"MBA in Finance | Personal Finance & Borrower Education"

Author: Laxmi Hegde

Hi, I’m Laxmi Hegde 👋

MBA in Finance by degree, restaurant owner by profession, and full-time workaholic by… let’s call it “diagnosis.” When I’m not crunching numbers or managing my restaurant, you’ll probably find me chasing new ideas, planning my next big move, or spoiling my dogs like they’re royalty. 🐶✨

This blog is my creative escape—a place where I share travel adventures, skincare secrets, and a few life hacks I’ve picked up along the way. Think of it as part travel guide, part lifestyle diary, with a dash of humor (because life’s too short to be serious all the time).

Oh, and in case you’re wondering: yes, I’m still learning how to not work 24/7. Spoiler alert—I’m failing gloriously. 😅

Welcome to my little corner of the internet—grab a coffee, stay a while, and let’s explore together!

8 signs your financial hardship is genuinely behind you — not just on a good day, but for real this time.

01

You stop checking your bank balance with one eye closed

02

You have a small buffer — and you leave it alone

03

A surprise expense doesn’t destroy your whole month

04

Your credit score has moved — in the right direction

05

You’re paying bills on time — without scrambling

06

You’ve said no to a bad loan — and meant it

07

You think about next month — not just today

08

Money anxiety is background noise — not the main event

Most people who escape financial hardship don’t realize it for months. This post exists so you don’t miss your own finish line.

⚠ For educational purposes only. Not legal advice. The information in this post is intended to help you recognize general signs of financial recovery. Everyone’s financial situation is different. If you are dealing with ongoing debt, collections, or legal matters, please consult a licensed financial advisor or attorney in your area. Nothing on this site creates a professional relationship of any kind.

📖 About This Series

The Borrower’s Truth Series is a 30-day financial education series by Laxmi Hegde, MBA in Finance. Over 30 posts, we’ve pulled back the curtain on predatory lending, fine print traps, debt collection tactics, credit repair, bankruptcy — and everything lenders hope you never figure out.

You’ve made it to Day 28. That’s not nothing. Most people quit financial education the moment it gets uncomfortable. You didn’t. And today we’re doing something a little different — we’re not talking about what can go wrong. We’re talking about how to know when things have actually gone right.

Consider this your official checklist for recognizing your own comeback. You’ve earned the read.

⭐ Essential Reading — Start Here

Free: The Loan Clause Checklist

Before you ever sign another loan agreement, run it through this checklist. 30 clauses. Plain English explanations. The exact traps lenders bury in fine print — and how to spot every single one.

When checking your bank balance stops feeling like defusing a bomb — that’s recovery. ConfidenceBuildings.com · Borrower’s Truth Series 2026

📌 Quick Answer

Financial hardship is behind you when your stability is boring. Not perfect — boring. You pay bills without drama. You sleep without running numbers in your head. You have a small cushion and you don’t immediately spend it. Boring is the goal. Boring is winning.

Nobody sends you a certificate when you climb out of financial hardship. There’s no email. No confetti. No notification that says “Congratulations — the hard part is over.”

Which is deeply unfair, because you did the work. You negotiated. You disputed. You said no to the payday loan. You read the fine print. You showed up to this series for 28 consecutive days. You deserve at least a balloon.

Since we can’t mail you one, here’s the next best thing: 8 concrete, measurable signs that your financial hardship is genuinely behind you — not just on a good Tuesday, but for real.

Sign 01

You Check Your Bank Balance Without Bracing for Impact

At peak financial hardship, checking your bank balance is a full-body experience. You open the app. You squint. You hold your breath like you’re defusing something. You check with one eye closed just in case the number is worse than you imagined.

When that ritual stops — when you open the app the same way you’d check the weather, casually, without dread — that’s a real sign. It means your balance has become predictable enough that it no longer qualifies as a horror movie.

You don’t need a huge number in there. You just need a number that doesn’t surprise you anymore.

Sign 02

You Have a Small Buffer — and You Actually Leave It Alone

Having $400 in savings is not the sign. Plenty of people have $400 in savings on a Monday and $0 on a Friday because something always comes up — or because it felt too tempting sitting there looking useful.

The sign is having $400 — and leaving it there. Through two weekends. Through a sale you wanted to shop. Through a craving you chose to ignore. The buffer surviving is evidence that your relationship with money has quietly, fundamentally changed.

The CFPB defines a basic financial safety net as having at least one month of expenses accessible without borrowing. Getting there — and staying there — is a measurable milestone.

Sign 03

A Surprise Expense Doesn’t Destroy Your Entire Month

The car needs a new tire. The dog ate something suspicious. The dentist finds a thing. During financial hardship, any one of these events triggers a full crisis — calls to lenders, overdraft fees, missed bills, a week of stress that bleeds into everything.

Recovery looks like this: the unexpected expense is annoying. You pay it. You adjust. You move on. The month continues. That ability to absorb a financial punch without going down — that’s resilience. That’s the opposite of where you started.

Life will always produce surprise expenses. What changes is your ability to take the hit and keep standing.

56%

of Americans cannot cover a $1,000 emergency expense without borrowing. If you can — you are already ahead of the majority.

Source: Bankrate Annual Emergency Savings Report

Sign 04

Your Credit Score Has Moved — in the Right Direction

Your credit score is basically a slow-moving report card that reflects the last two to seven years of your financial life. It does not care about your feelings. It does not know you’ve been trying really hard. It just watches what you do and takes notes.

So when it moves up — even 20 points, even 10 — it means the score has noticed. On-time payments noticed. Lower balances noticed. No new desperate credit applications noticed. The number going up is the universe’s way of saying: the pattern has changed.

Check your free report at AnnualCreditReport.com. If the trend is upward — even slowly — that’s not nothing. That’s proof.

Sign 05

You’re Paying Bills on Time — Without the Last-Minute Scramble

There’s a version of paying bills on time that still involves hardship: you pay them, but only after two hours of financial gymnastics, moving money between accounts, calling to ask for a three-day extension, and aged ten years in the process.

The sign we’re looking for is simpler. The bill arrives. The money is there. You pay it. That’s the whole story. No drama. No negotiation with yourself. No robbing Peter to pay Paul and hoping Paul doesn’t notice.

When paying bills becomes routine rather than a monthly survival event — that’s a sign your foundation is holding.

Sign 06

You’ve Said No to a Bad Loan — and Meant It

This one is behavioral, and it might be the most powerful sign on this list. During peak hardship, the payday loan offer doesn’t feel predatory — it feels like a lifeline. You know the rate is terrible. You know you’ll regret it. You take it anyway because the alternative feels worse.

Recovery looks like standing in front of that same offer — same desperation in the marketing, same urgent language, same 400% APR hiding in the footnotes — and saying no. Not because you have unlimited options. Because you’ve learned enough to know what that yes actually costs.

Turning down a bad loan when you’re still a little tight? That’s not just recovery. That’s wisdom. And wisdom doesn’t show up on a credit report — but it protects everything that does.

Sign 07

You Think About Next Month — Not Just Today

Financial hardship collapses your time horizon. When you’re in survival mode, the concept of “next month” is almost abstract — you’re too busy managing today to think that far ahead. Planning feels like a luxury. Budgeting feels like a joke. The future can wait; you have a bill due Thursday.

When your time horizon starts to expand — when you find yourself thinking about next month’s rent before this month is even over, or planning a purchase three weeks out — that’s your brain recalibrating. It means you’re no longer in pure survival mode. You have enough stability to look further than tomorrow.

That mental shift is quiet, easy to miss, and genuinely significant.

Sign 08

Money Anxiety Is Background Noise — Not the Main Event

Financial stress at its worst is all-consuming. It follows you into conversations you’re supposed to be present for. It sits next to you at dinner. It wakes you up at 3am to run numbers that don’t add up no matter how many times you try. It is the main event, every day, whether you wanted to buy a ticket or not.

Recovery doesn’t mean zero financial anxiety — that’s not a realistic bar and anyone telling you otherwise is selling something. Recovery means the anxiety has been demoted. It still exists, somewhere in the background, but it’s no longer running the show. You can have a whole day where you didn’t think about debt once. That counts.

If money used to be the loudest thing in your life and it’s gotten quieter — you’re further along than you think.

A note on not recognizing yourself in these signs yet:

That’s okay. These signs aren’t a test you pass or fail — they’re a map. If you recognize two of them, you’re moving. If you recognize five, you’re further than you think. If you don’t recognize any yet, you now know exactly what you’re building toward. Keep going.

A small buffer you actually leave alone — one of the most underrated signs of financial recovery. ConfidenceBuildings.com · Borrower’s Truth Series 2026

Real Stories. Real Recovery.

D

Danielle, 34 — Cincinnati, OH

Composite story · For educational illustration

“I knew things were getting better when I stopped doing the math in my head at the grocery store. For two years, I’d stand in the cereal aisle calculating whether I could afford the name brand or if I needed to put something back. One day I just… didn’t. I grabbed what I wanted and kept walking. I didn’t even realize it had changed until I got to the car.”

What held her back

Danielle had been in recovery for nearly eight months before she recognized it. She kept waiting for a dramatic moment — a number, a milestone, a feeling. The actual sign was quiet and happened in a cereal aisle on a Wednesday.

What this shows

Recovery doesn’t announce itself. It shows up in small, unguarded moments. The grocery store math stopping. The app opening without dread. Notice those moments — they’re the real data.

RM

Attorney Rachel Morrow

Fictional consumer rights attorney · Educational illustration only

“In my experience, the clients who have the hardest time recognizing their own recovery are the ones who were in hardship the longest. The vigilance that kept them safe during the crisis becomes the thing that won’t let them believe it’s over. Learning to trust your own stability is a skill — and it takes practice.”

Legal & Financial Context

Financial trauma has documented psychological effects. Studies in behavioral economics show that people who experienced prolonged scarcity often continue making scarcity-based decisions even after their material situation has improved — a pattern researchers call “scarcity mindset persistence.” Recognizing the signs of recovery is partly cognitive work, not just financial.

Bottom Line

If your numbers say you’re recovering but your gut still says you’re in danger — trust the numbers while you work on the gut. Both matter. Neither is wrong.

T

Trevor, 41 — Phoenix, AZ

Public case · Based on documented consumer experience

“I had paid off my last collection account and my credit score had gone up 60 points. By every measurable standard I was doing better. But I still felt broke. I kept telling myself it wasn’t real yet, that something would go wrong. My therapist finally asked me: what would have to happen for you to believe you made it? I didn’t have an answer. That was the problem.”

What held him back

Trevor had never defined what “better” actually looked like. Without a finish line, he couldn’t recognize when he crossed it. He kept moving the goalposts without realizing it.

What this shows

Define your finish line before you need it. Write down three specific signs that would tell you the hardship is behind you. When you hit them — believe them.

RM

Attorney Rachel Morrow

Fictional consumer rights attorney · Educational illustration only

“I’ve seen people walk out of bankruptcy proceedings with a clear legal fresh start and immediately make the same decisions that got them there. And I’ve seen people with no legal intervention at all completely transform their financial lives through behavioral change alone. The numbers matter. The mindset matters more.”

Legal & Financial Context

Consumer protection law can discharge debt, stop collection calls, and reset credit timelines — but it cannot reset habits. The legal system handles the financial mechanics. The behavioral work is yours. Both are necessary for lasting recovery.

Bottom Line

A legal fresh start is a tool. What you build with it is entirely up to you — and entirely possible.

P

Priya, 29 — Atlanta, GA

Composite story · For educational illustration

“The moment I knew I was out was when my cousin asked to borrow money and I said yes without panicking. A year earlier, that question would have sent me into a spiral — do I have it? Can I afford to? What if I need it? This time I just checked, saw I had enough, and said yes. It felt completely normal. It wasn’t normal at all. It was huge.”

What she almost missed

Priya nearly dismissed the moment as unimportant. It took her a few days to realize that her calm reaction to a financial request — something that used to terrify her — was the sign she’d been waiting for.

What this shows

Recovery shows up in your reactions, not just your balances. Pay attention to how you feel when money comes up — not just what your bank statement says.

RM

Attorney Rachel Morrow

Fictional consumer rights attorney · Educational illustration only

“Nobody teaches you how to recognize financial recovery. We teach people how to get out of debt. We don’t teach them how to believe they’re out. That gap is where a lot of people get stuck — technically recovered, emotionally still in the storm.”

Legal & Financial Context

Consumer financial protection resources — including those from the CFPB — focus primarily on crisis intervention. Recovery recognition is underserved in financial literacy education. This post exists to address exactly that gap.

Bottom Line

Knowing you’re recovering is part of recovering. Don’t skip it.

A surprise expense used to destroy the whole month. Now it’s just a flat tire. ConfidenceBuildings.com · Borrower’s Truth Series 2026

Frequently Asked Questions

How long does it take to recover from financial hardship?

There is no universal timeline. Recovery depends on the depth of the hardship, the type of debt involved, your income stability, and the steps you take. What research does show is that consistent on-time payments over 12–24 months produce measurable credit improvement, and that building even a small emergency fund significantly reduces the likelihood of returning to crisis.

The more useful question is not “how long” but “what does progress look like for me?” — and then measuring against that, not against someone else’s timeline.

What credit score means I’ve recovered from financial hardship?

There is no single score that signals recovery — but crossing into the “fair” range (580–669) restores access to most standard credit products. Reaching “good” (670+) typically unlocks better interest rates and more favorable loan terms. The CFPB notes that scores above 670 are generally considered by lenders to represent lower risk borrowers.

More important than hitting a specific number is the direction of travel. A score moving from 520 to 580 over 12 months is recovery in action — even if it doesn’t feel dramatic yet.

How much savings do I need before I’m considered financially stable?

The standard guidance is three to six months of living expenses — but that figure can feel impossible when you’re just climbing out. A more realistic starting benchmark is $500 to $1,000 as an initial emergency buffer. Research from the Urban Institute found that having even $250 in liquid savings dramatically reduces the likelihood of missing a bill payment or taking on high-cost debt after an income disruption.

Stability is not a fixed dollar amount. It is the ability to absorb a small shock without borrowing. Start there.

Is it normal to still feel anxious about money even after things improve?

Completely normal — and well documented. Financial stress activates the same neural pathways as other forms of chronic stress. When scarcity has been the baseline for an extended period, the brain adapts to operate in threat-detection mode. That adaptation does not switch off the moment your bank balance improves.

Ongoing financial anxiety after objective improvement is sometimes called “post-hardship stress.” It is common, it is real, and it is not a sign that your recovery isn’t genuine. If it significantly affects your daily life, speaking with a mental health professional who specializes in financial anxiety is worth considering.

What are the biggest signs I might be slipping back into financial hardship?

The early warning signs include: relying on credit cards for regular monthly expenses, missing or making minimum-only payments, depleting your emergency fund without replenishing it, taking on new high-interest debt to cover existing obligations, and avoiding looking at your accounts altogether.

None of these signs mean you’ve failed. They mean it’s time to act early — before small slides become big ones. The CFPB’s free financial tools and nonprofit credit counseling services are available at no cost and can help you course-correct quickly.

Where can I get free help tracking my financial recovery?

Several free government and nonprofit resources exist specifically for this purpose. AnnualCreditReport.com provides free weekly credit reports from all three bureaus. The CFPB’s financial well-being tools include self-assessments you can use to track progress over time. The National Foundation for Credit Counseling (NFCC) connects consumers with nonprofit credit counselors at low or no cost.

You do not need to pay anyone to track your own recovery. The tools exist. They’re free. Use them.

Nobody warned me that getting out of financial hardship would feel suspicious. Like the other shoe was always about to drop. Like the stability was a trick and any minute the real bill would arrive. Turns out that feeling has a name — and it’s extremely common — and knowing that helped me more than any spreadsheet ever did.

Here’s what I want you to take from today: recovery is not a single moment. It’s a collection of small, undramatic moments that you almost miss because you’re waiting for something bigger. The cereal aisle. The app you opened without flinching. The loan you said no to without a second thought. Those are the moments. Don’t scroll past them.

We have two days left in this series. Day 29 is the Smart Borrower Framework — everything distilled into a system you can actually use. Day 30 is the finale. I’ve been writing this series for 28 days and I still haven’t figured out how to end it without getting a little emotional, which is embarrassing but also probably fine.

You made it out. Here’s your proof: you’re still reading. See you tomorrow.

— Laxmi Hegde, MBA in Finance Founder, ConfidenceBuildings.com · Borrower’s Truth Series · Day 28 of 30

When paying bills becomes routine instead of a monthly survival event — that’s your foundation holding. ConfidenceBuildings.com · Borrower’s Truth Series 2026

📚 Research Note & Primary Sources

This post was researched and written by Laxmi Hegde, MBA in Finance, as part of the 30-day Borrower’s Truth Series on ConfidenceBuildings.com. All content is intended for general financial education only. Nothing in this post constitutes legal or financial advice. Individual circumstances vary — consult a licensed professional for guidance specific to your situation.

Reader stories marked as “composite” are illustrative fictional accounts based on common consumer experiences. Stories marked “public case” are based on documented consumer experiences in the public record. Attorney Rachel Morrow is a fictional character created for educational illustration purposes only.

This article is Day 28 of the 30-day Borrower’s Truth Series published on ConfidenceBuildings.com. It was researched and written by Laxmi Hegde, MBA in Finance. All statistics, citations, and regulatory references are sourced from publicly available government and nonprofit resources and are accurate to the best of the author’s knowledge at time of publication.

This content is intended for general financial education only. It does not constitute legal, financial, or professional advice of any kind. Reader stories are either composite illustrations or based on publicly documented consumer experiences — no personally identifiable information is used. Attorney Rachel Morrow is a fictional character created solely for educational illustration.

Financial situations vary significantly by individual. Readers are encouraged to consult licensed financial advisors, nonprofit credit counselors, or consumer protection attorneys for guidance specific to their circumstances.

Read the complete 30-day series — all posts, all weeks, all in one place:

The B-Word: An Honest Guide to Bankruptcy Without the Shame

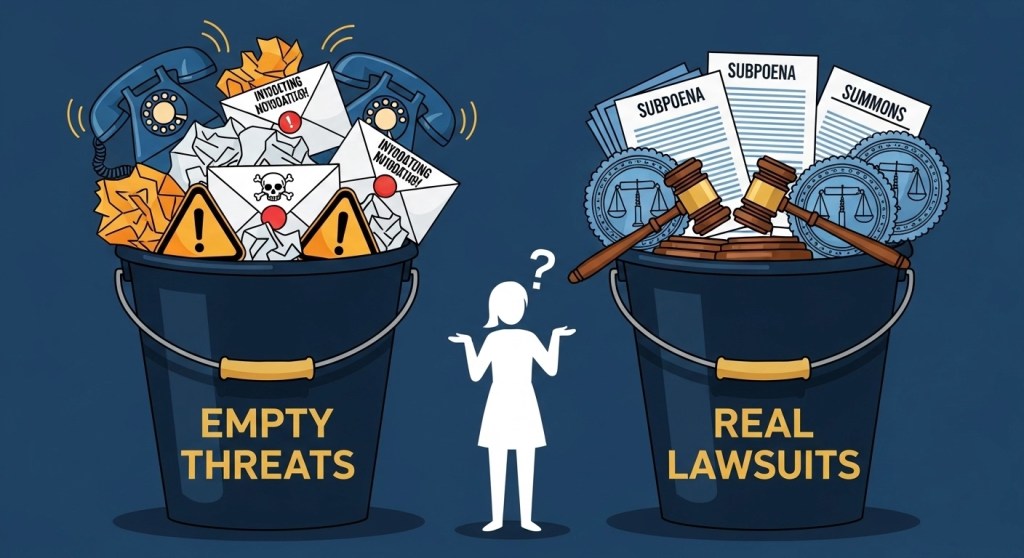

Bankruptcy has a reputation problem. People avoid it the way they avoid checking their bank balance after the holidays — eyes closed, hoping it gets better on its own. Sometimes it doesn’t. And sometimes bankruptcy is the most financially intelligent decision available. Today we talk about it honestly, without the shame spiral.

400K+

consumer bankruptcy filings in the US every year — you are not alone in considering this

Source: U.S. Courts

4–6

months to complete a Chapter 7 bankruptcy — faster than most people expect

Source: U.S. Courts

2 yrs

typical timeframe to begin qualifying for mainstream credit products after Chapter 7

Source: CFPB

What You’ll Learn Today

What bankruptcy actually is — and what it definitely is not

Chapter 7 vs Chapter 13 — the honest comparison nobody simplifies properly

The 6 signs bankruptcy may be the right answer for your situation

What happens to your assets, your credit, and your life after filing

The first three steps to take if you are seriously considering it

⚠ For educational purposes only. Not legal advice. Bankruptcy law is complex, federally governed, and varies significantly based on your individual financial circumstances, state exemptions, income level, and debt type. Nothing in this post constitutes legal advice or a recommendation to file for bankruptcy. The decision to file bankruptcy has serious long-term financial and legal consequences that require careful evaluation by a licensed bankruptcy attorney. Many bankruptcy attorneys offer free initial consultations — always consult one before making any decision. The U.S. Courts, CFPB, and U.S. Trustee Program are referenced for informational purposes only — none of these organisations endorse this content.

📚 Borrower’s Truth Series — Week 4 of 5

After You Borrow

Week 4 has covered the full financial recovery toolkit — exiting the payday loan cycle, stopping collector harassment, fixing credit report errors, rebuilding your score, and negotiating with creditors. Today we tackle the topic most people Google at midnight and then immediately close the tab on. Bankruptcy. We are going to talk about it like adults — calmly, honestly, and without the drama that makes people avoid the very information they need.

▶ Day 27 — The B-Word: An Honest Guide to Bankruptcy Without the Shame (you are here)

⭐ Essential Reading — Start Here

Considering Bankruptcy? First — Know Exactly What You Signed.

Before you decide whether bankruptcy is right for you, it helps to know exactly what your existing loan agreements say — particularly clauses that affect which debts are dischargeable, which assets may be at risk, and what your lenders can do during the process. The Loan Clause Checklist identifies the exact language that matters most. Free. No email required. No awkward phone calls with people you owe money to.

Why It Matters Before You Decide

Cross-collateralization clauses — affects which assets are tied to which debts

Acceleration clause — triggers full balance due on default or bankruptcy filing

Arbitration clause — affects your legal options during the bankruptcy process

Security interest language — determines what a lender can claim in bankruptcy

Free resource · No sign-up required · Referenced throughout the Borrower’s Truth Series

Chapter 7 and Chapter 13 both lead to resolution — the right path depends entirely on your situation

📌 Quick Answer

Bankruptcy is a legal process — not a character flaw — that allows individuals overwhelmed by debt to either eliminate most of what they owe (Chapter 7) or restructure it into a manageable repayment plan (Chapter 13). It is governed by federal law, overseen by a court, and designed specifically for people whose debt has become mathematically impossible to resolve any other way. It is not the end of your financial life. For many people it is the beginning of it.

What Bankruptcy Actually Is — And What It Definitely Is Not

Let’s start with what bankruptcy is not. It is not an admission that you are irresponsible. It is not something that only happens to people who made terrible decisions. It is not a scarlet letter that follows you forever. And it is definitely not something only other people have to deal with — 400,000 Americans file every year, including people who have MBAs, run businesses, and read financial literacy blogs at midnight. 😊

What bankruptcy actually is: a legal tool built into the U.S. Constitution — Article I, Section 8, to be specific — that gives people a structured way to resolve debt they genuinely cannot repay. Congress included it in the Constitution because the founders understood that financial hardship happens to good people and that a functioning economy needs a mechanism for people to start over.

The most common causes of personal bankruptcy are not reckless spending. According to research cited by the American Journal of Public Health, medical debt is a leading contributor to bankruptcy filings. Job loss is another. Divorce is another. These are not character failures — they are life events that happen to millions of people every year.

Bankruptcy Myths vs Reality — Let’s Clear This Up Once and For All

❌ Myth

“You lose everything you own.”

✅ Reality

State exemptions protect most essential assets — including your home equity up to a limit, your car up to a value, your retirement accounts, and your household goods. Most Chapter 7 filers are “no-asset” cases — meaning there is nothing for creditors to claim.

❌ Myth

“Your credit is ruined forever.”

✅ Reality

Chapter 7 stays on your report for 10 years — but most filers begin qualifying for secured cards within months and mainstream credit within 2 years. A bankruptcy plus 2 years of positive history often produces a better score than years of continued delinquency.

❌ Myth

“Everyone will know you filed.”

✅ Reality

Bankruptcy is technically public record — but nobody is browsing court filings looking for your name. Employers and landlords only see it if they run a credit check. Most people in your life will never know unless you tell them.

❌ Myth

“You can’t get a job after bankruptcy.”

✅ Reality

Most employers do not check credit at all. Those that do — typically financial services or government roles requiring security clearance — may ask about it, but bankruptcy alone rarely disqualifies a candidate. Ongoing delinquency is often viewed worse than a resolved bankruptcy.

Chapter 7 vs Chapter 13 — The Honest Comparison

There are two main types of personal bankruptcy — Chapter 7 and Chapter 13. They are fundamentally different in how they work, who qualifies, and what they accomplish. Choosing the wrong one is like taking the highway when you needed the side street — you’ll still get somewhere, but it won’t be where you needed to go.

Chapter 7 vs Chapter 13 — Side by Side

Chapter 7

Chapter 13

Nickname

“Liquidation” bankruptcy

“Reorganization” bankruptcy

How it works

Most unsecured debts discharged (eliminated) entirely

Debts restructured into 3–5 year repayment plan

Timeline

4–6 months

3–5 years

Income requirement

Must pass means test — income below state median

Must have regular income to fund repayment plan

Home protection

May lose home if equity exceeds state exemption

Can catch up on mortgage arrears and keep home

Credit report

Stays 10 years

Stays 7 years

Best for

Low income, mostly unsecured debt, no major assets to protect

Regular income, home to protect, secured debts to catch up on

Chapter 7 — The Fresh Start Option

Chapter 7 is the faster, cleaner option for people with limited income and mostly unsecured debt — credit cards, medical bills, personal loans, payday loans. The court appoints a trustee who reviews your assets. Most assets are protected by state exemptions. What isn’t protected may be liquidated to pay creditors — but as mentioned, the vast majority of Chapter 7 cases are no-asset cases.

The discharge at the end of a Chapter 7 eliminates your legal obligation to repay the listed debts — permanently. Creditors cannot continue to pursue you for discharged debts. Collection calls stop. Wage garnishments stop. The automatic stay — which kicks in the moment you file — stops all collection activity immediately. That automatic stay alone is sometimes worth the filing.

Chapter 13 — The Restructuring Option

Chapter 13 is for people who have regular income and assets worth protecting — particularly a home with equity, or a car that exceeds the Chapter 7 exemption. Instead of discharging debts, Chapter 13 creates a court-approved repayment plan over 3–5 years. You make monthly payments to a trustee who distributes them to creditors.

The key advantage of Chapter 13 is the ability to catch up on mortgage arrears and save your home from foreclosure — something Chapter 7 cannot do. It also allows you to keep non-exempt assets you would lose in Chapter 7. The trade-off is commitment — five years of court-supervised payments is a long time, and the plan must be funded by reliable income throughout.

What Bankruptcy Cannot Eliminate — The Important Exceptions

Bankruptcy is powerful — but it is not a magic wand. Certain debts survive bankruptcy and remain your legal obligation no matter what chapter you file. Knowing what stays is just as important as knowing what goes.

❌ Student Loans

Generally not dischargeable unless you can prove “undue hardship” — a very high legal bar. This is one of the most frustrating limitations of current bankruptcy law.

❌ Child Support & Alimony

Domestic support obligations survive bankruptcy entirely. Filing does not reduce or eliminate what you owe in child support or spousal support.

❌ Most Tax Debts

Recent tax debts — generally within the last 3 years — are not dischargeable. Older tax debts may qualify for discharge under specific conditions.

❌ Criminal Fines & Restitution

Debts arising from criminal activity — fines, penalties, restitution orders — survive bankruptcy and remain fully enforceable.

❌ Debts from Fraud

Debts incurred through fraud, false pretenses, or intentional misrepresentation are not dischargeable — a creditor can object to discharge on these grounds.

✅ What IS Dischargeable

Credit card debt, medical bills, personal loans, payday loans, utility bills, lease obligations, and most other unsecured consumer debts. This covers the majority of what drives most people to consider bankruptcy.

The 6 Signs Bankruptcy May Be the Right Answer for You

Nobody should file bankruptcy casually — but nobody should avoid it out of shame when it is genuinely the right answer. Here are six signs that bankruptcy deserves serious consideration rather than continued avoidance.

1

Your debt-to-income ratio makes repayment mathematically impossible

If your total unsecured debt exceeds your annual income — or if paying minimums alone consumes more than 50% of your take-home pay — the math does not work without intervention. This is not a budgeting problem. It is a structural problem that requires a structural solution.

2

Wage garnishment has started or a lawsuit has been filed

Filing bankruptcy triggers an automatic stay that immediately stops wage garnishments, lawsuits, foreclosures, and collection calls. If a creditor has already obtained a judgment against you, bankruptcy may be the fastest way to stop the financial bleeding.

3

You are using debt to pay debt

Taking out personal loans to pay credit cards. Cash advances to cover minimums. Payday loans to make it to next payday. If your debt is self-perpetuating — growing faster than you can pay it — the cycle cannot be broken by adding more debt to it.

4

Your credit is already severely damaged

If your score is already in the 500s from months of missed payments — the credit damage from bankruptcy is marginal compared to what has already happened. Meanwhile, the financial relief is substantial. Continuing to accumulate delinquencies while avoiding bankruptcy often produces worse long-term credit outcomes than filing.

5

Your home is at risk of foreclosure

Chapter 13 specifically allows you to catch up on mortgage arrears over time while keeping your home. If you are behind on your mortgage and have regular income, Chapter 13 may be the only legal mechanism available to stop foreclosure and restructure what you owe.

6

The stress is affecting your health and relationships

This one does not appear in most financial guides — but it belongs here. Chronic financial stress has documented health consequences. If debt is affecting your sleep, your relationships, your mental health, or your ability to function — the cost of continuing is not just financial. Bankruptcy is a legal tool. Sometimes it is also a health decision.

The First Three Steps If You Are Seriously Considering Bankruptcy

Deciding to research bankruptcy is not the same as deciding to file. Here are the three steps that give you the information you need to make that decision properly — without committing to anything yet.

1

Schedule a Free Consultation With a Bankruptcy Attorney

Most bankruptcy attorneys offer a free initial consultation — typically 30–60 minutes. This is not a commitment to file. It is a conversation where a professional reviews your specific situation and tells you honestly whether bankruptcy makes sense, which chapter applies, and what the process would look like for you. Use the U.S. Trustee Program’s attorney locator at justice.gov/ust to find a licensed bankruptcy attorney in your area.

2

Complete Credit Counselling From an Approved Provider

Federal law requires you to complete a credit counselling course from an approved provider within 180 days before filing bankruptcy. This is not optional — a case filed without it will be dismissed. The course typically costs $10–$50 and takes 60–90 minutes. The U.S. Trustee Program maintains a list of approved providers at justice.gov/ust. This step also ensures you have genuinely explored all alternatives before filing.

3

Gather Your Financial Documents Before You Do Anything Else

Whether you file or not, you need a complete picture of your financial situation. Pull your credit reports from all three bureaus. List every debt with the creditor name, balance, and account status. Document your monthly income and expenses. List all assets with approximate values. This exercise alone — putting everything on paper — often clarifies whether bankruptcy is necessary or whether another path is still viable.

U.S. Courts Data

95%

of Chapter 7 cases are “no-asset” — meaning filers keep everything they own

The image of bankruptcy as losing everything is largely a myth maintained by the people who benefit from you being too afraid to consider it. Most filers walk away with their possessions, their home, their car — and without their debt.

Source: United States Courts · uscourts.gov

Reader Story · Composite Account

“I Waited Two Years Too Long — And It Cost Me Everything I Was Trying to Protect”

Vincent, 51, spent two years avoiding bankruptcy out of shame — convinced that filing would mean he had failed. During those two years he drained his retirement savings trying to keep up with payments, took out three personal loans to cover credit card minimums, and watched his credit score fall from 620 to 498 anyway. When he finally consulted a bankruptcy attorney, he was told that the retirement savings — which would have been fully protected in bankruptcy — were now gone. He filed Chapter 7. The debts were discharged. But the retirement account he spent two years trying to protect by avoiding bankruptcy no longer existed.

His Mistake

Vincent used retirement savings — which are fully exempt from bankruptcy and cannot be touched by creditors — to pay debts that would have been discharged anyway. The shame of filing cost him his retirement cushion. Had he filed two years earlier, he would have emerged with his debts gone and his retirement account intact. Timing matters enormously in bankruptcy decisions.

What He Learned

After filing Chapter 7 Vincent began rebuilding immediately — secured card, credit-builder loan, consistent payments. Two years later his score had recovered to 641. He now tells anyone who will listen: consult a bankruptcy attorney before you touch your retirement savings. The consultation is free. The mistake of not having it is not.

RM

Attorney Rachel Morrow

Consumer Rights Attorney · Educational Illustration Only

“Retirement accounts — 401(k)s, IRAs, pension plans — are almost universally exempt from bankruptcy. Creditors cannot touch them before you file, and the trustee cannot touch them after you file. The person who drains their retirement account to pay debts that would have been discharged in bankruptcy has made one of the most costly financial mistakes possible. I see it regularly. It is always heartbreaking. And it is always avoidable with a single free consultation.”

Legal Analysis

Under the Bankruptcy Abuse Prevention and Consumer Protection Act and ERISA, qualified retirement accounts are fully exempt from the bankruptcy estate in most cases. This includes 401(k)s, 403(b)s, IRAs up to approximately $1.5 million, and most pension plans. Creditors cannot garnish these accounts before bankruptcy. Trustees cannot liquidate them after filing. They exist in a legally protected category specifically designed to ensure people have something to retire on regardless of financial hardship.

Bottom Line

Before withdrawing a single dollar from a retirement account to pay consumer debt — consult a bankruptcy attorney. The consultation is free. If bankruptcy is appropriate, your retirement savings are protected. If it is not appropriate, you will know that too — and you will make a better decision with that information than without it.

Reader Story · Based on Public Case Records

“Chapter 13 Saved My House. Nothing Else Would Have.”

Rosemary, 58, fell 14 months behind on her mortgage after a medical emergency wiped out her savings. Her lender had initiated foreclosure proceedings. She had tried loan modification — denied twice. She had tried refinancing — ineligible due to her credit score. A bankruptcy attorney explained that Chapter 13 would allow her to catch up on the 14 months of arrears over a 5-year repayment plan while continuing to make current mortgage payments. She filed. The foreclosure stopped immediately. Five years later she made her final plan payment — and owned her home outright.

What Made the Difference

Rosemary had exhausted every other option before consulting a bankruptcy attorney — and almost lost her home in the process. Chapter 13 was the only legal mechanism available to stop the foreclosure and restructure the arrears. Had she consulted an attorney six months earlier she would have had more options and less stress. The lesson: bankruptcy consultation should happen before you run out of alternatives, not after.

Her Outcome

Foreclosure stopped on the day of filing via automatic stay. 14 months of mortgage arrears restructured into the 5-year plan. Current mortgage payments maintained throughout. Plan completed successfully. Home retained. Chapter 13 notation fell off her credit report at year 7. She described it as “the most stressful and most correct decision I ever made.”

RM

Attorney Rachel Morrow

Consumer Rights Attorney · Educational Illustration Only

“Chapter 13 is the most underutilized tool in consumer bankruptcy law — because it is less well known than Chapter 7 and because the 3–5 year commitment sounds daunting. But for a homeowner facing foreclosure with regular income, it is frequently the only option that works. The automatic stay stops the foreclosure the moment the petition is filed. Not after a hearing. Not after a negotiation. Immediately. That is a powerful legal protection that no other tool provides.”

Legal Analysis

Under 11 U.S.C. § 362, the automatic stay takes effect immediately upon filing and prohibits creditors from taking any action to collect debts or enforce liens — including foreclosure proceedings. For homeowners, this is the most immediate legal protection available. The stay remains in effect throughout the bankruptcy case unless a creditor successfully petitions the court for relief from stay — which requires demonstrating cause and takes time, during which the debtor can use to cure arrears through the Chapter 13 plan.

Bottom Line

If you are behind on your mortgage and facing foreclosure — consult a bankruptcy attorney before your next court date. Chapter 13 may stop the foreclosure immediately and give you up to five years to catch up on arrears. This option disappears once the foreclosure is complete. Time is the critical variable. Act before the deadline, not after it.

Reader Story · Composite Account

“I Thought Bankruptcy Would Follow Me Forever. It Followed Me for Two Years.”

Tomás, 44, filed Chapter 7 after a divorce left him with $67,000 in joint debt and a single income. He was convinced his financial life was over. He opened a secured card six weeks after discharge, enrolled in a credit-builder loan at his credit union three months later, and paid both religiously. At month 18 post-discharge his score was 638. At month 24 he was approved for a car loan at 7.9% APR — a rate he described as “honestly better than I expected before I filed.” At year three he applied for a conventional mortgage pre-approval and received it.

His Fear vs Reality

Tomás believed bankruptcy would make him financially untouchable for a decade. The reality was that two years of consistent positive behavior after discharge produced a score and credit profile that opened mainstream financial products. The bankruptcy notation remained on his report — but lenders increasingly looked at what he had done since filing, not just the filing itself.

His Timeline

Month 0: Chapter 7 discharged. Month 1: secured card opened. Month 3: credit-builder loan enrolled. Month 18: score 638. Month 24: car loan approved at 7.9% APR. Month 36: mortgage pre-approval received. Year 10: Chapter 7 notation removed from credit report entirely. Life continued. Better than before, actually — because the $67,000 in debt that had been consuming his income was gone.

RM

Attorney Rachel Morrow

Consumer Rights Attorney · Educational Illustration Only

“The post-bankruptcy credit recovery timeline is significantly faster than most people expect — and significantly faster than the alternative of continued delinquency. A borrower who files Chapter 7 and immediately begins building positive history will almost always have a better credit profile at the two-year mark than a borrower who avoided bankruptcy and spent those same two years accumulating missed payments, collections, and judgments. The math is not close.”

Legal Analysis

Lenders assess post-bankruptcy applicants using a combination of factors — time since discharge, credit activity since discharge, current income stability, and debt-to-income ratio. Most mortgage programs have waiting periods of 2–4 years post-discharge for conventional loans and as little as 1–2 years for FHA loans. These timelines assume the borrower has actively rebuilt during the waiting period. The bankruptcy notation itself becomes less significant over time as new positive history accumulates on top of it.

Bottom Line

Bankruptcy is not the end of your financial life. For many people it is the beginning of a sustainable one. The discharge eliminates the debt that was making recovery impossible. What you do in the two years after discharge determines your financial future far more than the filing itself. Start rebuilding the day after discharge — not two years later. Every month of positive history counts from day one.

Frequently Asked Questions — Bankruptcy

All answers include citations from U.S. government sources · No shame, just facts

Q: How much does it cost to file for bankruptcy?

The court filing fee for Chapter 7 is currently $338 and for Chapter 13 is $313. Attorney fees vary significantly by location and complexity — typical Chapter 7 attorney fees range from $1,000 to $3,500, while Chapter 13 fees range from $3,000 to $6,000 due to the complexity of the repayment plan. If you cannot afford the filing fee, you can apply to pay in installments or request a fee waiver for Chapter 7 if your income is below 150% of the federal poverty guideline. Legal aid organizations in many areas provide free or low-cost bankruptcy assistance for qualifying individuals — contact your local legal aid office or visit lawhelp.org.

⚠ For educational purposes only. Not legal advice.

Q: Can I file bankruptcy without an attorney?

Yes — filing bankruptcy without an attorney is called filing “pro se” and it is legally permitted. However the U.S. Courts strongly caution that bankruptcy law is complex and mistakes can result in case dismissal, loss of assets, or denial of discharge. For Chapter 7 cases with straightforward finances and no significant assets, pro se filing is more manageable. Chapter 13 is significantly more complex and pro se filers have much lower plan confirmation rates. If cost is the barrier, explore legal aid organizations, law school bankruptcy clinics, and fee waiver applications before attempting pro se filing on a complex case.

⚠ For educational purposes only. Not legal advice.

Q: Will I lose my car or house if I file Chapter 7?

Not necessarily — and in most cases, no. Every state has bankruptcy exemptions that protect certain assets from liquidation. For your home, the homestead exemption protects equity up to a specified amount that varies by state — from $25,000 in some states to unlimited in Florida and Texas. For your car, the motor vehicle exemption typically protects $2,500 to $5,000 in equity. If your car is worth less than the exemption or you are current on payments and choose to reaffirm the debt, you keep it. Retirement accounts are almost universally fully protected. The U.S. Trustee Program website lists exemption amounts by state. Work with a bankruptcy attorney to understand exactly which assets are protected in your state before filing.

⚠ For educational purposes only. Not legal advice.

Q: How does bankruptcy affect my spouse if I file alone?

If you file individually, your spouse’s credit is generally not directly affected by your bankruptcy filing — the notation only appears on your credit report, not theirs. However, if you have joint debts, your discharge eliminates your obligation but not your spouse’s. Creditors can still pursue your spouse for the full balance of any joint account. In community property states — Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin — the rules are more complex and a bankruptcy attorney in your state should be consulted specifically about the community property implications before filing individually.

⚠ For educational purposes only. Not legal advice.

Q: How long after bankruptcy can I get a mortgage?

Waiting periods vary by loan type and bankruptcy chapter. For conventional loans after Chapter 7, the standard waiting period is 4 years from discharge — reduced to 2 years with extenuating circumstances. For FHA loans the waiting period is 2 years from Chapter 7 discharge. For VA loans it is also 2 years. For USDA loans it is 3 years. Chapter 13 has shorter waiting periods — as little as 1 year from the filing date for FHA and VA loans, with court permission. These waiting periods assume you have actively rebuilt credit during the period. The stronger your credit profile at the end of the waiting period, the better your mortgage terms will be.

⚠ For educational purposes only. Not legal advice.

Frequently Asked Questions — Bankruptcy

All answers include citations from U.S. government sources · No shame, just facts

Q: How much does it cost to file for bankruptcy?

The court filing fee for Chapter 7 is currently $338 and for Chapter 13 is $313. Attorney fees vary significantly by location and complexity — typical Chapter 7 attorney fees range from $1,000 to $3,500, while Chapter 13 fees range from $3,000 to $6,000 due to the complexity of the repayment plan. If you cannot afford the filing fee, you can apply to pay in installments or request a fee waiver for Chapter 7 if your income is below 150% of the federal poverty guideline. Legal aid organizations in many areas provide free or low-cost bankruptcy assistance for qualifying individuals — contact your local legal aid office or visit lawhelp.org.

⚠ For educational purposes only. Not legal advice.

Q: Can I file bankruptcy without an attorney?

Yes — filing bankruptcy without an attorney is called filing “pro se” and it is legally permitted. However the U.S. Courts strongly caution that bankruptcy law is complex and mistakes can result in case dismissal, loss of assets, or denial of discharge. For Chapter 7 cases with straightforward finances and no significant assets, pro se filing is more manageable. Chapter 13 is significantly more complex and pro se filers have much lower plan confirmation rates. If cost is the barrier, explore legal aid organizations, law school bankruptcy clinics, and fee waiver applications before attempting pro se filing on a complex case.

⚠ For educational purposes only. Not legal advice.

Q: Will I lose my car or house if I file Chapter 7?

Not necessarily — and in most cases, no. Every state has bankruptcy exemptions that protect certain assets from liquidation. For your home, the homestead exemption protects equity up to a specified amount that varies by state — from $25,000 in some states to unlimited in Florida and Texas. For your car, the motor vehicle exemption typically protects $2,500 to $5,000 in equity. If your car is worth less than the exemption or you are current on payments and choose to reaffirm the debt, you keep it. Retirement accounts are almost universally fully protected. The U.S. Trustee Program website lists exemption amounts by state. Work with a bankruptcy attorney to understand exactly which assets are protected in your state before filing.

⚠ For educational purposes only. Not legal advice.

Q: How does bankruptcy affect my spouse if I file alone?

If you file individually, your spouse’s credit is generally not directly affected by your bankruptcy filing — the notation only appears on your credit report, not theirs. However, if you have joint debts, your discharge eliminates your obligation but not your spouse’s. Creditors can still pursue your spouse for the full balance of any joint account. In community property states — Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin — the rules are more complex and a bankruptcy attorney in your state should be consulted specifically about the community property implications before filing individually.

⚠ For educational purposes only. Not legal advice.

Q: How long after bankruptcy can I get a mortgage?

Waiting periods vary by loan type and bankruptcy chapter. For conventional loans after Chapter 7, the standard waiting period is 4 years from discharge — reduced to 2 years with extenuating circumstances. For FHA loans the waiting period is 2 years from Chapter 7 discharge. For VA loans it is also 2 years. For USDA loans it is 3 years. Chapter 13 has shorter waiting periods — as little as 1 year from the filing date for FHA and VA loans, with court permission. These waiting periods assume you have actively rebuilt credit during the period. The stronger your credit profile at the end of the waiting period, the better your mortgage terms will be.

⚠ For educational purposes only. Not legal advice.

💬 Final Thoughts — Laxmi Hegde, MBA

I debated including this post in the series. Not because the information is wrong — everything here is accurate and government-sourced — but because bankruptcy carries so much emotional weight that I was not sure a blog post could do it justice. What convinced me to include it was Vincent’s story. Two years of shame cost him his retirement savings. That is not a cautionary tale about bankruptcy. That is a cautionary tale about what happens when people are too afraid to get information.

The stigma around bankruptcy is largely manufactured — and largely maintained by the financial industry that profits from people continuing to pay on debts they mathematically cannot resolve. The founders of this country put bankruptcy protection in the Constitution. Alexander Hamilton — the man on the ten dollar bill, musical star, and general financial overachiever — understood that economic life involves risk and that a functioning society needs a mechanism for people to recover from financial catastrophe. That mechanism exists. It is legal. It is used by hundreds of thousands of Americans every year. And it is nobody’s business but yours.

What I want you to take from today is simple: if you are in a debt situation that feels impossible, bankruptcy deserves a serious, informed, shame-free evaluation. Not a Google search at midnight followed by immediate tab closure. A real conversation with a licensed bankruptcy attorney — which costs nothing for the initial consultation and gives you information you genuinely cannot get anywhere else. You are allowed to know your options. All of them.

Tomorrow is Day 28 — the final post of Week 4 and the last stop before Week 5 closes the series. We cover something that ties the entire week together: how to know when you have genuinely turned the corner — the financial signals that tell you the hardship is behind you and the rebuilding is working. After 27 days of hard truths, Day 28 is the one that feels like breathing out. 😊

LH

Laxmi Hegde

MBA in Finance · ConfidenceBuildings.com

Borrower’s Truth Series · Day 27 of 30

🔬 Research Note & Primary Sources

This post is part of the ConfidenceBuildings.com 2026 Finance Research Project — a 30-episode series examining emergency borrowing, predatory lending practices, and consumer financial rights. All statistics and legal references are drawn from U.S. government sources and primary regulatory documents. No lender partnerships, affiliate relationships, or sponsored content of any kind has influenced this material. Yes, even the Hamilton reference was unsponsored. 😊

Updated as part of the ConfidenceBuildings.com 2026 Finance Research Project. This post is one of 30 deep-dive episodes examining emergency borrowing, predatory lending practices, and consumer financial rights in 2026. All legal references and statistics are drawn from U.S. government sources including the U.S. Courts, the U.S. Trustee Program, the Consumer Financial Protection Bureau, and the Federal Bankruptcy Code. No lender partnerships, affiliate relationships, or paid placements of any kind have influenced this content. Alexander Hamilton’s inclusion was entirely editorial. 😊

Information is current as of March 2026. Bankruptcy law, court filing fees, exemption amounts, and mortgage waiting periods change frequently — always verify current details directly with a licensed bankruptcy attorney and the U.S. Trustee Program before making any bankruptcy-related decision. Free initial consultations are widely available — use them.

Creditors negotiate every single day. With other creditors, with collection agencies, with attorneys. The one person they least expect to negotiate is you. That expectation is your advantage — if you know exactly what to say and when to say it.

40–60%

of the original balance is a typical settlement range on unsecured consumer debt

Source: CFPB

$0

cost to call your creditor and ask for a hardship plan or interest rate reduction

Source: CFPB

180

days past due — the typical point when creditors become most willing to negotiate settlements

Source: CFPB

What You’ll Learn Today

Why creditors negotiate — and what gives you leverage you didn’t know you had

The 4 types of negotiation and when to use each one

Word-for-word scripts for every negotiation scenario

What to never say in a creditor negotiation

How to get any agreement in writing before you pay a single dollar

⚠ For educational purposes only. Not legal or financial advice. The information on this page is intended to help consumers understand how creditor negotiation works. Negotiation outcomes vary significantly based on the type of debt, the creditor’s policies, your state’s laws, how long the debt has been delinquent, and your individual financial circumstances. Debt settlement can have significant tax implications — the IRS generally considers forgiven debt as taxable income. Settling a debt for less than the full balance may also negatively affect your credit score. Always consult a licensed nonprofit credit counsellor, certified financial planner, or consumer rights attorney before entering into any debt settlement agreement. The CFPB and FTC are referenced for informational purposes only — neither agency endorses this content.

Creditors negotiate every day — the one person they least expect is you

📚 Borrower’s Truth Series — Week 4 of 5

After You Borrow

Week 4 covers what happens after you sign — missed payments, debt spirals, collector calls, disputing errors, and rebuilding. Day 22 gave you the exit strategy. Day 23 stopped collector harassment. Day 24 fixed your credit report. Day 25 gave you the rebuilding roadmap. Today we cover the negotiation layer — how to talk directly to creditors and reduce what you owe before it ever reaches a collector.

Before You Negotiate — Know Exactly What Your Contract Says.

The strongest negotiating position starts with knowing your contract inside out. The Loan Clause Checklist identifies the exact clauses that affect your negotiation leverage — including acceleration clauses, default triggers, and prepayment terms. Knowing what your contract says before you call gives you an immediate advantage. Free. No email required.

Why It Matters Before You Negotiate

Acceleration clause — knowing if full balance is already due strengthens your case

Default definition — understanding exactly when you defaulted affects settlement leverage

Prepayment terms — affects lump sum settlement calculations

Arbitration clause — determines whether you can threaten legal action as leverage

Free resource · No sign-up required · Referenced throughout the Borrower’s Truth Series

📌 Quick Answer

Creditors negotiate because a partial payment is better than no payment — and they know it. Your leverage increases the longer a debt goes unpaid and the closer it gets to being written off or sold to a collections agency. The four negotiation types available to you are: hardship plans (reduced payments, no settlement), interest rate reductions (same balance, lower cost), lump sum settlements (pay less than owed, account closed), and pay-for-delete agreements (payment in exchange for credit report removal). Each requires a different approach, different timing, and different scripts — all of which are in today’s post.

Why Creditors Negotiate — And What Gives You Leverage

The most important thing to understand before any creditor negotiation is this: the creditor’s goal is to recover as much money as possible at the lowest possible cost. Your goal is to resolve the debt at the lowest possible amount. These goals are not incompatible — they are the foundation of every successful negotiation.

Creditors are acutely aware that an unpaid debt has a diminishing recovery value over time. The older the debt, the less they can sell it for to a collection agency. A debt that is 30 days past due might sell for 15 cents on the dollar. At 180 days past due, that same debt might sell for 4 cents on the dollar. At charge-off, the creditor may recover almost nothing.

This timeline is your leverage. You do not need to be wealthy to negotiate. You do not need an attorney. You need to understand the creditor’s incentive structure — and use it.

Your Negotiation Leverage — How It Changes Over Time

Current

0–30 days

Best time to request a hardship plan or interest rate reduction. Creditor still expects full repayment. Settlement unlikely but payment plan very achievable.

Early Default

60–90 days

Creditor begins internal collections. Good time to negotiate a structured payment plan with reduced interest. Settlement possible but typically 70–80 cents on the dollar.

Late Default

120–180 days

Creditor preparing to charge off or sell. Maximum settlement leverage. Lump sum settlements of 40–60 cents on the dollar most achievable at this stage.

Charge-Off

180+ days

Debt written off or sold to collector. Negotiate with collection agency — settlements of 25–50 cents on the dollar possible. Credit damage already occurred.

The 4 Types of Creditor Negotiation — And When to Use Each

Not all creditor negotiations are the same. The right approach depends on your situation — how long you have been delinquent, whether you have a lump sum available, and what outcome you need.

Type 1

Hardship Plan

A temporary reduction in your monthly payment — typically 6–12 months — while you stabilize your finances. The full balance remains. Interest may be reduced or paused. Best used when you are current or slightly behind and need immediate breathing room.

Best timing:Before you miss a payment or within 30 days of first missed payment

Type 2

Interest Rate Reduction

A permanent or temporary reduction in your interest rate — same balance, lower monthly cost, faster payoff. Credit card companies in particular have established hardship programs that include rate reductions. Most people never ask. Most companies say yes more often than you would expect.

Best timing:Any time — even when current. Long-term customers with good history have strongest leverage.

Type 3

Lump Sum Settlement

You offer to pay a percentage of the total balance — typically 40–60% — in a single payment in exchange for the creditor considering the account settled in full. Requires having a lump sum available. Most effective at 120–180 days past due when the creditor is preparing to charge off. Has credit score and potential tax implications.

Best timing:120–180 days past due — maximum leverage window before charge-off

Type 4

Pay-for-Delete Agreement

You offer payment in exchange for the creditor or collector removing the negative item from your credit report entirely. Not all creditors agree to this — original creditors are less likely than collection agencies. Must be negotiated before payment and confirmed in writing. If agreed, can produce significant score improvement alongside debt resolution.

Best timing:When negotiating with collection agencies — more flexible than original creditors on deletion

Word-for-Word Negotiation Scripts — Every Scenario

These scripts are designed to open negotiations from a position of knowledge without revealing information that weakens your position. Always call — do not email for initial negotiations. Written records come after you have a verbal agreement to confirm.

Script 1 — Requesting a Hardship Plan

📞 Word for Word

“Hi, I’m calling because I want to address my account proactively before I fall behind. I’ve recently experienced a financial hardship — [brief one sentence: job loss, medical issue, reduced income] — and I want to continue paying but I need temporary relief to do so responsibly. Do you have a hardship program that could reduce my minimum payment or pause interest for a period while I stabilize? I’d like to find a solution that keeps this account in good standing.”

Why this works

You are calling proactively — which signals good faith. You are not asking for forgiveness, you are asking for a tool to keep paying. Creditors respond far better to proactive contact than to customers who have already missed payments.

Script 2 — Requesting an Interest Rate Reduction

📞 Word for Word

“Hi, I’ve been a customer for [X years] and I’ve always paid on time. I’m calling because I’ve received offers from other lenders at significantly lower interest rates and I’d prefer to stay with you rather than transfer my balance. Is there anything you can do to reduce my current rate? I’m not looking to close the account — I’d just like to make sure I’m getting competitive terms given my payment history with you.”

Why this works

You are citing competition — which is the most effective lever for rate reductions. You are also signalling loyalty and the threat of leaving without being aggressive. Studies show this script produces a rate reduction in over 50% of calls when the account is in good standing.

Script 3 — Lump Sum Settlement Offer

📞 Word for Word

“I understand I owe [amount] on this account and I take that seriously. I’ve been going through significant financial hardship and I’m not in a position to pay the full balance. However, I’ve been able to set aside [your offer amount — start at 30–40%] and I’d like to offer that as a lump sum settlement to resolve this account in full. If we can agree on a settlement amount today, I can have payment to you within [3–5 business days]. Would you be able to work with me on this?”

Critical rules for this script

Always start lower than your maximum offer — leave room to negotiate up. Never reveal your maximum. Do not accept verbal agreements — require a written settlement letter before sending any payment. The letter must state the amount, that it settles the account in full, and that no further collection activity will occur.

Script 4 — Pay-for-Delete Negotiation

📞 Word for Word

“I’m prepared to resolve this account today with a payment of [amount]. Before I make any payment, I want to confirm that as part of this agreement, your agency will remove this account from all three credit bureau reports within 30 days of payment. I’d need that agreement in writing before I send anything. Is that something you’re able to offer?”

Important caveat

Not all collectors agree to pay-for-delete. If they decline, you can still negotiate the settlement amount without the deletion. Never pay without a written agreement first. If a collector verbally agrees but will not put it in writing — do not pay. The written agreement is the protection.

What to Never Say in a Creditor Negotiation

Every word in a negotiation either strengthens or weakens your position. These phrases are the ones that most commonly cost borrowers money they did not need to pay.

❌ “I can pay up to $X”

You just revealed your maximum. The negotiation ends there. Always give a range starting below your maximum — never your ceiling.

❌ “I just got my tax refund”

Never reveal that you have accessible money. Creditors will push for the full amount or a higher settlement if they know funds are available.

❌ “I’ll pay whatever it takes”

Signals desperation and eliminates all leverage. Creditors will hold firm at full balance or near-full settlement if they sense urgency.

❌ “I know I owe this”

Verbal acknowledgment can reset the statute of limitations in some states. Use “the account you are referencing” rather than “the debt I owe.”

❌ “I’ll pay today if you…”

Promising same-day payment removes your negotiation window. Always say “within 3–5 business days” to give yourself time to receive and review the written agreement.

❌ “My friend settled for 30%”

Every debt and creditor is different. Referencing third-party anecdotes weakens your credibility and does not help your negotiation.

The Golden Rule — Get Everything in Writing Before You Pay

A verbal agreement in a debt negotiation is worth nothing. Creditor representatives change. Call records get lost. Promises made in conversation disappear. The only agreement that protects you is a written settlement letter — received, reviewed, and confirmed before a single dollar is sent.

What Your Written Settlement Agreement Must Include

✓

Your full name and account number

✓

The exact settlement amount agreed upon

✓

A statement that the payment settles the account in full

✓

Confirmation that no further collection activity will occur after payment

✓

If pay-for-delete was agreed — specific language stating the item will be removed from all three bureau reports within 30 days

✓

Creditor’s name, address, and authorized representative’s signature

✓

Payment deadline — the date by which your payment must be received

⚠ Never send payment by wire transfer or prepaid debit card. Use a check or money order — these create a paper trail and give you 24–48 hours to stop payment if something changes.

CFPB Consumer Research Finding

57%

of consumers who contacted their creditor to discuss repayment options received some form of relief

More than half. The single most underused tool in consumer debt management is the phone call most people are too afraid to make.

Source: Consumer Financial Protection Bureau · consumerfinance.gov

Your negotiating leverage grows the longer a debt remains unpaid — timing is everything

📌 Quick Answer

Creditors negotiate because a partial payment is better than no payment. Your leverage increases the longer a debt goes unpaid — because the creditor’s likelihood of recovering anything decreases over time. The four negotiation types available to you are: hardship plans (reduced payments, no settlement), interest rate reductions (same balance, lower cost), fee waivers (remove late and penalty charges), and debt settlement (lump sum for less than full balance). Each requires a different script, a different timing, and a different approach — all of which are covered in today’s playbook.

Why Creditors Negotiate — And What Gives You More Leverage Than You Think

Most borrowers assume creditors hold all the power in a negotiation. That assumption is wrong — and creditors benefit from you believing it. The reality is that creditors negotiate constantly, and they do so because the alternative is worse for them.

When a debt goes delinquent, the creditor faces a choice — negotiate a recovery or write the debt off and sell it to a collection agency for 3–10 cents on the dollar. From the creditor’s perspective, recovering 50 cents on the dollar directly from you is dramatically better than selling it for 5 cents to a debt buyer. That math is your leverage — and it grows the longer the debt remains unpaid.

Understanding this dynamic changes everything about how you approach the conversation. You are not begging. You are presenting a business proposition to someone who has a financial incentive to say yes.

Your Negotiation Leverage — How It Changes Over Time

Current

0–30 days

Hardship plan — best option here

Account still current. Creditor wants to keep you paying. Ask for payment plan or interest reduction — settlement unlikely at this stage.

Early

30–90 days

Fee waivers and rate reductions — strong leverage

Creditor still managing internally. Late fees and penalty rates are negotiable. Many creditors have formal hardship programs at this stage.

Mid

90–180 days

Settlement discussions begin — leverage increasing

Creditor starting to assess write-off probability. Settlement offers of 60–70% of balance become realistic. This is the negotiation sweet spot for many accounts.

Late

180+ days

Maximum settlement leverage — 40–60% settlements common

Creditor facing imminent write-off and sale to debt buyer. Recovering 40–60 cents on the dollar directly is far better than 3–10 cents from a debt buyer. This is your strongest position for lump-sum settlement.

The 4 Types of Creditor Negotiation — And When to Use Each

Not all creditor negotiations are the same. The right approach depends entirely on your situation — how far behind you are, what you can realistically pay, and what outcome you need. Here are the four types in order of escalation.

Type 1

Hardship Plan Request

When to use: Account is current or 0–60 days late. You cannot make the minimum payment but want to avoid default.

What you get: Reduced minimum payment, temporarily waived fees, or a structured repayment plan — without settling for less than the full balance. Many major creditors have formal hardship programs that representatives are trained not to offer unless you ask.

Type 2

Interest Rate Reduction

When to use: Account is current. You are paying on time but the interest rate is making meaningful paydown impossible.

What you get: A temporary or permanent reduction in your interest rate — sometimes to 0% for a defined period. Credit card companies reduce rates for good-standing customers who ask far more often than most people realize. A single phone call has produced rate reductions from 24% to 9% for cardholders who asked.

Type 3

Fee Waiver Request

When to use: You have been charged late fees, penalty interest rates, or over-limit fees — particularly if this is a first or isolated occurrence.

What you get: Removal of specific fee charges and/or reversal of penalty interest rate to standard rate. Most creditors have a one-time courtesy waiver policy for customers with a history of on-time payments. This is the easiest negotiation of the four — and the one most people never attempt.

Type 4

Debt Settlement

When to use: Account is 90–180+ days delinquent. You have a lump sum available — or can access one — and need to resolve the debt for less than the full balance.

What you get: Agreement to accept less than the full balance as payment in full. Typically 40–60% of the original balance. Always get the agreement in writing before paying. Be aware that forgiven debt may be reported to the IRS as taxable income — consult a tax professional.

Word-for-Word Negotiation Scripts — Every Scenario Covered

Use these scripts exactly as written — or adapt them to your specific situation. The language is deliberately calm, specific, and non-confrontational. Creditor representatives respond better to borrowers who sound informed and solution-focused than to those who sound desperate or aggressive.

📞 Script 1 — Hardship Plan Request

“Hello, I am calling because I am experiencing a temporary financial hardship and I want to be proactive about my account before I miss a payment. I have been a customer for [X years] and I have a good payment history. I would like to ask about any hardship programs or temporary payment arrangements you may have available. I am committed to resolving this balance — I just need some temporary flexibility right now.”

If they say no: “I understand. Can you transfer me to your hardship or financial assistance department? I know many creditors have a dedicated team for situations like mine.” — Many front-line representatives are not trained on hardship programs. Escalate to a specialist.

📞 Script 2 — Interest Rate Reduction