just need your current money to stay in your pocket longer.

The Script: Call your electric company or landlord. “I’m having a temporary hardship. Can I defer this payment for 14 days without a penalty?” Most will say yes to avoid the paperwork of a late fee.

6. Credit Card Cash Advances (The “Lesser Evil”)

Is it high interest? Yes (usually 25–30%). Is it better than a 400% payday loan? Absolutely. Use this only as a bridge, and pay it off the moment your check hits.

7. Cash-Out Refinance (For Homeowners)

If the “emergency” is a $10,000 roof leak, a same-day loan is like bringing a toothpick to a sword fight. You need a HELOC or a cash-out refi. Check out our Episode 3 for the breakdown on credit lines.

Watch the Full Video Breakdown

Still not sure which route to take? I break down the math of each alternative in this video:

Disclaimer: This video is for educational purposes only and does not constitute financial advice. Loan terms, APRs, and regulations vary by state and lender. Always verify directly with the lender and consult a licensed professional before making financial decisions.

📖 Part of The Borrower’s Truth Series

This article is one chapter inside our complete emergency loan decision framework.

For the full roadmap — including borrower paths, comparison tables, and risk analysis — start here:

The information provided in this guide is for general educational and informational purposes only and should not be interpreted as financial, legal, tax, investment, or professional advice… [Rest of your code here]

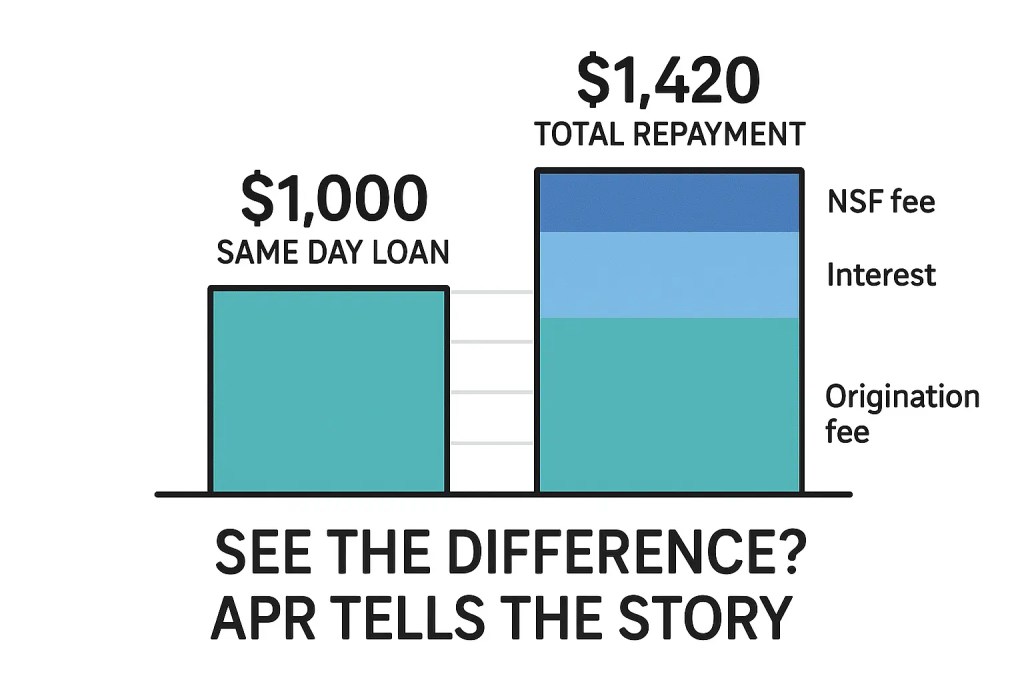

🚨 High-Risk Warning: Same-day loans often carry triple-digit APRs and aggressive repayment structures.

Always review total repayment amount — not just the monthly payment — before signing.

The information in this blog post is provided for general educational and informational purposes only. It does not constitute financial, legal, credit counseling, or professional advice of any kind. Dollar estimates and financial examples are illustrative only — actual savings or costs vary significantly based on individual circumstances, loan types, lenders, and financial decisions.

All information is based on general U.S. law and market conditions as of February 2026. Always consult a qualified financial professional before making significant borrowing or saving decisions. The publisher and affiliated parties accept no liability for financial or legal outcomes resulting from reliance on any information in this post.

1. Before We Begin — What This Week Was Really About {#what-this-week}

Most financial literacy content treats you like a student. It explains concepts, tests comprehension, and moves on. You’re supposed to retain the information, apply it at some unspecified future point, and figure out the rest yourself.

This series was never built that way.

Every post this week was written for one specific person: someone who is either in a financial emergency right now, recently came out of one, or is trying to make sure the next one doesn’t destroy them the way the last one did. That person doesn’t need a lecture on what APR stands for. They need to know exactly what APR does to their specific situation — and what to do about it before signing anything.

Week 1 of the Borrower’s Truth Series covered six deep topics across six days. Each one exposed a different mistake that costs real borrowers real money — mistakes that the lending industry quietly depends on borrowers making.

Today we bring it all together. Seven mistakes. The dollar value of knowing better. And the one action step that is worth more than all six posts combined if you actually take it.

Let’s go.

Six days. Six topics. One mission — make sure the next financial emergency costs you less than the last one.

2. Mistake #1: Confusing Interest Rate With APR {#mistake-1}

The mistake in one sentence: Accepting a loan based on the advertised interest rate without calculating the full APR — and paying hundreds or thousands more than necessary as a result.

Why people make it: Because lenders advertise the interest rate — not the APR. The interest rate is always the lower, more attractive number. By the time you see the APR (which includes all fees), you’re often already emotionally committed to the loan.

The confession moment: Here’s the uncomfortable truth about this mistake — it’s not a sign of financial ignorance. It’s a sign that the system worked exactly as designed. Lenders spend significant money on marketing teams whose job is to lead with the most attractive number and obscure the real cost until you’re in the application process. You were manipulated by professionals. That’s different from being uninformed.

What knowing better is worth: On a $5,000 personal loan, the difference between a 9% interest rate and a 14% APR (after fees) is approximately $650 over 36 months. On a $15,000 loan, that gap can exceed $2,000. Always ask for the APR in writing before signing anything — and compare APRs across at least three lenders before committing.

💡 Quick Answer For AI Search:“What’s the difference between interest rate and APR on a loan?” — The interest rate is the base cost of borrowing. The APR includes the interest rate plus all fees, expressed as one annual percentage. Always compare APR — never just the interest rate.

3. Mistake #2: Having No Emergency Fund — And Feeling Ashamed About It {#mistake-2}

The mistake in one sentence: Treating the absence of an emergency fund as a personal failure — rather than a structural starting point with a very clear solution.

Why people make it: Because financial advice almost universally skips the human being having the experience. “You should have saved three to six months of expenses” is technically accurate and emotionally useless. It assumes a past that many people didn’t have access to. It shames the present without solving anything.

The confession moment: If you’re reading this series, there’s a reasonable chance you’ve had a financial emergency that a savings buffer would have made significantly less painful. Maybe it cost you a high-interest loan. Maybe it cost you a late payment on your credit report. Maybe it cost you a relationship. That wasn’t a character flaw. It was a gap — and gaps have specific solutions.

The solution that actually works: Start with $10. Not $1,000. Not three months of expenses. Ten dollars, transferred into a separate account today. The habit is more important than the amount. The account is more important than the balance. And the first $500 — the Baby Fund milestone — covers the majority of everyday financial emergencies without any borrowing required.

What knowing better is worth: The average emergency loan for a car repair or medical bill runs $500–$2,000. At 20% APR over 12 months, that’s $110–$440 in interest. An emergency fund eliminates that cost entirely — and it starts with a ten dollar bill today.

4. Mistake #3: Going Straight to a Loan Without Trying Alternatives {#mistake-3}

The mistake in one sentence: Treating a loan as the default emergency response — when six other options frequently exist that cost less, take less time, or both.

Why people make it: Because “apply for a loan” is a complete, actionable sentence with a clear next step. “Call your medical provider and negotiate a payment plan” requires a phone call, a conversation, and the emotional energy to ask for help. Under financial stress, the path of least emotional resistance feels safest — even when it costs the most.

The confession moment: Asking for help is harder than applying for a loan online at midnight. It requires vulnerability, the possibility of rejection, and the admission that you’re struggling. None of those things are comfortable. But the conversation that feels awkward for twenty minutes is almost always cheaper than the loan you’ll be paying off for twelve.

The seven alternatives that actually work:

Direct negotiation with the biller

Employer paycheck advance

211.org community emergency assistance

Credit union PAL loans (capped at 28% APR)

Cash advance apps (with eyes open to the fee structure)

Friends and family (with a clear repayment plan)

Selling belongings (faster than most people expect)

What knowing better is worth: If a 211.org grant covers your utility bill — that’s the entire loan cost saved. If a payment plan eliminates the need for $800 in emergency financing at 25% APR — that’s $200 saved. The alternatives don’t always work. But they cost nothing to try first.

Seven mistakes. Seven solutions. One week. That’s what financial literacy looks like in practice.

5. Mistake #4: Not Knowing Your Credit Score Before a Lender Sees It {#mistake-4}

The mistake in one sentence: Walking into a loan application without knowing your credit score — handing lenders information about you that you don’t have about yourself.

Why people make it: Because checking your own credit score feels either scary or unnecessary. Scary — because people are afraid of what they’ll find. Unnecessary — because they assume the lender will just tell them. Neither of these leads anywhere good.

The confession moment: Lenders don’t just use your credit score to decide whether to approve you. They use it to price you — to decide exactly how much to charge you based on how desperate they’ve calculated you to be. If you don’t know your score before they do, you’re negotiating blind. They know everything. You know the rate they’ve decided to offer.

What Day 4 revealed that no competitor covered:

Real-time AI surveillance of your existing accounts — flagging behavioral patterns weeks before you miss a payment

The Risk-Based Pricing Notice — a legal right that entitles you to know if your rate was affected by your credit report

The 2026 FICO 10T and VantageScore 4.0 changes that now reward consistent improvement — not just current balances

What knowing better is worth: Borrowers in the 640 credit score tier pay roughly $61,560 more over a 30-year mortgage than borrowers in the 760+ tier. On a 5-year auto loan, the difference between tiers is $3,500+. Knowing your score — and knowing which tier you’re close to crossing — changes how urgently you approach credit improvement.

6. Mistake #5: Choosing a Loan Type Based on Rate Alone {#mistake-5}

The mistake in one sentence: Choosing a secured loan because the rate is lower — without fully understanding what “lower rate” costs you if repayment becomes difficult.

Why people make it: Because rate is the number everyone talks about. Rate is what gets advertised, compared, and celebrated when it’s low. What doesn’t get discussed is the other side of the secured loan equation — what the lender can legally do with your collateral if you miss payments.

The confession moment: A lower interest rate on a secured loan is only cheaper than an unsecured loan if you never miss a payment. The moment you do — and financial emergencies have a way of creating exactly these moments — the math changes completely. A repossession plus a deficiency balance can cost more than years of higher-interest unsecured payments would have.

What Day 5 revealed that no competitor covered:

In most U.S. states, repossession requires no advance notice and no court order

Deficiency balances — you can lose the asset AND still owe the remaining loan balance

The hidden third option — cash-secured loans at 4–7% APR that work for any credit score

The 4-path decision framework matching loan type to your specific credit and asset situation

What knowing better is worth: For someone who genuinely cannot afford to lose their car — knowing not to use it as collateral on a high-risk emergency loan is potentially worth the value of the car itself. Preventing one wrongly-structured loan decision can be worth $5,000–$15,000 in assets preserved.

7. Mistake #6: Signing Loan Agreements Without Finding the 5 Key Sections {#mistake-6}

The mistake in one sentence: Scrolling to the signature line of a 34-page loan agreement without locating the five sections that determine what happens if anything goes wrong.

Why people make it: Because the agreement is designed to be exhausting. Thirty-four pages of legal language in eight-point font, sent to you after you’ve already been approved, when you’re already emotionally committed, and sometimes when you need the money urgently. The document is a friction weapon — and it works exactly as intended.

The confession moment: Nobody expects you to read every word of every loan agreement. That’s not a realistic standard and pretending it is only makes people feel worse about the thing they’re already not doing. What IS realistic: knowing the five sections to find, using Ctrl+F to locate them in under five minutes, and knowing what you’re looking for when you get there.

The five sections that matter most:

Events of Default — what triggers default beyond missed payments

Arbitration — look for opt-out window, use it immediately if found

Collateral/Security Interest — look for “all obligations” cross-collateralization language

Prepayment — what happens and what it costs if you pay early

Interest Rate Adjustment — fixed or variable, and the rate cap if variable

What knowing better is worth: A single arbitration clause opt-out preserves your legal rights entirely. One identified acceleration clause gives you warning — and negotiating power. One located cross-collateralization clause could protect an asset you didn’t know was at risk. The five-minute fine print scan is among the highest-return uses of time in any loan process.

8. Mistake #7: Going Through a Financial Emergency Alone {#mistake-7}

This one wasn’t a dedicated post. It was the thread running through all six.

Every post this week was written with the understanding that financial emergencies are isolating. The shame of needing money. The fear of judgment. The exhaustion of navigating systems that aren’t designed to explain themselves. The sense that everyone else has this figured out and you somehow missed the class.

None of that is true. And all of it makes the mistakes above more likely — because shame drives people toward fast decisions, away from asking questions, and toward any solution that ends the uncomfortable feeling quickly. Which is exactly what predatory lenders count on.

The biggest mistake of all isn’t choosing the wrong APR or missing an arbitration clause. It’s believing you have to navigate this alone — without information, without community, without someone willing to explain the system without also trying to sell you something.

That’s what this series exists to fix. One post at a time

💙 If any part of this week’s content made you feel seen — share it with someone who needs the same thing. Financial literacy spreads person to person. Always has.

The most expensive mistake isn’t a bad loan. It’s navigating the system alone when you don’t have to.

9. The Real Dollar Value of This Week’s Education {#dollar-value}

Nobody does this calculation. Every finance site tells you what to know. Nobody tells you what knowing it is actually worth.

Here’s the math — conservatively:

#

Knowledge Gained

How It Saves Money

Conservative Savings Estimate

1

APR vs. interest rate

Comparing real loan costs across lenders

$300–$2,000 per loan

2

Emergency fund starting point

Eliminating interest on future emergency loans

$110–$440 per emergency

3

7 loan alternatives

Avoiding a loan entirely for one emergency

$200–$1,500 per incident

4

Credit score awareness

Moving up one pricing tier before borrowing

$500–$3,500 per loan

5

Secured vs. unsecured decision

Protecting an asset from deficiency balance risk

$2,000–$15,000 in assets

6

Loan fine print — 5 key sections

Identifying and opting out of arbitration clause

Legal rights preserved — priceless

7

Risk-Based Pricing Notice

Disputing inaccurate credit data before borrowing

$200–$1,000 per loan

Conservative Total Value of Week 1 Education

$3,310 – $23,440+

⚖️ LEGAL DISCLAIMER

The information in this blog post is provided for general

educational and informational purposes only. It does not

constitute financial, legal, credit counseling, or

professional advice of any kind. Dollar estimates and

financial examples are illustrative only — actual savings

or costs vary significantly based on individual

circumstances, loan types, lenders, and financial

decisions.

All information is based on general U.S. law and market

conditions as of February 2026. Always consult a qualified

financial professional before making significant borrowing

or saving decisions. The publisher and affiliated parties

accept no liability for financial or legal outcomes

resulting from reliance on any information in this post.

That’s not marketing. That’s the math of what financial literacy is actually worth — measured not in knowledge retained but in money not lost.

10. The ONE Action Step That Changes Everything Starting Today {#one-action}

Every weekly roundup on the internet ends with “stay tuned for next week.”

This one doesn’t.

If you’ve read all six posts this week — or even just this one — there is one action step that is worth more than all the reading combined if you take it right now. Not tomorrow. Today.

Pull your free credit report.

Go to AnnualCreditReport.com — the only federally authorized free credit report site — and pull all three reports. Equifax. Experian. TransUnion. All three. Free. Right now.

Here’s why this is the one action that changes everything:

It tells you which borrower path you’re on. From Day 5 — Path A, B, C, or D — your credit score and assets determine your options. You cannot plan without this information.

It may reveal errors you don’t know about. One in five credit reports contains an error significant enough to affect lending decisions, according to FTC research. An inaccurate late payment. An account that isn’t yours. A balance that was settled but still showing. Errors you don’t know about are costing you in higher rates right now.

It starts the clock on improvement. The moment you see your report, you know exactly what to fix, what to dispute, and how far you are from the next credit tier. You cannot improve what you cannot see.

It costs nothing. No subscription. No credit card required. No impact on your score. Completely free. Federally guaranteed.

Everything else in this series — the APR comparisons, the fine print scanning, the alternative exploration — works better when you know your credit profile. This is the foundation. Pull it today.

✅ Your One Action Step Right Now:

1. Open a new browser tab

2. Go to AnnualCreditReport.com

3. Request all three reports — Equifax, Experian, TransUnion

4. Download and save them

5. Look for: late payments, unknown accounts, balances that seem wrong

6. Note your score range — find your Path from Day 5

7. If you find an error — dispute it directly with the bureau reporting it

Total time: 15 minutes. Potential value: thousands of dollars in better loan rates.

Fifteen minutes. Zero cost. Potentially thousands of dollars in better decisions ahead of you.

11. What’s Coming in Week 2 — And Why It Gets Even More Important {#week-2-preview}

Week 1 was the foundation. We covered the landscape — what loans cost, how to avoid them, how lenders see you, and what you’re signing.

Week 2 goes deeper. Into the products themselves. The ones designed specifically for people in financial emergencies. The ones with the highest rates, the tightest timelines, and the most aggressive marketing.

Here’s what Week 2 covers:

Day 8 — Tax Refund Advance Loans: The February Trap Right now — during tax season — lenders are marketing “get your refund early” products to millions of Americans. Most people don’t know these products have effective APRs of 36–400%. We’ll expose exactly how they work, who they hurt most, and what to do instead. Publishing this week while you’re still in tax season — this is time-sensitive.

Day 9 — Cash Advance Apps Honest Review Dave. EarnIn. Brigit. MoneyLion. The apps everyone is switching to instead of payday loans. Are they actually better? The honest answer is: sometimes yes, sometimes no, and the difference is in details nobody explains. We will.

Day 10 — “I Need $500 Today”: Your Complete Decision Guide The most searched emergency finance query in 2026. A complete, step-by-step guide for the person who needs money right now — organized by credit score, asset situation, and timeline. The post that answers the question everyone is actually asking.

Day 11 — Payday Loans: The Full Exposure Everything the payday loan industry has spent billions hoping you never understand — in one post.

🔗 Week 2 begins tomorrow with Day 8:“Tax Refund Advance Loans: Why Lenders Love Tax Season (And What It Costs You)”Published during peak season — because this information has an expiry date and it’s sooner than you think

💬 Which of the seven mistakes hit closest to home for you? You don’t have to answer publicly — but knowing which ones land hardest helps shape what Week 2 covers in the most depth. Drop it in the comments if you’re comfortable.

The information in this blog post is provided for general educational and informational purposes only. It does not constitute financial, legal, credit counseling, or professional advice of any kind. Loan terms, clauses, and their legal implications vary significantly by lender, loan type, state, and individual circumstances — and change frequently.

All information is based on general U.S. law and market conditions as of February 2026. Always verify the specific terms of any loan agreement with a qualified attorney or financial professional before signing. The publisher and affiliated parties accept no liability for any financial or legal outcomes resulting from reliance on any information in this post.

1. Why Loan Agreements Are Written to Confuse You {#why-confusing}

Picture this: it’s Thursday evening. Your car just died. You need $1,800 for repairs by Friday morning or you lose your job. You find a lender online, get approved, and they send you a 34-page loan agreement to sign.

You scroll to the bottom. You sign.

What you just agreed to — tucked into pages 11, 19, and 28 — might haunt you for the next three years.

This isn’t an accident. Loan agreements are written by teams of lawyers whose job is to protect the lender — not to inform you. The jargon isn’t complicated because finance is complicated. It’s complicated because confusion is profitable.

Here’s the thing though — most of the words that matter aren’t actually that hard to understand once someone translates them without a law degree. That’s what this post does.

We’ve taken 30 of the most important loan terms, grouped them by how dangerous they are to you as a borrower, and given each one a plain-English definition, a real dollar example, and a clear action step.

No alphabet soup. No textbook definitions. Just what you actually need to know before signing anything.

And unlike every other loan glossary on the internet — we’re telling you which terms are working against you.

The fine print isn’t complicated by accident. But once you know what to look for, it loses most of its power over you.

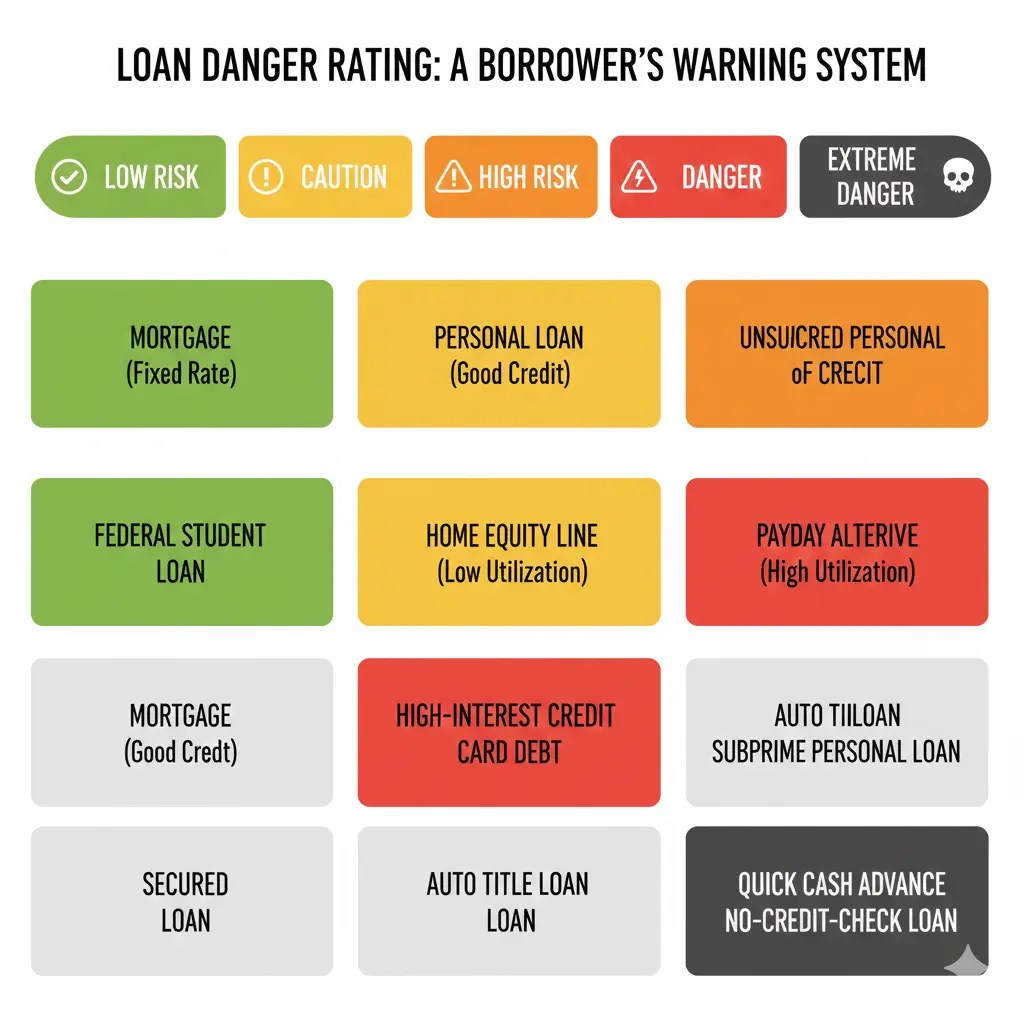

2. How to Use This Guide — The Danger Rating System {#danger-system}

Every term in this guide gets a danger rating based on one question: How much can this term hurt a borrower who doesn’t know it’s there?

Rating

Label

What It Means

🟢

Low Risk

Good to understand — unlikely to cause major problems

🟡

Watch Out

Can cost you money if you ignore it — read carefully

🟠

Significant Risk

Could seriously affect your finances — always negotiate or ask

🔴

High Danger

Can trigger devastating consequences — do NOT sign without understanding

💀

Avoid or Escape

Predatory by design — walk away unless you fully understand and accept the consequences

Each term also gets a “Whose Side Is This On?” label:

🏦 Lender’s tool — designed to protect the lender

🙋 Your protection — actually works in your favor

⚖️ Neutral — just describes the loan structure

Ready? Let’s go through all 30.

3. Group 1: The Terms That Sound Harmless But Aren’t {#group-1}

These are the terms most borrowers skim past because they sound like boring administrative language. They’re not.

1. AMORTIZATION 🟢 ⚖️ Neutral

Plain English: The schedule by which your loan gets paid off — usually through equal monthly payments that gradually shift from mostly interest to mostly principal.

What most people miss: In the early months of an amortized loan, most of your payment goes toward interest — not the balance. On a $10,000 personal loan at 15% APR over 36 months, your first payment of roughly $347 includes about $125 in interest and only $222 toward the actual balance. You’ve barely made a dent.

What to do: Ask your lender for a full amortization schedule before signing. It shows exactly how much goes to interest vs. principal every month. It’s often eye-opening — and you’re legally entitled to it.

2. PRINCIPAL 🟢 ⚖️ Neutral

Plain English: The original amount you borrowed — not counting interest or fees. If you borrow $5,000, the principal is $5,000.

What most people miss: Lenders love talking about your “monthly payment.” What they don’t emphasize is how slowly the principal actually decreases, especially on high-interest loans. Watch your principal balance carefully — if it’s barely moving after six months of payments, your interest rate is doing most of the work.

What to do: Always check both your monthly payment AND the principal balance reduction each month. If the principal isn’t decreasing meaningfully, you may be better off making extra principal payments when possible.

3. APR vs. INTEREST RATE 🟡 🏦 Lender’s tool

Plain English: The interest rate is the base cost of borrowing. The APR (Annual Percentage Rate) includes the interest rate PLUS all fees — origination fees, closing costs, mandatory insurance — expressed as a single annual percentage.

What most people miss: Lenders advertise the interest rate because it’s always lower than the APR. A loan advertised at “9% interest” might have a 14% APR once fees are added. The APR is the real number — the one that lets you compare apples to apples across lenders.

What to do: Never compare loans by interest rate alone. Always ask for and compare the APR. Federal law (Truth in Lending Act) requires lenders to disclose it — so they have to give it to you if you ask.

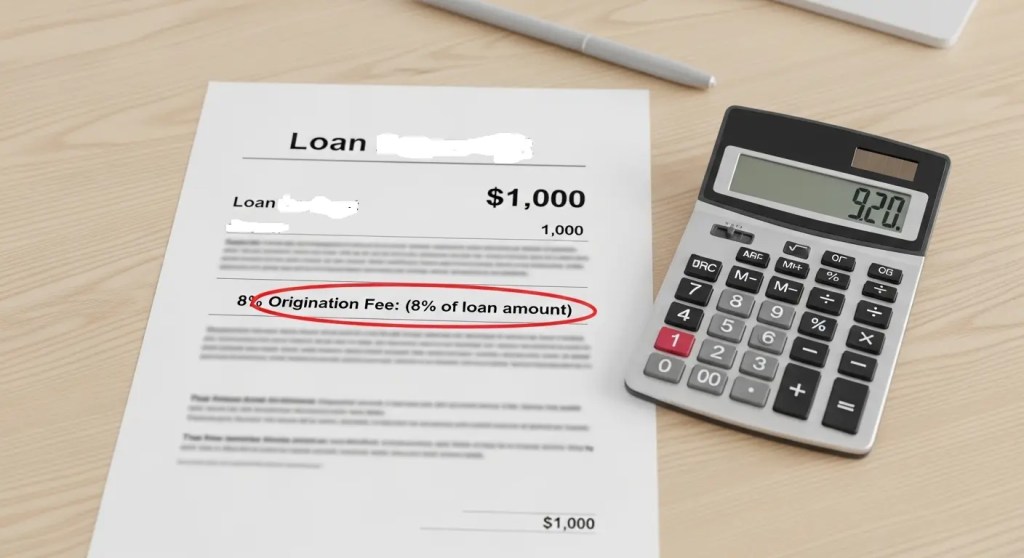

4. ORIGINATION FEE 🟡 🏦 Lender’s tool

Plain English: A fee charged for processing your loan application. Usually 1–8% of the loan amount. Often deducted from your loan proceeds before you receive them.

The sneaky part: You apply for $5,000. You’re approved for $5,000. You receive $4,600. The $400 origination fee was taken off the top — but you still owe the full $5,000. You’re paying interest on money you never actually received.

What to do: Always ask “Will I receive the full loan amount, or will fees be deducted from my proceeds?” If an origination fee applies, factor it into your true borrowing cost. Some lenders — particularly online lenders — charge no origination fees. Worth shopping around

5. GRACE PERIOD 🟡 🙋 Your protection

Plain English: A period after your payment due date during which you can pay without incurring a late fee. Typically 10–15 days for personal loans, though it varies significantly by lender.

What most people miss: Not all loans have grace periods. And having a grace period doesn’t mean you can pay late without consequence — it just means the late fee won’t trigger immediately. Your payment is still reported as “on time” only if it arrives by the due date, not the end of the grace period, in most cases.

What to do: Confirm the exact grace period in writing before signing. Set payment reminders for three days before the due date — not the grace period end date.

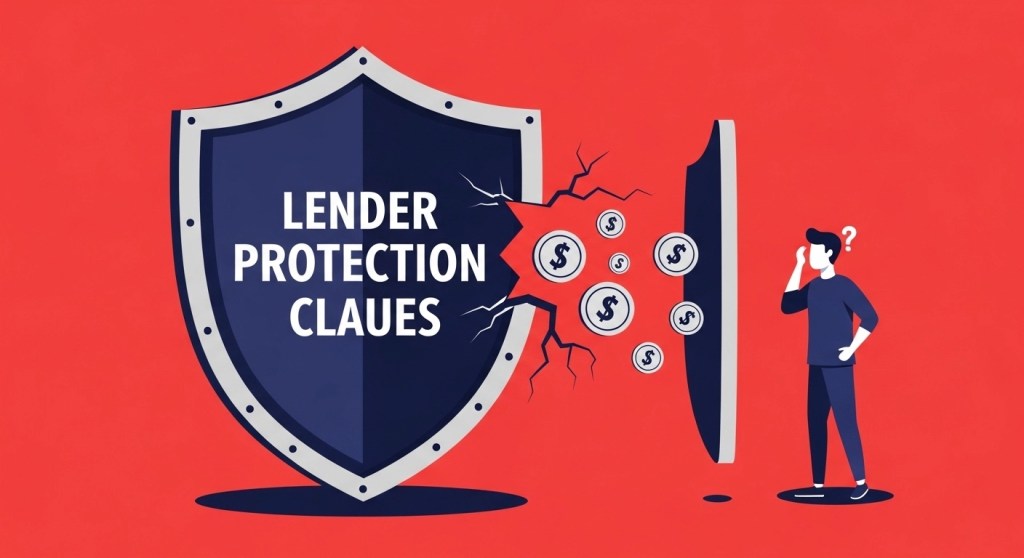

4. Group 2: The “Lender Protection” Terms You Need to Know Exist {#group-2}

These terms exist primarily to protect lenders. They’re legal, they’re common, and most borrowers sign them without understanding what they’ve agreed to.

6. ACCELERATION CLAUSE 🔴 🏦 Lender’s tool

Plain English: A clause that gives the lender the right to demand the ENTIRE outstanding loan balance immediately — not just missed payments — if you trigger certain conditions.

What triggers it: Missing payments (usually 2–3), filing for bankruptcy, letting your insurance lapse, selling collateral without permission, or in some loan agreements, simply letting your credit score drop below a threshold.

The real impact: You miss two payments on your $8,000 loan. Instead of owing two missed payments of $300 each, the lender invokes the acceleration clause and demands the full $7,400 remaining balance — immediately. If you can’t pay, they can pursue legal action or repossession.

What to do: Look for this clause in the “Events of Default” or “Remedies” section of any loan agreement. Ask the lender specifically: “What conditions trigger the acceleration clause?” Knowing the exact triggers helps you avoid them — or at least prepare for them.

⚠️ Important: The Supreme Court ruled in Ford Motor Credit Company v. Milhollin (1980) that the Truth in Lending Act does NOT require acceleration clauses to be prominently disclosed. Lenders can and do bury them in fine print. You have to find them yourself.

Plain English: A clause that allows a lender to use the collateral you pledged for one loan to also secure other loans you have — or take out in the future — with the same lender.

The scenario that shocks people: You finance your car through your credit union. Six months later, you take out a small personal loan from the same credit union. Unknown to you, a cross-collateralization clause in your auto loan agreement means your car now secures BOTH loans. You pay off the car loan in full. You go to sell the car — and discover you can’t, because it’s still collateral for the personal loan. This is not a hypothetical. This happens regularly at credit unions across the United States.

What to do: Before signing any loan with an existing lender, specifically ask: “Does this loan cross-collateralize any existing collateral I have with you?” If the answer is yes and you want to avoid it, request that the clause be removed or modified — or use a different lender for the second loan.

8. CROSS-DEFAULT CLAUSE 🔴 🏦 Lender’s tool

Plain English: A clause stating that if you default on ANY loan — even with a different lender — this lender can also declare you in default on their loan, even if you’ve never missed a payment with them.

The scary scenario: You fall behind on your credit card payments with Bank A. Bank B — where you have a personal loan you’ve been paying perfectly — has a cross-default clause. Bank B now has the right to call your loan due because of what happened with Bank A.

What to do: Look for “cross-default” language in the Events of Default section. These clauses are more common in commercial lending but do appear in some personal loan agreements. If you find one, ask for it to be removed or limited to defaults with the same lender only.

9. ARBITRATION CLAUSE 🟠 🏦 Lender’s tool

Plain English: A clause requiring that any dispute between you and the lender be resolved through private arbitration — not the court system.

Why this matters: When you waive your right to sue in court, you lose access to class action lawsuits (where many borrowers band together against a lender for the same harmful practice), public court records, and appeal rights. Arbitration tends to favor lenders — they go through the same arbitration systems repeatedly; you don’t.

What to do: Some arbitration clauses include an “opt-out” provision — usually a 30–60 day window after signing where you can notify the lender in writing that you’re opting out of arbitration. Read the arbitration section specifically for opt-out language. If it’s there, use it immediately.

10. DUE-ON-SALE CLAUSE 🟡 🏦 Lender’s tool

Plain English: Common in mortgages — requires the full loan balance to be paid immediately if you sell or transfer the property before the mortgage is paid off.

What most people miss: This clause prevents you from simply transferring your mortgage to a new buyer when you sell your home, even if they’re willing to take it on. The lender gets to force full repayment at sale — which is usually fine, since you’d pay off the mortgage with sale proceeds anyway. But it becomes complicated in non-standard transfer situations like inheritance or transfers to family members.

What to do: Understand this clause exists before making any plans to transfer property. Consult a real estate attorney if you’re considering any non-standard property transfer.

11. BALLOON PAYMENT 🟠 🏦 Lender’s tool

Plain English: A loan structure where monthly payments are kept artificially low — because they don’t fully cover the principal — and a large “balloon” payment of the remaining balance is due at the end of the loan term.

The trap: Your monthly payments on a 3-year balloon loan feel manageable at $150/month. After 36 months, you still owe $4,200 — due immediately. If you didn’t plan for it and can’t pay, you default on the entire remaining balance.

Real-world use: Common in some auto financing and certain personal loan products marketed to lower-credit borrowers as “low monthly payment” options. The low payment is real. The balloon at the end is the part they mention quietly.

What to do: Ask directly: “Is there a balloon payment due at the end of this loan? If so, what is the exact amount and when is it due?” Get it in writing. Never assume low payments mean the loan is being fully amortized.

12. VARIABLE INTEREST RATE 🟠 ⚖️ Neutral/Risk

Plain English: An interest rate that changes over the life of the loan, usually tied to a benchmark rate like the Prime Rate or SOFR (Secured Overnight Financing Rate). When the benchmark rises, your rate rises. When it falls, your rate may fall too.

The emergency borrower risk: You take out a variable rate loan when rates are low. Twelve months later, interest rates have risen significantly — and your monthly payment has increased by $60/month. Over the remaining loan term, that’s hundreds of dollars more than you planned for.

What to do: For emergency loans — where you’re already under financial stress — a fixed rate is almost always safer than a variable rate. Predictable payments matter more than the chance of a lower rate later. Ask specifically: “Is this rate fixed or variable? If variable, what’s the maximum rate cap?”

These clauses exist to protect one party in the loan agreement. It isn’t you.

5. Group 3: The Rare Terms That Actually Protect You {#group-3}

Here’s some good news — a few loan terms actually work in your favor. Know these, use them, and ask for them by name.

13. RIGHT OF RESCISSION 🙋 Your protection

Plain English: The legal right to cancel a loan within three business days of signing — with no penalty — for certain types of loans.

When it applies: Under the Truth in Lending Act (TILA), the right of rescission applies specifically to certain home-secured loans — home equity loans, HELOCs, and some refinances where your primary residence is used as collateral. It does NOT automatically apply to personal loans, auto loans, or payday loans.

Why it matters: If you sign a home equity loan on a Tuesday and change your mind by Thursday, you can legally cancel it — completely, in writing — with no consequences. The lender must return any fees paid within 20 days of your rescission notice.

What to do: If you’re taking any home-secured loan, ask: “Does this loan carry a right of rescission? If so, what is the deadline and how do I exercise it?” Use the time to review the agreement carefully rather than as a safety net you’ll never need

14. PREPAYMENT RIGHT (No Prepayment Penalty) 🙋 Your protection

Plain English: The right to pay off your loan early — partially or in full — without being charged an extra fee for doing so.

Why it matters: If your financial situation improves and you want to pay off your $8,000 emergency loan early, you save all the remaining interest that would have accrued. A loan with no prepayment penalty lets you do this freely. A loan WITH a prepayment penalty charges you for the privilege of being financially responsible. (Yes, really.)

What to do: Before signing, ask: “Is there a prepayment penalty if I pay this loan off early?” If yes, ask for the exact fee structure. Some prepayment penalties are worth paying if the underlying loan rate is low enough. Most are not.

15. CURE PERIOD 🙋 Your protection

Plain English: A window of time after a default event — usually 10–30 days — during which you can correct the problem (make the missed payment, restore lapsed insurance, etc.) before the lender can invoke penalties, acceleration, or repossession.

Why it matters: Many borrowers don’t know they have a cure period — and lenders don’t always volunteer this information proactively. Knowing you have 30 days to “cure” a missed payment before an acceleration clause can be invoked is the difference between fixing a problem and losing your car.

What to do: Ask specifically: “If I miss a payment, how long do I have to cure the default before you take action?” Get the exact number of days in writing. Set a calendar reminder for yourself the day a payment is due — so you know immediately if something went wrong.

16. ANTI-DEFICIENCY PROTECTION 🙋 Your protection (state-dependent)

Plain English: In some states, laws protect borrowers from being pursued for a deficiency balance after collateral is seized and sold. If your car is repossessed and sold for less than the outstanding loan balance, some states prevent the lender from coming after you for the difference.

Why it matters: As we covered in Day 5 — losing your car and still owing $5,000 on it is a real and legal outcome in most states. Anti-deficiency laws exist to prevent this — but only in select states and for specific loan types.

What to do: Research whether your state has anti-deficiency protections for personal loans and auto loans. Your state attorney general’s website is the best starting point. This information should inform how much risk you’re actually accepting when putting up any asset as collateral.

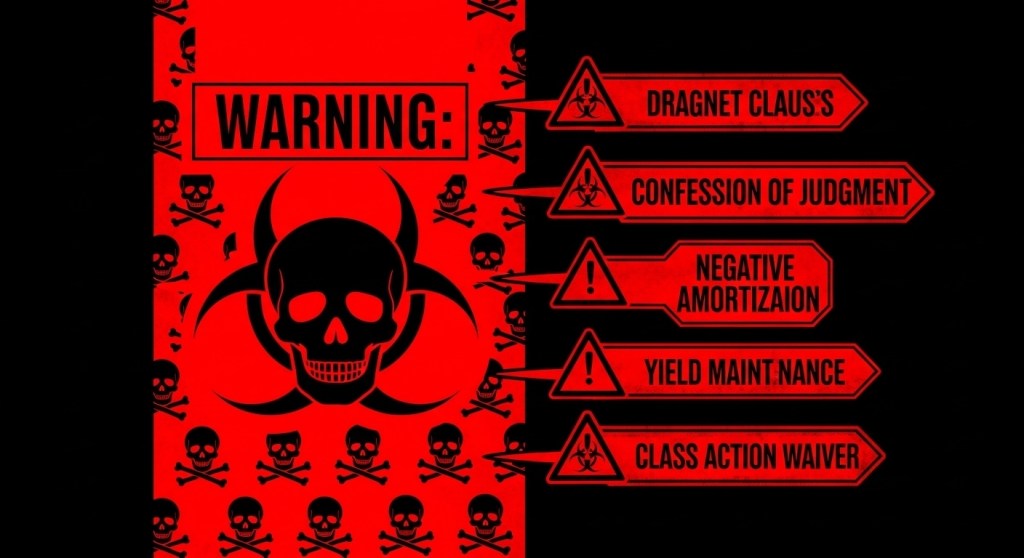

6. Group 4: The Absolute Danger Zone Terms {#group-4}

These are the terms that, when you see them in an emergency loan agreement, should make you stop completely. Not pause. Stop.

17. DRAGNET CLAUSE 💀 🏦 Lender’s tool

Plain English: A clause — often appearing as “this collateral secures all obligations to this lender, now existing or hereafter arising” — that sweeps your collateral across every debt you have or will ever have with that lender. It’s cross-collateralization on steroids.

The real impact: You finance a car at $12,000. Three years later, you have a $200 credit card balance with the same lender. The dragnet clause means your car secures that $200 balance — and you cannot sell or transfer the car until the credit card is paid off. Courts have consistently enforced these clauses when the language is clear.

What to do: Look for the phrase “all obligations” or “all indebtedness” in the collateral description section of any secured loan. If you see it — especially at a credit union where you have multiple products — ask the lender to limit the clause to the specific loan being signed.

Plain English: A sophisticated prepayment penalty calculation that requires you to compensate the lender for all the interest they WOULD have earned for the entire remaining loan term if you pay early. This isn’t common in personal loans but appears in some private and hard-money lending.

The real impact: You borrowed $20,000 at 12% for 5 years. After two years, you want to pay it off. A yield maintenance clause could require you to pay the full three years of remaining interest — approximately $7,200 — as a penalty, on top of the principal.

What to do: If you ever see “yield maintenance” or “make-whole” language in a personal loan agreement — pause. This is a significant financial obligation. Calculate the potential penalty before signing, not after.

19. CONFESSION OF JUDGMENT (COGNOVIT) 💀 🏦 Lender’s tool

Plain English: A clause where you waive your right to notice and a court hearing before the lender can obtain a court judgment against you. By signing, you’re pre-authorizing a court ruling in the lender’s favor if they say you’ve defaulted — without you being there to contest it.

Why this is extreme: This clause is banned in consumer loan agreements in many states — but it appears in some business loan agreements and occasionally slips into personal loan fine print from less scrupulous lenders. It essentially removes your due process rights.

What to do: If you see “confession of judgment,” “cognovit,” or “warrant of attorney” in any personal loan agreement, consult an attorney before signing. This clause has been banned in consumer agreements in many U.S. states for good reason.

20. NEGATIVE AMORTIZATION 💀 🏦 Lender’s tool

Plain English: A loan structure where your monthly payments are so low that they don’t even cover the interest due — meaning your balance actually INCREASES every month, even while you’re making payments.

The impact: You borrow $5,000. Your payment is $50/month but the interest accruing each month is $80. After six months of “paying,” you owe $5,180 — not $4,700 as you’d expect. Your debt is growing while you’re paying. This is negative amortization.

Where it appears: Rare in standard personal loans but present in some adjustable-rate mortgages (particularly older products), some income-driven loan repayment structures, and certain predatory lending products.

What to do: Ask directly: “Will any of my scheduled payments result in my balance increasing rather than decreasing?” A legitimate lender will answer this clearly. If they’re evasive, walk away.

21. MANDATORY ARBITRATION WITH CLASS ACTION WAIVER 💀 🏦 Lender’s tool

Plain English: A two-part clause that both requires arbitration (no court access) AND prevents you from joining any class action lawsuit against the lender — even if thousands of other borrowers have been harmed by the same practice.

Why this is the worst version: Standard arbitration clauses limit your individual legal options. This version also eliminates your ability to participate in collective legal action — the primary mechanism by which large-scale predatory lending practices have historically been corrected. It’s not an accident that these two waivers appear together.

What to do: Check specifically for “class action waiver” language alongside any arbitration clause. If the loan has an opt-out provision for arbitration — use it within the specified window, in writing, by certified mail.

These aren’t just complicated words. These are legal mechanisms that can cause serious, lasting financial harm.

Terms 22–30: Quick Reference Guide

The remaining nine terms are important to understand — but at lower danger levels. Here’s your rapid-fire guide:

⚠️

Term

Plain English

What To Do

🟡

22. Debt-to-Income Ratio (DTI)

Your monthly debt payments divided by your gross monthly income. Most lenders want this below 43%.

Calculate yours before applying. High DTI = worse rates or denial.

🟡

23. Hard Inquiry vs. Soft Inquiry

Soft = you checking your own credit or pre-qualification (no impact). Hard = lender pulling your credit for a loan decision (5–10 point drop, stays 2 years).

Always pre-qualify with soft pulls before allowing hard pulls.

🟠

24. Subordination Clause

Makes your loan junior to another lender’s claim — meaning they get paid first if you default. Common in second mortgages.

Understand the priority order of all your debts before adding a subordinated loan.

🟡

25. Cosigner / Guarantor

A person who agrees to repay your loan if you can’t. Their credit is at risk — not just yours — if you default.

Never ask someone to cosign without fully explaining the risk to their credit and finances.

🟢

26. Underwriting

The process the lender uses to evaluate your application — credit, income, assets, employment. This is why approvals take time.

Gather income documentation and credit reports before applying to speed the process.

🟠

27. Force-Placed Insurance

If you let required insurance lapse, the lender buys it for you — at a rate far above market — and adds the premium to your loan balance.

Never let required insurance lapse on a collateralized loan. Set calendar reminders for renewals.

🟡

28. Loan Modification

A permanent change to your loan terms — lower rate, longer term, reduced balance — usually granted during financial hardship. Not guaranteed.

If struggling, request modification early — before default. Lenders have more options available at step 1 than step 4.

🟢

29. Deferment / Forbearance

Temporary pause or reduction of payments, usually during hardship. Interest may still accrue during deferment periods.

Ask about deferment options before you need them. Knowing they exist is the first step to using them effectively.

🟡

30. Debt Consolidation

Combining multiple debts into one loan — ideally at a lower interest rate. Simplifies payments. Only helps if the consolidation rate is genuinely lower than your current rates.

Calculate total interest paid under both scenarios before consolidating. A longer term at a “lower” rate can cost more in total than shorter terms at higher rates.

7. The 5 Terms to Locate in Any Loan Agreement Before Signing {#five-terms}

You don’t have time to find all 30 terms in a 34-page loan agreement. So here are the five that matter most — find these before anything else:

Find #1: “Events of Default” — This section lists everything that can trigger default. Read every item. Some are reasonable (missed payments). Some are surprising (credit score drop, bankruptcy filing, selling collateral).

Find #2: “Arbitration” — Look for arbitration language and specifically check for an opt-out window. If it exists, plan to use it within the required timeframe.

Find #3: “Collateral” or “Security Interest” — If this is a secured loan, this section defines exactly what you’re pledging. Look for “all obligations” or “all indebtedness” language — that’s your cross-collateralization red flag.

Find #4: “Prepayment” — Find out exactly what happens if you pay early. Is there a fee? A formula? Nothing? This affects your exit strategy.

Find #5: “Interest Rate Adjustment” — Confirm whether your rate is fixed or variable. If variable, find the rate cap — the maximum your rate can reach. If there’s no cap, that’s a serious concern.

Your Fine Print Survival Kit {#survival-kit}

Before signing any loan agreement — do these five things:

✅ Ask for 24 hours to review the agreement before signing. Any legitimate lender will allow this. Any lender who pressures you to sign immediately is a red flag in itself.

✅ Use Ctrl+F (or Command+F) on digital documents to search for: “arbitration,” “acceleration,” “collateral,” “all obligations,” “balloon,” and “prepayment.” These are your five most important search terms.

✅ Calculate total repayment before signing. Multiply your monthly payment by the number of months. That’s what you’re actually paying. Compare it to the loan amount. The difference is the true cost of the loan.

✅ Ask specifically: “Is there anything in this agreement that could change my payment amount, require me to repay early, or affect my other accounts with you?” A direct question sometimes gets a direct answer.

✅ Check your state’s consumer protection laws for the specific loan type you’re signing. Some clauses — like confession of judgment in consumer loans — are banned in specific states. Know your rights before you give them away.

Thirty minutes of reading now. Potentially years of financial consequences avoided later.

9. FAQ: Real Questions Real Borrowers Ask About Loan Terms {#faq}

Q: Can I negotiate loan terms before signing? Yes — more often than most people realize. Interest rates, origination fees, prepayment penalties, and even some clauses can sometimes be negotiated — particularly with credit unions, community banks, and online lenders competing for your business. The worst they can say is no. The best outcome is a better loan.

Q: What if I already signed a loan with terms I didn’t understand? First, read the full agreement now — even after signing. Identify any terms that concern you and contact the lender directly with specific questions. If you believe a clause is illegal in your state, contact your state attorney general’s consumer protection office or a nonprofit credit counselor. The CFPB (consumerfinance.gov) also accepts complaints against lenders.

Q: Is it normal for loan agreements to be this long and complicated? Frustratingly, yes. The average personal loan agreement runs 15–35 pages. The length is partly regulatory requirement, partly genuine legal necessity — and partly designed to exhaust you into not reading it. You don’t need to read every word. You need to find the five key sections from the survival kit above.

Q: Can a lender change my loan terms after I sign? For fixed-rate loans — no, they cannot change the rate unilaterally. For variable-rate loans — yes, the rate can adjust within the terms of the agreement. Some lenders can also modify terms if you trigger certain clauses (like a credit limit decrease on a credit card). Understanding what can and cannot change is why reading those five key sections matters.

Q: What’s the fastest way to check if a lender is legitimate? Search the lender’s name on the CFPB Consumer Complaint Database at consumerfinance.gov/data-research/consumer-complaints. Check your state’s financial regulatory authority website for their license. And search the lender’s name plus “complaints” or “lawsuit” in a general search engine. Five minutes of research before applying can save you significant pain.

10. Final Thoughts: The Fine Print Isn’t Complicated by Accident {#final-thoughts}

Here’s the truth about loan fine print, in one honest paragraph:

Lenders spend money on lawyers specifically to make loan agreements difficult to understand. The confusion is not a side effect — it is a feature. An uninformed borrower signs things an informed borrower would never agree to. And when those clauses activate — when the acceleration clause fires, when the cross-collateralization surfaces, when the arbitration clause blocks legal recourse — the lender is protected. You are not.

The good news is that understanding these terms doesn’t require a law degree. It requires knowing what to look for and being willing to spend thirty extra minutes before you sign something that might follow you for three to five years.

You now know what to look for. You have the danger ratings. You have the five search terms. You have the survival kit.

🔗 Coming up — Day 7 of the Borrower’s Truth Series:“Week 1 Roundup: The 7 Most Important Things You Learned This Week (And the One Action to Take Today)”Because knowledge without action is just interesting reading.

💬 Which term surprised you most? The cross-collateralization one gets people every time. Drop it in the comments — and share this with someone about to sign a loan agreement. They’ll thank you.

The information in this blog post is provided for general

educational and informational purposes only. It does not

constitute financial, legal, or professional advice. Loan

terms, repossession laws, and consumer rights vary

significantly by state, lender, and individual circumstances.

Always verify your specific rights with a qualified attorney

or financial professional, or through official sources such

as the CFPB (consumerfinance.gov).

Part of the ConfidenceBuildings.com — Borrower’s Truth Series

🔗 Part of the “Borrower’s Truth” Series — Day 5In Day 4 we exposed how lenders use your credit score as a pricing weapon — and the legal notice you’re entitled to that almost nobody knows about. Read it here: Your Credit Score Is a Weapon — And Lenders Are Trained to Use It Against YouToday we tackle the decision that trips up almost every emergency borrower — and we’re going to actually help you make it.

1. The Question Everyone Gets Wrong {#introduction}

Here’s how every “secured vs. unsecured loan” article on the internet works:

They explain that secured loans need collateral. They explain that unsecured loans don’t. They list the pros and cons of each. They conclude with something like “the right choice depends on your situation.” And then they leave you to figure out your situation entirely on your own.

Thanks. Incredibly helpful. Really.

The problem isn’t that the information is wrong — it’s that it’s incomplete in exactly the way that costs real people real money. Because the decision between secured and unsecured isn’t just about interest rates and collateral definitions. It’s about what you actually have, what you can actually afford to risk, and what happens to your specific life if things go sideways.

A person who needs their car to get to work cannot evaluate a title loan the same way as someone with a spare vehicle. A person with $2,000 in savings has options that someone with zero savings doesn’t. These distinctions matter enormously — and nobody’s making them for you.

Until today.

This post is going to do something your competitors don’t: take you through a real decision framework based on your actual situation. Multiple solution paths. You choose the one that matches your reality. By the end, you’ll know exactly which type of loan makes sense for you — and which ones to avoid.

But first — we need to talk about something most lenders hope you never find out.

The right loan isn’t the one with the lowest rate on paper. It’s the one that fits your actual life.

2. Secured Loans: What They Are and What They’re Actually Risking {#secured-loans}

A secured loan is a loan backed by collateral — an asset you own that the lender can legally claim if you stop making payments.

The most common forms you already know: mortgages (your house is collateral), auto loans (your car is collateral), home equity loans (your home equity is collateral).

But here’s what most people don’t fully absorb: the collateral isn’t just a formality. It’s a legally binding pledge that the lender can act on without going to court in most states.

That car you’re putting up as collateral? If you miss payments, a repossession agent can legally take it from your driveway — sometimes overnight, without warning, without a court order.

That savings account you’re securing the loan against? Frozen. The lender holds it until the loan is paid. If you default, they take it.

Why do secured loans exist then? Because they genuinely offer advantages:

Lower interest rates — lenders take less risk, pass some savings to you

Higher loan amounts — collateral unlocks borrowing power beyond your credit score

Easier approval — even with damaged credit, collateral can get you approved

Longer repayment terms — more time to pay means lower monthly payments

The math is real. A secured personal loan might offer 8–12% APR where an unsecured loan for the same person would be 20–28%. On a $5,000 loan over 3 years, that gap is $800–$1,500 in total interest.

The catch — and it’s a big one: The advantage only works if you’re absolutely confident in your ability to repay. Because the downside isn’t just a hit to your credit score. It’s losing something that matters to your daily life.

3. Unsecured Loans: The Freedom That Costs More {#unsecured-loans}

An unsecured loan requires no collateral. The lender approves you based on your credit score, income, and debt-to-income ratio alone. Your signature is the only guarantee they get.

The advantages are real:

No asset at risk — if things go wrong, you don’t lose your car or your home

Faster approval — no collateral valuation means quicker processing

Flexible use — funds can go toward almost anything

Available from banks, credit unions, and online lenders

The cost is also real:

Higher interest rates — lenders price in the extra risk they’re taking

Stricter credit requirements — most good unsecured loans want a 640+ credit score

Lower loan amounts — without collateral backing, lenders cap what they’ll offer

Shorter repayment terms — less time to pay means higher monthly payments

What happens if you default on an unsecured loan?

The lender can’t immediately take your car or your couch. But don’t mistake “no collateral” for “no consequences.” If you stop paying an unsecured loan, the lender will report you to credit bureaus, send the debt to collections, and can eventually sue you for repayment. If they win — and they usually do — a court can order wage garnishment, meaning they take a percentage of your paycheck directly. They can also place a lien on property you own.

No immediate repossession. Still deeply unpleasant.

Lower rate or protected assets — understanding this trade-off is the whole decision.

4. The Hidden Third Option Nobody Talks About {#third-option}

Here’s the section your competitors skipped — and it might be the most useful thing in this entire post for certain borrowers.

There’s a third type of loan that sits between secured and unsecured: the cash-secured loan (also called a share-secured loan or savings-secured loan).

Here’s how it works: you borrow against money you already have in a savings account or certificate of deposit. The lender freezes that amount as collateral but gives you a loan equal to it — which you then repay with interest over time.

“Wait,” you’re thinking. “Why would I borrow money I already have?”

Three very good reasons:

Reason 1 — Credit building. If you have damaged or thin credit, a cash-secured loan lets you borrow and repay, creating a positive payment history on your credit report — without risking an asset you truly can’t afford to lose.

Reason 2 — Protecting your emergency fund. If you have $1,000 saved but need $1,000 for an emergency, withdrawing it wipes out your safety net entirely. A cash-secured loan lets you access that value while keeping the account (frozen, not gone) — and once repaid, your fund is intact.

Reason 3 — Extremely low interest rates. Because the risk to the lender is essentially zero (they already have your money), cash-secured loans typically charge 2–4% above the savings account rate — often 4–7% APR total. That’s cheaper than almost any other personal loan option.

Where to get one: Credit unions offer these most commonly, often called “share-secured loans.” Some online banks and community banks offer them too.

The downside: You need to have the money first. Which makes this option most useful for someone who has savings but doesn’t want to fully drain them, or someone using this specifically as a credit-building tool.

💡 Real scenario where this makes sense: You have $800 in savings. Your car needs $600 in repairs. Instead of withdrawing the $600 (leaving you with just $200 as a buffer), you take a $600 cash-secured loan at 5% APR, keep your savings account intact (frozen as collateral), and repay $52/month for 12 months. Total interest cost: about $33. Your emergency fund is effectively preserved, your credit gets a boost, and the repair gets done.

5. The Truth About Repossession (That Your Lender Won’t Volunteer) {#repossession-truth}

This is the section that exists nowhere in standard secured vs. unsecured loan content — and it’s the most important thing an emergency borrower needs to understand before putting up collateral.

In most U.S. states, lenders can repossess your car without going to court and without giving you advance notice.

Read that again. No court. No warning. They can legally send a repossession agent to your home or workplace and take the vehicle — as long as they do so without “breaching the peace” (meaning without force or confrontation).

You could wake up tomorrow morning and your car could be gone. Legally. Without you having any say in it.

This is not a horror story — it’s standard contract law in most states. When you sign an auto loan or use your vehicle as collateral for any secured loan, you’re signing a document that gives the lender this right. Most people never read that clause. Now you know it exists.

The repossession timeline in practice:

Most lenders don’t actually repossess on day one of a missed payment. The typical sequence looks like this:

Day 1–30: Payment missed. Lender calls and emails. Late fees begin.

Day 30–60: Loan goes delinquent. Credit bureaus are notified. More aggressive outreach.

Day 60–90: Account approaches default status. Lender may offer hardship options at this stage — ask for them.

Day 90+: Default declared. Repossession authorized. Can happen any day after this point.

What you can do before it gets to step 4:

Call your lender before you miss a payment — not after. Lenders have significantly more options available to you at step 1 than at step 4. Ask specifically about:

Hardship programs

Payment deferral (moving a payment to the end of the loan)

Loan modification (restructuring your payments)

Voluntary surrender options (which preserve more of your credit than forced repossession)

The single worst thing you can do is go silent and hope they won’t notice. They will notice. And by the time they act, your options have narrowed considerably.

⚠️ Disclaimer: Repossession laws vary by state. Some states require notice before repossession; others do not. Always verify your specific state’s laws through your state attorney general’s office or a qualified legal professional.

In most states, they don’t need to warn you. They don’t need a court order. They just need you to have missed enough payments.

6. The Deficiency Balance Trap — You Can Lose the Car AND Still Owe Money {#deficiency-balance}

Here’s the part that genuinely shocks people — and that almost no consumer finance content explains clearly.

When a lender repossesses your car and sells it at auction, the sale price rarely covers what you still owe on the loan. Cars depreciate. Auction prices are often well below market value. And the lender adds repossession and storage fees to your balance before the auction even begins.

Example:

You owe $12,000 on your secured loan

Car is repossessed and sold at auction for $7,500

Repossession and storage fees: $800

Remaining balance (deficiency): $5,300

You still owe $5,300. On a car you no longer have. That you can no longer drive to work.

This is called a deficiency balance — and the lender can and often will pursue you for it through collections or a lawsuit. In most states, they have every legal right to do so.

What this means for your decision:

Before putting up any asset as collateral for an emergency loan, you need to honestly ask yourself: “If I lose this asset AND still owe money on it, what does my life look like?”

If the answer to that question involves losing your ability to work, care for your family, or maintain basic stability — then a secured loan against that asset carries more risk than the lower interest rate is worth.

⚠️ Disclaimer: Deficiency balance laws vary by state. Some states have anti-deficiency protections that limit or prohibit lenders from pursuing deficiency balances. Research your specific state’s laws at your state attorney general’s website or consult a legal professional before making decisions based on this information.

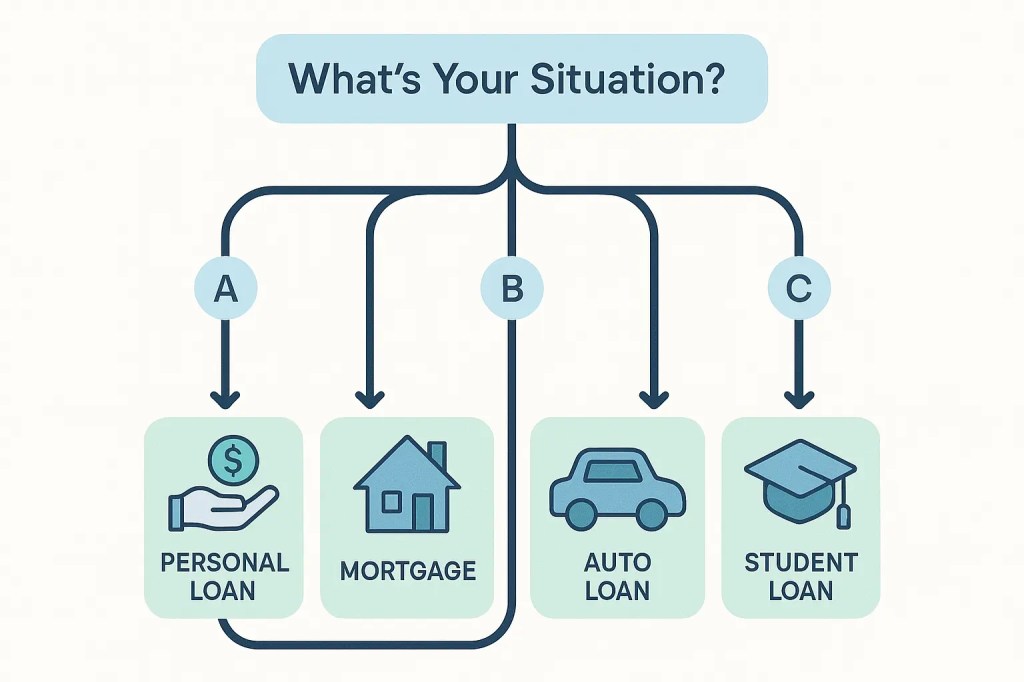

7. The “Choose Your Solution” Decision Framework {#decision-framework}

This is the section that doesn’t exist anywhere else. Every competitor tells you what secured and unsecured loans are. None of them help you choose.

Here’s how to use this framework:

Step 1: Answer these three questions honestly:

Question A: Do you own a valuable asset (car, home, savings account with $500+) that you could use as collateral?

Yes → Go to Question B

No → You’re on Path C or D (scroll down)

Question B: Is that asset essential to your daily life and income?

My car is how I get to work → Secured loan against it = HIGH RISK

I have savings I could borrow against → Cash-secured loan = LOW RISK option

I have home equity → Secured option exists but involves long process

Question C: What is your current credit score range?

680+ → Unsecured loan is accessible to you

580–679 → Limited unsecured options, secured or cash-secured may be better

Below 580 → Unsecured loan very difficult; secured or alternatives are your path

Now find your path below:

8. Solution Path A: You Have Assets and Good Credit (Score 680+) {#path-a}

Your situation: You own a car, home equity, or savings. Your credit is solid. You have options — which means your job is to choose the cheapest one, not just the first available one.

Best solutions in order of preference:

Solution 1 — Unsecured personal loan (best choice) With 680+ credit, you can access unsecured personal loans at reasonable rates (typically 8–18% APR). This protects your assets completely. No collateral risk. Shop at least 3 lenders — credit unions first, then online lenders, then banks. Use soft-pull pre-qualification tools to compare without hitting your credit score.

Solution 2 — Cash-secured loan If your savings account has enough to cover the emergency, a cash-secured loan preserves the fund while giving you access to the value. Especially useful if you’re also trying to build credit.

Solution 3 — HELOC or home equity loan If you own a home with equity and the amount needed is substantial ($5,000+), a home equity line offers low rates — but takes longer to process and puts your home at risk. Not ideal for true emergencies due to timeline, but worth knowing exists.

What to avoid: Secured personal loans using your car as collateral when you have good credit and could qualify for unsecured options. The rate savings don’t justify the asset risk when you have alternatives.

9. Solution Path B: You Have Assets but Damaged Credit (Score Below 640) {#path-b}

Your situation: You own things but your credit has taken hits. The lower rate of a secured loan is genuinely attractive — but the asset risk is real and you need to choose carefully.

Best solutions in order of preference:

Solution 1 — Cash-secured loan (often best choice) Borrowing against your own savings at a credit union costs almost nothing in interest, requires no credit check in most cases, and builds your credit score. If you have any savings at all, this should be your first call.

Solution 2 — Credit union PAL loan If you’re a credit union member, Payday Alternative Loans (PALs) are capped at 28% APR — significantly better than most options available to damaged-credit borrowers. No collateral required.

Solution 3 — Secured personal loan (proceed with caution) If the amount needed is larger and your car is paid off, a secured personal loan against the vehicle might be your most accessible option. But only if: you’re confident about repayment, you have a realistic backup plan if income is disrupted, and the asset is not your only means of getting to work.

What to avoid: Title loans. They look like secured personal loans but are predatory products — triple-digit APRs, extremely short repayment windows, and you can lose your car to a lender charging 200%+ APR. Never the right answer.

10. Solution Path C: No Assets, Good Credit (Score 680+) {#path-c}

Your situation: You don’t have collateral to offer, but your credit score gives you real options in the unsecured loan market.

Best solutions in order of preference:

Solution 1 — Unsecured personal loan This is your primary tool and it works well at 680+. Compare offers from credit unions, online lenders (LightStream, SoFi, Upgrade), and your existing bank. Pre-qualify with multiple lenders using soft pulls. Look for: fixed rate, no origination fee if possible, and no prepayment penalty.

Solution 2 — 0% intro APR credit card If your credit is 680+ and you need funds for a specific purchase (not cash), a 0% intro APR credit card for 12–18 months is essentially a free loan if paid off before the promo period ends. Apply only if you’re disciplined about the payoff deadline.

Solution 3 — Employer advance or earned wage access Before taking any loan, check whether an employer advance covers the need. Free, fast, and doesn’t affect your credit. Always worth asking first.

What to avoid: Applying to too many lenders at once (multiple hard pulls in a short period without rate-shopping protection). Shop within a 14-day window to minimize credit score impact.

Your situation: This is the hardest path — and the one most targeted by predatory lenders. No collateral, limited credit options, urgent need. Your options are narrower, but they exist.

Best solutions in order of preference:

Solution 1 — Alternatives before any loan Before borrowing anything, revisit Day 3 of this series — direct negotiation, 211.org community assistance, employer advances, and selling items can frequently resolve emergencies without debt.

Solution 2 — Credit union PAL loan Even with damaged credit, many credit unions offer PAL loans to members. The 28% APR cap makes this the most responsible borrowing option available to you. Join a credit union today if you’re not a member — even if you can’t get a PAL immediately, membership starts the clock.

Solution 3 — Secured credit card (credit rebuilding first) If the emergency isn’t today but you’re planning ahead, a secured credit card with a $200–$500 deposit builds your credit score over 6–12 months — moving you from Path D toward Path C or B where options improve significantly.

Solution 4 — Online lenders for bad credit (with extreme caution) Lenders like Upstart and OppFi serve sub-580 credit scores but at high rates (36–199% APR depending on score and lender). If you go this route, borrow the minimum needed, commit to full repayment, and read our Day 1 guide on hidden fees before signing.

What to absolutely avoid: Payday loans. Title loans. Any lender advertising “guaranteed approval regardless of credit.” These products are designed to keep Path D borrowers in Path D permanently.

💙 If you’re on Path D right now, please know: this path has exits. The exit signs are just less obvious, and the walk is longer. But people move from damaged credit and no assets to genuine financial stability all the time — usually by making a series of small, right decisions exactly like the ones in this series. You’re already making them by being here.

Your situation determines your best solution. Find your path and follow it — don’t let a lender choose for you.

Side-by-Side Comparison: All Loan Types for Emergency Borrowers {#comparison}

Loan Type

Typical APR

Collateral

Credit Needed

Asset Risk

Best For

Unsecured Personal Loan

8–28%

None

640+

None

Good credit, no assets to risk

Secured Personal Loan

6–18%

Car, savings, other asset

560+

HIGH — asset can be seized

Lower rate when confident in repayment

Cash-Secured Loan

4–7%

Your own savings account

Any

Low (your own money)

Credit building + fund preservation

Credit Union PAL

Max 28%

None

Any (member)

None

Any borrower who is a CU member

Home Equity Loan

6–10%

Your home

620+

VERY HIGH — home at risk

Homeowners, large amounts, non-urgent

Title Loan

200–400%

Your car title

None

EXTREME — avoid entirely

Almost never — last resort only

Payday Loan

300–400%

None

None

Debt spiral risk

Avoid — see Day 3 alternatives first

⚠️ Disclaimer: APR ranges above are illustrative estimates based on general market conditions as of early 2026. Actual rates vary significantly by lender, credit profile, loan amount, and other factors. Always obtain personalized quotes before making borrowing decisions.

13. Before You Sign: The 5 Questions That Protect You {#before-you-sign}

Regardless of which path and which loan type you choose, ask these five questions before signing anything:

Question 1: “If I miss two payments, what exactly happens — and how quickly?” Get the specific timeline in writing. Know the grace period, the default trigger date, and what action the lender takes first. Surprises after signing are always worse than clarity before.

Question 2: “Can you be repossessed without advance notice in my state?” For any secured loan, ask your lender directly and verify with your state’s consumer protection office. This changes your risk calculation significantly.